Uncovering the Development of RWA's On-Chain National Debt Ecological Project

The starting point of all RWA protocols is to allow investors to conveniently convert between stablecoins and real-world assets, and the high liquidity and low risk of U.S. Treasury bonds naturally make them a relatively perfect choice. When the RWA Treasury bond platform successfully launches a widely used interest-bearing stablecoin, the DeFi Lego built upon it is highly anticipated.

The starting point of all RWA protocols is to allow investors to conveniently convert between stablecoins and real-world assets, and the high liquidity and low risk of U.S. Treasury bonds naturally make them a relatively perfect choice. When the RWA Treasury bond platform successfully launches a widely used interest-bearing stablecoin, the DeFi Lego built upon it is highly anticipated.Author: Flamie, DODO Research

Background

With changes in the macroeconomic environment, DeFi products are adapting and evolving. In DeFi 1.0, sustainable stablecoin yields were a pillar, but now the yields of low-risk instruments have fallen below those of traditional financial markets. As a result, traditional financial products have become more attractive due to their low-risk characteristics, leading to an interesting intertwining between traditional finance and DeFi.

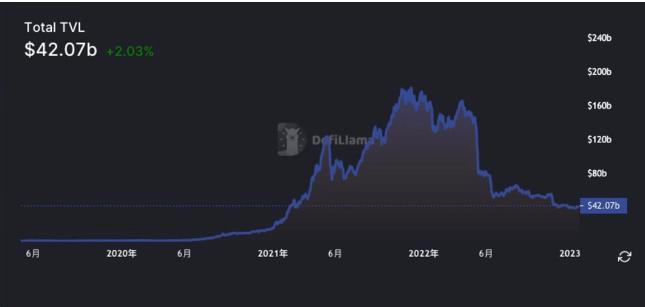

Data from Defillama shows that over the past year, affected by the significant decline in crypto assets, the total value locked in DeFi has dropped from a peak of over $180 billion to about $39 billion, a decline of over 78%, which is incomparable to the scale of traditional assets.

Source: https://defillama.com/

Source: https://defillama.com/

Before this, many projects had already begun to explore bringing real-world assets into DeFi. For example, JPMorgan, DBS Bank, and SBI Digital Asset Holdings have used the Aave protocol on Polygon to complete foreign exchange and government bond transactions on the Ethereum network. The banks tokenized Singapore government securities into Japanese government bonds, exchanging yen for Singapore dollars as a test.

Additionally, MakerDAO issued the world's first DeFi-based real asset loan, using the Fix&Flip loan pool New Silver on the Centrifuge protocol as the asset originator, obtaining the first loan using MakerDAO as a credit tool. Furthermore, in 2022, MakerDAO partnered with BlockTower Credit to launch a $220 million fund to finance real-world assets. In 2021, Aave collaborated with the crypto company Centrifuge to launch a real-world asset market RWA Market, allowing businesses to enable users to invest in markets collateralized by real-world assets.

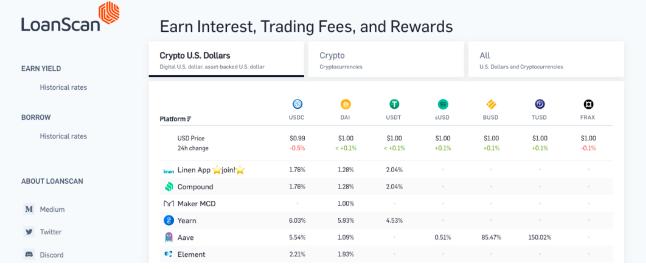

With the arrival of the crypto winter in 2022, as enticing APRs disappeared, people began to explore risk-free yields, and tokenized real-world assets are fundamentally changing wealth management and investment methods. As an important financing means and financial tool, bonds are low-risk safe-haven assets and fixed-income investment varieties, especially since U.S. Treasury rates are generally recognized as the risk-free rate in the market. However, the collapse of high-yield products like UST, which boasted 20% interest during the last bull market, has shaken investor confidence, and the yield performance in the high-return DeFi sector has also been unsatisfactory. For instance, in leading lending projects Compound and Aave, LoanScan data shows that as of May 8, the deposit rates for USDC on Compound and Aave have dropped to 1.76% and 5.54%, far below U.S. Treasury rates.

Source: https://linen.app/interest-rates/

Source: https://linen.app/interest-rates/

Let’s take a closer look at this branch of RWA—on-chain government bonds—and explore the development status of on-chain government bond ecological projects.

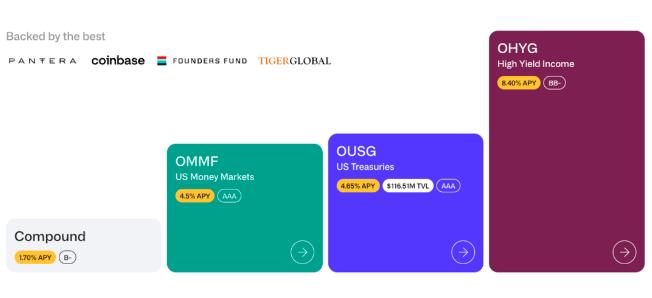

Ondo Finance

In January 2023, Ondo Finance announced the launch of tokenized funds, providing institutional investors with opportunities to invest in U.S. Treasury bonds and investment-grade bonds.

It is understood that Ondo Finance has launched three tokenized U.S. Treasury and bond products through large, highly liquid ETFs managed by institutional giants such as BlackRock and Pacific Investment Management Company (PIMCO): the U.S. Government Bond Fund (OUSG), Short-Term Investment Grade Bond Fund (OSTB), and High-Yield Corporate Bond Fund (OHYG).

Among them, OUSG is pegged to a stablecoin and is collateralized by short-term U.S. Treasury bonds, initially through the BlackRock U.S. Short-Term Treasury ETF (SHV), with an expected yield of 4.65%; OSTB will invest in short-term investment-grade corporate bonds, initially through PIMCO Enhanced Short Maturity Active ETF (MINT), with a yield of 5.45%; OHYG will invest in high-yield corporate bonds, initially through BlackRock iBoxx High Yield Corporate Bond (HYG), with a yield of 8.02%. Bond investors can transfer the net asset value of the tokenized fund on-chain through smart contracts, and Ondo Finance will charge an annual management fee of 0.15%.

Source: https://ondo.finance/ousg

Source: https://ondo.finance/ousg

In light of the failures of unregulated companies in the crypto space in 2022, Ondo Finance has chosen to collaborate with strictly regulated third-party service providers and hold assets in bankruptcy-remote qualified custodians. Among them, Clear Street, which provides a wholesale brokerage platform for institutional investors, is the primary broker for the fund and will custody the fund's securities in DTC (Depository Trust Company) accounts; Coinbase Custody will hold any stablecoins held by the fund, with Coinbase Prime handling the conversion between stablecoins and fiat; accounting and consulting firm Richey May will serve as the fund's tax advisor and auditor, having been repeatedly recognized as one of the best companies by Inside Public Accounting.

However, for compliance reasons, Ondo Finance will implement a whitelist system, requiring investors to pass KYC and AML screenings before signing subscription documents, with stablecoins or U.S. dollars being acceptable. The SEC defines "qualified purchasers" as individuals or entities investing at least $5 million.

Matrixdock

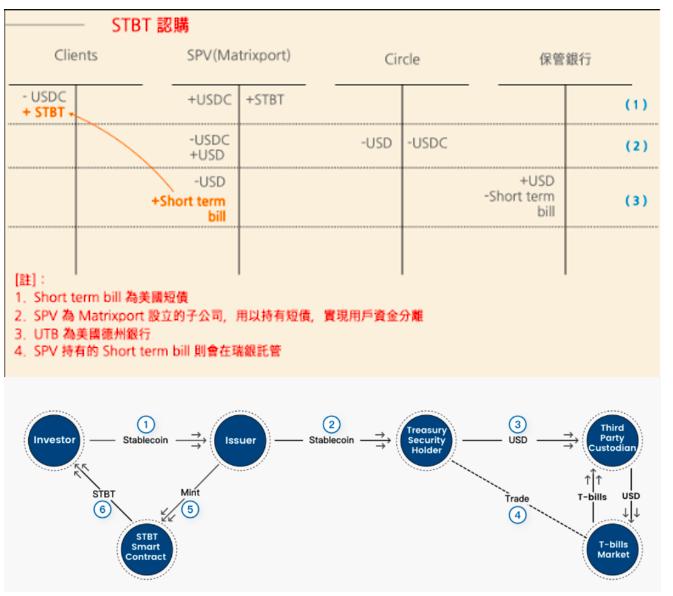

Matrixdock is an on-chain government bond platform launched by the Singapore asset management platform Matrixport. STBT is the first product of Matrixdock, introducing a risk-free rate based on U.S. Treasury bonds.

At issuance, 1 STBT will trade at the price of 1 USDC. The underlying assets of STBT are 6-month U.S. Treasury bonds and reverse repurchase agreements collateralized by U.S. Treasury bonds. STBT is an ERC-1400 standard token issued on the Ethereum chain, which is issued and redeemed by Matrixdock, with a contract whitelist mechanism restricting transfers and trades only among authorized account holders on Matrixdock.

The mechanism of STBT is as follows:

Investors hand over USDC or USDT to the issuer, who mints the corresponding STBT through a smart contract;

The STBT issuer exchanges USDC for fiat currency through Circle;

The fiat currency is held by a third-party custodian, which purchases short-term bonds maturing within six months through traditional financial institutions' U.S. Treasury trading accounts or invests in the Federal Reserve's overnight reverse repurchase market;

STBT holders can transfer STBT back to their wallet addresses, such as cold wallets or third-party custodial platforms, after minting;

The smart contract of STBT will automatically allocate the interest from bonds or reverse repos daily to the holding addresses through a Rebase mechanism, based on the number of STBT;

As shown in the diagram below, the final result of the transaction will be that the reserves of STBT will consist of U.S. government short-term bonds (orange).

Source: https://github.com/Matrixdock-STBT/STBT-contracts/blob/main/whitepaper/STBT White Paper.pdf

Source: https://github.com/Matrixdock-STBT/STBT-contracts/blob/main/whitepaper/STBT White Paper.pdf

After the minting application is submitted, Matrixdock will mint and issue the corresponding amount of STBT according to a T+3 settlement cycle, and the tokens will be distributed within a maximum of 4 New York banking days. After a redemption application is submitted, Matrixdock will promptly redeem STBT tokens through the following process: deducting STBT tokens from your account, halting the circulation of those STBT tokens or "burning" them, and transferring a digital asset principal equivalent to the value of your STBT tokens (at a rate of 1 U.S. dollar per STBT token at redemption) to your account, minus any related fees, reflecting any trading losses that correspond to the value of the underlying assets at the time of redemption, and any trading losses and/or trading costs deemed necessary by related entities to effectuate the redemption.

It is worth noting that the STBT issuer is a special purpose vehicle (SPV) established by Matrixport. The SPV will pledge the U.S. Treasury bonds and cash it holds to STBT holders, who will have first priority in the repayment of the underlying asset pool. Even in the most extreme cases, such as Matrixport's bankruptcy, the value of STBT is still guaranteed by the asset pool, and corresponding assets can still be redeemed after liquidating these securities.

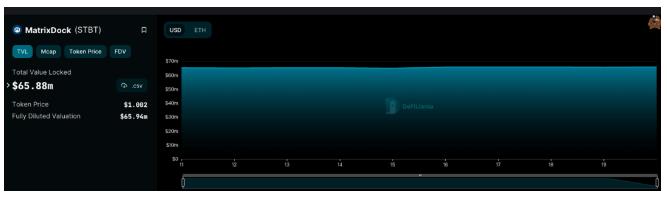

Data from Defillama shows that the current circulation of STBT is 65.88 million.

TProtocol

TProtocol is also a new on-chain government bond protocol, which is a fork of the stablecoin protocol Liquity, using Matrixdock as its underlying. TProtocol introduces three tokens: TBT, sTBT, and wTBT:

sTBT: Issued by Matrixdock, with a Rebase occurring every working day at 6 PM (Hong Kong time), maintaining a price of 1 U.S. dollar. Only high-net-worth individuals or institutions that have undergone KYC can purchase.

TBT: A permissionless Rebase token that allows retail investors to mint, fully corresponding to sTBT. Users can mint using USDC, with a price always at 1 U.S. dollar (excluding fees). Users can redeem TBT for USDC, with the redemption price always at 1 U.S. dollar.

wTBT: An interest-bearing token, a wrapped version of TBT that can be exchanged for TBT. The purpose is to allow TProtocol to integrate into existing DeFi protocols, as most DeFi protocols do not support Rebase tokens.

Additionally, the minting fee for TBT is 0.1%, and the redemption fee for TBT is 0.3%. The APR for TBT can be calculated using a formula. TProtocol emphasizes asset transparency. The value of TBT and wTBT is supported by three types of assets: MCsTBT, IDLEFUND, and PENDING_sTBT.

TBT can be traded on decentralized exchanges, and TProtocol will launch a liquidity pool on Curve Finance to ensure minimal slippage. TProtocol also allows users to stake TBT-3CRV LP to earn esTPS rewards, incentivizing DeFi users to utilize the TProtocol protocol and TBT, significantly enhancing TBT's liquidity and ensuring low trading costs when exchanging TBT.

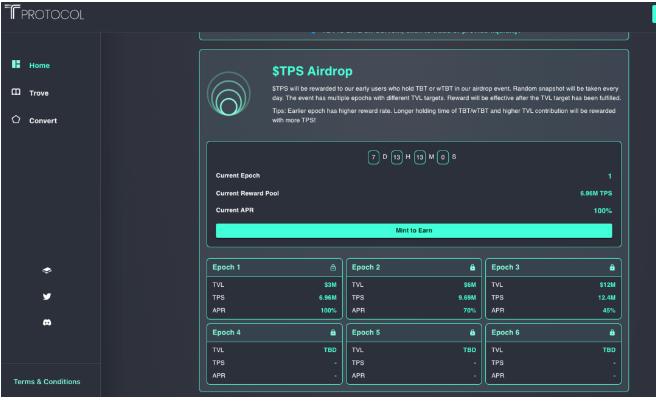

Currently, TProtocol has just launched on the Ethereum mainnet, allowing users to mint wTBT 1:1 with USDC to participate in early airdrop incentives, with corresponding TPS tokens awarded as incentives for early participation in each Epoch. Additionally, TProtocol has launched on Velodrome on Optimism, where users providing liquidity can earn government bond yields while also receiving Bribe rewards.

Source: https://app.tprotocol.io/

Source: https://app.tprotocol.io/

OpenEden

OpenEden is a crypto startup founded in early 2022 by Jeremy Ng, former head of Asia-Pacific at Gemini, and Eugene Ng, head of business development.

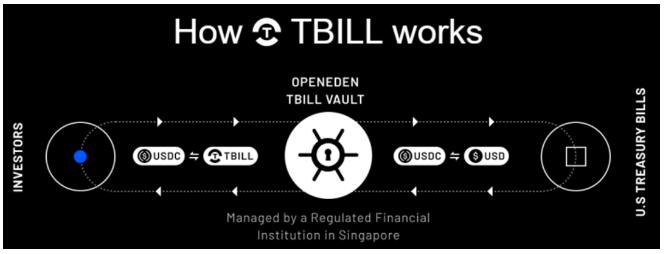

The OpenEden T-Bill treasury is an on-chain pool that allows stablecoin holders to earn yields from U.S. Treasury bills, currently yielding about 4.86%. Most of the assets in this pool will be directly invested in short-term U.S. Treasury bonds, while a small portion of USDC will remain on-chain for 24/7 instant withdrawals. Users can mint TBILL tokens from USDC in their wallets to enter the treasury and earn yields, with redemptions also occurring on-chain, benefiting from the instant settlement of blockchain technology, unlike traditional finance, which requires a process of 1 to 2 working days.

Source: https://openeden.com/#how-tbill-works

Source: https://openeden.com/#how-tbill-works

Ribbon Finance

Ribbon Finance announced on April 17 the launch of a principal-protected options product based on government bonds, Ribbon Earn USDC (V2), in collaboration with another RWA protocol, BackedFi, with a yield of about 2%, lower than other tokenized government bond products.

According to the documentation, Ribbon Earn USDC V2 is an all-weather product that generates yields by purchasing Backed IB01 $ Treasury Bond 0-1yr tokens backed by BlackRock certificates. As of April 10, its average expected yield was 4.64%, which is enhanced by purchasing ETH's exotic options to gain exposure to market short-term volatility, thereby increasing yields. Depositors can benefit from the upside of the cryptocurrency market while keeping their principal protected.

Source: https://www.research.ribbon.finance/blog/ribbon-earn-v2-is-live

Source: https://www.research.ribbon.finance/blog/ribbon-earn-v2-is-live

Conclusion

Currently, apart from TProtocol, which is truly a permissionless protocol for users, the other projects require KYC. Moreover, the vast majority of government bond tokens do not support transfer functions, thus limiting their use cases, such as the composability of DeFi, not to mention full-chain circulation. Additionally, another core aspect of on-chain government bonds is the qualifications of the cooperating government bond acceptors, which pose significant and opaque counterparty risks, smart contract risks, and oracle risks, as well as the widely criticized centralized characteristics of CeDeFi.

At present, all RWA protocols aim to allow investors to conveniently convert stablecoins into real-world assets, with the high liquidity and low risk of U.S. Treasury bonds naturally becoming a relatively perfect choice. When an RWA government bond platform successfully creates a widely used interest-bearing stablecoin, the DeFi Lego built from it is highly anticipated. For example, a Layer 1 blockchain created based on the RWA platform, but the accompanying regulatory issues may also be unavoidable. References https://www.binance.com/en-IN/feed/post/121124

Risk warning

Risk warning Risk warning

Risk warning