Wang Chuan: Why can't people hold onto their assets that have tripled in four years?

After Blackrock, the largest asset management group in the United States, officially applied for a Bitcoin ETF with the U.S. Securities and Exchange Commission on June 15, 2023, the price of BTC has approached $31,000.

After Blackrock, the largest asset management group in the United States, officially applied for a Bitcoin ETF with the U.S. Securities and Exchange Commission on June 15, 2023, the price of BTC has approached $31,000.Source: investguru

Author: Wang Chuan from Silicon Valley

After the largest asset management group in the United States, Blackrock, officially applied for a Bitcoin ETF to the SEC on June 15, 2023, the price of BTC has approached $31,000. This scene reminds one of June 2019, when the BTC price returned to $10,000. A threefold increase in four years is not too bad. It should easily outperform 99.9% of fund managers during the same period.

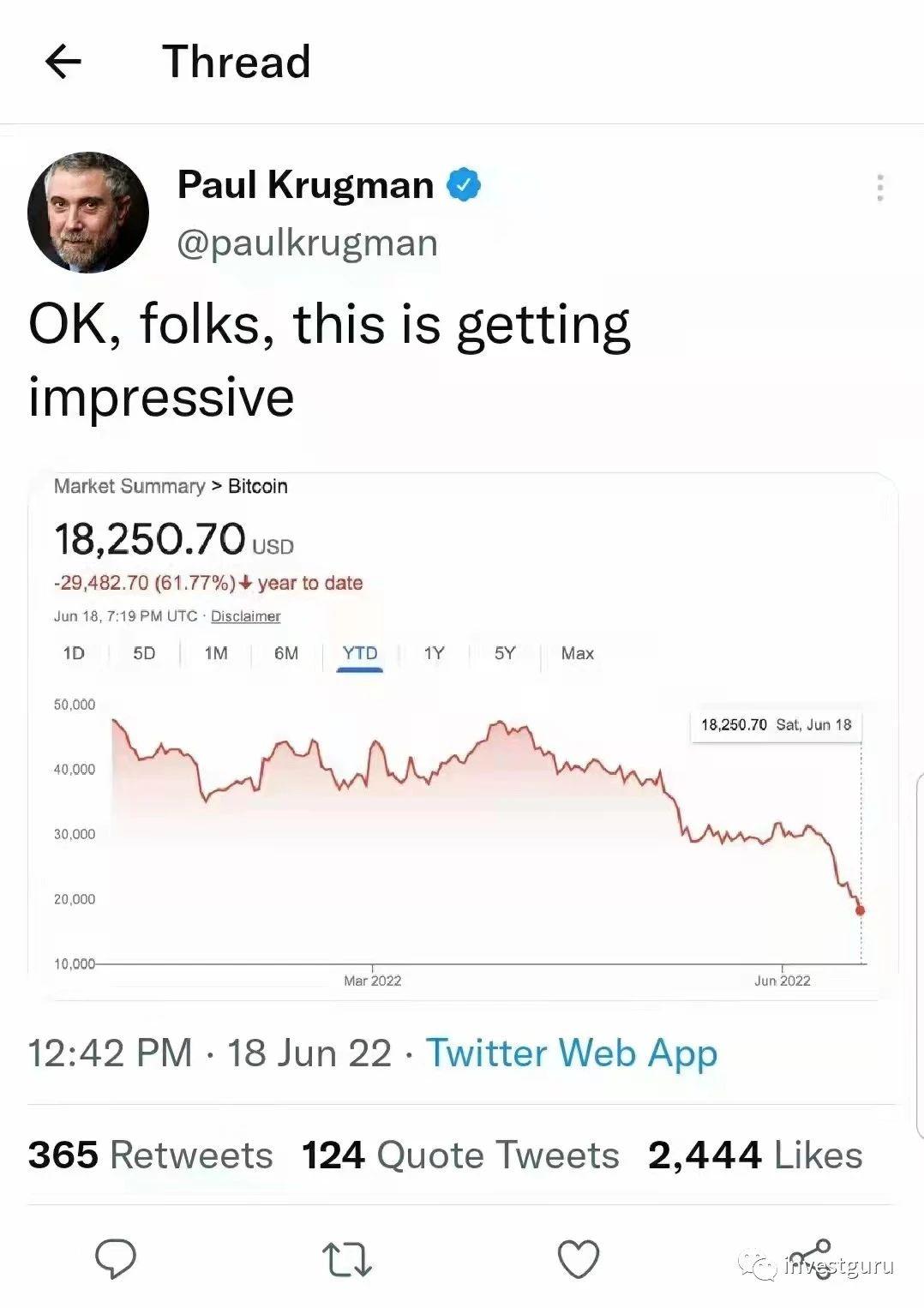

On June 18, 2022, the price of BTC once dropped to $18,250. The famous economist and Nobel laureate Paul Krugman timely jumped onto Twitter, gleefully saying, "Folks, this is so touching" (he had also commented back in late 2018 when Bitcoin fell to $3,000). A year after Krugman's statement, Bitcoin rose by 69%. Indeed, it was very touching.

However, many early entrants in the industry no longer hold much BTC. The reason is simple: most people seek higher short-term returns and adopt various subjective and flashy strategies, but essentially, they are just gambling with leverage, leaving no room for themselves. Sooner or later, they will be forced to cut losses and close positions amid the inevitable but unpredictable large fluctuations in the market.

There were institutional funds that nearly faced liquidation during the crash in March 2020 but continued to gamble heavily, later earning even more, thus persisting with this aggressive strategy. Consequently, during the significant drop in June 2022, they were inevitably wiped out.

Players lacking redundancy may quickly encounter a chain reaction when impacted by an unpredictable event, where the collapse of one subsystem leads to a cascading failure of higher-level systems, escalating into a massive disaster in a short time, potentially resulting in the complete destruction of the entire system. However, after such extinction, the experiences and lessons of these individuals are difficult to pass on to future generations, inevitably leading to the next wave of oblivious newcomers repeating their experiences.

Many people cannot bear the price volatility of BTC, but this volatility actually reflects more the changes in the growth and contraction of dollar credit. The Federal Reserve itself cannot accurately predict changes in inflation and employment, let alone forecast adjustments to its monetary policy. It is impossible for everything in the world to be "both… and." It is not possible to "have small price pullbacks when the market is bad and good returns when the market rises," nor is it possible to "have the horse run and not let it eat grass." If a client makes such demands, leave them; they will eventually fall into the arms of scammers like Madoff. If a boss makes such demands, they just want to take credit when things go well and scapegoat you when problems arise.

People often mistake things that have temporary premiums due to short-term constraints for scarce assets. After the outbreak of the Russia-Ukraine war, the spot price of crude oil was once driven up to $120 a barrel. Upon calm reflection, one realizes that high oil prices will suppress demand while increasing extraction activities and supply, and crude oil prices will eventually come down. But no matter how many new mining machines you buy to mine, the supply of BTC will not increase; it will still halve every four years on schedule, which is a fundamental difference between it and commodities/precious metals.

In March 2023, when Silicon Valley Bank was on the verge of collapse and hundreds of billions in depositor funds faced significant risks of being sheared, the Federal Reserve decisively intervened, magically conjuring up hundreds of billions in emergency loans to save the depositors. BTC, however, remained indifferent, still quietly producing a block every ten minutes and adjusting its difficulty every two weeks. It was at this moment that people suddenly realized what a truly scarce asset is and what is merely a game that can be arbitrarily inflated by a few individuals.

As long as one firmly grasps scarce resources, there is no need to care about how others compete; let them squander the truly scarce resources to exchange and compete for the factually non-scarce resources.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles