A Brief Analysis of the 10 Major Web3 Applications That Continue to Frenziedly "Suck Up" Capital in a Bear Market

In the constantly evolving DeFi ecosystem, these projects play a key role in driving continuous innovation and development in the blockchain and cryptocurrency space.

In the constantly evolving DeFi ecosystem, these projects play a key role in driving continuous innovation and development in the blockchain and cryptocurrency space.Author: Huo Huo, Plain Language Blockchain

After experiencing high prices in 2021, the crypto space has seen a significant cooling down this year. Of course, with fortune comes misfortune; in this calm state, crypto infrastructure can actually settle and develop, such as those DeFi protocols with strong revenue, real demand, and positive returns. Looking at the overall market, there is a trend of shifting from "fat protocols and thin applications" to "fat applications."

What are fat and thin protocols and applications? This is because the early internet resembled a "thin protocol network," composed of less noticeable elements like TCP, IP, and HTTP, which form the foundation of the internet, while the value of these protocols is captured by application software, i.e., apps. For example, the apps we use now, like Douyin, WeChat, and Meituan, are "thin protocols and fat applications."

However, on the basis of blockchain decentralization, value is concentrated at the shared protocol layer, with only a small portion of value distributed at the application layer, hence it is referred to as a stack of "fat" protocols and "thin" applications.

Today, we will continue to organize this topic and take a look at the top ten most profitable protocols in the DeFi space.

Source: Defillama September 9 data

01 Lido

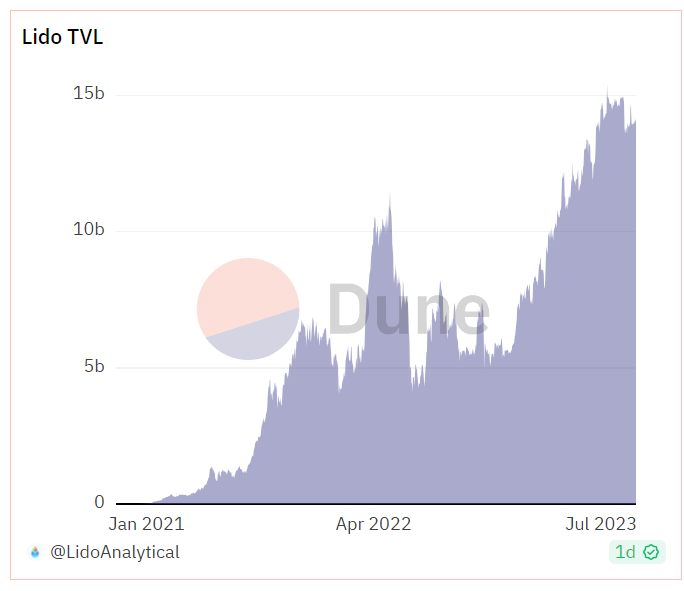

Lido is currently the largest staking protocol in the market, established in 2020, primarily providing liquid staking solutions for ETH and other PoS blockchains.

After users deposit PoS assets into Lido, their tokens will be staked on the PoS blockchain through the Lido protocol. Users can earn staking rewards while also utilizing the staked tokens to obtain tokenized assets for further earnings.

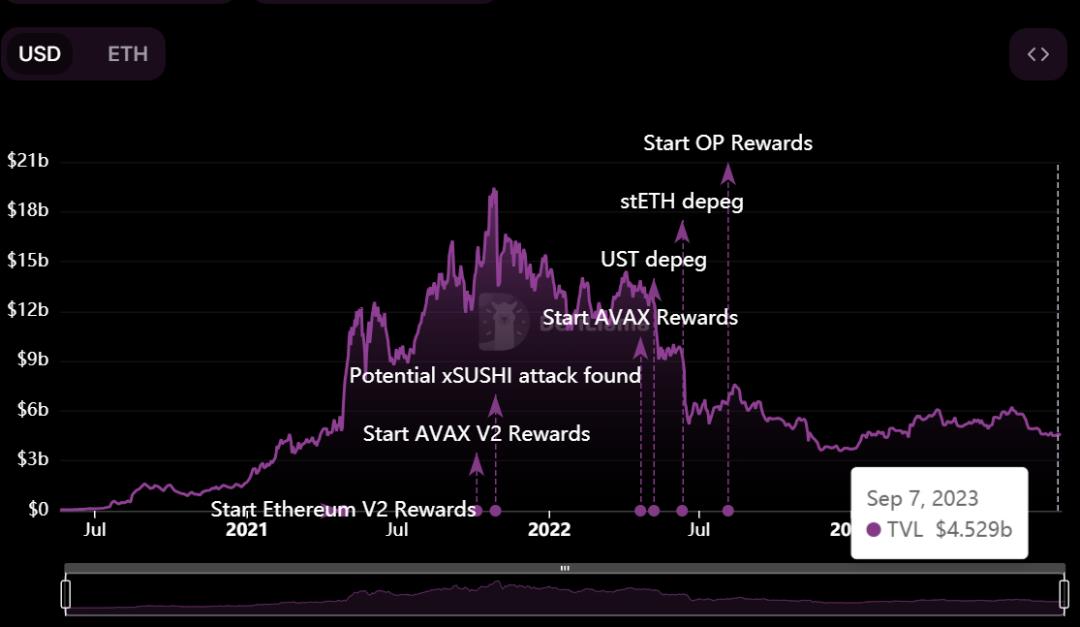

Since the beginning of this year, Lido's TVL has been on the rise. Why has Lido developed into the largest staking protocol in the market, with the highest TVL among DeFi protocols, occupying 32.5% of the staking space, almost four times that of the second-place Coinbase, with nearly $14.2 billion in TVL? The main reasons are as follows:

1) First-mover advantage, user-friendly for newcomers:

Since the launch of the ETH 2.0 contract in December 2020, many ordinary users have been reluctant to lock up 32 ETH directly. At that time, PoS and PoW had not yet merged, and ETH could only flow one way from the PoW chain to the PoS chain, losing liquidity as it could not be retrieved. In this context, Lido emerged. Therefore, the project itself was born to address the staking issues during Ethereum's transition period, allowing Lido to quickly become the first choice for ordinary users participating in ETH 2.0 staking, leading to significant growth.

2) Support for multiple mainstream public chains:

Including Solana (SOL), Polygon (MATIC), Polkadot (DOT), and Kusama (KSM), with a strong ecosystem. Due to its large user base and investment portfolio, Lido has the highest liquidity compared to other platforms, creating a Matthew effect. Especially after the Ethereum Shanghai upgrade, Lido's network effect with stETH has become even more pronounced.

Currently, Lido's revenue model mainly relies on taking a 10% cut from staking rewards as income, with 5% going to staking node operators and another 5% entering the Lido treasury for governance.

According to relevant news, despite activating the feature to withdraw staked ETH earlier this year, the protocol still sees a significant net inflow of ETH deposits each month. The July report from Ethereum staking protocol Lido shows that the total value locked (TVL) has exceeded $15 billion for the first time since May 2022, and it is expected that the staked ETH in September may exceed 8 million. Following this development trend, Lido is likely to maintain its advantage and achieve a doubling of profits in the medium to short term.

02 MakerDAO

MakerDAO is a decentralized autonomous organization on the Ethereum blockchain, dedicated to promoting the development of cryptocurrency collateralization. Founded in 2015, it is the longest-running project on the Ethereum blockchain, currently ranking second in TVL, at about $5 billion.

MakerDAO consists of the DAI stablecoin pegged to the US dollar and the Maker protocol based on Ethereum smart contracts (a dApp on the Ethereum blockchain), with DAI built on the Maker protocol and launched in 2017.

As the first DAO organization established on Ethereum, DAI currently holds the NO.1 position in the application scale of decentralized stablecoins, and MakerDAO has also made significant contributions in the DeFi space. MakerDAO's over-collateralization mechanism eliminates the risk of "printing money out of thin air" and operates entirely on-chain, representing a breakthrough in solving centralized custody risks.

MakerDAO's current sources of income come from three aspects:

1) Stability fee income from over-collateralized vaults

2) Liquidation penalty income from liquidation vaults

3) Stablecoin exchange transaction fees

Before 2022, the stability fees and liquidation fees collected from the ETH-Assets vault on MakerDAO were the largest source of income each month. However, with the gradual increase in investments in RWA (real-world assets), it is evident that the current reliance on RWA for profitability is significant, with profits accounting for as much as 56.4%. This shows that RWA currently contributes the most to the protocol's income.

03 AAVE

Aave is also a cryptocurrency collateralization protocol, originally called ETHLend, created in Switzerland in 2017 to allow people to collateralize cryptocurrencies and RWAs without centralized intermediaries. Initially built on the Ethereum network, all tokens on the network also use the Ethereum blockchain for transaction processing. Aave has since expanded to other blockchain networks, including Avalanche, Fantom, and Harmony.

Users can deposit various crypto assets into AAVE's smart contracts, forming a "deposit pool," which can be used to provide collateralization services to other users. Borrowers need to provide collateral to ensure the safety of the loan, while depositors can earn interest on their deposited assets.

The AAVE token plays an important role in the protocol, used for governance and fee payments. AAVE's advantages include support for multiple crypto assets and high liquidity, but it also comes with risks, as both collateralization and borrowing are affected by price fluctuations in the crypto market.

The revenue model is similar to that of MakerDAO; Aave generates income by charging various fees on its platform. These revenues are then deposited into the Aave community treasury, where AAVE token holders have the right to decide how to use these funds.

Specifically, some ways Aave charges fees include:

1) Borrowing fees: Fees charged to borrowers on the platform, typically ranging from 0.01% to 25%, depending on the borrowed asset, loan-to-value ratio, and loan term;

2) Flash loan fees: Fees charged to users utilizing the platform's "flash loan" feature, allowing them to borrow funds without collateral for a short period. The fee is usually 0.09% of the borrowed amount;

3) Other feature fees: In V3, Aave will offer additional fees for features such as liquidation, instant liquidity, and portal bridges;

Currently, AAVE's TVL is approximately $4.5 billion, maintaining a trend consistent with the overall market.

04 Justland

JustLend is a decentralized collateralization protocol based on TRON, launched in the third quarter of 2020 by Sun Yuchen. Its name is derived from the first four letters of the founder's name.

JUSTLend features various DeFi solutions, including JustStable, JustLend, JustSwap, JustLink, and cross-chain tokens, forming an algorithmic asset pool that allows users to earn interest on different asset classes. Users can generate returns by providing assets, obtain digital assets through collateralization, and stake TRX on the TRON blockchain.

The core DeFi product of the network is JustStable, supported by USDJ pegged to the US dollar, and JustStable serves as a cross-border stablecoin collateralization platform where users can borrow stablecoins by providing collateral.

JUSTLend's current revenue model mainly includes:

1) Interest rate differential: The platform earns profits from the difference between the high interest charged to borrowers and the low interest paid to depositors;

2) Collateralization fees: The platform may charge certain fees from borrowers;

3) Platform token appreciation: If there is a platform token, its value may increase by encouraging users to use the token to pay fees or receive discounts.

JUSTLend is growing rapidly due to its generous collateralization market deposit APY rewards, sometimes reaching as high as 30%. Its project advantage lies in its backing by the TRON ecosystem, which has attracted a large user base and resources. Therefore, despite the current market downturn, its TVL has increased, currently around $3.6 billion, ranking fourth.

05 Uniswap

Uniswap is a DEX created in 2018, built on Ethereum. The idea was initially proposed by Ethereum co-founder Vitalik Buterin and founded by former Siemens mechanical engineer Hayden Adams. To date, the technology behind Uniswap has undergone multiple iterations. It has now evolved to Uniswap v3, one of the most notable changes being improved capital efficiency and enhanced market liquidity.

As an automated liquidity protocol, Uniswap's trading does not require any order books or centralized participants, meaning it allows users to trade directly without intermediaries, bringing a high degree of decentralization and censorship resistance to the market, making it a leading project in the DEX space.

Currently, Uniswap's TVL is approximately $3.3 billion, but due to the protocol's decentralization, the creators of Uniswap do not take a cut from any transactions conducted on the protocol. Liquidity providers on Uniswap control the trades and charge fees for their services.

Currently, Uniswap's TVL is about $3.3 billion, and its overall performance aligns with the current market environment, peaking during the bear market in 2021 at over $20 billion.

Source: Coingecko

Uniswap adopts different fee structures for its V3 pools, with rates of 0.01%, 0.05%, 0.3%, and 1%. However, for V2 pools, a standard fee rate of 0.3% is applied. These fees are automatically added to the liquidity pool, but liquidity providers can redeem them at any time. Transaction fees are distributed based on the liquidity provider's share in the pool, with a portion of the fees used for Uniswap's development iterations.

V2 liquidity pool operational structure

06 Curve Finance

Curve Finance is an automated market maker protocol launched in January 2020, aimed at providing a DEX built on an AMM architecture, primarily focusing on mainstream stablecoins, synthetic assets, and derivatives. It currently operates mainly on Ethereum and has multi-chain deployments on Fantom, Polygon, Avalanche, Arbitrum, and Optimism.

On Ethereum, Curve is one of the hottest AMMs operating. It facilitates low-fee and low-slippage exchanges between stablecoins in a non-custodial manner and serves as a decentralized liquidity aggregator, allowing anyone to add their assets to several different liquidity pools and earn fees.

Curve's fees range between 0.04% and 0.4%. These fees are shared between liquidity providers and veCRV holders. Its main revenue models include:

1) Transaction fees: Curve charges a certain percentage of fees from users' transactions;

2) Collateralization and stablecoin exchange: Curve provides collateralization and stablecoin exchange services, earning certain fees from these activities;

3) Synthetic asset trading: Supporting synthetic asset trading attracts more liquidity and generates revenue.

Curve Finance holds a core position in the DeFi space. In August 2020, it created Curve DAO and issued its native token CRV, after which the protocol's TVL began to rise steadily, once becoming the largest DEX by TVL. After experiencing over a year of turmoil in the crypto world, especially following the re-entry vulnerability incident in August, the protocol's current locked TVL remains among the top in various DeFi protocols, at over $2.2 billion. One reason, aside from its popular liquidity pools, is that other blockchain protocols highly rely on it for various decentralized applications.

07 SummerFi

SummerFi was formerly known as Oasis, originating from MakerDAO, established in 2016, even earlier than the stablecoin DAI launched in 2017. OasisDEX was the first DEX deployed by MakerDAO on Ethereum. Its primary purpose at that time was to allow the exchange of Maker governance token MKR for WETH. In June 2021, as part of the dissolution of the Maker Foundation, the development and operation of Oasis.app were transferred from the Maker Foundation to its own entity.

Recently, the platform was renamed Summer.fi, symbolizing a bright, sunny, joyful, and relaxing image, also hinting at the team's vision to provide an enhanced experience for traders.

Summer.fi currently mainly offers three services: collateralization, leverage, and staking. Like other decentralized protocols, Summer.fi charges fees for its services, which are similar to interest rates for borrowing funds but are referred to as stability fees. These fees are not consistent and vary based on different vaults and tokens, determined by MKR token holders, ranging from 0% to 4.5%. Other applicable fees may include:

1) Collateralization: This feature does not charge any fees; instead, users incur ETH transaction gas fees;

2) Leverage: A fee of 0.2% is charged, and ETH transaction gas costs apply;

3) Staking: Setting up a vault to enjoy this feature incurs a fee of 0.04%;

4) Stop-loss: To close a vault, a fee of 0.2% must be paid, and transaction gas fees will be incurred when the protection is triggered.

Since establishing itself in 2021, its TVL has followed the bull market cycle to peak and has now returned to a stable state, currently around $2.2 billion in TVL, ranking seventh.

08 Coinbase Wrapped Staked ETH

Coinbase Wrapped Staked ETH was launched in June 2022, representing Ethereum hosted on Coinbase, as a token project to function like an ERC-20 token and be compatible with DApps on the Ethereum blockchain, with 1 WETH equaling 1 ETH in value.

Users can wrap ETH into cbETH without any cost, trade it on Coinbase, and use it on CEXs like Uniswap and Curve. Its design is seamlessly compatible with DeFi applications and provides rewards for staked ETH without locking it. It achieves secure, fee-free custody of ETH, providing liquidity and compatibility with various DeFi platforms.

Users can earn a 3.3% annual interest rate on Coinbase and gain additional earnings through different DeFi protocols. Supported by Coinbase's robust security measures, cbETH offers a user-friendly way to maximize staking rewards and is considered a secure and transformative utility token in the cryptocurrency ecosystem.

In the cbETH white paper released by Coinbase in August 2022, it stated: "We hope cbETH will be widely adopted in transactions, transfers, and uses within DeFi applications." "Through cbETH, Coinbase aims to contribute to the broader crypto ecosystem by creating a highly usable wrapped token and open-source smart contracts."

Overall, backed by the largest compliant CEX in the U.S., Coinbase has a large user base and resources. In terms of profitability, converting staked ETH into cbETH is free, but Coinbase, as an Ethereum validator node, takes a portion of the staking rewards as its delegation fee, which ranges from 0.5% to 4.5%. Born during a downturn in the crypto cycle and combined with the development of the staking space, it has been in a state of slow growth, currently with about $2.1 billion in TVL.

09 Compound Finance

Compound Finance is a decentralized protocol launched in 2018, built on the Ethereum network, allowing users to lend and borrow crypto assets without any third parties. It is also an algorithmic asset market protocol that provides users with a way to earn interest from savings. It primarily focuses on maximizing the profits from idle crypto assets locked in wallets to generate stable passive income. This means anyone with a Web 3.0 wallet (like MetaMask) can access it and start earning from staking.

Compound was initially funded by venture capitalists. It then created the COMP token, granting holders the right to earn fees and govern the protocol, leading to a decentralized governance structure.

Thus, Compound Finance currently operates in a decentralized manner, and the protocol is EVM compatible. The latest version, Compound V3, brings several improvements, making it safer, more user-friendly, lower risk, and easier to manage.

Compound Finance competes with JustLend, MakerDAO, AAVE, and others mentioned earlier. Although it has been surpassed in recent years, as a pioneer in the liquidity mining model, it has made significant contributions to user profitability and asset liquidity promotion in DeFi collateralization.

Compound Finance's revenue model is similar to its competitors, mainly derived from the interest rate spread between borrowing and depositing. The interest rate for tokens borrowed on the platform is determined algorithmically based on the borrowing and deposit volumes in the platform, with the platform retaining 10% of the borrowing interest as revenue and distributing the remaining interest equally among the depositors of that token.

Compound Finance currently has a TVL of nearly $1.9 billion. According to DefiLlama, the total TVL is significantly influenced by the crypto market cycle, but the "skinny camel is bigger than a horse," and it still ranks within the top ten.

10 InstaDapp

InstaDapp is a middleware protocol that simplifies and unifies the DeFi front end, which can be understood as an aggregator, established in 2018. Its goal is to simplify the complexity of DeFi and ultimately become a unified front end for DeFi, facilitating convenient asset management. Currently, it has integrated mainstream DeFi protocols through smart wallets and bridging protocols, including Maker, Aave, Compound, and Uniswap, while also supporting the migration of collateralized assets between protocols.

InstaDApp's vision seems to be to become the entry point for DeFi: catering to both ordinary users and developers and asset managers. Referencing previously successful internet companies like Google and Taobao, which are essentially aggregators or "platforms." However, a significant portion of DeFi users still lacks understanding of InstaDApp, and its success needs to be validated by the market.

InstaDapp has three products: Avocado, InstaDapp Pro, and InstaDapp Lite.

Among them, Avocado is an account-abstracted Web3 wallet; InstaDapp Pro is a layer that aggregates multiple DeFi protocols into an upgradable smart contract; while InstaDapp Lite is a vault designed specifically for various stETH-related strategies, launched after the Shanghai upgrade to keep up with the development of LSDFi.

Lite v2 enhances returns through market cycle operations to obtain boosted LSD yields, after which InstaDapp takes a 20% cut of the profits. Even so, depositors can earn slightly higher returns than Lido's stETH, indicating the high efficiency of its capital operations.

Currently, the revenue model mainly involves InstaDapp charging a 20% fee on profits, which is then transferred to the DAO, responsible for allocation and usage. However, influenced by market cycles, it is currently running steadily, with a total TVL of about $1.8 billion.

11 Summary

From the above TVL ranking data, it is not difficult to see that the DeFi space remains the leading sector in the entire crypto industry. Uniswap and Curve dominate the trading space, while MakerDAO, AAVE, and Compound rule the collateralization field. Lido provides a robust decentralized staking solution for ETH2.0, AAVE's security module innovation enhances fund safety, and Curve Finance's algorithms provide lower slippage for large stablecoin transactions. JUSTLand and Coinbase Wrapped Staked ETH have accumulated a large user base and resources thanks to the support of TRON and Coinbase, respectively.

In the continuously evolving DeFi ecosystem, these projects play key roles in driving ongoing innovation and development in the blockchain and cryptocurrency fields.

What do you think about these applications and protocols with rapidly rising TVL?

Risk warning Risk warning

Risk warning Risk warning