Analysis of Frax Finance's RWA Product Strategy

Since it is possible to earn guaranteed returns, why take risks in cryptocurrencies, real estate, or other asset classes?

Since it is possible to earn guaranteed returns, why take risks in cryptocurrencies, real estate, or other asset classes?Original Title: 《What is Frax's plan for Real-World Asset Tokenization?》

Author: Kyrian Alex

Compiled by: Lynn, MarsBit

The total TVL in the RWA tokenization space is $2.385 billion, rapidly rising in the DeFi rankings from 22nd to 8th place. What's next? What options are currently available?

Currently, only 0.06% of the population on Earth uses DeFi, highlighting the enormous growth potential of the market. The DeFi industry needs to tap into the $16.1 trillion traditional asset market to effectively scale; this represents a 500% growth opportunity!

RWA tokenization stands out in this field, becoming a bridge between DeFi and TradFi. Why? Because tokenization makes a range of asset classes, including bonds, commodities, and real estate, more accessible to everyone.

Tokenized assets can be partially owned, providing more people with investment opportunities they previously could not access. Citibank and industry leaders like Jeremy Allaire have already been advocating for tokenization as the future.

Now, let's take a look at the connection between bonds, yields, and RWA.

Now, let's take a look at the connection between bonds, yields, and RWA.

After the UST-Terra collapse, DeFi users seem to shy away from yields that seem too good to be true. But is this maturity in DeFi or just PTSD?

Want to know what the truth is? In DeFi, there are many excellent opportunities to generate income using stablecoins while minimizing risk.

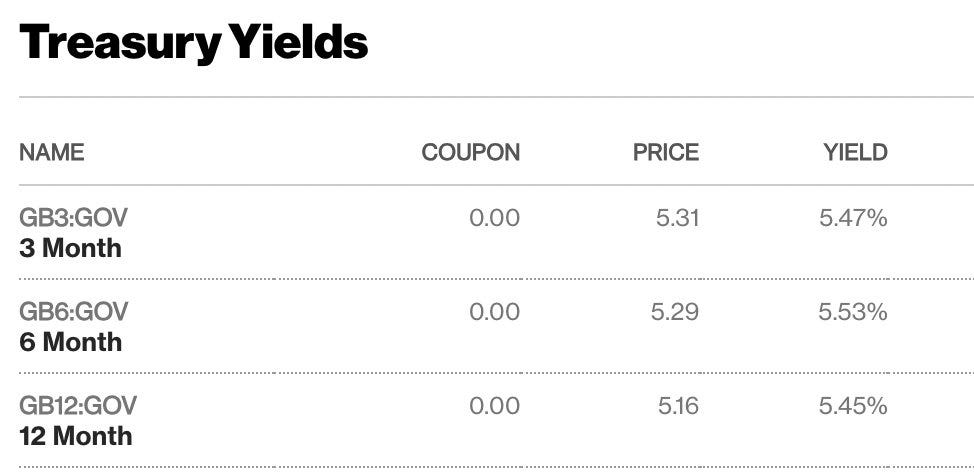

Looking at today's TardFi yields, the current yield on three-month U.S. Treasury bonds far exceeds 5%. This has significant implications for the state of all asset classes globally.

Investors are now eyeing each other:

Investors are now eyeing each other:

"Since I can earn guaranteed returns, why should I risk my money in cryptocurrencies, real estate, or other asset classes?"

Given the dangers involved (exploits, decoupling, and private key issues), DeFi yields are severely underestimated.

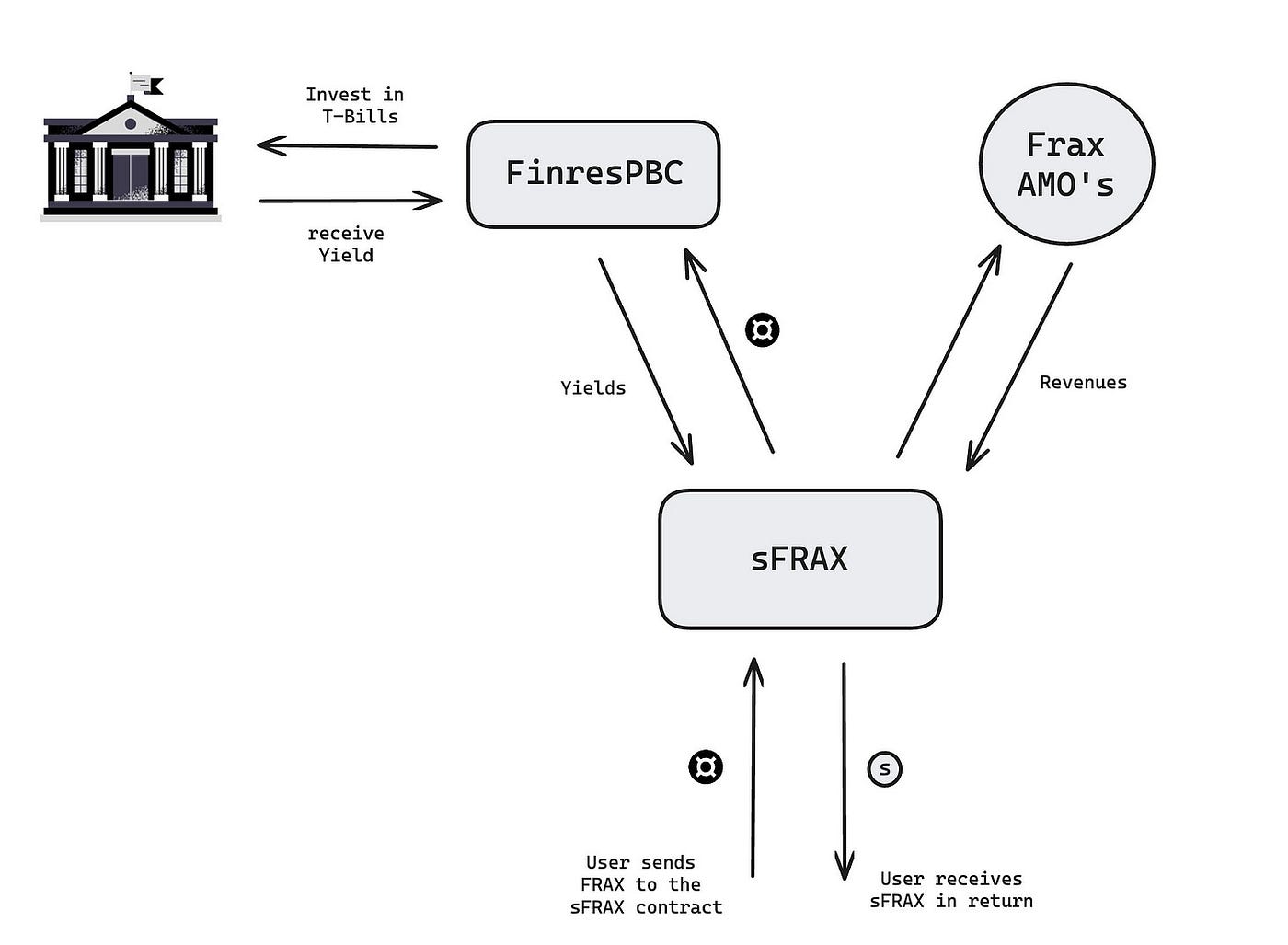

I believe Frax Finance has considered all of this when starting its FinresPBC journey. FinresPBC is Frax's RWA custodian, similar to how MakerDAO has entities that hold its treasury bonds and money market funds.

FinresPBC holds dollar deposits in FDIC-insured IntraFi savings accounts and earns interest from them. It does not seek profit or charge fees, but returns all earnings to the Frax DAO.

However, to earn these returns, Frax has launched sFRAX and FXB.

Similar to DAI savings rates, sFRAX allows users to deposit Frax (pegged to $1) and earn interest in the form of FRAX stablecoins, providing users with low-term savings options.

The interest rate is variable and may come from multiple sources. One of the mentioned sources of yield will come from the Frax algorithmic market operations controller (e.g., autonomous contracts owned by Frax) and the distribution of income from the Frax protocol's real-world asset strategy.

The annual interest rate will always "gently target" the Federal Reserve's interest on reserve balances (IORB), which is currently at 5.4%. If this cannot be achieved, Frax will always prioritize maintaining the collateralization rate of $FRAX at 100%, then transfer any excess income to sFrax.

In summary, the introduction of sFRAX aims to enable developers to build on the foundation of sFRAX, thereby promoting the development of an enhanced stablecoin ecosystem while attracting greater liquidity as the supply of FRAX increases.

On the other hand, according to Sam K, FraxBonds are "decentralized utility tokens that are priced in FRAX stablecoin debt at a certain timestamp." FRAX holders will be able to purchase discounted FRAX later in the form of Fraxbonds or FXB.

This is all part of the Frax RWA strategy and is very easy to understand.

- Users deposit their FRAX tokens into the treasury to receive sFRAX.

- The DAO selects the best options for earning yield based on current market conditions.

- If there are no good yield sources on-chain, Frax's RWA partner (Finres) will convert the FRAX tokens deposited in sFRAX into USDC.

- The converted USDC is off-chain and invested in U.S. Treasury bonds.

- Then, the receipt of this conversion will be converted back to FRAX and transferred to the Frax treasury.

- Users can then purchase FXB at a discount to earn returns upon redemption.

For example, you could buy $1 worth of FRAX for $0.90 after 2 years. When you exchange FRAX for bonds, the protocol now has the collateral to ensure it earns enough income over two years to repay the debt.

As Sam Kazemian said, "FXB does not grant holders any rights to off-chain assets, nor does it confer any legal rights to redeem for fiat currency or similar items, so they are merely utility tokens within the Frax protocol. They only guarantee that each FXB will convert to 1 FRAX stablecoin at maturity. That's it."

FXB will automatically convert to FRAX on the designated maturity date of January 1st each year. Frax will offer FXB with maturities of 1 year, 2 years, 3 years, or 4 years. This will allow Frax to bring yield curves on-chain (for at least 4 years).

Conclusion:

Conclusion:

While this strategy offers attractive yields, it is also important to understand the risks involved.

The primary risk is protocol risk. If the protocol where you deposit stablecoins is exploited, you may run into trouble. Additionally, while the coding design of stablecoins aims to maintain a value of $1, they are not immune to market fluctuations. We all have UST PTSD.

Moreover, these RWA-backed stablecoins also face regulatory risks. The U.S. government harbors significant animosity towards cryptocurrencies and will find means to slow down these protocols, potentially leading to their demise. While in the short term, we may rely on yields supported by Treasury bonds, in the long term, these protocols may face some serious issues.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles