LD Capital Macro Commentary (10.16): The outbreak of the Middle East conflict, how to view the current increase in geopolitical risks?

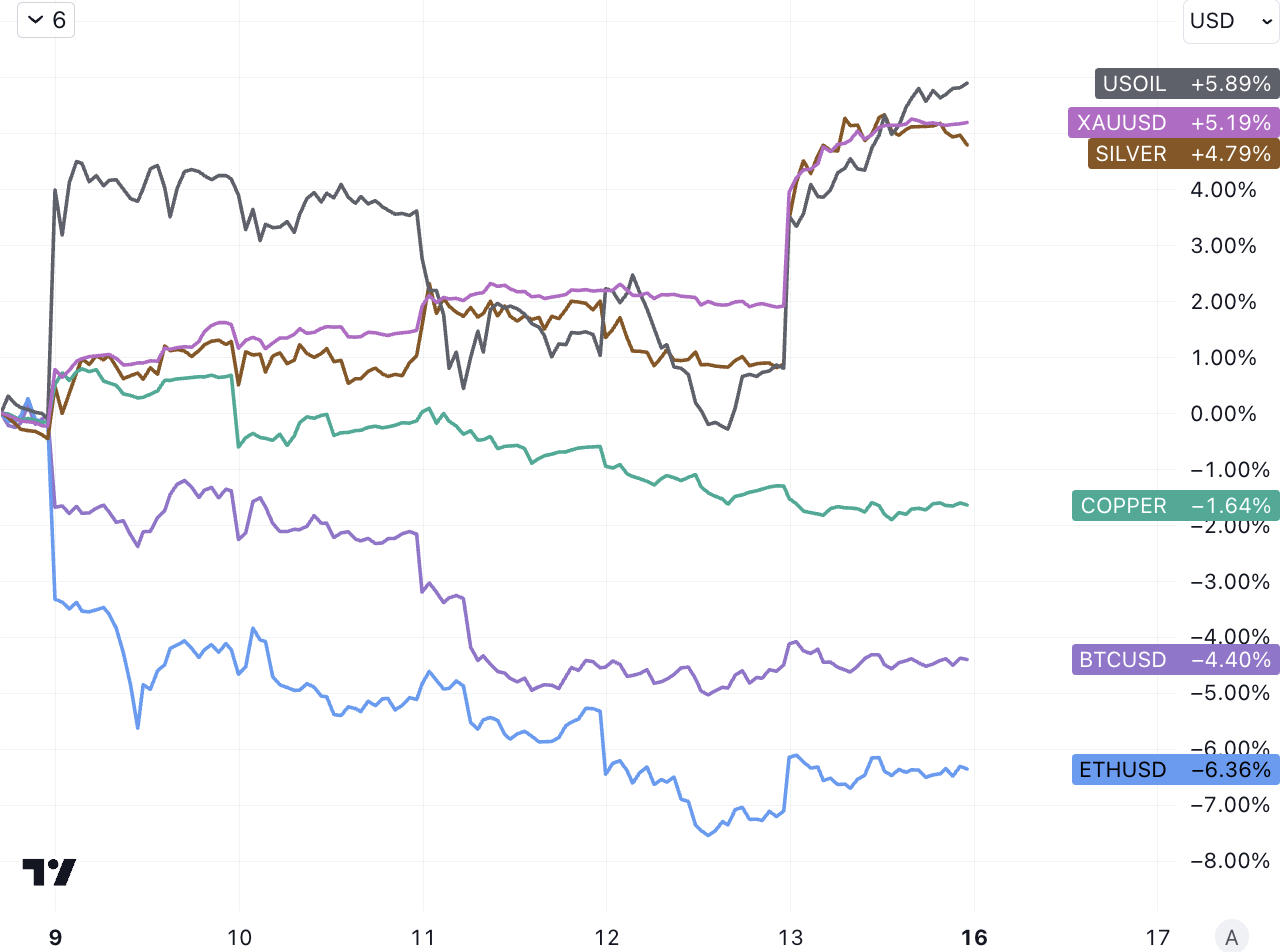

The Middle East conflict has exceeded market expectations and shows signs of escalation. The market exhibited a clear risk-averse attitude in the latter half of last week, leading to a repricing. During this period, the U.S. 30-year Treasury bond auction was lukewarm, and yields rose at one point, but could not withstand the impact of geopolitical conflicts. Ultimately, long-term yields fell significantly over the week, the stock market declined, gold, silver, and oil surged, while cryptocurrencies dropped.

The Middle East conflict has exceeded market expectations and shows signs of escalation. The market exhibited a clear risk-averse attitude in the latter half of last week, leading to a repricing. During this period, the U.S. 30-year Treasury bond auction was lukewarm, and yields rose at one point, but could not withstand the impact of geopolitical conflicts. Ultimately, long-term yields fell significantly over the week, the stock market declined, gold, silver, and oil surged, while cryptocurrencies dropped.Author: LD Capital

Market Overview

The Middle East conflict has exceeded market expectations and shows signs of escalation. The market exhibited a clear risk-averse attitude in the latter half of last week, leading to a repricing. During this period, the U.S. 30-year Treasury auction was lukewarm, and yields rose temporarily, but could not withstand the impact of geopolitical conflict, ultimately resulting in a significant decline in long-end yields for the week. The stock market fell, while gold, silver, and oil surged, and cryptocurrencies declined.

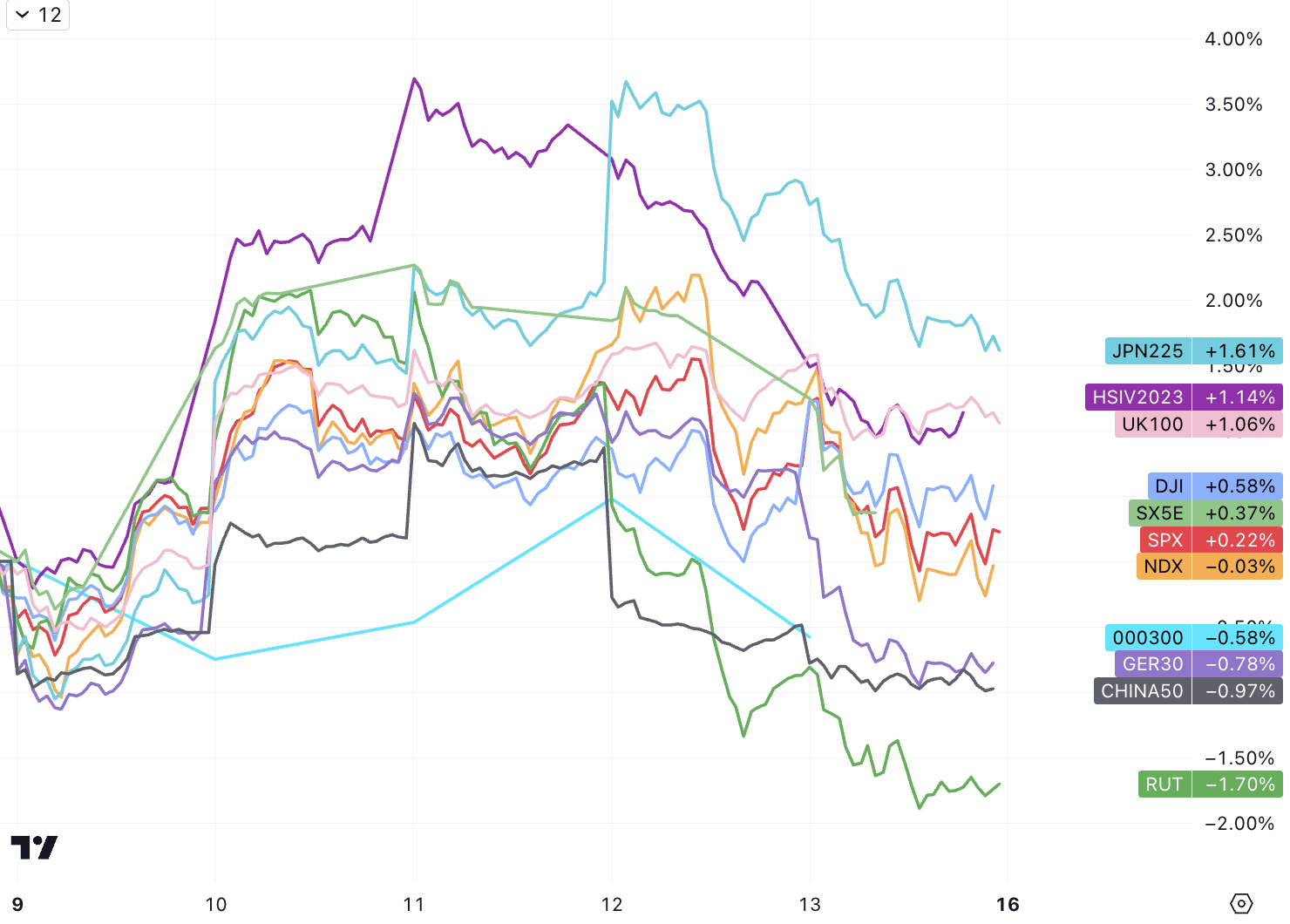

In terms of the global stock market, as we mentioned in our morning meeting last week, the stock market did not consider the Israel-Palestine conflict too much in the first half, still digesting the positive impact of several Fed officials adopting a dovish tone, leading to an overall rise. However, during Thursday and Friday, the market experienced a significant drop due to the combination of a lukewarm U.S. 30-year auction, CPI slightly exceeding expectations, initial jobless claims better than expected, rising inflation survey expectations, and the worsening situation of the Israel-Palestine conflict. Nevertheless, Japanese stocks, U.S. stocks, and Hong Kong stocks still ended the week higher:

Last week, the U.S. earnings season kicked off well, with JPMorgan Chase, Wells Fargo, and Citigroup reporting impressive Q3 results, with net interest income and revenue figures exceeding expectations. There were concerns about an increase in bad debts due to credit deterioration and rising deposit costs leading to competition, which could potentially reduce banks' net interest income, but in reality, neither of these points has yet manifested; currently, only the favorable aspect of the widening interest margin due to the rising interest rate environment is evident.

Gold performed strongly throughout the week, while BTC failed to demonstrate its safe-haven properties this time. On Friday, news that the SEC does not plan to appeal the court's ruling on Grayscale's Bitcoin ETF briefly boosted prices; this event will require the SEC to re-evaluate Grayscale's application, but it can still refuse approval for other reasons:

Oil prices surged by 6%, but an optimistic view suggests that the actual price of oil is already high, making it hard to imagine it rising two or three times from current levels. The oil intensity of the global economy is far less than before, so the impact of the Middle East situation on the real economy and inflation process will be very limited. This may be the reason why the market ignored geopolitical risks in the first half.

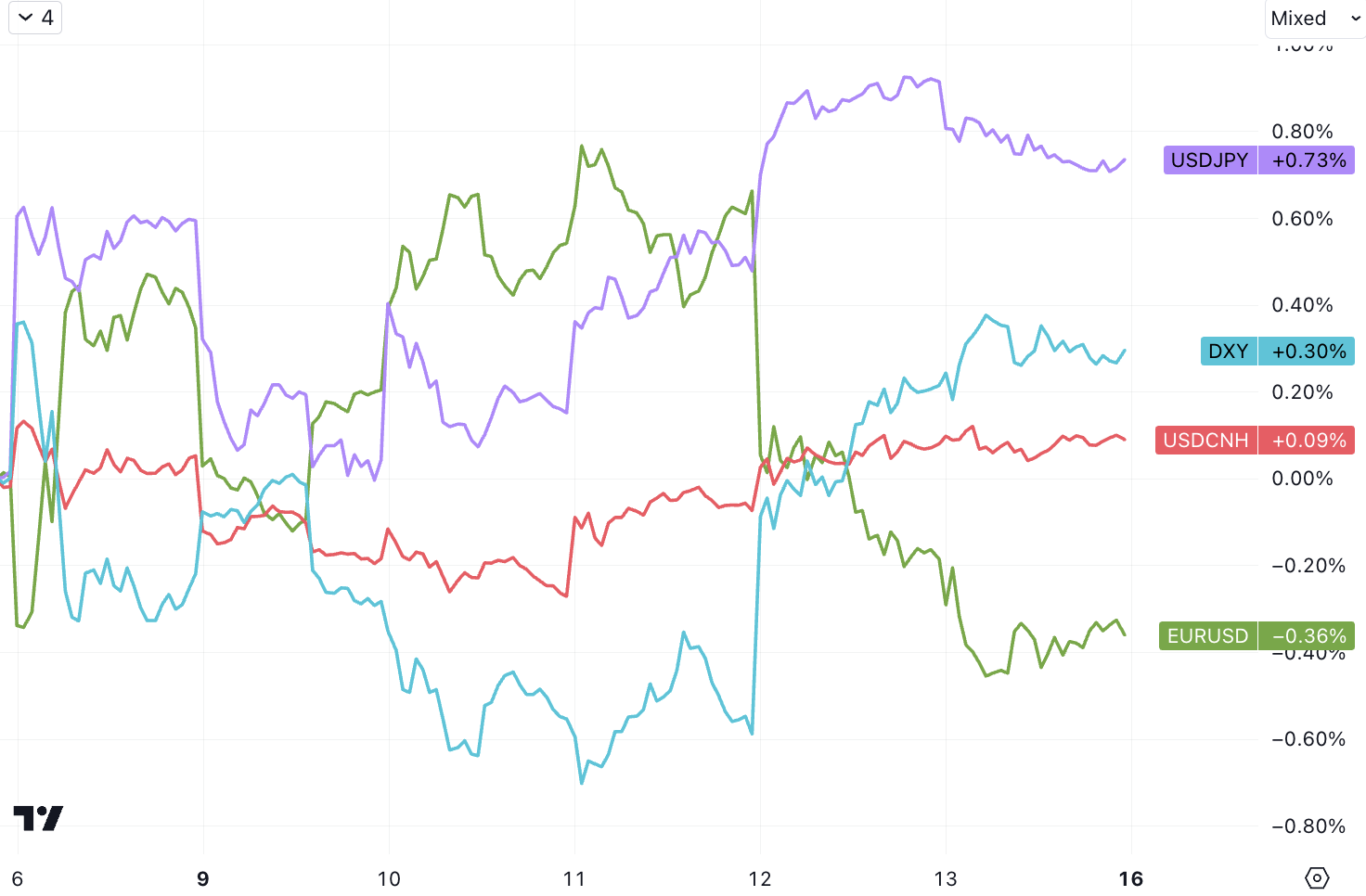

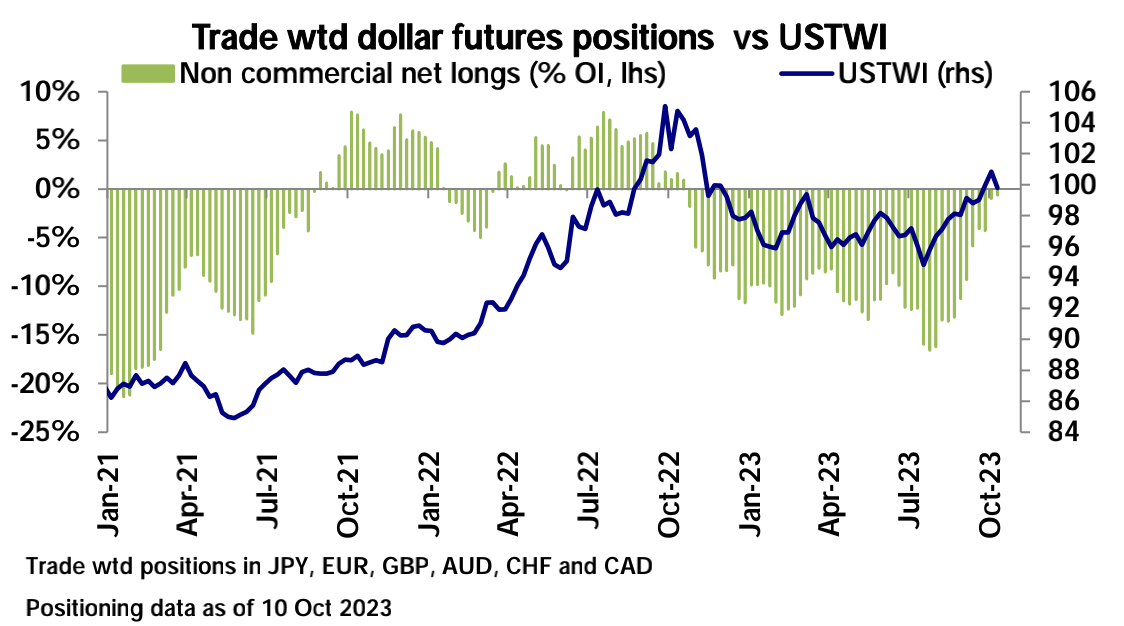

The dollar only retraced for a week, rebounding strongly last week, with the DXY returning above 106.6, and USDJPY continuing to oscillate at high levels near the 150 mark:

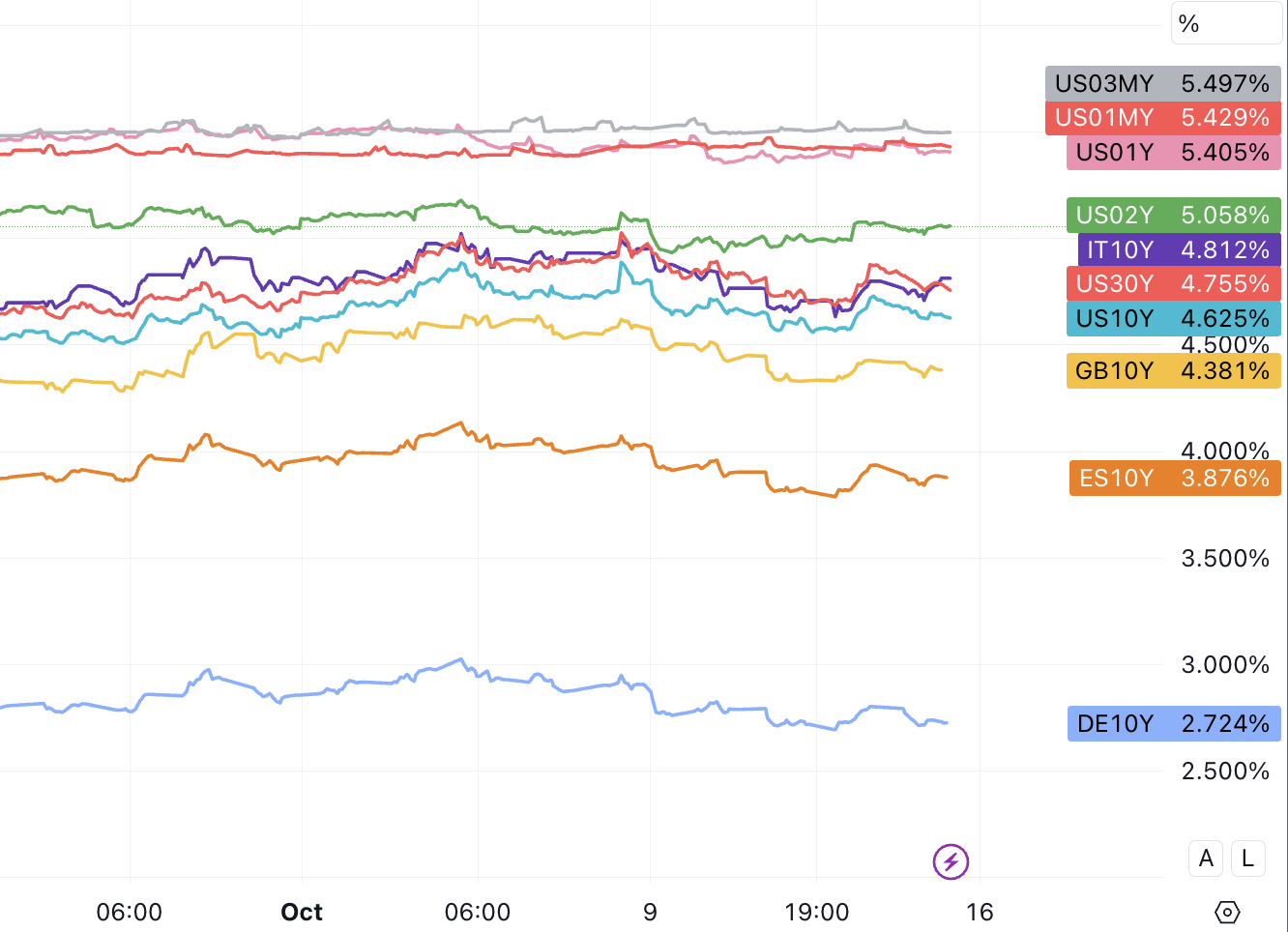

Long-end rates have clearly declined, while short-end changes have been minor. The market focused on supply-side issues in bonds last week.

All three new issuance auctions last week were priced lower than expected, especially the last 30-year auction, which not only saw yields reach a new high since 2007 but also had a significantly reduced subscription multiple. Before the 30-year auction, U.S. Treasury yields had already risen significantly due to CPI and initial jobless claims data, in other words, it was a preemptive price reduction promotion. However, terminal demand remains unsatisfactory.

The U.S. federal budget deficit for the fiscal year 2023 is $1.7 trillion, up from $1.38 trillion in fiscal year 2022. The lack of fiscal discipline is a major reason for the pessimistic market sentiment. The results of this auction, combined with the Treasury's expansion of 4-week, 8-week, and 17-week bill issuances to the highest scale ever, remind one of the massive financing plan announced by the Treasury in August (10-year yields surged from 3% to 4.46%). The difference now compared to August is that the Fed's tone regarding the tightening monetary policy outlook has slightly softened, but U.S. Treasury yields remain too high. Therefore, some viewpoints suggest that if there is a desire to curb the rising yield momentum, Powell himself must make a dovish statement, making this an asymmetrical opportunity to go long on U.S. Treasuries, including gold, silver, and even cryptocurrencies.

Currently, the volatility in the bond market has exceeded that of the stock market, with the three-month implied volatility of the iShares 20+ Year Treasury Bond ETF (TLT) being over 4 percentage points higher than that of the SPDR S&P 500 ETF (SPY), overturning their traditional relationship, as bond ETFs usually average 3 percentage points lower in volatility. Despite TLT dropping 37% over the past two years, investors continue to flock to TLT funds, betting that once yields begin to decline, they could achieve excess returns.

It is also worth noting that Italy's 10-year yield is nearing 5%, the highest level since the end of the Eurozone debt crisis in 2012. This is concerning because Italy is one of the most heavily indebted members of the Eurozone, and its government's spending plans remain aggressive and, in the eyes of many market participants, unsustainable. Italy's public debt stands at 145% of GDP, about 15 percentage points higher than during the 2012 crisis. Is another debt crisis in the Eurozone looming?

Whether the Fed has completed its rate hike cycle is an important topic. Currently, the market leans towards the view that the labor market has loosened and inflation data has softened, suggesting that the FOMC should abandon the last rate hike. A pause in rate hikes at the next meeting could be more easily reached within the FOMC. Furthermore, if Q4 growth and inflation data develop as expected, the rationale for a December rate hike will also be insufficient.

How to View Geopolitical Risks

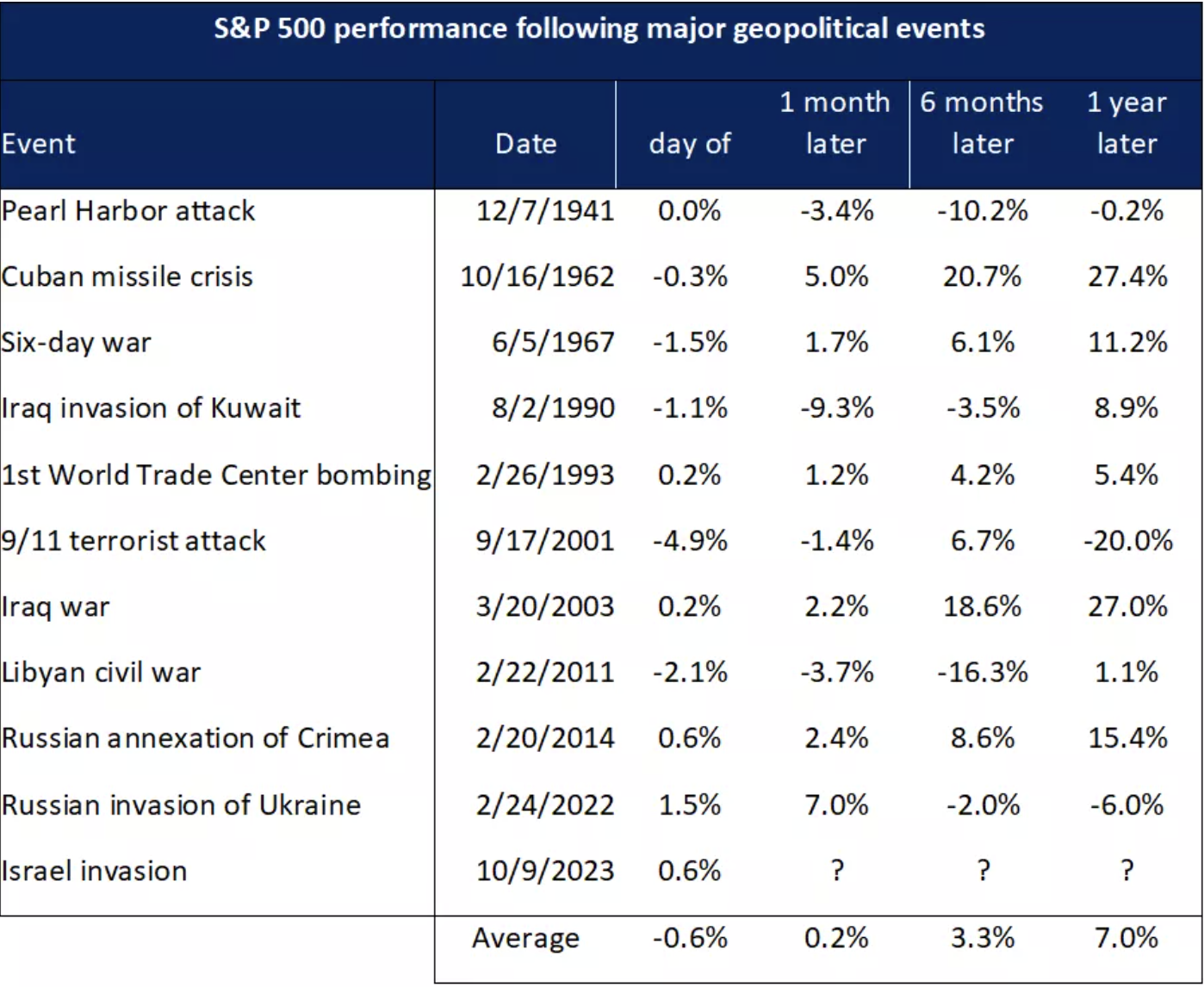

Investors naturally tend to be averse to uncertainty; in the short term, the stock market may decline after a conflict occurs, but this impact is usually temporary. Historically, in most cases, even if the stock market performs poorly within a month after a conflict, it tends to rebound after 6 months or a year. The main drivers of stock market value remain sustainable profits, and the shocks from geopolitical events are often overshadowed by fundamentals.

Regarding the impact on the investment industry: in the context of rising geopolitical risks, the significance of quantitative models used for asset pricing and trend judgment may weaken. Supported by global trade growth and minimal political shocks, decades of relative stability have made it easier to predict macroeconomic variables such as growth, interest rates, and inflation. When there are fewer and simpler fundamental assumptions about the world, it becomes relatively easy to assess how these values will evolve.

Today, the economy is increasingly influenced by political and diplomatic policies, which transcend charts, balance sheets, and ratios. Attempting to parse geopolitical events will only introduce more artificial errors into the market. However, research indicates that market volatility has widened the range of returns for active funds, testing the capabilities of fund managers. In a high-volatility environment, portfolio diversification becomes attractive, including alternative assets such as commodities, crypto assets, and art.

Current risk points in the Middle East situation: Will it involve more major powers/energy powers like Iran, the U.S., Saudi Arabia, or even Russia? Extreme "tail risks" --- for example, will there be a conflict in the Taiwan Strait, or will Russia use nuclear weapons in Ukraine?

Market behavior patterns often tend to either perceive risks as manageable, with minimal price disturbances, or catastrophic, leading to a complete abandonment of risk exposure. They oscillate between two extremes rather than evolving gradually.

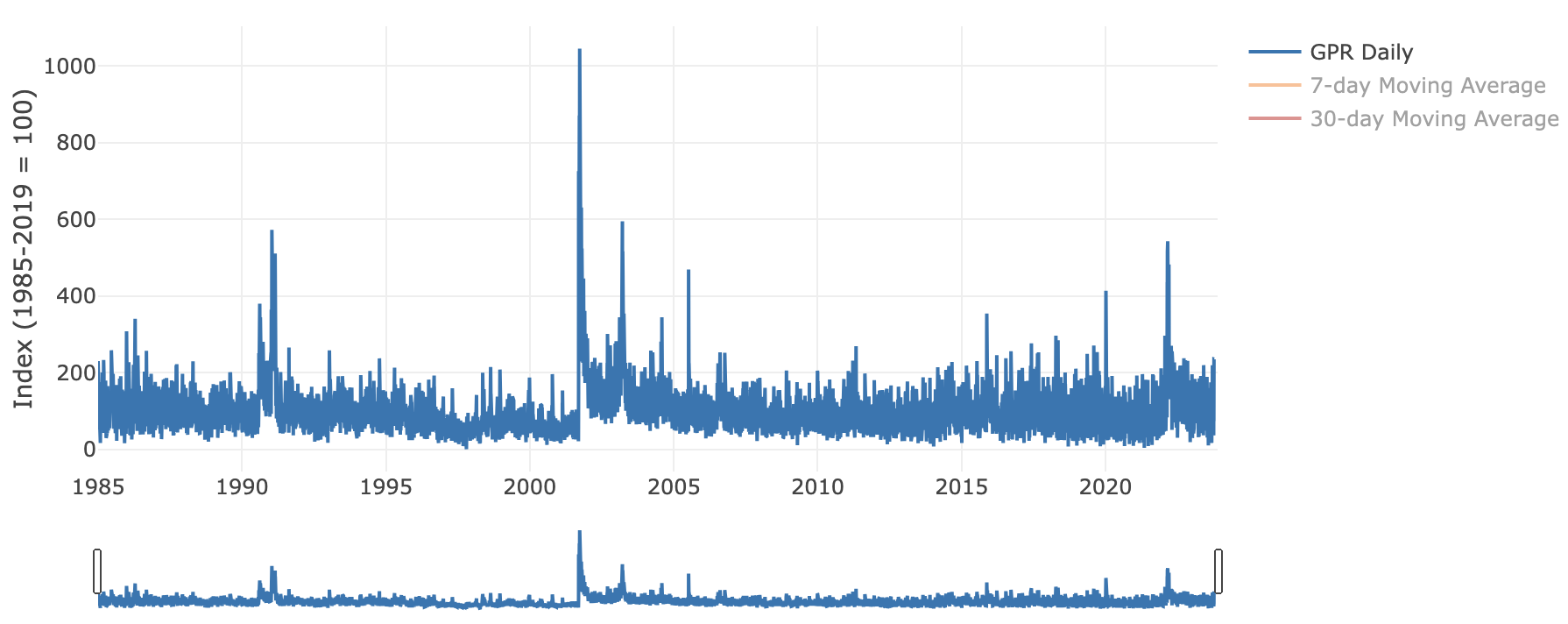

Attached are three high-frequency updated risk indices (the principle is to capture the frequency of keywords related to specific risks in analyst reports or traditional and social media, along with the associated sentiment) which have not seen significant increases yet:

Dario Caldara and Matteo Iacoviello's geopolitical risk (GPR) index:

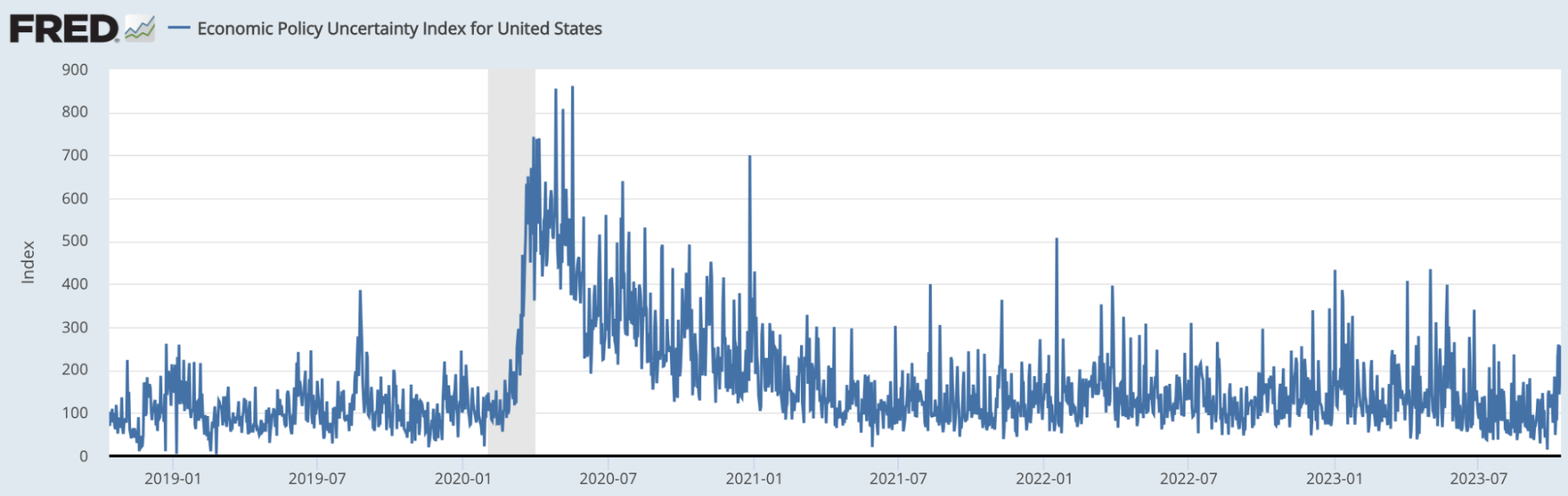

Economic Policy Uncertainty Index for the United States:

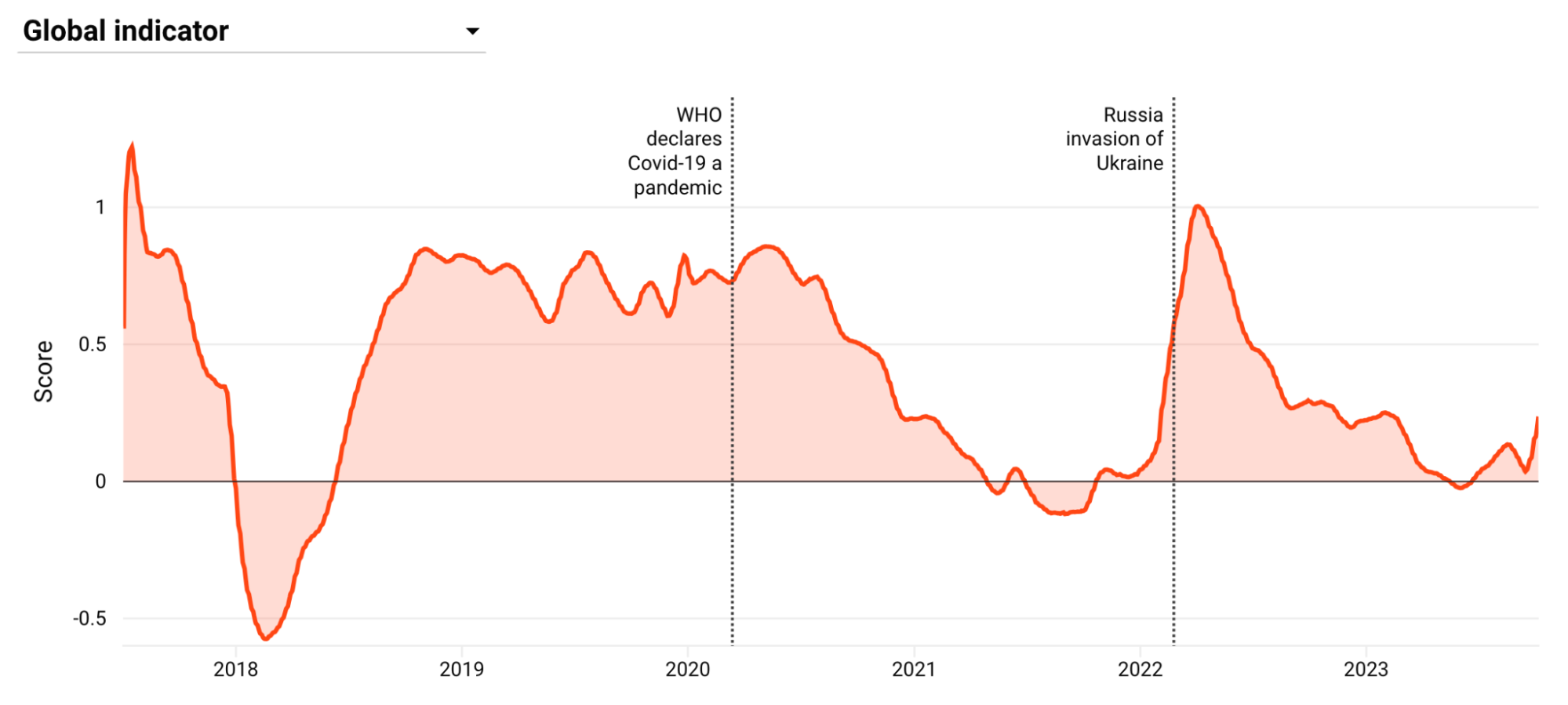

BlackRock chart on its Geopolitical Risk Indicator:

Market News

Early Friday, media reports that Israel requested the entire population of the Gaza Strip to relocate to the south shocked the world, becoming the biggest driver of the market. Western media, including BBC and CNN, are discussing the phenomenon that half of Gaza's population consists of children, and public opinion is not as one-sided in favor of Israel as it was the previous weekend.

Israeli Prime Minister Benjamin Netanyahu vowed on Sunday to "destroy Hamas," while Hamas told local residents to ignore Israel's messages about moving south. The World Health Organization stated that Israel's order to evacuate 22 hospitals in Gaza is a "death sentence for the injured."

(Israel has invaded Gaza twice by force. The first time was "Operation Cast Lead," a 15-day ground invasion in January 2009. At that time, the Defense Forces occupied territory near the border with the aim of closing tunnels used for smuggling food, fighters, and weapons.

The second time was in 2014 during "Operation Protective Edge," where the Israeli Defense Forces stayed on the ground for 19 days.

Now a third ground invasion is imminent. It appears to be potentially larger, longer, and more violent than any previous incursions. Gaza is a densely populated area with over 2 million people, and Israel has a strong sense of retaliation, making it possible for anything to happen in a state of rage. Hamas is deeply rooted in Gaza, embedded in a series of charities, schools, and mosques. Separating Hamas from Gaza is almost an impossible task. Fourteen years ago, Hamas had hundreds of kilometers of tunnels in Gaza. Now Trump has tweeted that there are effectively two Gazas: one above ground and one below. One can imagine the scale of the underground Gaza. The latest news is that Israel and Hezbollah have already exchanged fire at the Israel-Lebanon border, with Hezbollah claiming to be equipped with precision weapons. Let's pray for world peace this weekend.)

Gaza reported on Sunday that, so far, Israel's retaliatory strikes have resulted in over 2,450 deaths, a quarter of whom are children, and nearly 10,000 injuries. Hezbollah announced over the weekend that it has also begun mutual attacks with Israel, and experts speculate that this could serve as a trigger for Israeli ground attacks on Gaza.

In the early hours of today, Iranian officials stated they would no longer stand by, saying, "If crimes continue in Gaza tomorrow, it will be too late."

The overall CPI in the U.S. exceeded expectations in September, with core CPI rising 0.3% month-on-month for the second consecutive month due to persistent housing inflation. The Fed's "last mile" in combating inflation is quite challenging. Overall, the stickiness of housing projects is the main reason for this nominal inflation exceeding expectations, followed by the traditionally volatile energy and food sectors, while goods excluding energy and food have made a negative contribution. In core service projects, the housing index's month-on-month growth rate accelerated from 0.3% to 0.6% in September, with the rent index rising 0.5% and the owner's equivalent rent index increasing 0.6% month-on-month.

The U.S. Treasury expanded the issuance of 4-week, 8-week, and 17-week Treasury bills to the highest scale ever. U.S. Treasury Secretary Yellen stated that the U.S. has not ruled out imposing new sanctions on Iran.

Foreign media reported that China is considering establishing a new stock market stabilization fund worth hundreds of billions of RMB. This plan may involve existing financial institutions and professional management funds investing in domestic stocks. Not only government funds but also institutions will match the contributions.

Since October, more and more Federal Reserve officials have emphasized that the recent tightening of financial conditions, if it continues, may offset the need for further rate hikes.

- Logan stated that if long-term rates remain high due to rising term premiums, the necessity for further rate hikes may decrease. However, if strong economic performance is the reason for rising long-term rates, the FOMC may need to take more action.

- Daly expressed that it is absolutely conceivable to adjust the neutral rate to around 2.5% to 3%, and the tightening financial conditions may equate to one rate hike.

- Bostic mentioned that the Fed does not need to raise rates again unless inflation stagnates. He does not believe the U.S. will enter a recession.

- Collins stated that he is realistically optimistic about achieving a soft landing, suggesting that we may be close to or at peak rates.

- Jefferson indicated that he is closely monitoring changes in yields and is at a critical position for assessing how much monetary policy can tighten. Looking ahead, he is well aware that higher bond yields will tighten financial conditions.

The University of Michigan's consumer confidence index has fallen across the board, with inflation expectations rising for both the short and long term.

The UAW has expanded its strike to a Ford plant in Kentucky, with Ford currently stating it cannot meet UAW's demands. Kaiser has indicated that it has reached a preliminary agreement with the union, ensuring that the scale of the strike will not expand further.

On Friday, Scalise announced his withdrawal from the race for House Speaker. Trump's supporter, Jim Jordan, who previously lost to Scalise, received the GOP's internal nomination. The recently ousted Kevin McCarthy expressed support for Jordan to succeed him, and there is anger within the Republican Party over McCarthy's compromise with Democrats a few weeks ago to avoid a partial government shutdown.

Some Democrats criticized Jordan's previous remarks that incited the mob's storming of the Capitol in early 2021. He is politically conservative, but in the eyes of the far-right within the Republican Party, he is clearly not conservative enough, so this faction does not support Jordan's rise.

From preliminary statistics, Jordan still lacks sufficient internal support, which may lead to continued dysfunction within the Republican Party. If the House cannot operate normally, no legislation can pass Congress and be submitted to the President.

The IRS has issued a notice to Microsoft for the recovery of up to $28.9 billion in taxes. Microsoft plans to appeal these notices administratively and is willing to pursue judicial proceedings if necessary. There is also good news for Microsoft, as the UK's Competition and Markets Authority (CMA) has approved Microsoft's $69 billion acquisition of Activision Blizzard. This record-setting acquisition in gaming history has finally been finalized after 20 months of negotiations. Upon completion of this transaction, Microsoft will become the third highest-grossing gaming company in the world, behind Tencent and Sony.

The "weight loss miracle drug" is incredibly popular, with Novo Nordisk raising its full-year revenue growth forecast three times this year, from 27-33% to 32-38%, and raising its EBIT growth forecast from 31-37% to 40-46%, with analysts expecting a 37.5% increase. As a result, Novo Nordisk's stock price surged over 5%, reaching an all-time high, and has risen nearly 50% year-to-date. Its market capitalization has surpassed that of luxury giant LVMH, making it the most valuable company in Europe.

Positions and Fund Flows

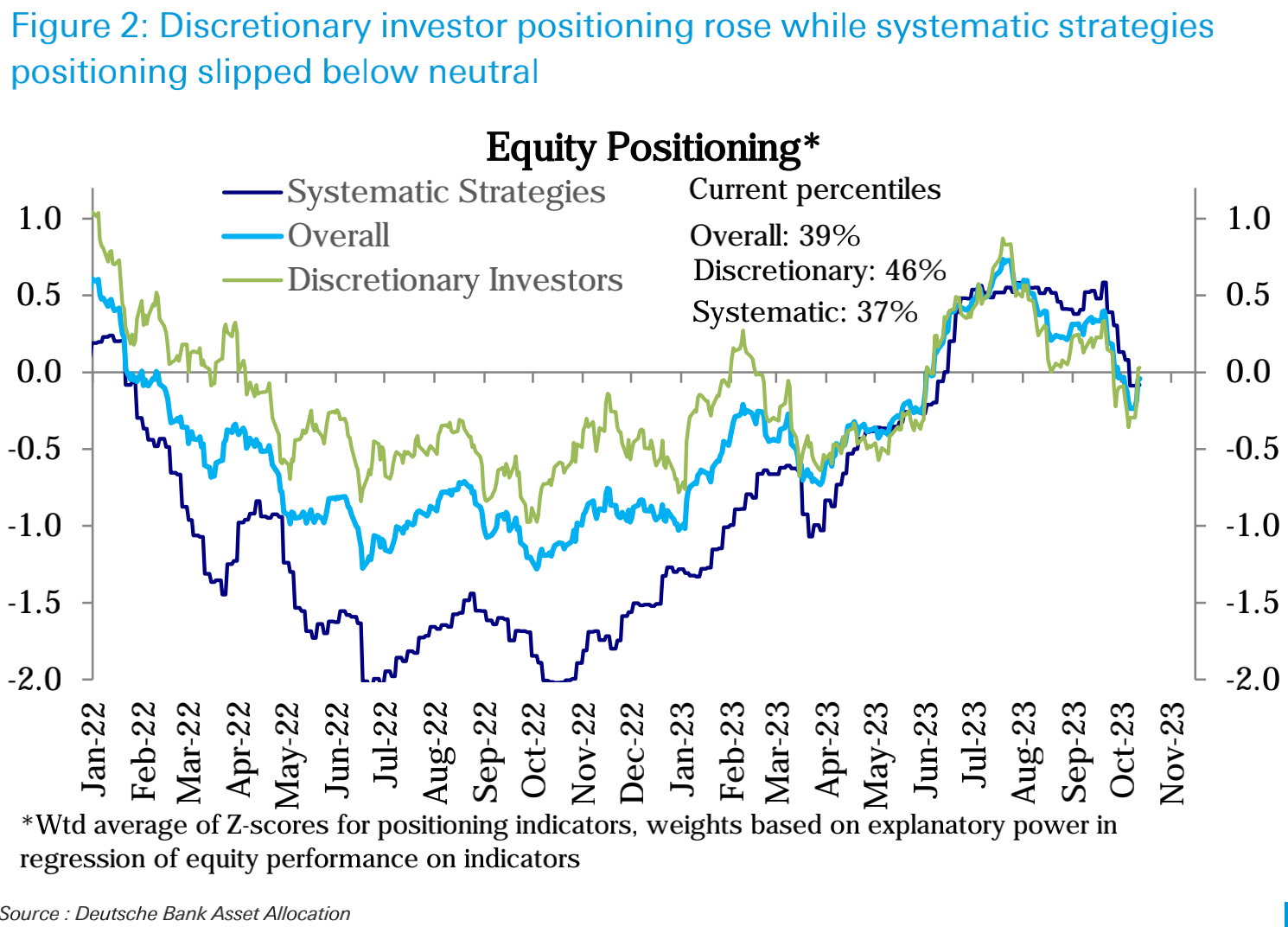

Subjective investor positions shifted from moderately short to neutral (46th percentile), while systematic strategy positions decreased to slightly below neutral (37th percentile):

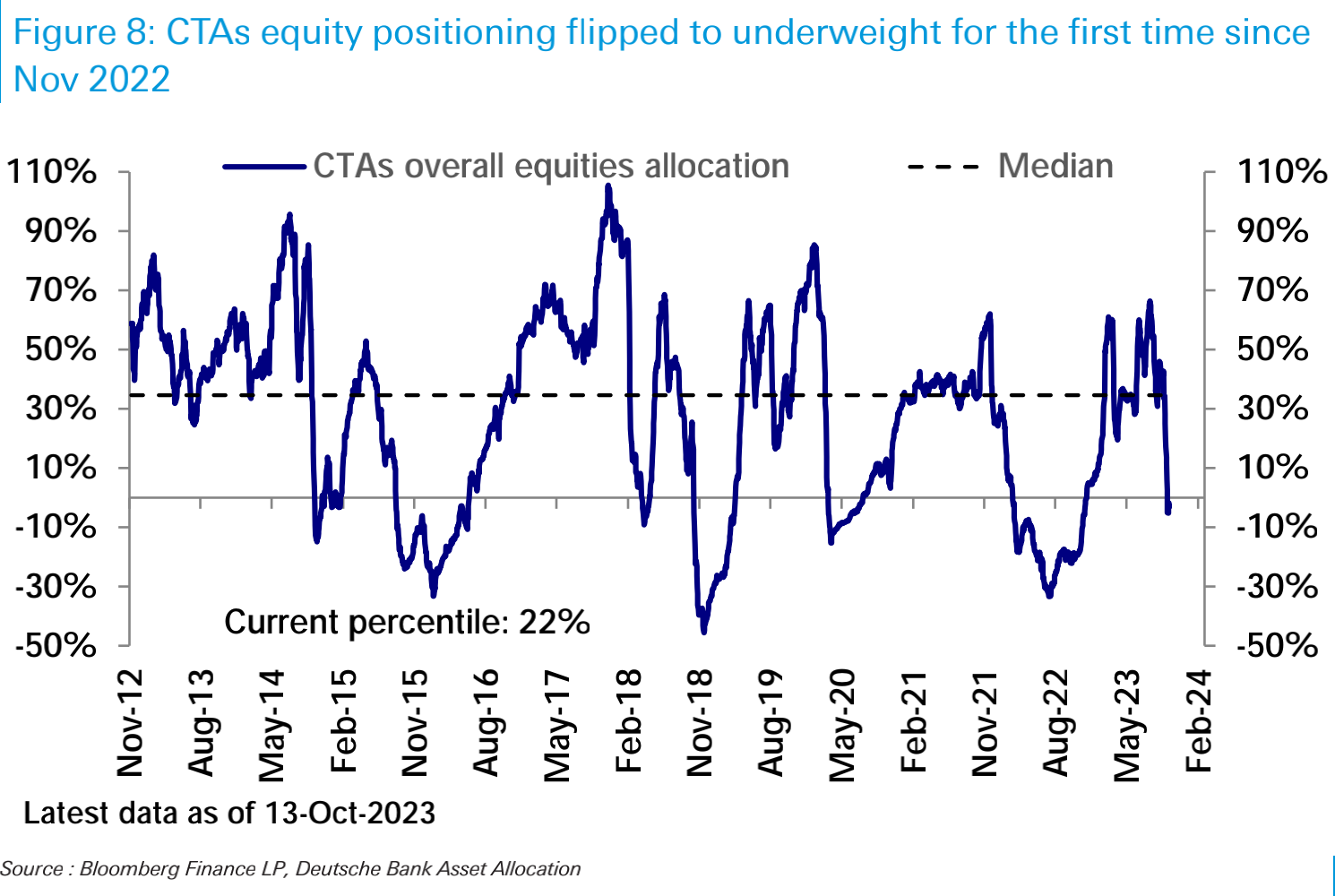

It is noteworthy that CTA funds have turned bearish on the stock market for the first time in nearly a year:

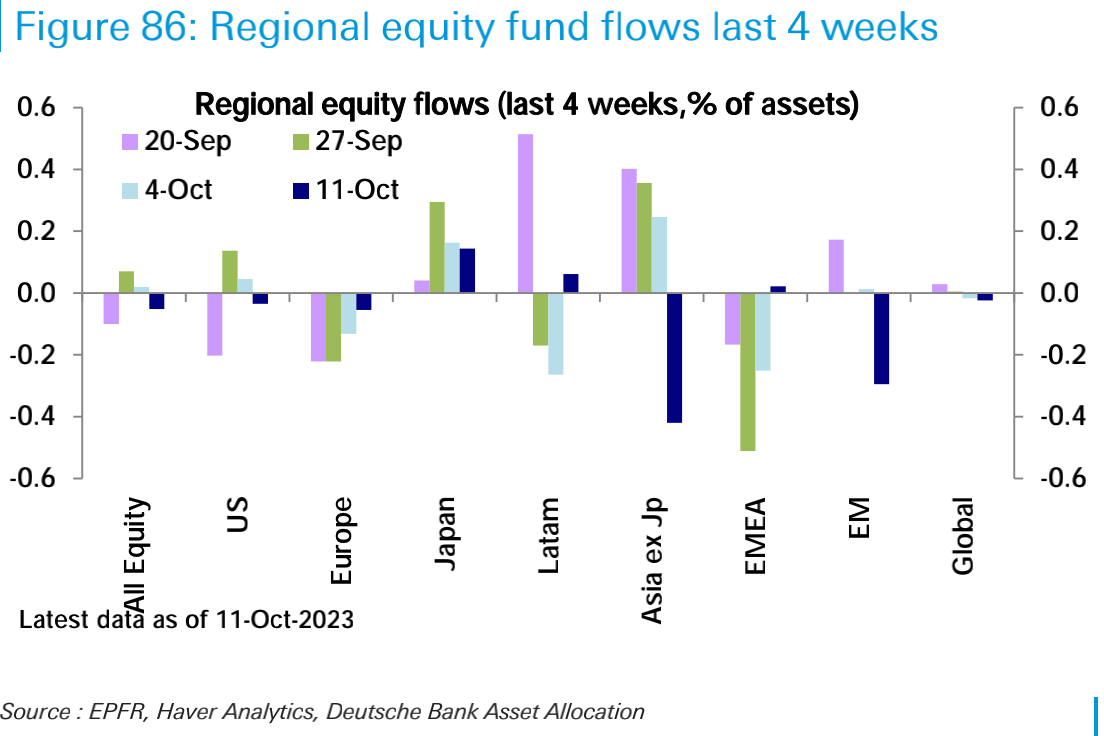

Equity funds experienced a net outflow of $8.2 billion this week, ending two consecutive weeks of net inflows. Emerging markets (outflow of $4.3 billion) and the U.S. (outflow of $3 billion) dominated the outflows.

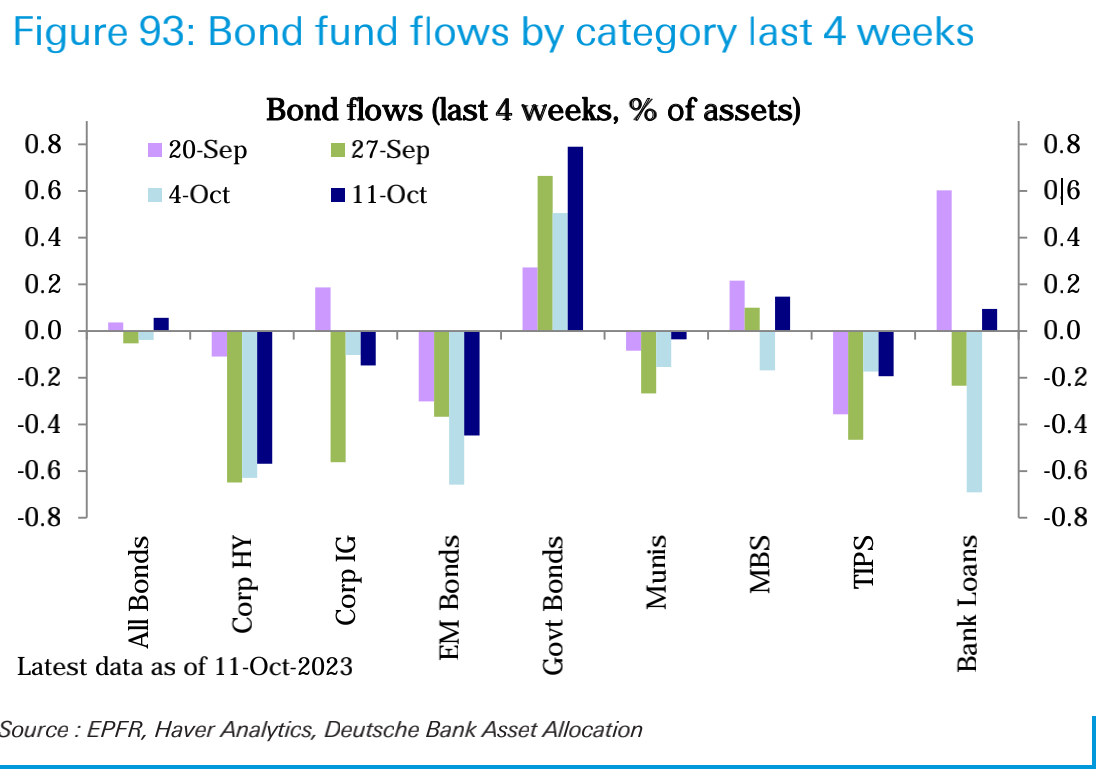

Bond funds (inflow of $3.7 billion) turned to net inflows after two weeks of net outflows, primarily driven by a surge in government bond inflows (inflow of $7.2 billion) to a three-month high:

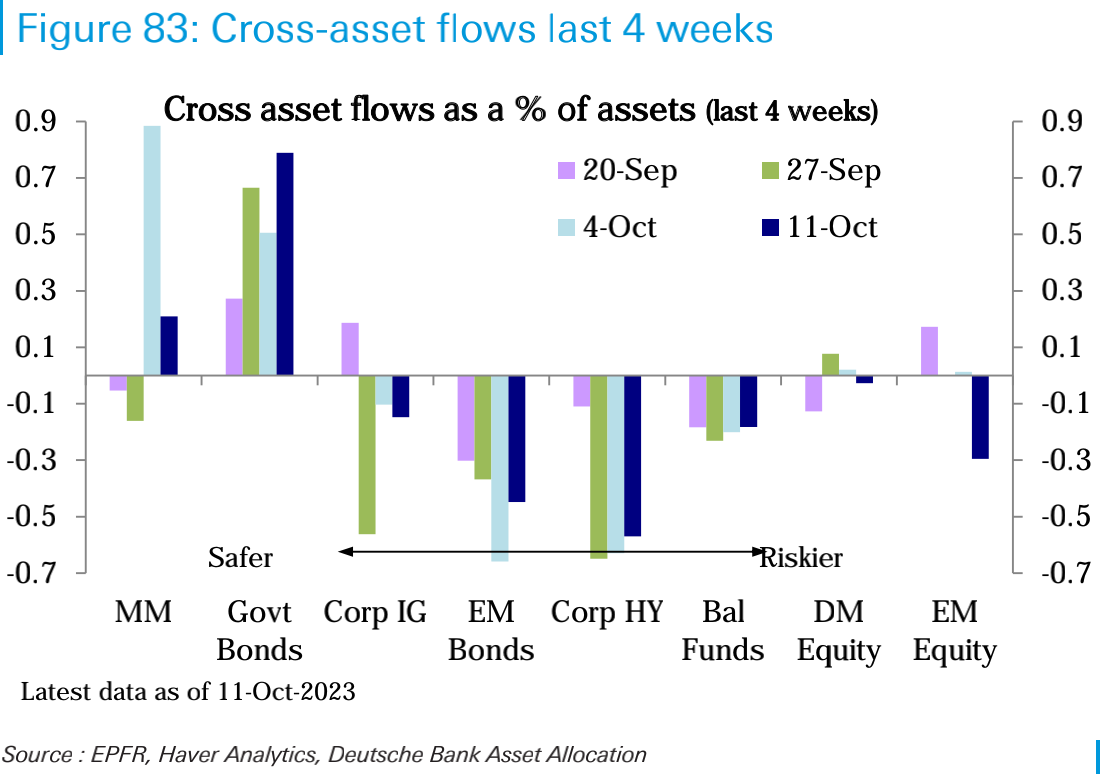

Money market funds (inflow of $16.9 billion), but the scale is much smaller than last week:

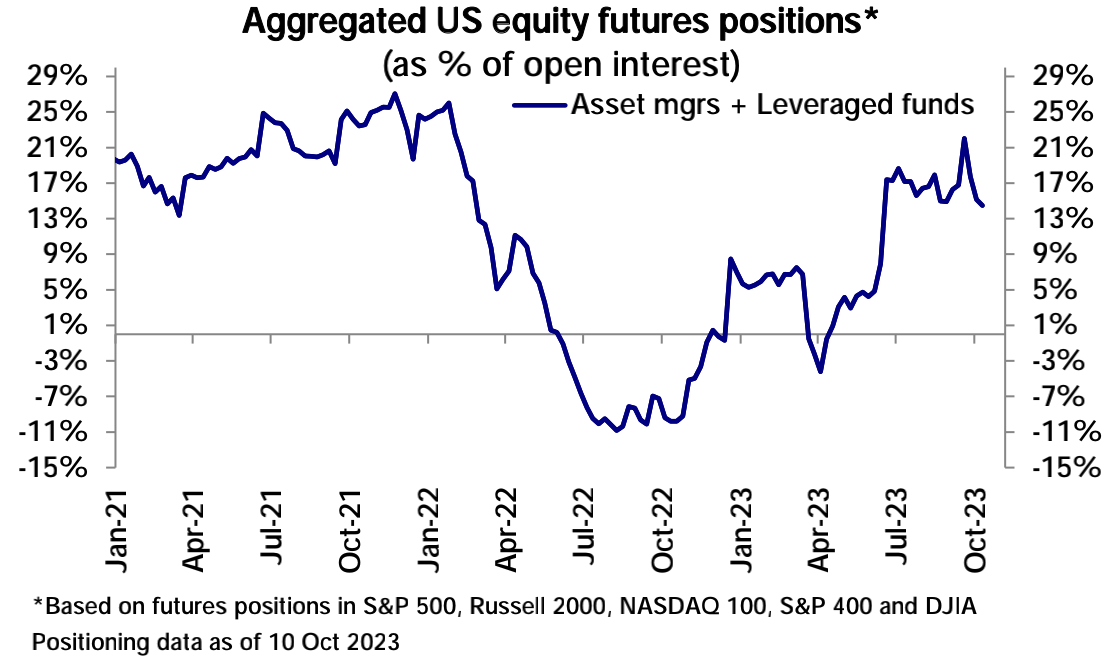

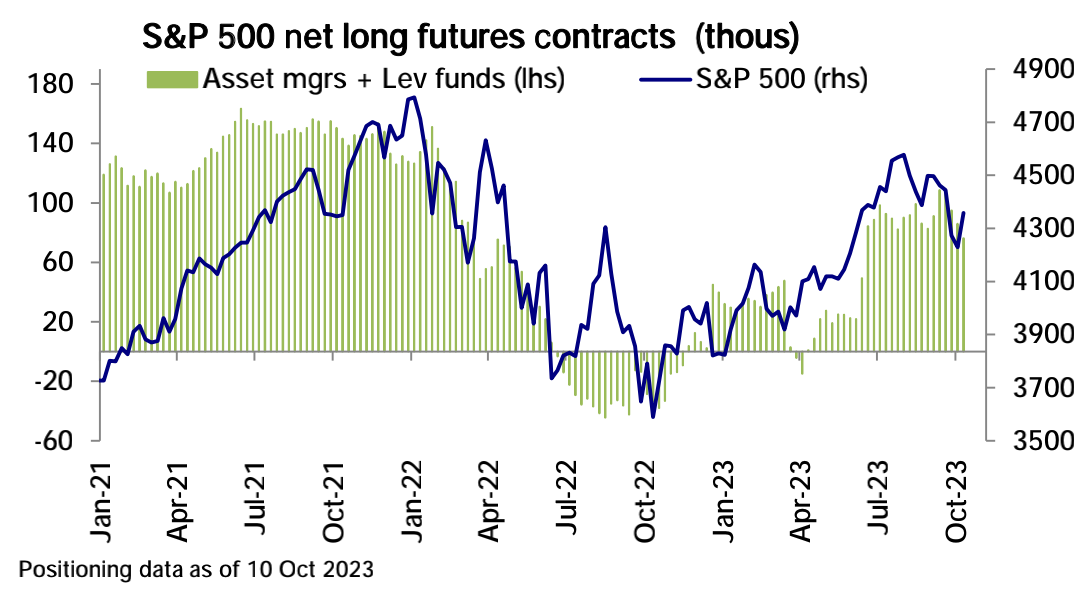

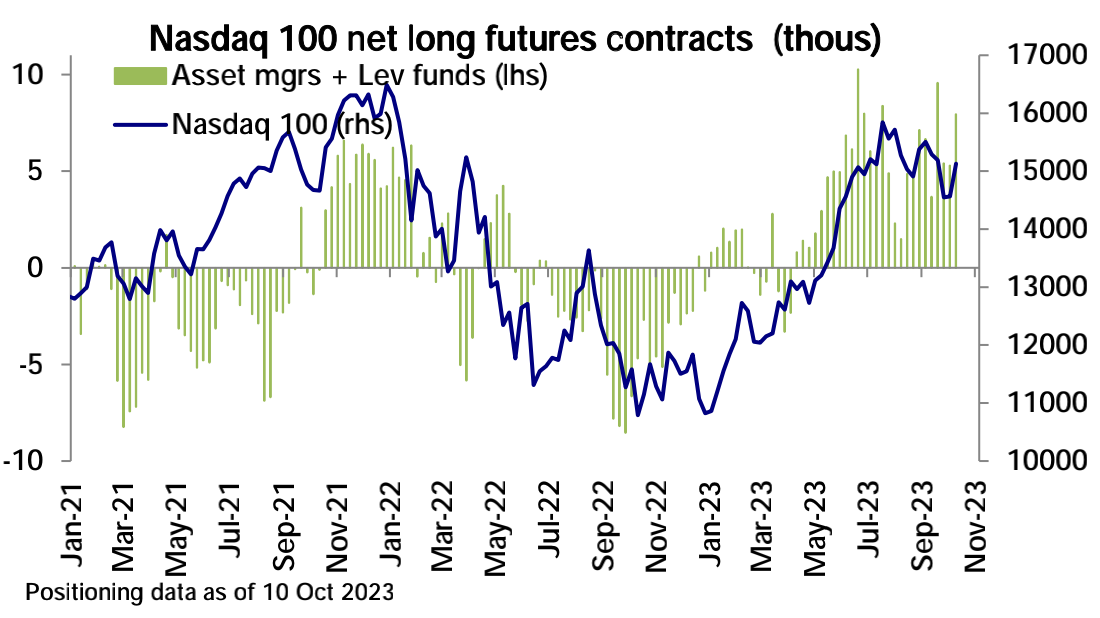

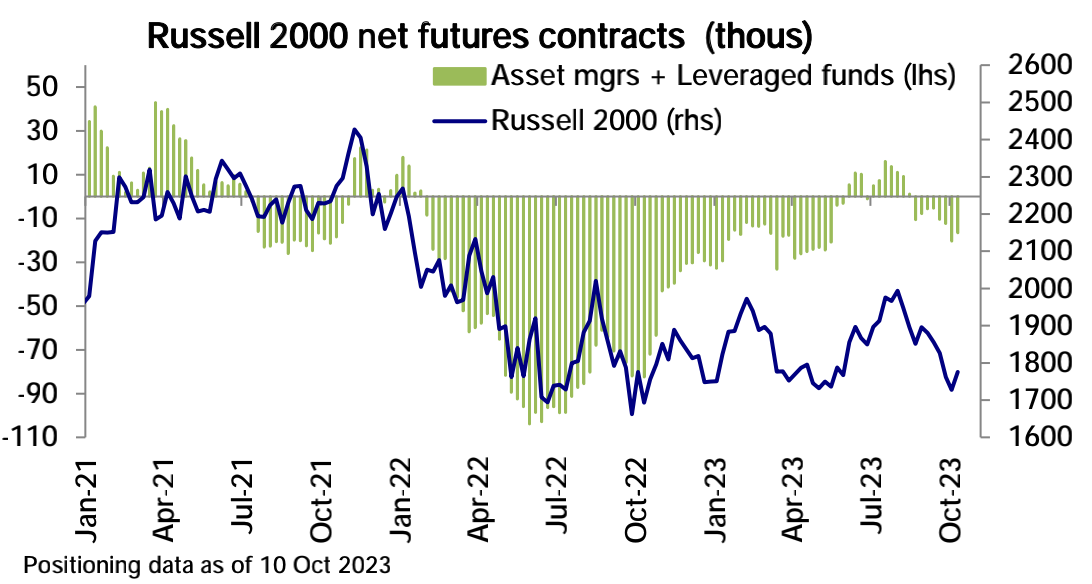

CFTC data shows that net long positions in U.S. stock index futures have decreased for the third week. The decline in net long positions in the S&P 500 dominated this trend, while net long positions in the Nasdaq 100 increased, and net short positions in the Russell 2000 decreased:

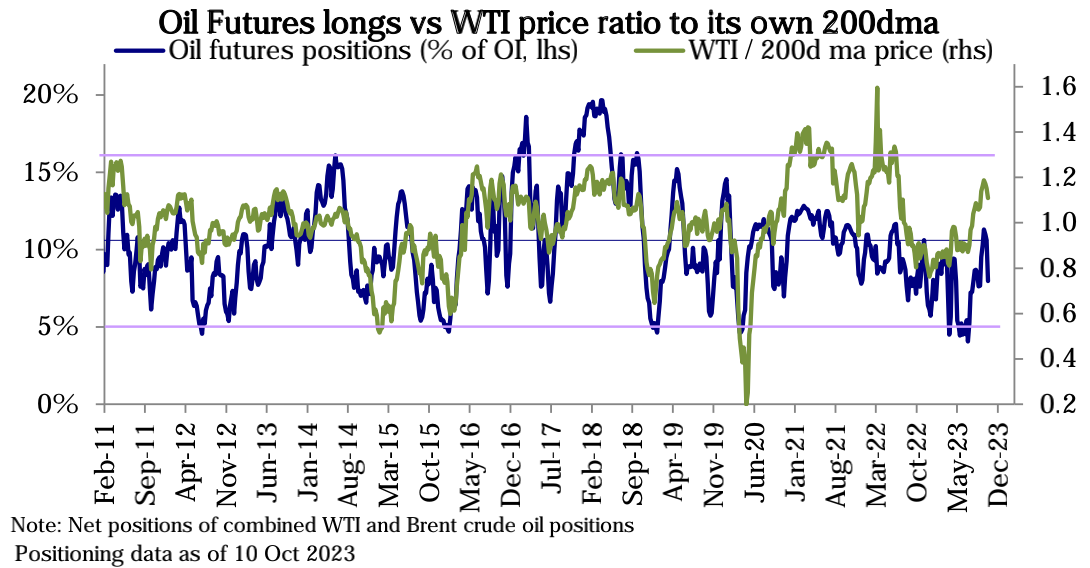

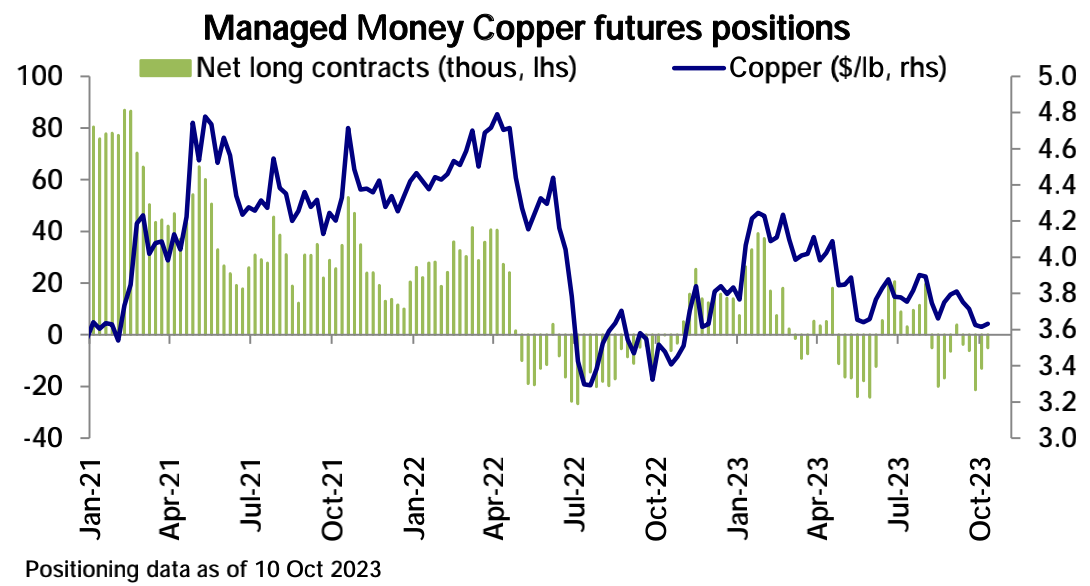

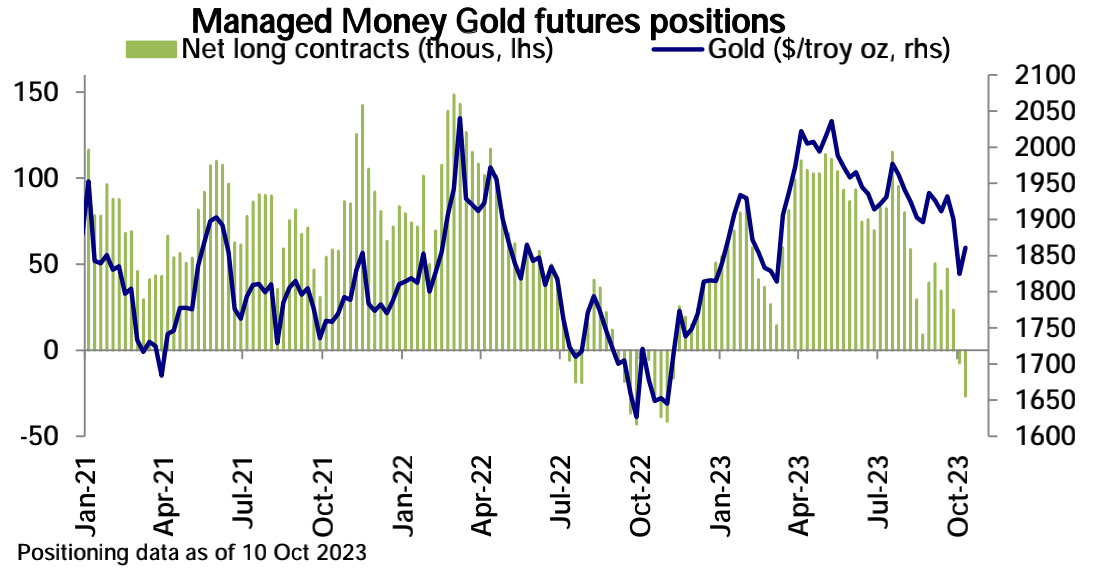

In the commodities sector, net long positions in oil have decreased, while net short positions in gold and silver have increased. Net short positions in copper have decreased:

Market Sentiment

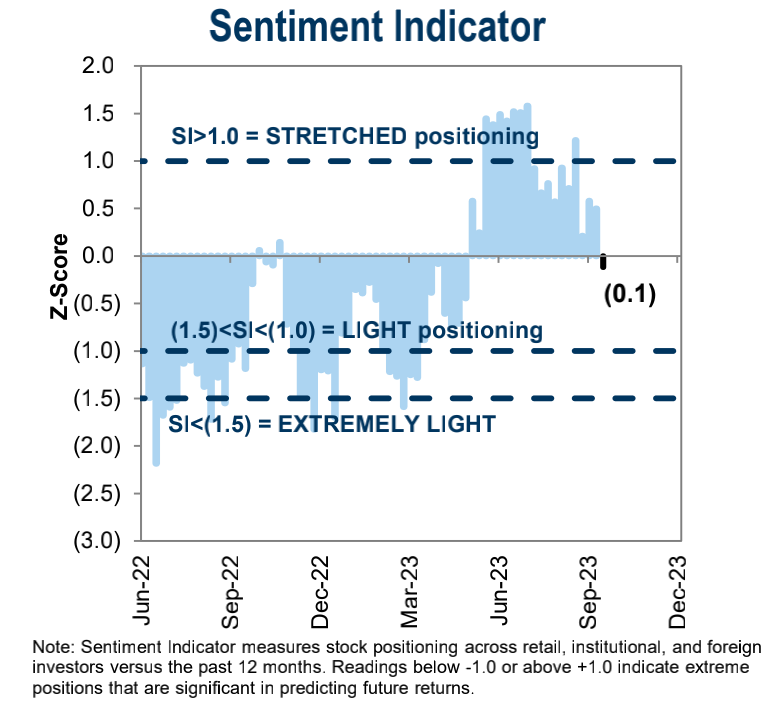

Goldman's institutional sentiment indicator has fallen to negative territory, the lowest level since late May:

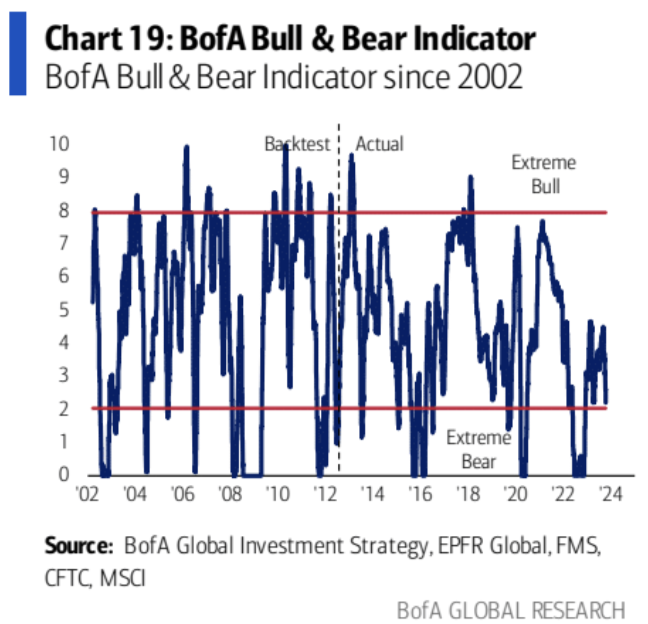

Bank of America's bull-bear indicator has further declined to 2.2, with below 2.0 indicating an overly pessimistic buying zone:

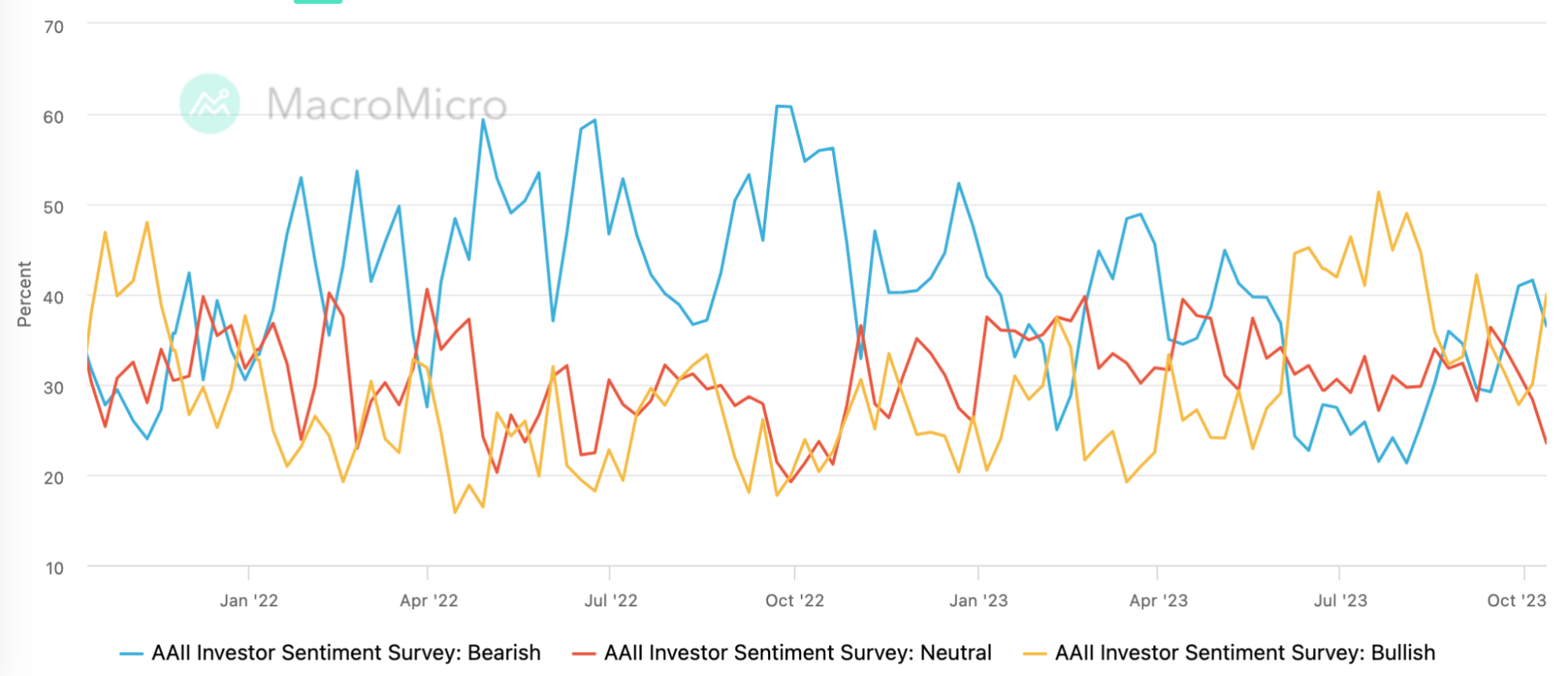

AAII survey: Bullish sentiment has risen significantly, bearish sentiment has decreased, and the proportion of neutral views has fallen to a one-year low:

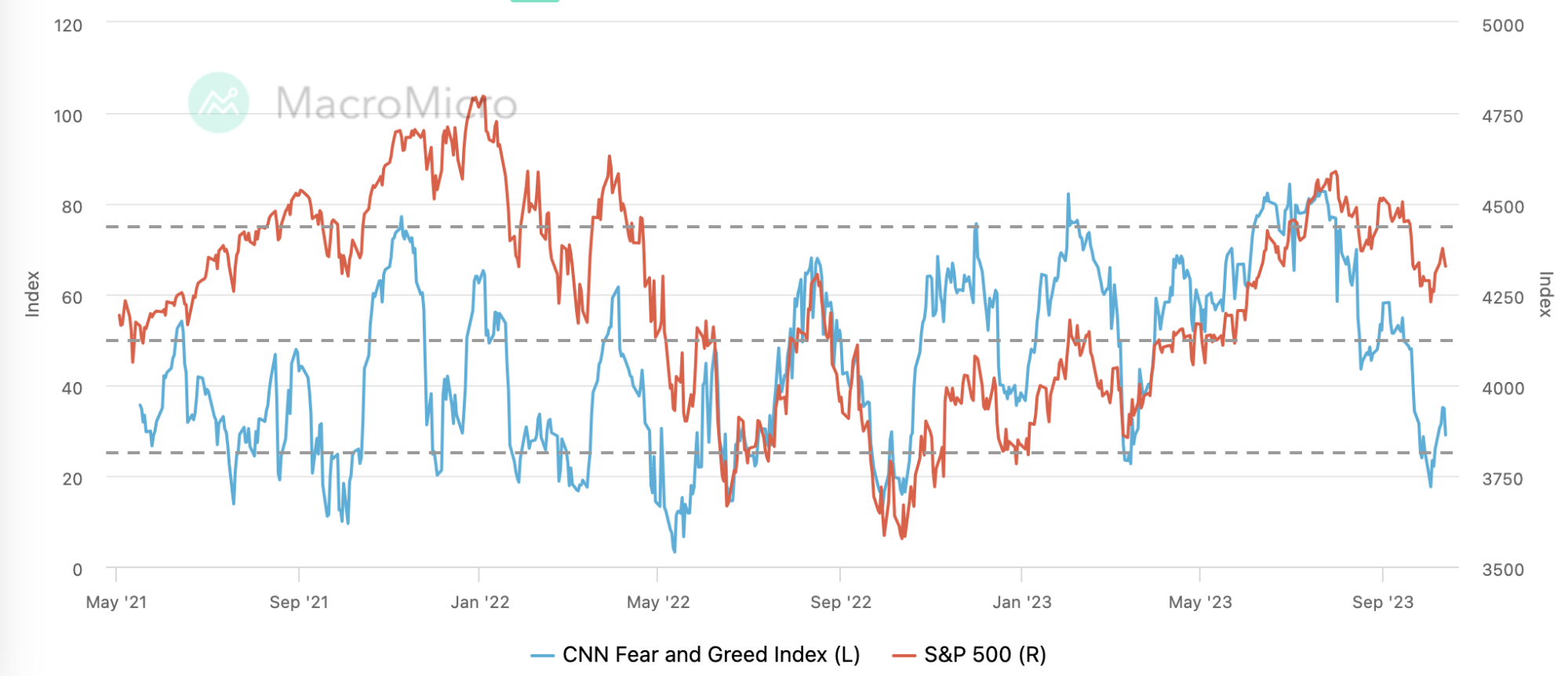

CNN's Fear & Greed Index has hovered at low levels with little change throughout the week:

Expert Opinions

【World War, the Most Dangerous Moment】

Bridgewater's Dalio published an article titled "Taking a Step Closer to International War" on Thursday, stating that the likelihood of the Israel-Palestine conflict escalating into a world war has reached 50%. "I believe this war carries a high risk of igniting different types of conflicts in many places, and its harmful effects are likely to spread beyond Israel and Gaza… The conflict between Israel and Hamas could ignite other bloody battles, and the possibility of a world war breaking out is now fifty-fifty." Dalio believes these two conflicts are part of a larger power struggle that will define a new world order.

Coincidentally, Jamie Dimon expressed concerns about the future global situation in JPMorgan Chase's Q3 earnings report this week: the Russia-Ukraine conflict and the Middle East conflict could have profound impacts on energy and food markets, global trade, and geopolitical relations. This could be the most dangerous moment in the world in decades.

【Goldman Sachs: Bond Supply is Not a Problem, Yields Will Not Rise Significantly】

Although the widening fiscal deficit has led to increased Treasury issuance, the current yield levels are already significantly above the potential for economic growth, making Treasuries sufficiently attractive to investors, so the increase in supply will not further push up yields. Additionally:

- Although the Fed is reducing its balance sheet, other central banks are still pursuing easing policies, putting downward pressure on yields.

- Slowing economic growth and falling inflation also help limit upward pressure on yields.

- The rise in yields will itself drag on economic growth, creating a self-stabilizing effect.

- A reduced preference for stocks among investors will also lead to an increased preference for fixed income, limiting significant upward movement in yields.

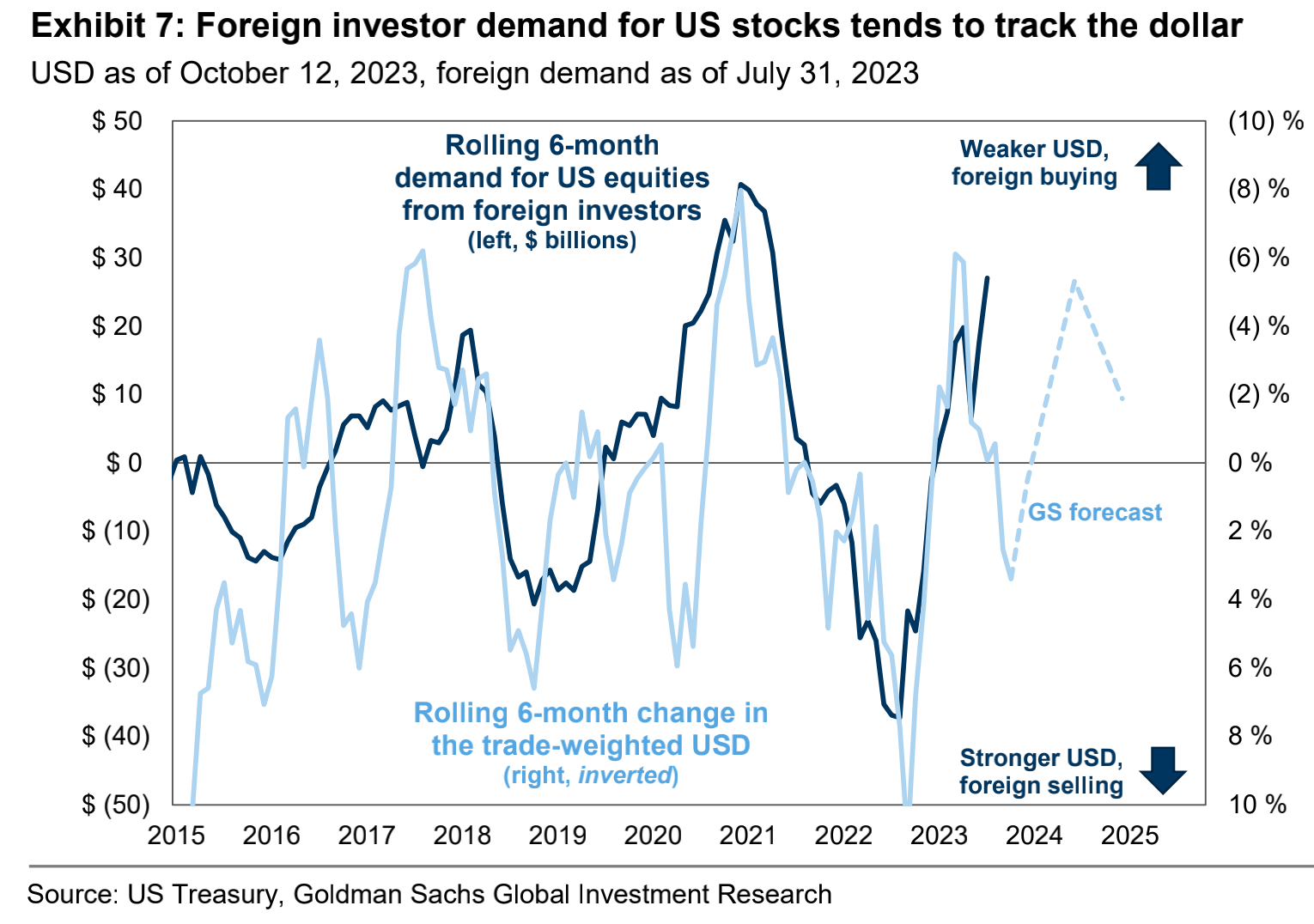

【Goldman Sachs: Dollar Peak Will Help Foreign Funds Buy U.S. Stocks】

Historical data shows a clear negative correlation between foreign investment in U.S. stocks and the dollar index.

GS expects the dollar to weaken moderately before the end of 2024, which means that foreign investors' demand for U.S. stocks will remain positive. GS predicts that foreign investors will net buy $150 billion in U.S. stocks in 2023, with an additional $100 billion in 2024.

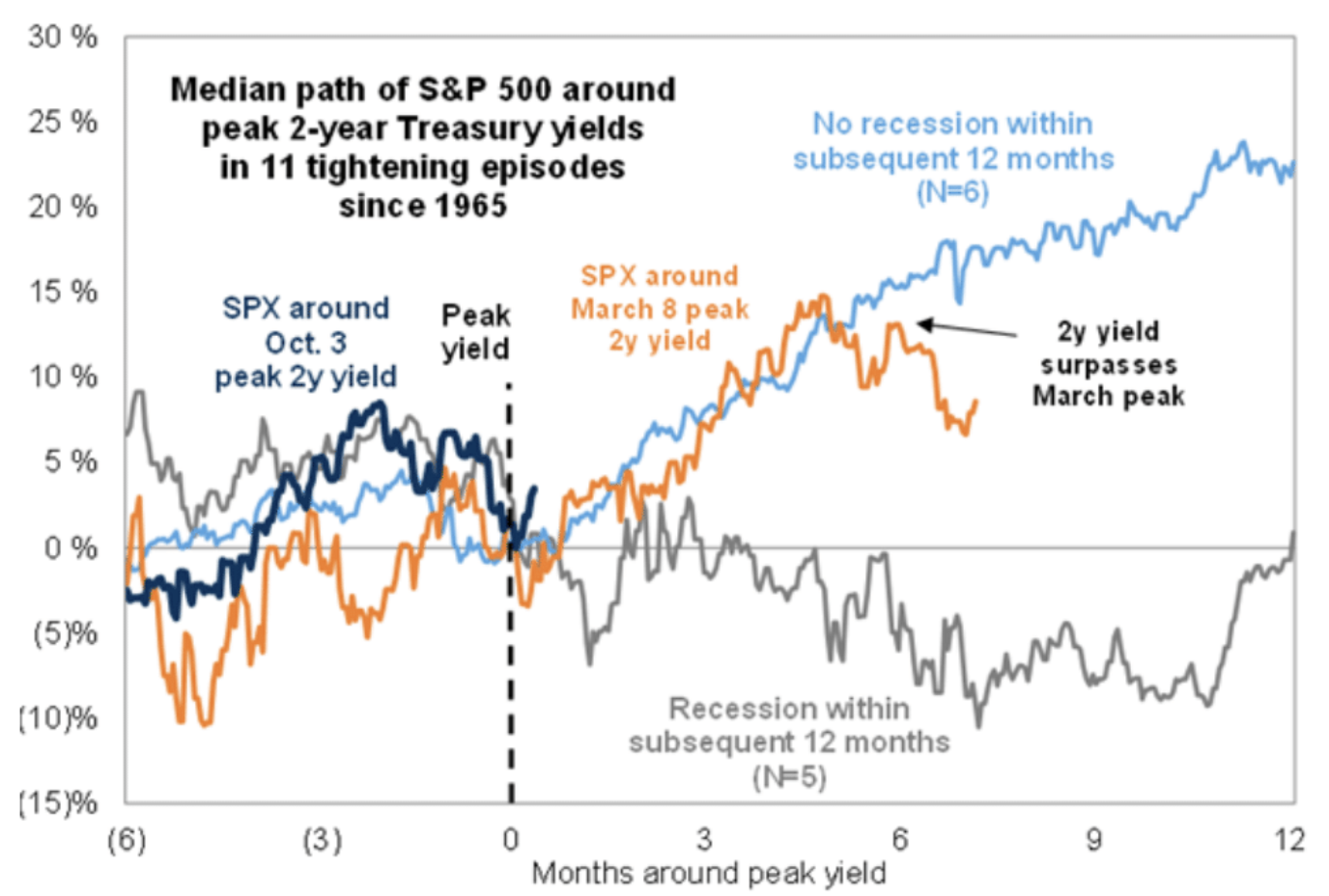

【GS Ryan Hammond: Historical Evolution of Recessionary and Non-Recessionary Stock Markets】

History shows that if the economy avoids recession, U.S. stocks typically rebound after the "hawkish peak" (see chart below). In the 11 tightening cycles since 1965, if the economy did not enter recession, the S&P 500 index usually rebounds 8% in the following three months after the peak of the 2-year U.S. Treasury yield and 23% in the following 12 months. If a recession occurs in the following 12 months, stocks typically decline.

"We assume the U.S. achieves a soft landing, and we predict the S&P 500 index will rise to 4,500 points (+3%) by the end of the year and to 4,700 points (+8%) in the first half of 2024. Although we expect stocks to continue to rise from current levels, our predicted gains are lower than historical performances after previous 'hawkish peaks.' Compared to previous Fed tightening cycles, current valuation levels are higher, and expected earnings growth is slower. Absolute valuation levels are currently ranked in the 85th percentile historically, above the average levels at the end of previous Fed tightening cycles (excluding the tech bubble period). The yield gap between stocks and real yields (as an alternative indicator of ERP) has also narrowed to 332 basis points, ranking in the 88th percentile historically, the lowest since 2002."

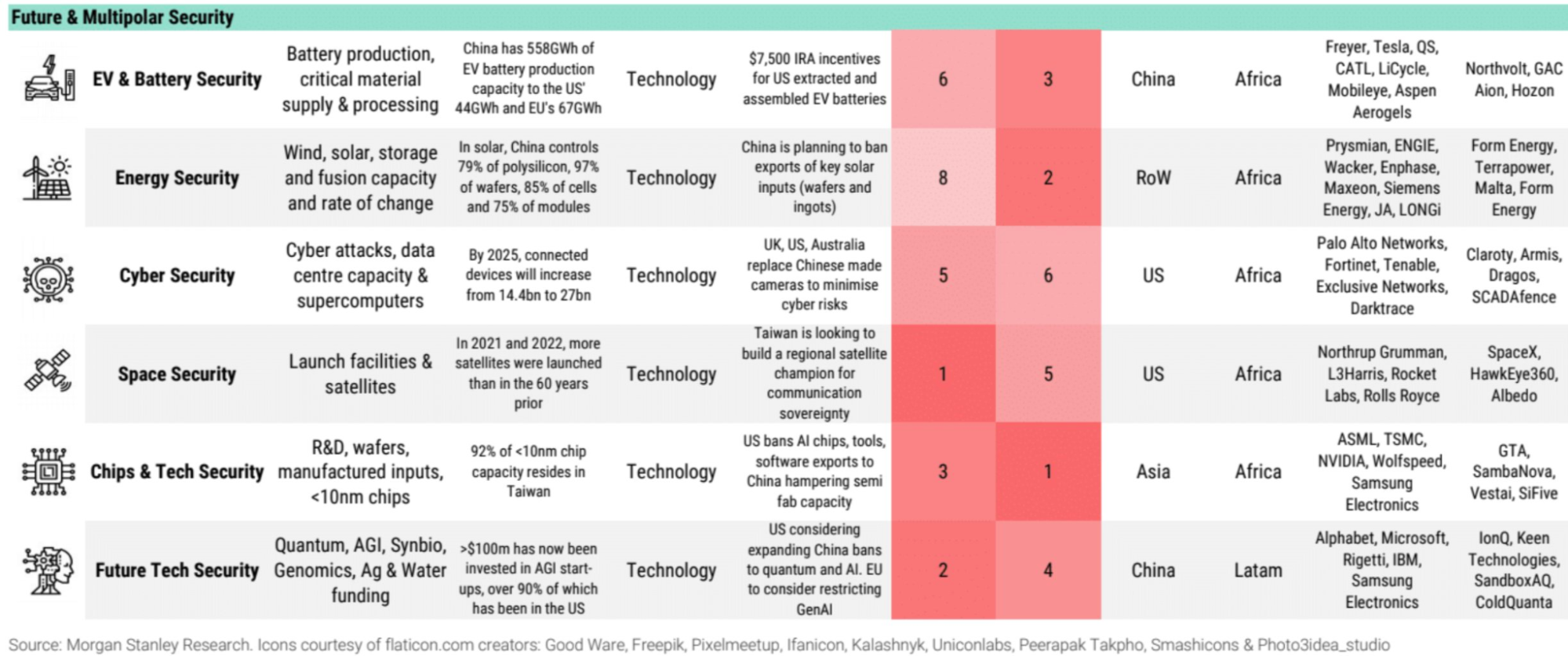

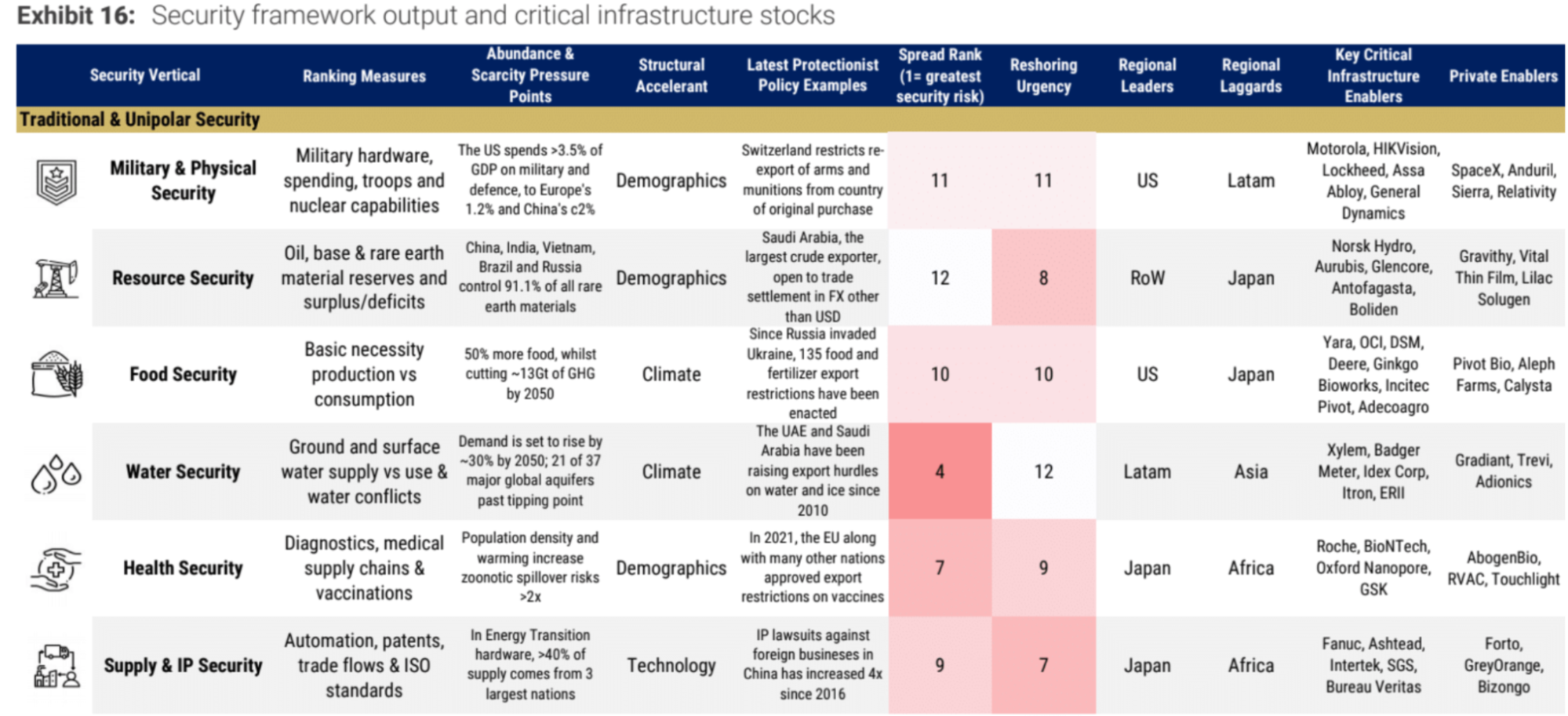

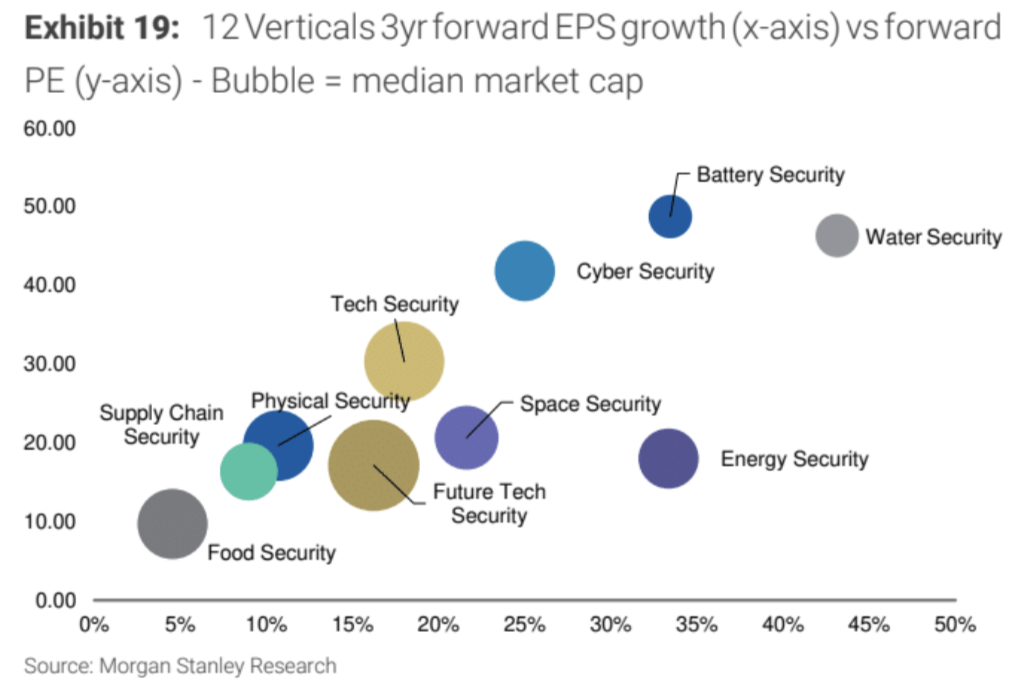

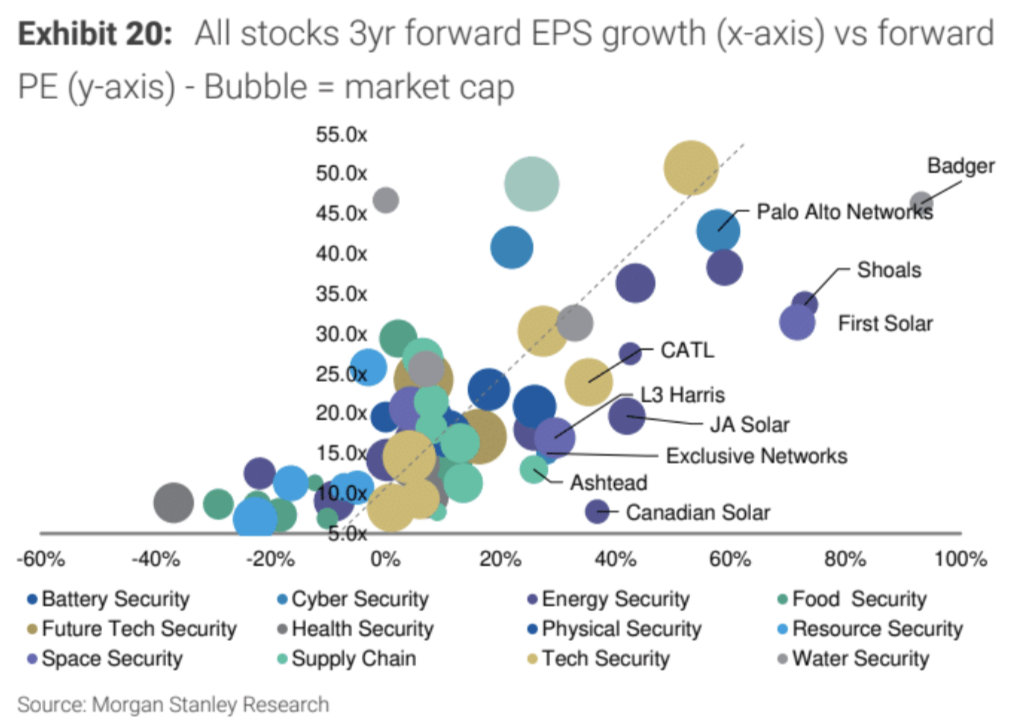

【Morgan Stanley: 80 Strategic Safety Targets in a Multipolar World】

Including industries such as military, resources, food, aerospace, semiconductors, and batteries. The areas they operate in align with the government's goal of enhancing strategic autonomy, so they are expected to achieve sustained growth in a multipolar world.

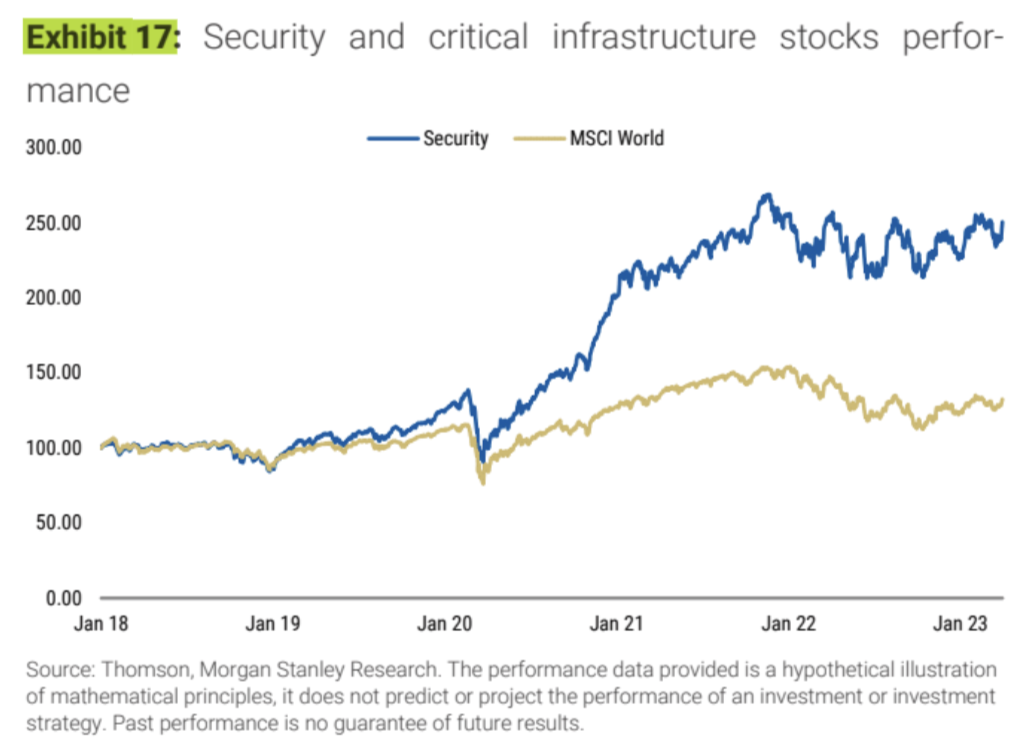

The results of the simulated portfolio backtest far outperform the market:

The valuation and growth expectations of industries and individual stocks indicate that the further to the bottom right, the greater the potential:

Among the 80 key infrastructure companies selected in this report, some Chinese companies are included, mainly concentrated in the following areas:

- Hikvision in the physical security sector. Hikvision is one of the world's largest suppliers of video surveillance products and solutions, holding a significant market share in China.

- China Nonferrous Metal Industry Co., Ltd. in the natural resources security sector. This company is one of the largest producers and processors of nonferrous metals in China.

- CATL in the new energy vehicle and battery security sector. CATL is the largest power battery manufacturer in China and is technologically leading in lithium batteries.

- Baidu in the future technology security sector. Baidu provides internet search, cloud services, and other services to customers in China and globally through artificial intelligence technology.

Risk warning Risk warning

Risk warning Risk warning