MIIX Capital Research Monthly Report

ETFs drove and dominated the market in February, with market performance centered around BTC and ETH. Occasional sector rotations further propelled a comprehensive rise in tokens. Accompanied by the UNI proposal, the long-dormant DEFI sector also saw a full rebound; the MEME coin sector began to show a new round of wealth creation effects; and the BTC Staking ecosystem quietly emerged amidst the token surge and market frenzy.

ETFs drove and dominated the market in February, with market performance centered around BTC and ETH. Occasional sector rotations further propelled a comprehensive rise in tokens. Accompanied by the UNI proposal, the long-dormant DEFI sector also saw a full rebound; the MEME coin sector began to show a new round of wealth creation effects; and the BTC Staking ecosystem quietly emerged amidst the token surge and market frenzy.Author: MIIX Capital

1. Macroeconomic Perspective

1.1 Expected Rate Cut in June by the U.S., Market Attitude Optimistic

The U.S. Department of Labor reported a significant increase in non-farm payrolls in January, reaching 353,000, the largest monthly increase since January 2023, far exceeding the estimated 185,000 and the previous value of 216,000. This strong employment market performance raised concerns in the market about potential inflation, a worry that was later confirmed by the year-on-year growth data of the Consumer Price Index (CPI) released on February 13, which showed a 3.1% increase in January CPI, surpassing the market expectation of 2.9%.

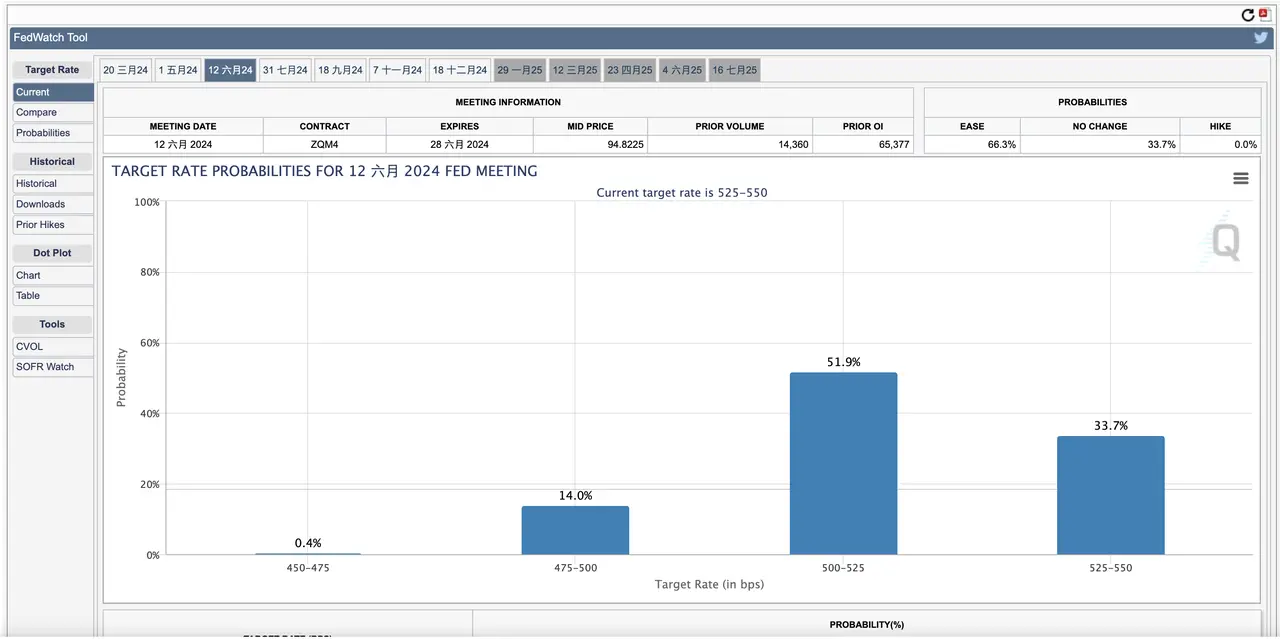

FedWatch

From FedWatch data, it can be seen that despite some prior expectations for a rate cut, the latest data and analysis indicate that the market generally expects the Federal Reserve (Fed) to begin cutting rates only in June.

Additionally, Goldman Sachs has adjusted its expectations, no longer anticipating a rate cut in May, but instead forecasting four rate cuts this year, down from the previous expectation of five. This adjustment reflects a reassessment of the market regarding the sustained growth of the U.S. economy and inflation pressures.

From market performance, despite the current level of inflation in the U.S. economy, it has not suppressed the rise of the stock and crypto asset markets. The market remains optimistic about future economic developments and monetary policy adjustments, expecting that the Federal Reserve will be able to find an appropriate balance between controlling inflation and promoting economic growth.

1.2 BTC Price Surge Mainly Driven by ETF and MicroStrategy

BTC prices have surged, rising continuously from $43,000 at midnight on February 8 to nearly $64,000, an increase of 32%.

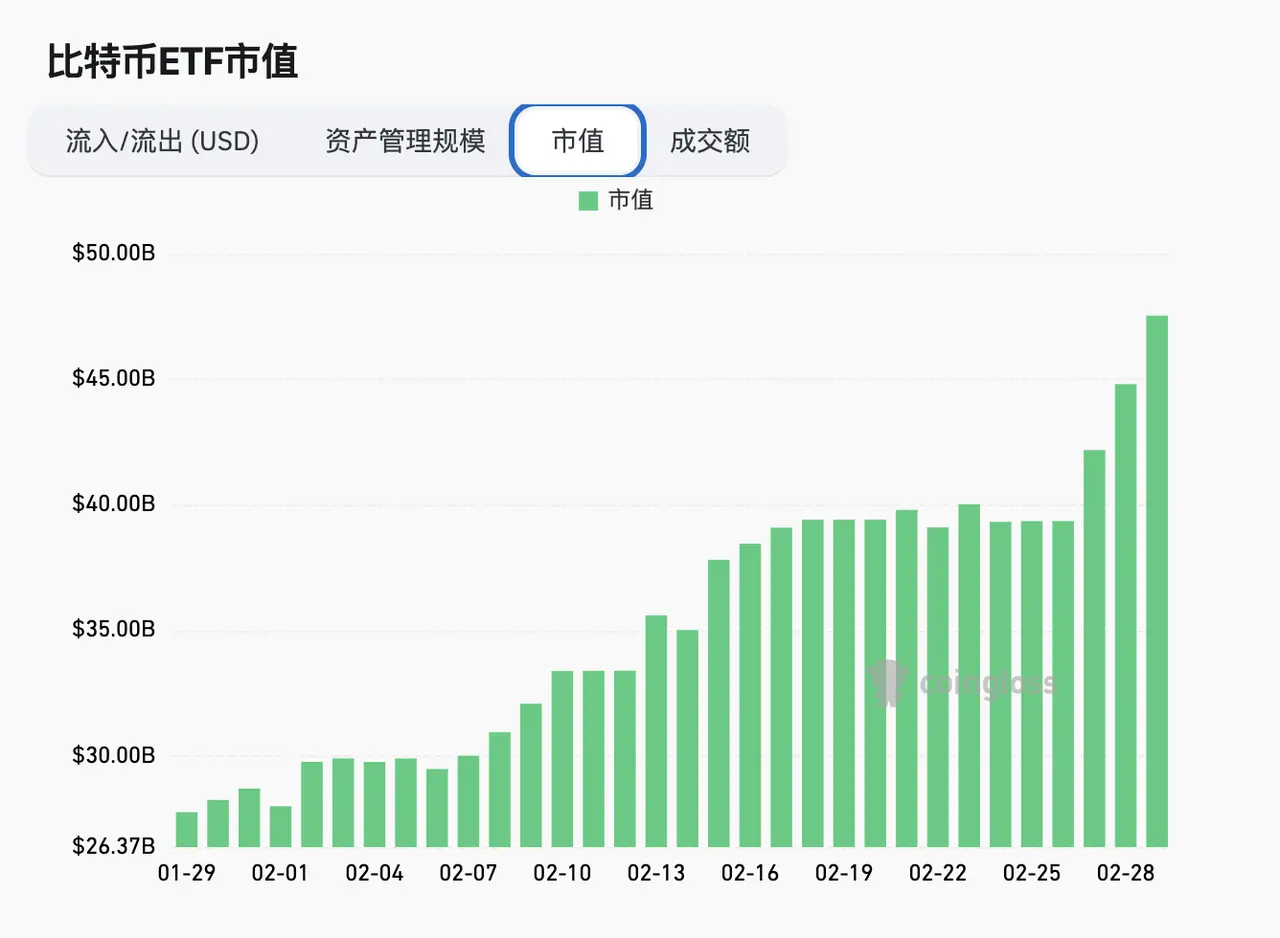

coinglass Bitcoin ETF Overview

From the perspective of ETF inflows, the timing of the price increase overlaps with the inflow of ETF funds, highlighting the driving effect of ETFs on Bitcoin prices. As of the 29th, the total managed assets of 11 ETFs have reached $42.238 billion, accounting for 3.81% of Bitcoin's total market capitalization, a figure that exceeds the amount of Bitcoin held by Binance exchange wallet addresses.

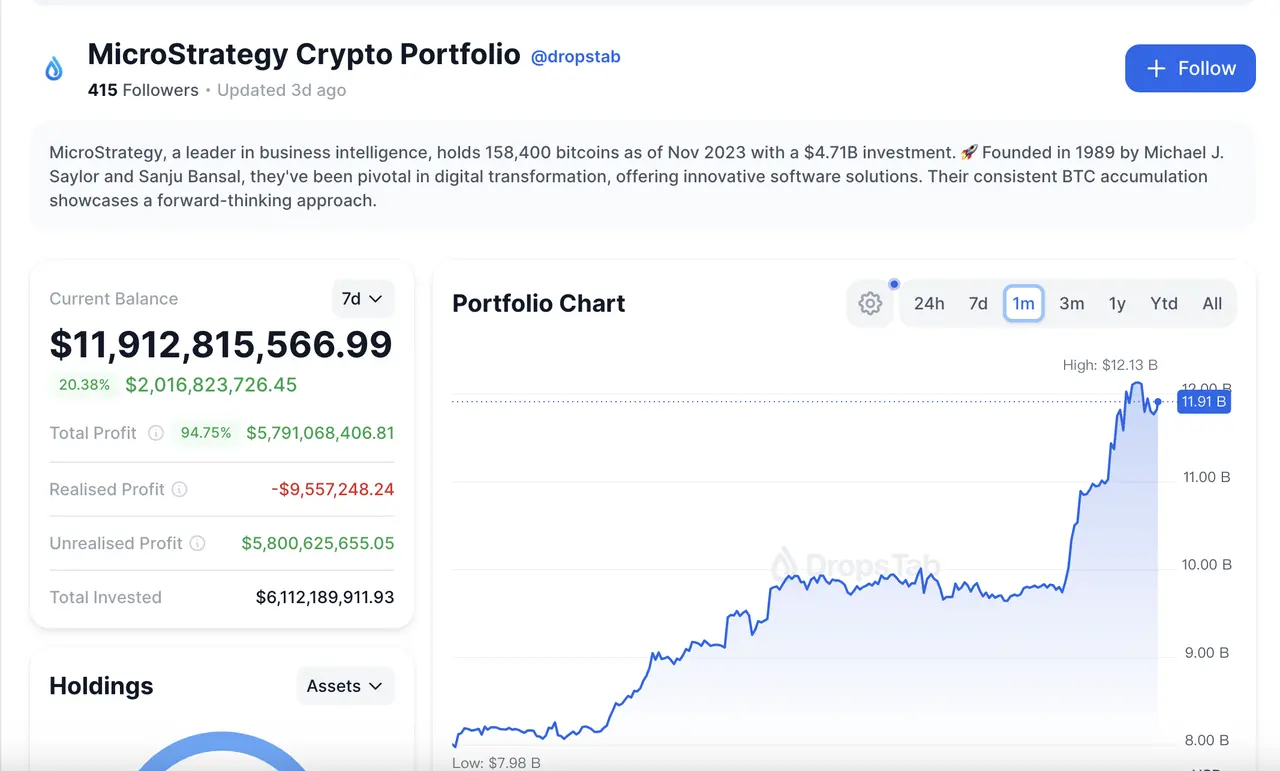

Moreover, MicroStrategy is also a significant source of capital inflow into the BTC market. On the 26th, MicroStrategy founder Michael Saylor stated on his social platform that MicroStrategy purchased 3,000 Bitcoins between February 15 and 25, at an average purchase price of $51,813. As of now, MicroStrategy holds a total of 193,000 Bitcoins, with assets reaching a peak of $11.9 billion.

1.3 ETH Spot ETF Becomes the Next Market Focus

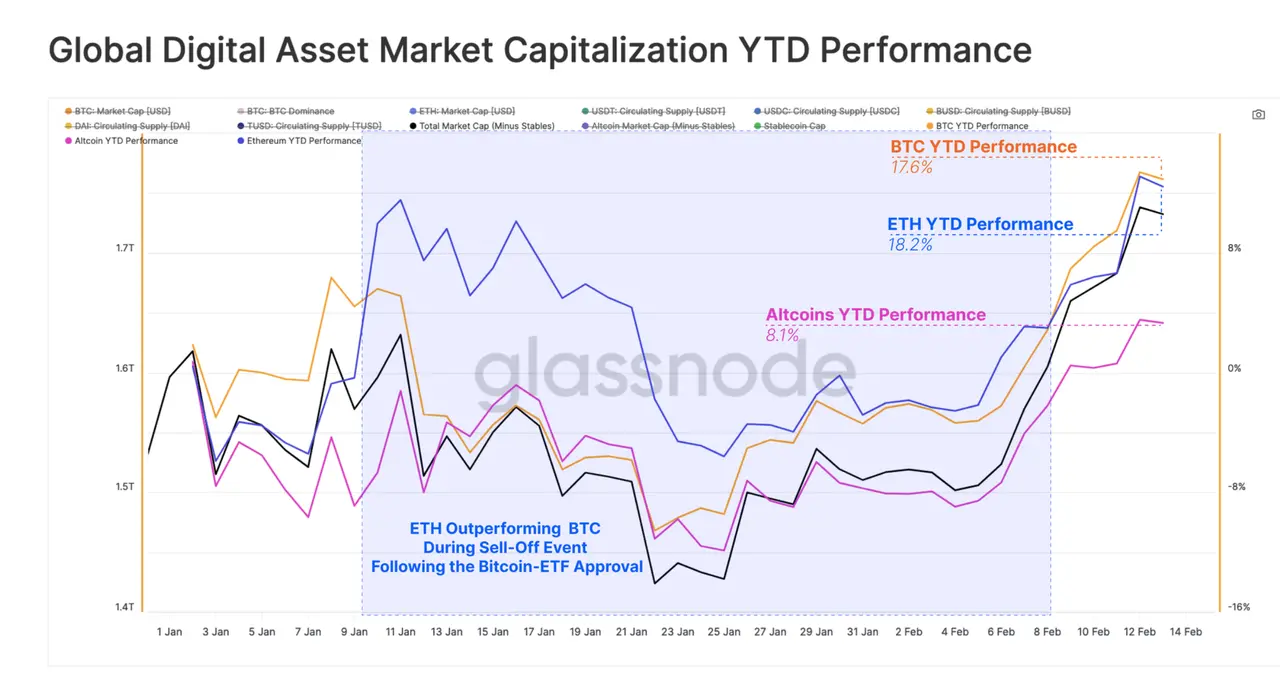

glassnode Global Digital Asset Market Year-To-Date (YTD) Market Capitalization Performance

The approval of the BTC spot ETF has injected tremendous confidence into the market, making the launch date of the ETH spot ETF one of the current market focuses. At the same time, ETH's price increase has begun to lead and surpass BTC, with the market shifting its attention to ETH. The most important date currently is May 23 (the date the SEC will make a final decision on VanEck's ETH spot ETF). If the ETH spot ETF is approved subsequently, it will represent another significant victory for the crypto market, allowing more traditional investors to participate in the ETH market through this traditional investment tool, bringing new funds into the crypto market.

On a macro level, despite facing challenges from rising inflation, the market performance in February remained unaffected, still reaching new highs under the strong push from ETF funds. Currently, the market is more focused on the delay of the rate cut timing rather than the possibility of continued rate hikes. As the selling pressure from grayscale investments gradually diminishes, we will continue to monitor market capital inflows to see if BTC can continue to create new historical highs.

2. Industry Data

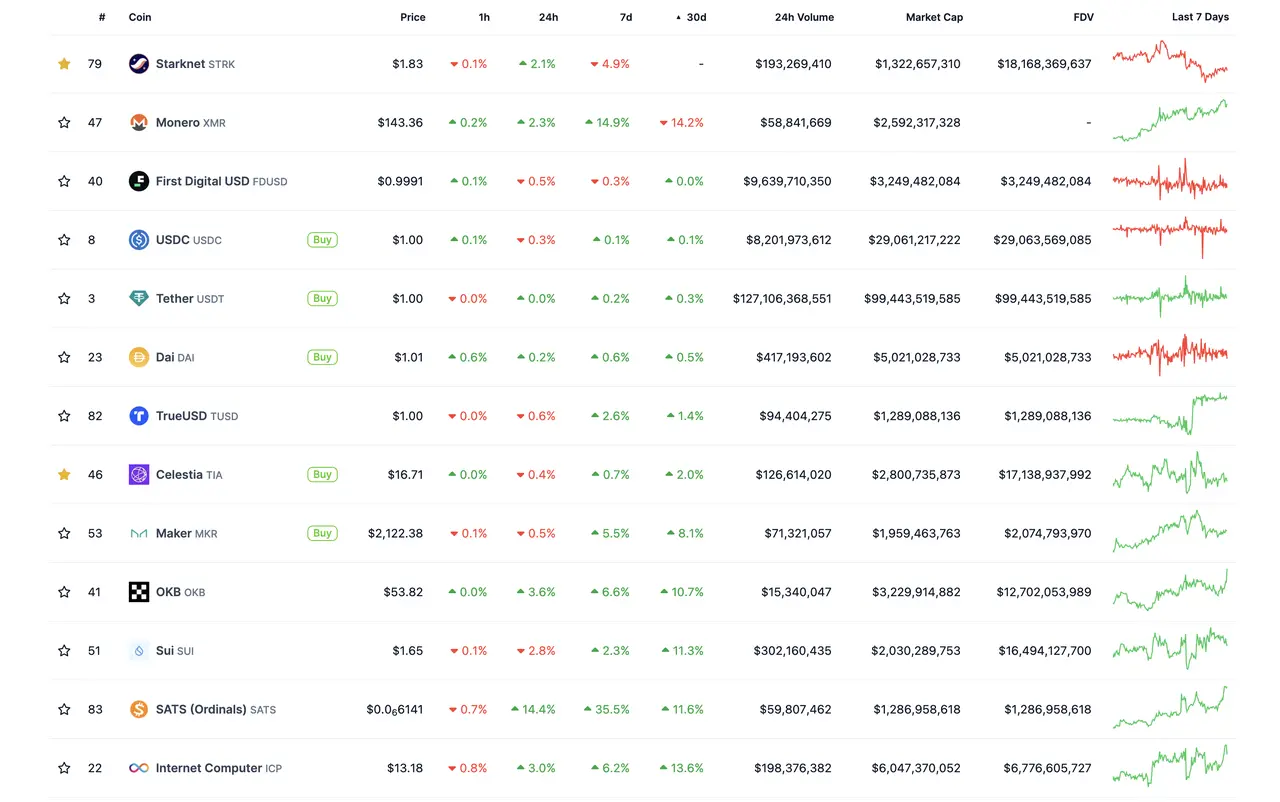

2.1 Market Capitalization & Ranking Data

Both BTC and ETH have seen nearly a 50% increase in the past 30 days, primarily due to actual fund inflows from ETFs and expectations surrounding the ETH ETF. However, for ETH, the hype surrounding the Dencun upgrade on March 13 has not yet shown a significant market reaction. Currently, the market predicts that the approval time for the ETH spot ETF will be before May 23.

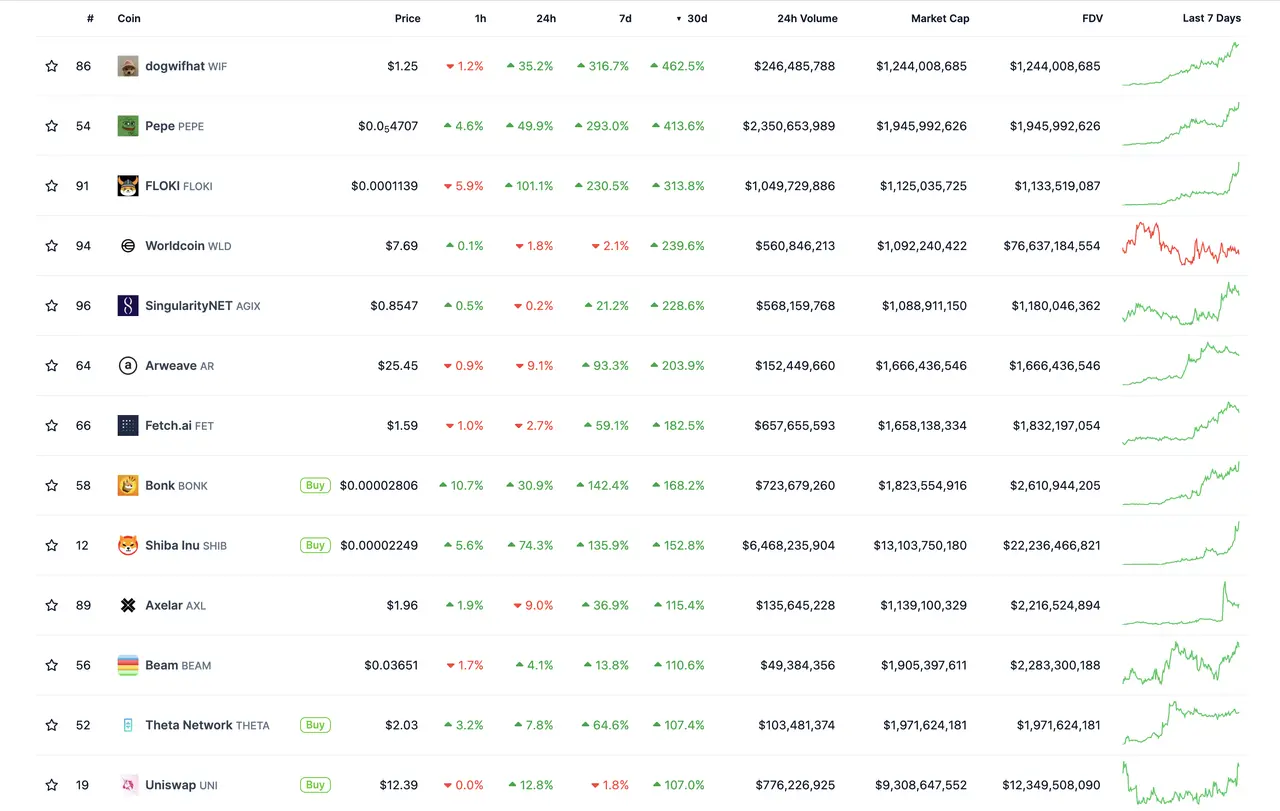

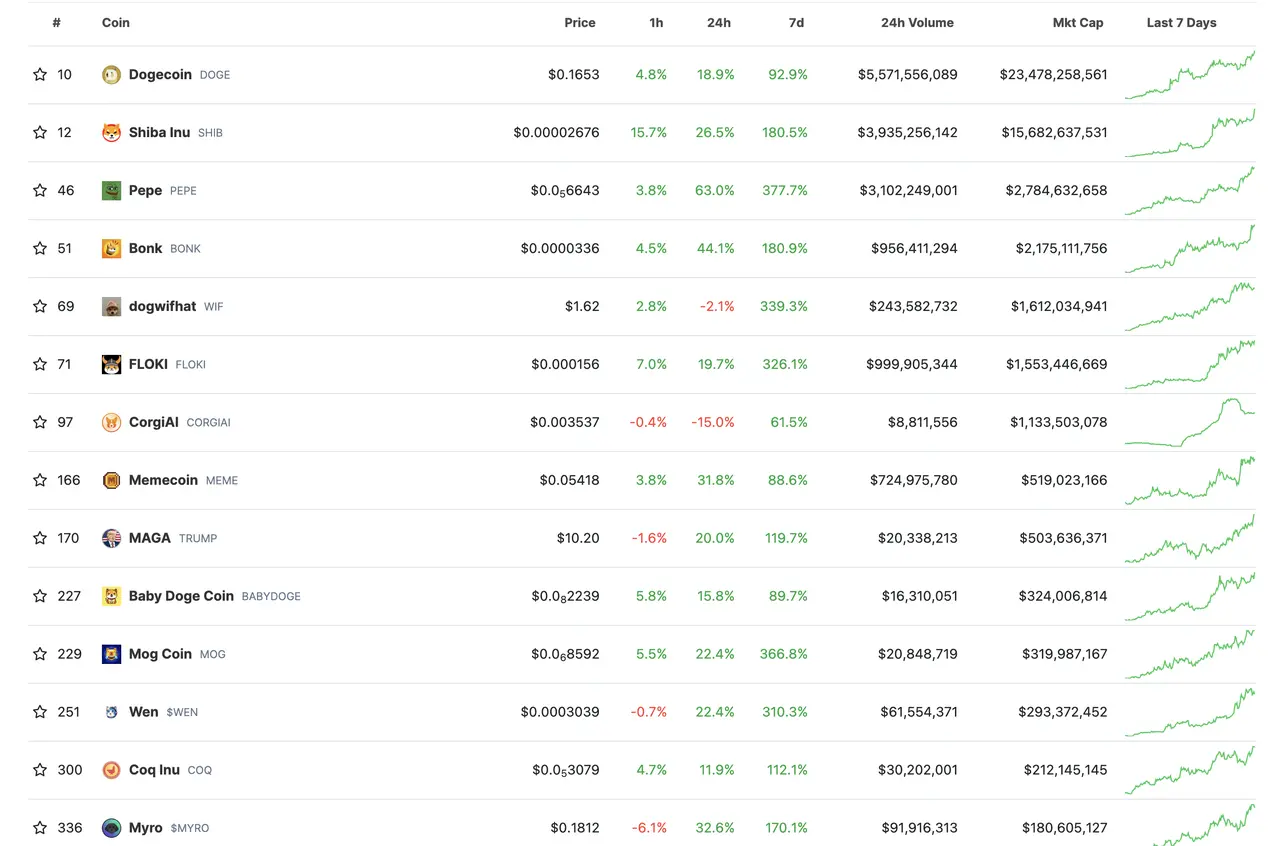

Among the top 100 tokens by market capitalization, the tokens with the highest gains in February were WIF (+462.5%), PEPE (+413.6%), and FLOKI (+313.8%), with the upward performance mainly concentrated in the last week of February, showing clear signs of sector rotation. Currently, the upward momentum is concentrated in the MEME coin sector, which differs significantly from past cycles, especially during bull markets.

Note: It is recommended that investors remain cautious when the sector rotates to MEME coins, as in past cycles, MEME coins are usually the last sector to rotate, indicating that this round of increases is nearing a phase-end.

Among the top 100 tokens by market capitalization, only Monero saw a decline of 14.2% in February (StarkNet launched less than 30 days ago), primarily due to Binance's announcement on February 6 that it would delist XMR, Aragon, Multichain, Vai, and other tokens on February 20. Binance stated that "these tokens do not meet the expected standards."

About WIF (dogwifhat)

dogwifhat is a MEME coin on the Solana chain, which began planning in April 2023 and had been trading sideways around $0.15 for about three months. As of March 2, 2024, its market capitalization has reached $1.2 billion, making it a dark horse in this round of MEME market surge, and its entire website design is also very interesting. (This token has not yet been listed on Binance)

About PEPE

PEPE is a MEME coin launched in April 2023, and it was the MEME coin with the largest increase during that round, reaching a peak of $0.00000372 on May 6, 2023. BTC also reached its recent peak shortly after, followed by an overall correction, sliding down to October 20, 2023. Recently, it restarted on February 5, 2024, reaching a historical high of $0.00000444, with a market capitalization of $1.863 billion.

About FLOKI

FLOKI was first listed in the summer of 2021, following reports that Tesla's founder bought a Shiba Inu and named it Floki. As a concept pet of Musk, FLOKI soared, and Musk often posts pictures of his pet on X. In the past month, it has also increased by more than three times.

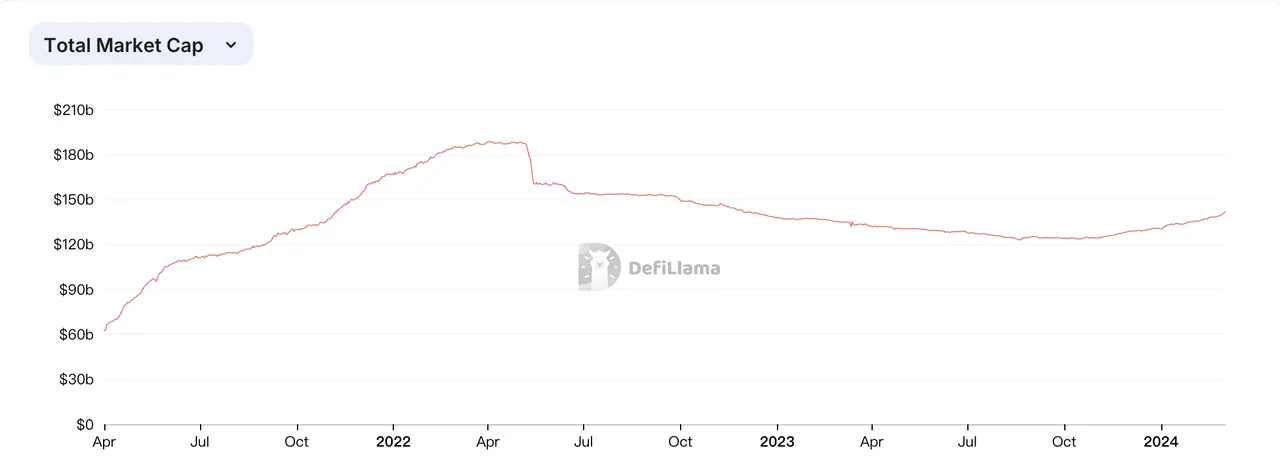

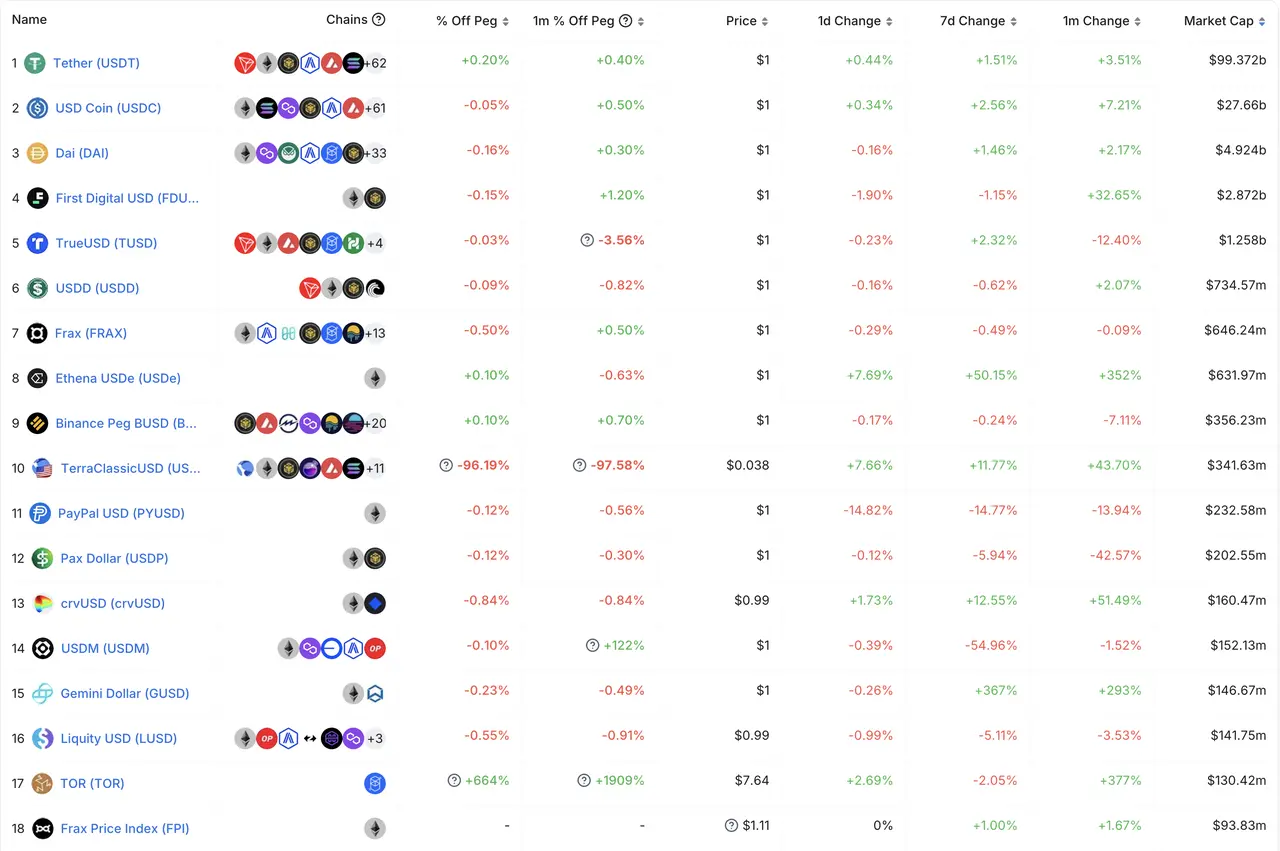

2.2 Stablecoin Inflows and Outflows

The number of stablecoins continued to grow in February, and the slope indicates that this growth may be accelerating, with the total amount of stablecoins reaching $141.2 billion. The fastest-growing stablecoin this month is FDUSD, similar to January (up 32.65% this month, up 20.41% in January). Based on this trend, it is expected that FDUSD will surpass DAI within a quarter, becoming the third-largest stablecoin.

FDUSD is issued by FD121 Limited, a subsidiary of the Hong Kong custodian company First Digital Limited, and is a stablecoin pegged to the U.S. dollar at a 1:1 ratio. The rapid growth of FDUSD is believed to be due to its listing on Binance, replacing BUSD's position.

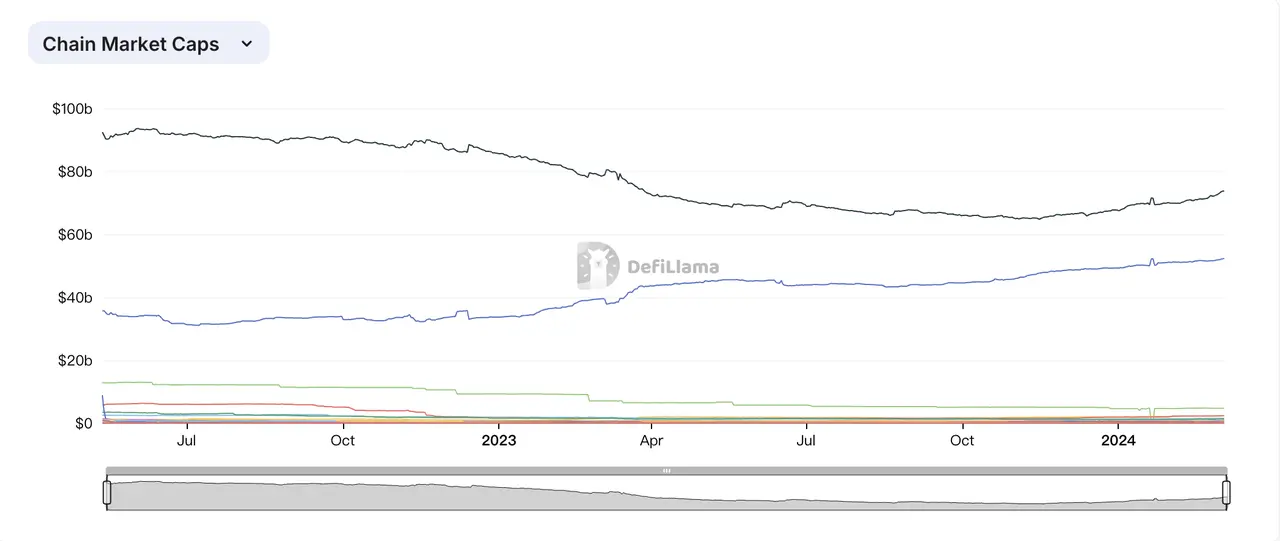

From the perspective of public chains: The stablecoins on Ethereum amount to approximately $73.7 billion, accounting for 52.2% of all public chain stablecoin reserves. Apart from Ethereum and Tron, which are the two major stablecoin public chains, other public chains have seen minimal growth.

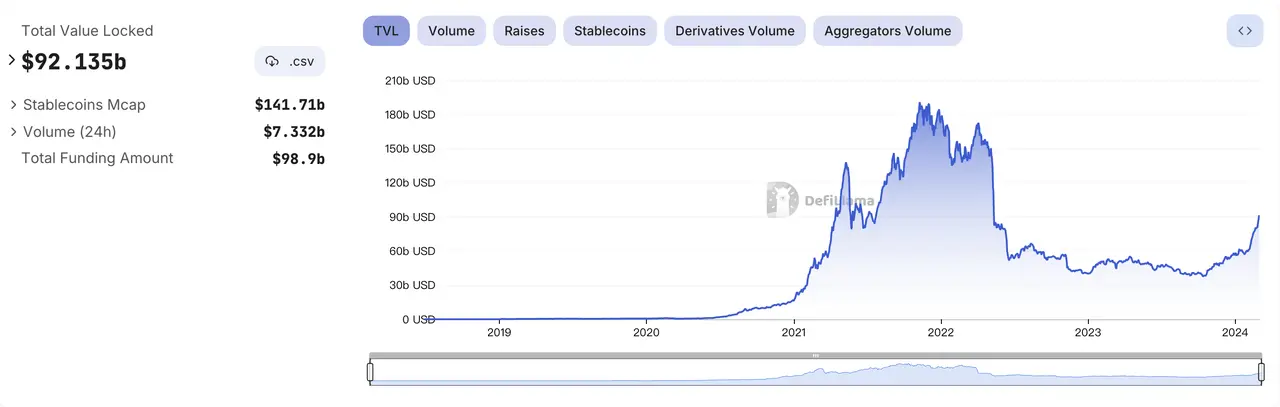

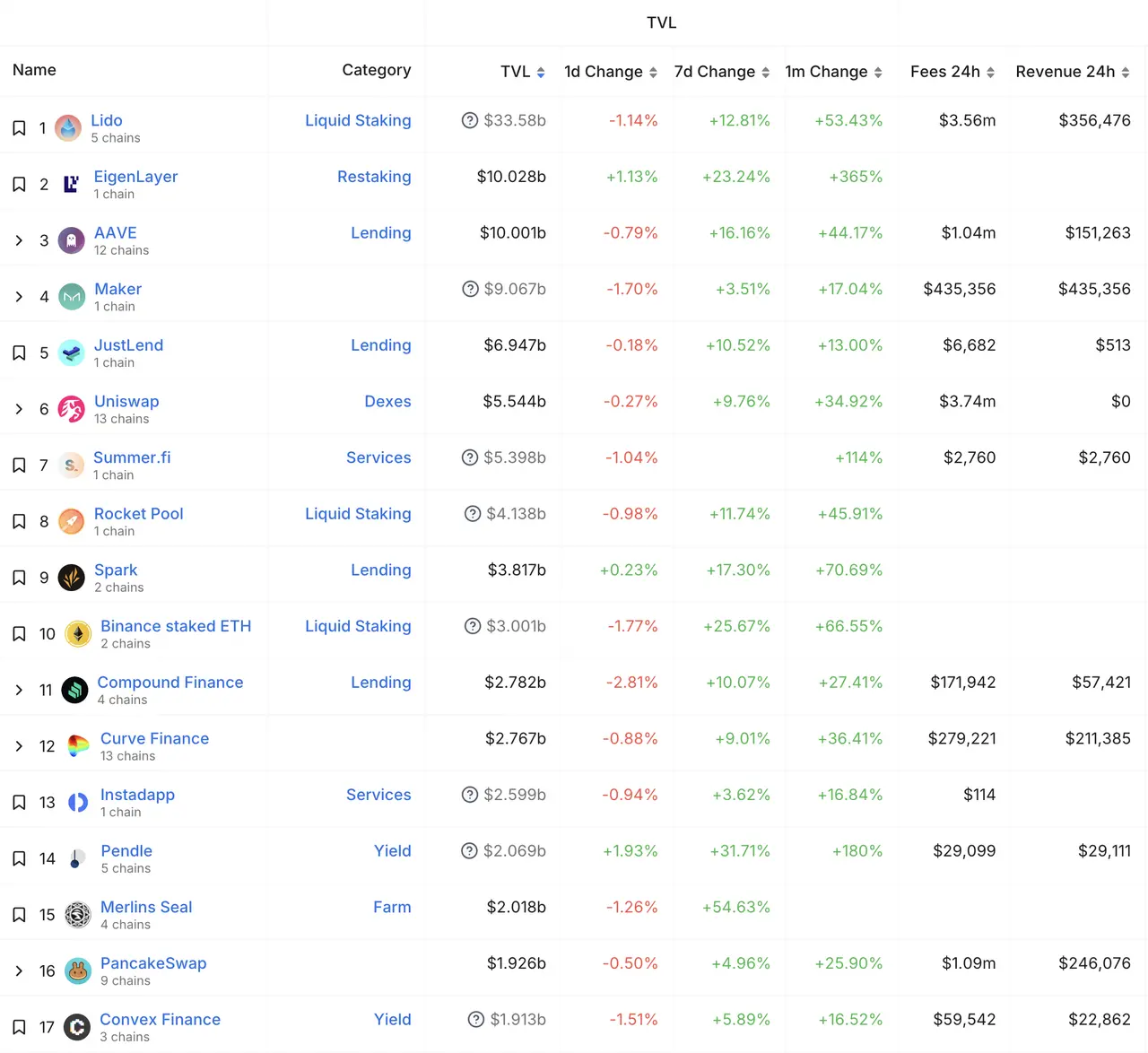

2.3 On-chain TVL Ranking

U-based

DefiLlama Data: The on-chain TVL has accelerated its rise alongside the increase in ETH prices.

Due to the significant increase in ETH and the Fee Switch proposal from Uniswap, the overall performance of the DeFi sector has been impressive, with the most notable EigenLayer project seeing its TVL surpass $10 billion, with a monthly increase of over 360%, surpassing the former second place, AAVE.

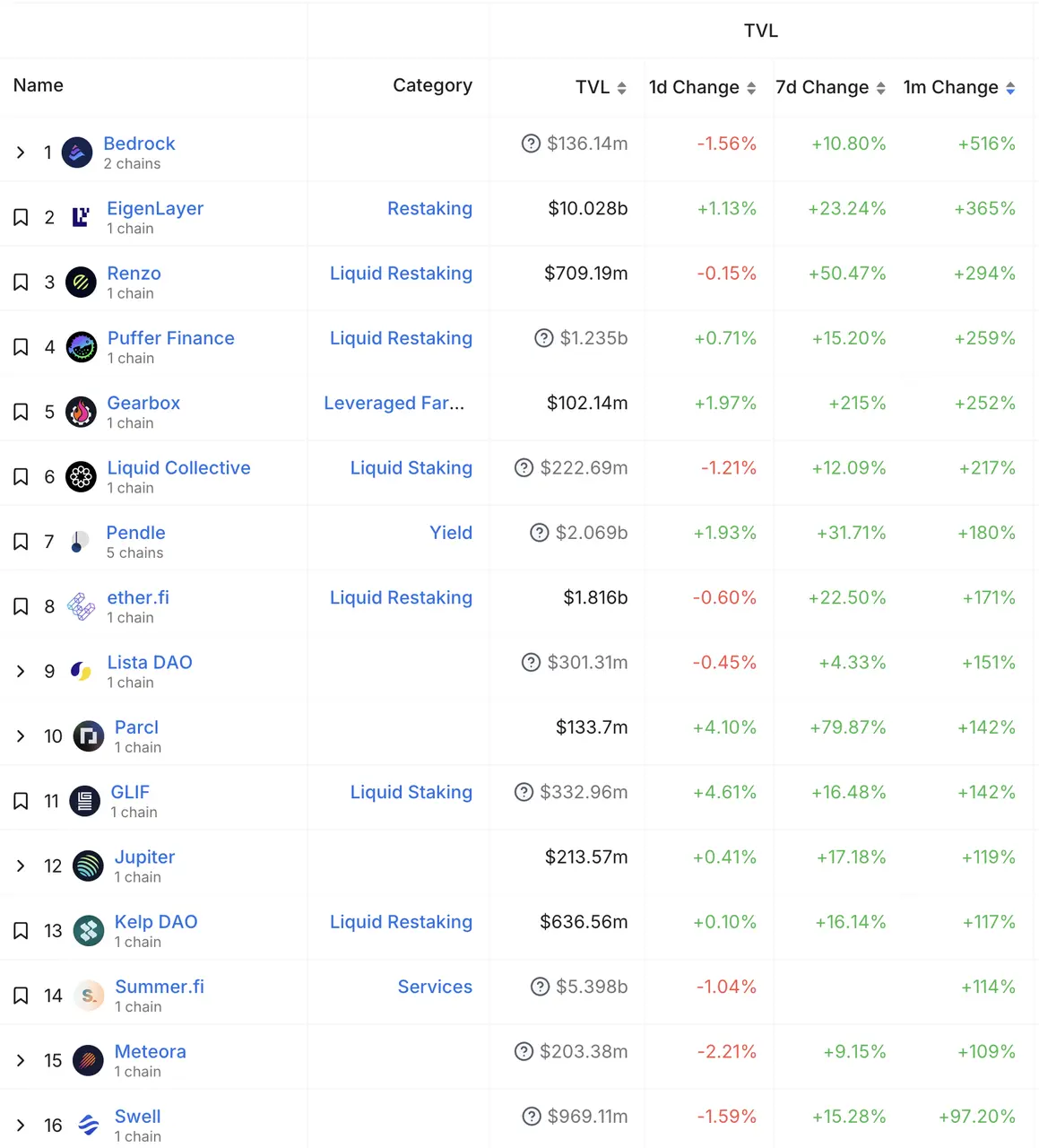

Defillama data: Among the 131 projects with a TVL above $100 million (up from 96 in January), the largest increase was seen in Bedrock. As the LRT market and Restaking narrative gradually heat up, the rigid demand for Pendle is also becoming apparent, especially for future institutions, which may find Pendle a good tool for hedging risks.

By DeFi category, the highest TVL ranking remains in the LSD sector, approximately $53.3 billion; Restaking projects based on LSD amount to about $10 billion; and LRT projects based on Restaking total about $5 billion.

By chain category, Bitcoin's TVL increased by 694%, reaching $2.43 billion, while Ethereum's TVL rose to $5.23 billion.

The significant increase in Bitcoin's ecosystem TVL benefits from its Layer 2 narrative, with many projects starting to support BTC staking and receiving funding from top VCs. This trend is expected to continue and manifest in the cycle market.

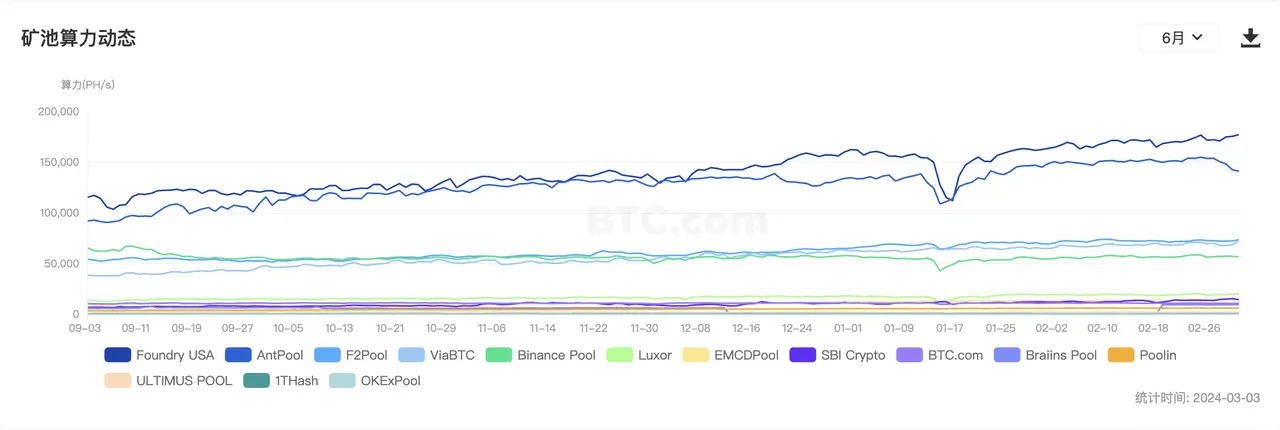

2.4 BTC/ETH Mining Pool Data

BTC Hashrate Continues to Rise Steadily

The growth of Bitcoin's mining pool data is shown in the above chart, with the total network hashrate now reaching 575.08 EH/s. Foundry USA, AntPool, and F2Pool rank as the top three in hashrate, with the mining pool's hashrate continuing to maintain a steady upward trend this month, increasing by 7.2% compared to last month. Currently, there are 7,044 blocks remaining until the halving, with the expected halving date on April 19, 2024, which is two days earlier than the previously estimated April 21.

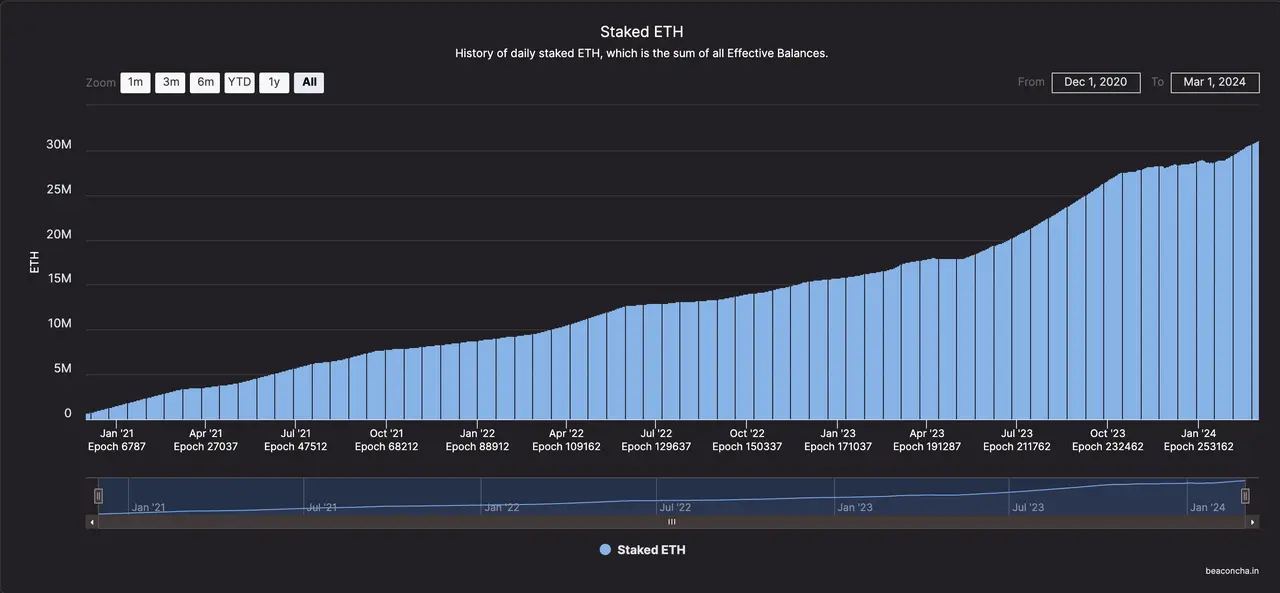

ETH Staking Volume Continues to Rise

https://beaconcha.in/charts/staked_ether

The amount of ETH staked continues to rise, currently accounting for 26% of the total, with a staking volume of 1.82 million this month. The Restaking market is still ongoing.

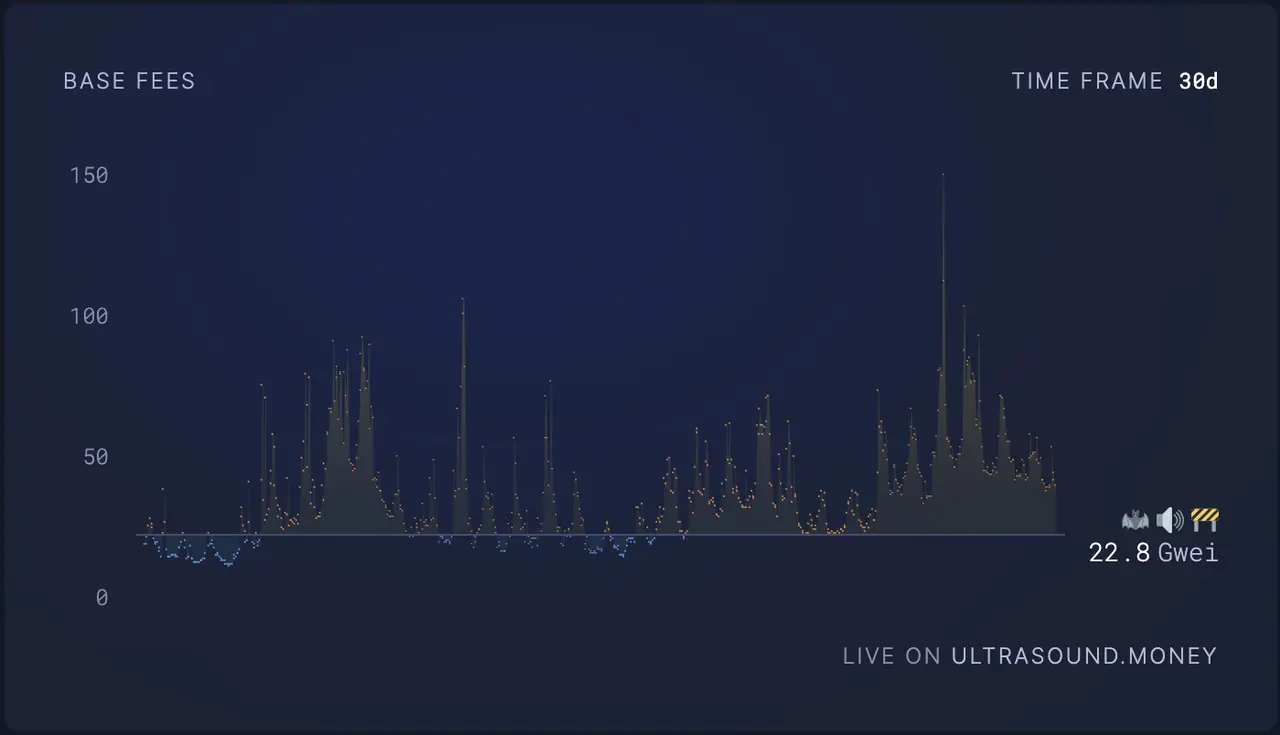

Additionally, ETH mainnet gas has significantly increased with the market, with a net burn of 46,839 ETH in February. It is expected that the high gas situation due to the Dencun upgrade and ETH ETF will continue until June, with the total amount of Ether expected to be below 120 million by then.

3. Market Trends

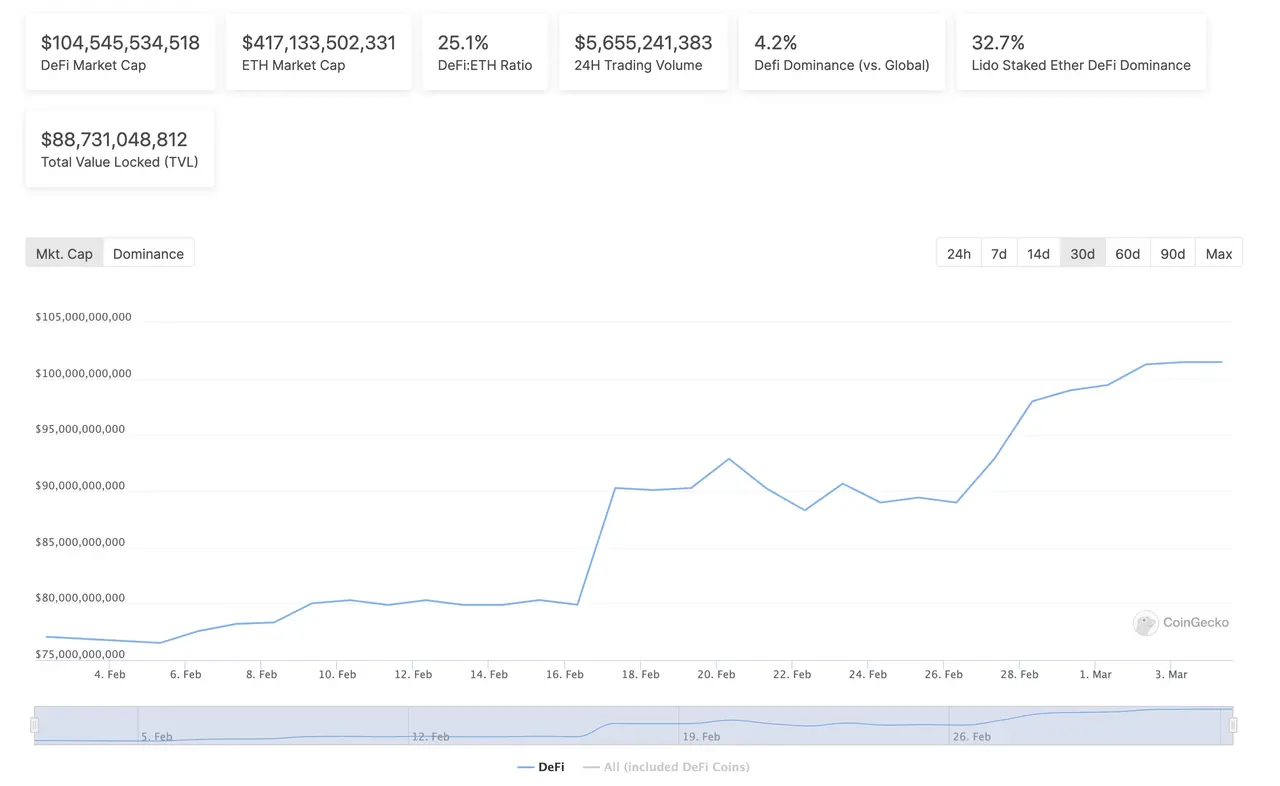

3.1 DeFi Sector Fully Recovers

https://www.coingecko.com/en/categories/decentralized-finance-defi

In February, the prices of DeFi project tokens saw significant increases. According to Coingecko data, the market capitalization of DeFi category tokens increased by 31% over the past 30 days, with Uniswap rising by 100%. This was mainly due to the Uniswap Foundation's fee switch proposal, which rekindled market interest in the DeFi sector, leading to a substantial rise in the prices of the overall DeFi category.

3.2 MEME Sector Rotates Upward

The recent market rally has sequentially experienced rotations through mainstream coins, AI, DePIN, GameFi, DeFi, and MEME sectors. In February, MEME coins like Dogecoin, Shib, and PEPE all rose over 300%, showing a clear wealth effect. However, the MEME coin market is highly volatile, and recent market makers for SHIB have primarily focused on selling, so investors should remain cautious.

3.3 BTC Staking Ecosystem Begins to Emerge

https://x.com/MerlinLayer2/status/1763783422529695862?s=20

Using BTC staking as an underlying asset, leveraging BTC's market capitalization consensus, and introducing BTC ecosystem narratives and airdrop expectations have rapidly absorbed BTC to increase TVL, becoming a highly anticipated business model. Currently, Merlin Chain's TVL has reached $3 billion, with BTC accounting for 53% and ORDI accounting for 33%. Consequently, many BTC Layer 2 projects have begun to gain attention, such as Babylon, which received investment from Binance, using BTC for re-staking to ensure the security of the Cosmos ecosystem chain. The broad prospects of the BTC staking sector are increasingly recognized, and it is recommended to keep an eye on it.

4. Investment and Financing Trends

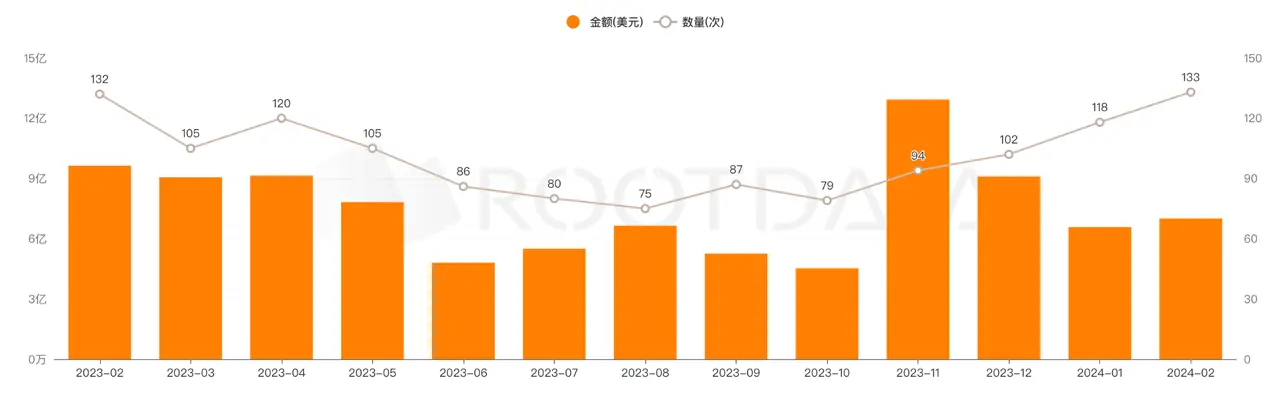

In February 2024, the crypto market completed a total of $700 million in financing, slightly up from the previous period's $695 million, an increase of 0.67%. The public data is as follows:

- 134 financing events, a year-on-year increase of 55.81% (118 projects in January 2024);

- 6 acquisition events, a year-on-year increase of 20%, indicating an increase in acquisition activities;

- The average financing amount was $7.2193 million, a year-on-year decrease of 10.74%;

- The median financing amount was $4 million, a year-on-year increase of 19.4%.

Although the average financing amount has declined, the number of financing events, acquisition events, and median financing amounts have all increased, indicating a rise in market activity and investor confidence.

The five largest financing rounds in February were:

- EigenLayer completed $100 million in financing, valuation undisclosed;

- Flare Network completed $35 million in financing, valuation undisclosed;

- Ether.Fi completed $27 million in financing, valuation undisclosed;

- Avail completed $27 million in seed round financing, valuation undisclosed;

- MetaStreet completed $25 million in financing, valuation undisclosed;

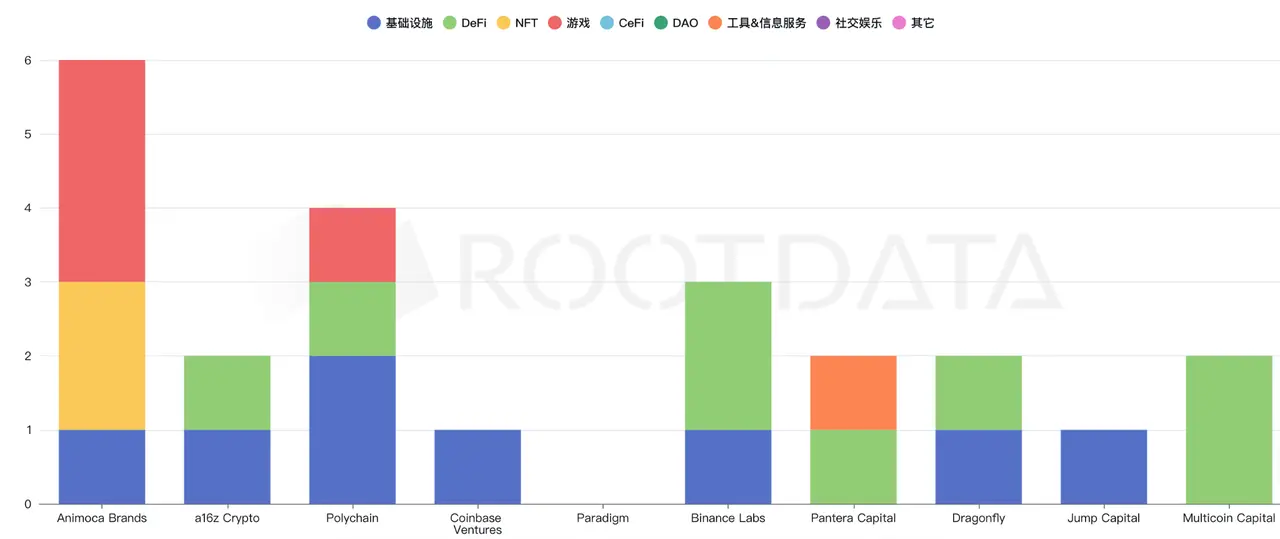

Additionally, in the financing events, there were 38 seed rounds (up 40% year-on-year), 15 strategic financings (down 21% year-on-year), 13 pre-seed rounds (up 30% year-on-year), and 8 other types (no change), with seed rounds being the most frequent, followed by strategic financings and pre-seed rounds, while other types of financing events were relatively few.

From the VC perspective, Animoca Brands has been active in investments in infrastructure, NFTs, and GameFi, while Binance Labs and Multicoin Capital have made the most investments in the DeFi sector, and other VC firms have focused on infrastructure investments.

Investment activities in the crypto space increased in February, both in terms of the number of projects and investment amounts, reaching a near one-year high, with investments still concentrated in infrastructure and DeFi directions. This trend may positively impact market sentiment in March, attracting more investors into the market.

Entering March, the development trends of cryptocurrency and blockchain investment activities may be influenced by various factors, including global economic conditions, technological innovations, and policy environments. Unless significant adverse events or policies arise, and if market sentiment remains positive and technological innovations continue to advance, it is expected that investment activities in March will continue to grow. However, market volatility and policy changes remain key risk factors, and investors must remain vigilant and continuously monitor to make timely and accurate investment decisions.

5. Summary

The market trends and dynamics in February 2024 have revealed several important trends:

- The market reacts significantly to macroeconomic data and policy expectations, especially following the release of employment growth and inflation data;

- The production market shows strong momentum, particularly with BTC and ETH prices rising significantly this month driven by ETFs;

- Continuous issuance of stablecoins, ongoing growth in on-chain TVL, and stable increases in mining pool data all demonstrate investors' optimistic expectations for the future;

- The increase in total financing amounts indirectly reflects the rising market activity and investor confidence;

Despite facing uncertainties in the macroeconomic environment and regulatory challenges, investments in technological innovation and infrastructure development continue to grow, indicating the long-term potential and development space of the crypto market. Investors and market participants should continue to monitor macroeconomic indicators, technological innovations, and changes in the policy environment to make informed decisions in the ever-changing market. We look forward to the crypto market in April continuing to showcase its unique innovative capabilities and its penetration and influence on the global financial ecosystem.

Note: All views expressed above are for reference only and do not constitute investment advice. If there are any disagreements, please feel free to contact us for corrections.

*Follow and join the MIIX Capital community to learn more about cutting-edge information: Twitter CN: * https://twitter.com/MIIXCapital_CN*; Telegram CN: * https://t.me/MIIXCapitalcn;

*Join the MIIX Capital team: * hr@miixcapital.com: Positions available: Investment Research Analyst / Operations Manager / Visual Designer.

Risk warning Risk warning

Risk warning Risk warning