The Era of Stablecoins: The Financial Future Behind Circle's IPO

Looking back at history, Circle attempted to go public via SPAC in 2022, with an expected valuation of around $9 billion, but ultimately abandoned the plan due to unfavorable regulatory and market conditions. This successful listing reflects both its prudent pricing and the mature judgment of the market.

Looking back at history, Circle attempted to go public via SPAC in 2022, with an expected valuation of around $9 billion, but ultimately abandoned the plan due to unfavorable regulatory and market conditions. This successful listing reflects both its prudent pricing and the mature judgment of the market.Circle officially conducted its IPO on the New York Stock Exchange on June 5, 2025, publicly offering 34 million shares of Class A common stock at a listing price of $31 per share. On the first day, the closing price surged to $83.23, an increase of about 168%, with the market capitalization reaching between $18 billion and $21 billion at one point. The three major investment banks—J.P. Morgan, Citigroup, and Goldman Sachs—served as lead underwriters and opened a 30-day greenshoe option to stabilize the stock price and for additional allocation.

Looking back, Circle attempted to go public via a SPAC in 2022, with an estimated valuation of about $9 billion, but ultimately abandoned the plan due to unfavorable regulatory and market conditions. This successful listing reflects both its prudent pricing and the maturity of market judgment.

1. Analysis of Operating Model and Profit Structure

USDC Minting and Reserve Income Mechanism

- USDC is backed by cash and short-term U.S. Treasury securities. As of June 5, 2025, the circulation of USDC was approximately $61 billion, with reserves matching that amount. Revenue for Q1 2025 was $578.6 million, with a net profit of $63.2 million, and adjusted EBITDA reached $122.4 million.

Highly Sensitive to Interest Rates

Circle's revenue for 2024 is expected to be about $1.68 billion, with 99% coming from USDC reserve interest income. According to MarketWatch, "98% of revenue in 2024 will come from short-term Treasury yields, and every 25 basis point cut by the Fed will reduce EBITDA by $100 million." If this structure is not diversified or hedged, its profits will be directly influenced by interest rate policies.

2. Market Position and Growth Prospects

Leading Global Market Share of USDC

- USDC holds nearly 29% of the global stablecoin market, second only to Tether; however, in on-chain transaction volume, USDC accounts for over 58%, becoming the preferred choice for transactions. The circulation of USDC grew from $32 billion (early 2024) to $60 billion; since 2018, the cumulative on-chain transaction volume has exceeded $25 trillion. In Q1 2025, on-chain transaction volume reached $5.9 trillion, a year-on-year increase of about 500%, with the total surpassing $25 trillion.

New Products and Ecosystem Expansion

- Launched the euro-denominated stablecoin EURC, actively pursuing international collaborations, and has initiated a cross-border payment network called "Payments Network," aiming to compete with traditional systems like Visa and SWIFT.

Building Barriers through Network Effects:

- The S-1 filing emphasizes Circle's reliance on developer tools, decentralized wallets, and strategic partnerships with Grab, Mercado Libre, Nubank, SBI, and Binance to create an ecological closed loop.

Initial Success in Business Diversification:

- Achieved non-reserve income growth to 3.6%, with payments, cross-border payments, and developer services becoming new revenue growth points.

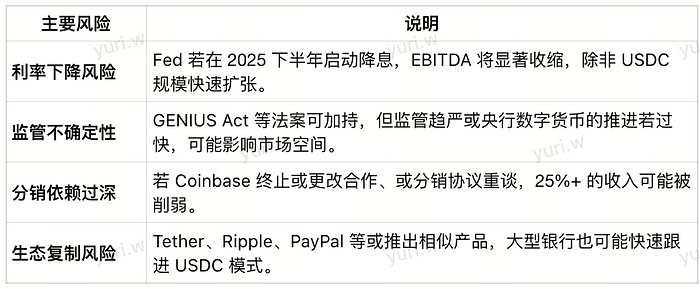

3. Analysis of Core Risk Points

- Profit Risk from Falling Interest Rates

Q1 has emphasized reliance on interest margin income. If the Federal Reserve cuts interest rates in the second half of the year, every 25bp cut will reduce EBITDA by about $100 million. Unless USDC continues to expand significantly, profits may be under pressure. - Uncertainty in Regulatory Policies

Congress is advancing the GENIUS Act to establish a clear management system for stablecoins, which may provide short-term support. However, if regulations tighten in the future or compete with central bank digital currencies, it will compress market space. - High Distribution Costs:

Circle's revenue-sharing agreement with Coinbase allocates 50-60% of reserve income, with nearly $940 million out of an estimated $1.7 billion in reserve income for 2024 going to Coinbase. - Risks from Dependence on Distribution Partners

There has been a joint issuance relationship with Coinbase; if distribution methods are adjusted or agreements renegotiated, it will weaken the efficiency of USDC promotion and impact the revenue structure. - Intensifying Competition and Ecosystem Replication Risks

In the digital financial transformation, small and medium-sized banks, PayPal, Ripple manufacturers, and Tether may all push into stablecoins or related payment networks, putting pressure on USDC.

4. Valuation and Insights into Investor Behavior

- Premium Frenzy and Valuation Bubble

The IPO raised $1.1 billion, with a market capitalization of $6.9 billion (not accounting for over-allotment), and the market cap soared to around $18 billion after listing. However, based on a net profit of $157 million in 2024, the PE ratio reached 106 times, increasing expectations of overvaluation. - Institutional Funds and ETF Vitality

Institutions like ARK Invest and Cathie Wood are actively positioning themselves, with rapid follow-up on ETF issuance, reflecting market optimism towards stablecoins and the financial infrastructure behind them. - IPO as a Hot Product:

CRCL was issued at $31 per share but jumped to $107.7 on the first day, closing up 168% (later rising to about $100), reflecting speculative enthusiasm and an influx of institutional funds.

5. Future Development and Key Observation Indicators

Key Observation Signals:

- Monitor the growth rate of USDC circulation, reserve composition (T-bills vs. cash/repo), interest rate trends, and changes in distribution structure.

- Trends in reserve allocation changes: proportions of Treasury bonds, cash, and repos.

- Combine the Fed's monetary policy statements for the second half of 2025, inflation, and employment data to assess whether the interest margin income model can continue to support valuation.

- The speed of advancement of the GENIUS Act or other stablecoin-related legislation.

Growth Path and Market Layout:

- The commercial implementation of the cross-border payment network and bank wallet integration;

- The acceptance of EURC in the European market;

- Whether the infrastructure behind stablecoins (such as USYC) can become a true digital asset ecological tool.

Circle's IPO is not only a fusion of fintech and the crypto economy but also an important experiment for stablecoins entering the era of "mainstream financial infrastructure."

Risk warning Risk warning

Risk warning Risk warning

Popular articles