Token vs Equity Battle: On-chain Sovereignty vs Regulatory Constraints, How Does the Crypto Economy Restructure?

Can the tokens "bound hand and foot" by the SEC break free from the regulatory fog and redefine the autonomous ownership of digital property?

Can the tokens "bound hand and foot" by the SEC break free from the regulatory fog and redefine the autonomous ownership of digital property?Written by: Jesse Walden, Variant Partner; Jake Chervinsky, Variant CLO

Compiled by: Saoirse, Foresight News

Introduction

Over the past decade, entrepreneurs in the crypto industry have generally adopted a value distribution model: attributing value to two independent vehicles, tokens and equity. Tokens provide a new way for networks to expand at an unprecedented scale and speed, but this potential can only be realized if tokens represent the genuine needs of users. However, the ongoing regulatory pressure from the U.S. Securities and Exchange Commission (SEC) has significantly hindered entrepreneurs from injecting value into tokens, forcing them to shift their focus to equity. This situation urgently needs to change.

The core innovation of tokens lies in achieving "self-ownership" of digital assets. With tokens, holders can independently own and control funds, data, identities, and the on-chain protocols and products they use. To maximize this value, tokens should capture on-chain value, which is transparent, auditable, and directly controlled by token holders.

Off-chain value, on the other hand, is different. Since token holders cannot directly own or control off-chain income or assets, this type of value should rightfully belong to equity. Although entrepreneurs may wish to share off-chain value with token holders, this often carries compliance risks: companies controlling off-chain value typically have fiduciary duties and must prioritize returning assets to shareholders. If entrepreneurs want to direct value to token holders, then this value must exist on-chain from the outset.

The fundamental principle that "tokens correspond to on-chain value, and equity corresponds to off-chain value" has been distorted since the inception of the crypto industry due to regulatory pressures. The SEC's broad interpretation of securities law has not only led to an imbalance in the incentive mechanisms between companies and token holders but has also forced entrepreneurs to rely on inefficient decentralized governance systems to manage protocol development. Now, the industry has ushered in a new opportunity for entrepreneurs to re-explore the essence of tokens.

The SEC's Old Rules Restrict Entrepreneurs

During the ICO era, crypto projects often raised funds through public token sales, completely ignoring equity financing. They promised that the construction of the protocol would boost the value of tokens after their launch, making token sales the sole fundraising method, with tokens being the only value-bearing asset.

However, ICOs failed to pass the SEC's scrutiny. Since the 2017 DAO Report, the SEC has applied the Howey test to public token sales, determining that most tokens qualify as securities. In 2018, Bill Hinman (former Director of the SEC's Division of Corporation Finance) established "sufficient decentralization" as a key compliance criterion. In 2019, the SEC further released a complex regulatory framework that increased the likelihood of tokens being classified as securities.

In response, companies abandoned ICOs and turned to private equity financing. They relied on venture capital to support protocol development and only distributed tokens to the market after the protocol was completed. To comply with SEC guidance, companies had to avoid any actions that might raise the value of tokens after their launch. The SEC's regulations were extremely strict, requiring companies to almost completely sever ties with the protocols they developed, and they were even discouraged from holding tokens on their balance sheets to avoid being seen as having financial motives to inflate token values.

Entrepreneurs subsequently transferred governance of the protocols to token holders and focused on building products on top of the protocols. The core idea was that a governance mechanism based on tokens could serve as a shortcut to achieving "sufficient decentralization," while entrepreneurs continued to contribute to the protocol as ecosystem participants. Additionally, entrepreneurs could create equity value through a business strategy of "commodifying complementary goods," offering open-source software for free and then monetizing through upper or lower-layer products.

However, this model exposes three major issues: misaligned incentive mechanisms, low governance efficiency, and unresolved legal risks.

First, the incentive mechanisms between companies and token holders have become misaligned. Companies are forced to direct value toward equity rather than tokens, both to reduce regulatory risks and to fulfill their fiduciary duties to shareholders. Entrepreneurs no longer pursue market share competition but instead develop business models centered on equity appreciation, even having to abandon commercialization paths.

Second, this model relies on decentralized autonomous organizations (DAOs) to manage protocol development, but DAOs are not suited for this role. Some DAOs operate through foundations but often fall into issues of misaligned incentives, legal and economic constraints, operational inefficiencies, and centralized access barriers. Other DAOs adopt collective decision-making, but most token holders lack interest in governance, leading to slow decision-making, unclear standards, and poor outcomes due to the token-based voting mechanism.

Third, compliance designs have not genuinely mitigated legal risks. Although this model aims to meet regulatory requirements, the SEC still investigates companies adopting it. Governance based on tokens also introduces new legal risks, such as DAOs potentially being classified as general partnerships, exposing token holders to unlimited joint liability.

Ultimately, the actual costs of this model far exceed the expected benefits, undermining the commercial viability of the protocols and damaging the market appeal of the associated tokens.

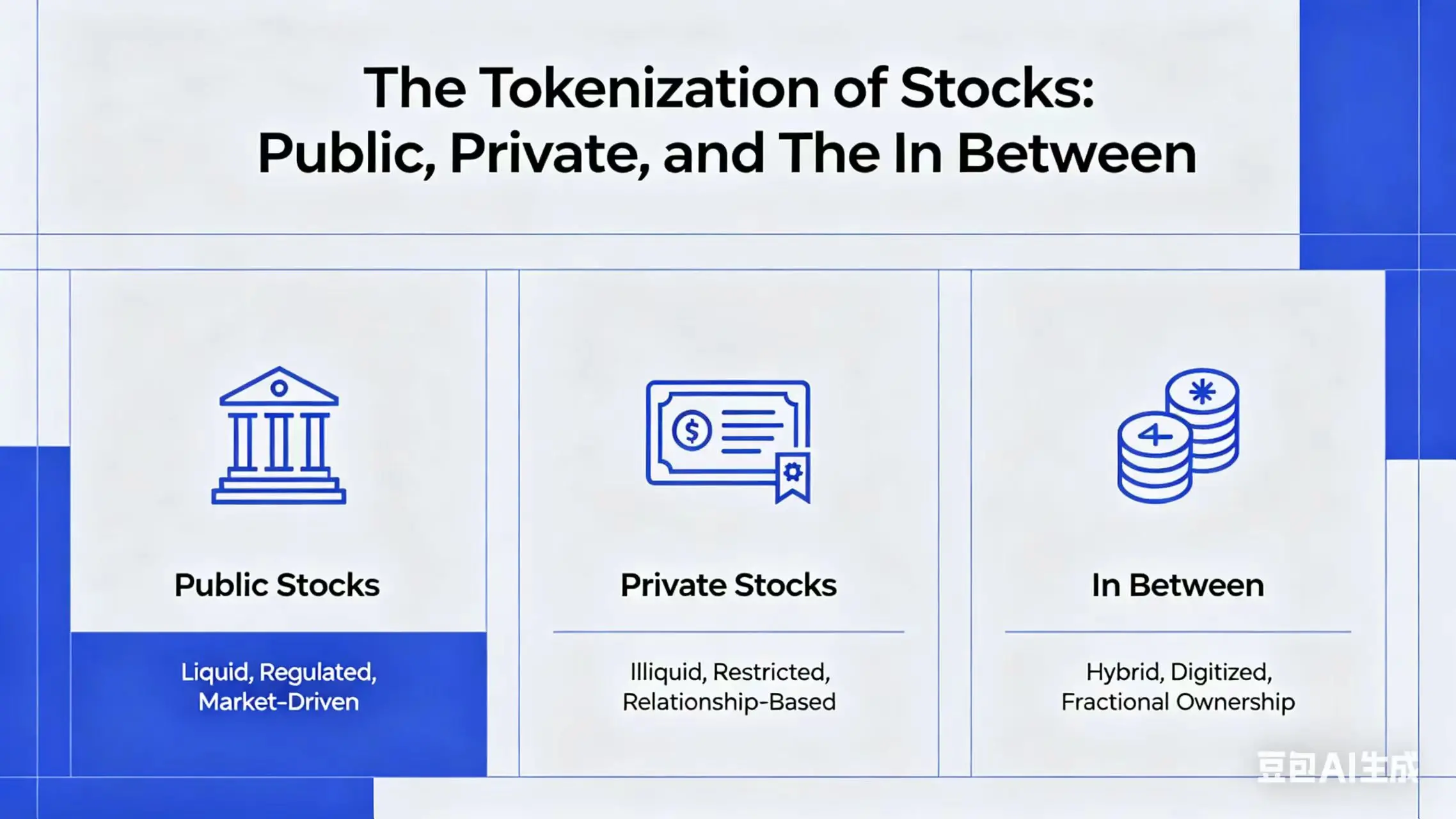

Tokens Carry On-Chain Value, Equity Carries Off-Chain Value

The new regulatory environment provides entrepreneurs with an opportunity to redefine the reasonable relationship between tokens and equity: tokens should capture on-chain value, while equity corresponds to off-chain value.

The unique value of tokens lies in achieving self-ownership of digital assets. They grant holders ownership and control over on-chain infrastructure, which possesses global real-time auditability and transparency. To maximize this feature, entrepreneurs should design products to direct value on-chain, allowing token holders to directly own and control.

Typical cases of capturing on-chain value include: Ethereum benefiting token holders through the EIP-1559 protocol by burning transaction fees, or directing DeFi protocol revenues to an on-chain treasury through fee conversion mechanisms; token holders can also profit from intellectual property authorized for third-party use or earn revenue by routing all fees through on-chain DeFi front-end interfaces. The core principle is that value must be transacted on-chain, ensuring that token holders can directly observe, own, and control without intermediaries.

In contrast, off-chain value should belong to equity. When income or assets exist in off-chain scenarios such as bank accounts, business partnerships, or service contracts, token holders cannot directly control them and must rely on companies as intermediaries for value transfer, a relationship that may be subject to securities law. Furthermore, companies controlling off-chain value have fiduciary duties to prioritize returning profits to shareholders rather than token holders.

This does not negate the rationality of the equity model. Even if the core product is open-source software like public chains or smart contract protocols, crypto companies can still succeed using traditional business strategies. As long as there is a clear distinction between "tokens corresponding to on-chain value and equity corresponding to off-chain value," actual value can be created for both.

Minimize Governance, Maximize Ownership

In the context of the new era, entrepreneurs need to abandon the mindset of using tokenized governance as a shortcut for regulatory compliance. Instead, governance mechanisms should only be activated when necessary and should remain minimal and orderly.

One of the core advantages of public blockchains is automation. Overall, entrepreneurs should automate all processes as much as possible, reserving governance authority only for matters that cannot be automated. Some protocols may benefit from "humans at the edges" involvement, such as executing upgrades, allocating treasury funds, and monitoring dynamic parameters like fees and risk models. However, the scope of governance should be strictly limited to functions exclusive to token holders; in short, the higher the degree of automation, the better the governance efficiency.

When complete automation is not feasible, delegating specific governance rights to trusted teams or individuals can enhance decision-making efficiency and quality. For example, token holders can authorize protocol development companies to adjust certain parameters, eliminating the need for consensus voting on every action. As long as token holders retain ultimate control (including the ability to monitor, veto, or revoke authorization at any time), the delegation mechanism can ensure adherence to decentralization principles while achieving efficient governance.

Entrepreneurs can also ensure effective governance mechanisms through customized legal structures and on-chain tools. It is advisable for entrepreneurs to consider adopting new entity structures like Wyoming's DUNA (Decentralized Autonomous Nonprofit Association), which grants token holders limited liability and legal personality, enabling them to contract, pay taxes, and seek judicial protection; additionally, they should consider governance tools like BORG (Blockchain Organization Registration Governance) to ensure that DAOs operate under a framework of on-chain transparency, accountability, and security.

Moreover, it is essential to maximize token holders' ownership of on-chain infrastructure. Market data indicates that users have very low recognition of the value of governance rights; very few are willing to pay for voting rights related to protocol upgrades or parameter changes, but they are highly sensitive to the value attributes of income distribution rights and on-chain asset control.

Avoiding Securities-Like Relationships

To mitigate regulatory risks, tokens must be clearly distinguished from securities.

The core difference between securities and tokens lies in the rights and powers they confer. Generally, securities represent a series of rights tied to a legal entity, including economic benefits, voting rights, information rights, or legal enforcement rights. For example, stockholders receive specific ownership linked to the company, but these rights are entirely dependent on the company entity. If the company goes bankrupt, the associated rights become void.

In contrast, tokens confer control over on-chain infrastructure. These powers exist independently of any legal entity (including the creators of the infrastructure); even if a company ceases operations, the powers conferred by tokens will persist. Unlike securities holders, token holders typically do not enjoy fiduciary duty protections and do not possess statutory rights. The assets they own are defined by code and are economically independent of their creators.

In some cases, on-chain value may partially depend on a company's off-chain operations, but this fact does not necessarily fall under the purview of securities law. Although the definition of securities is broadly applicable, the law does not intend to regulate all relationships where one party relies on another to create value.

In reality, many transactions exist where income dependency relationships do not fall under securities regulation: consumers purchasing luxury watches, limited-edition sneakers, or high-end handbags may expect brand premiums to drive asset appreciation, but such transactions clearly do not fall within the SEC's regulatory scope.

A similar logic applies to many commercial contract scenarios: for instance, landlords rely on property managers to maintain assets and attract tenants for income, but this cooperative relationship does not make landlords "securities investors." Landlords retain complete control over their assets and can veto management decisions, change operators, or take over operations at any time. Their control over the property exists independently of the manager and is entirely disconnected from the manager's performance.

Tokens aimed at capturing on-chain value are closer to the aforementioned tangible assets than traditional securities. When holders acquire such tokens, they clearly understand the assets and powers they own and control. They may expect the company's continued operation to drive asset appreciation, but there is no statutory rights connection between them and the company; ownership and control of digital assets are entirely independent of the corporate entity.

Ownership and control of digital assets should not constitute a securities regulatory relationship. The core logic of securities law is not "one party benefits from the efforts of another," but rather "investors rely on entrepreneurs in a relationship of information and power asymmetry." If no such dependency exists, token transactions centered on property rights should not be classified as securities offerings.

Of course, even if securities law should not apply to such tokens, it does not preclude the SEC or private plaintiffs from claiming its applicability; the court's interpretation of legal texts will determine the final classification. However, recent policy trends in the U.S. have sent positive signals: Congress and the SEC are exploring new regulatory frameworks, shifting their focus to "control over on-chain infrastructure."

Under a "control-oriented" regulatory logic, as long as the protocol operates independently and token holders retain ultimate control, entrepreneurs can legally create token value without triggering securities regulations. Although the path of policy evolution is not yet fully clear, the trend is evident: the legal system is gradually recognizing that not all value appreciation activities need to fall under securities regulation.

Single Asset Model: Full Tokenization, No Equity Structure?

While some entrepreneurs prefer to create value through a dual-track of tokens and equity, others favor a "single asset" model that anchors all value on-chain and attributes it to tokens.

The "single asset" model has two core advantages: first, it aligns the incentive mechanisms of companies and token holders; second, it allows entrepreneurs to focus on enhancing the competitiveness of the protocol. With a minimalist design logic, leading projects like Morpho have already begun to practice this model.

Consistent with traditional analysis, the determination of securities attributes still centers on ownership and control, which is particularly critical for the single asset model, as it clearly concentrates value creation on tokens. To avoid securities-like relationships, tokens must confer direct ownership and control over digital assets. While legislative measures may gradually institutionalize this model, the current challenge remains the uncertainty of regulatory policies.

Under the single asset structure, companies should be set up as non-profit entities without equity, solely serving their self-developed protocols. When the protocol goes live, control must be transferred to token holders, ideally organized through blockchain governance-specific legal entities like Wyoming's DUNA (Decentralized Autonomous Nonprofit Association).

After launch, companies can continue to participate in protocol development, but their relationship with token holders must be strictly separated from the "entrepreneur-investor" paradigm. Viable paths include: token holders authorizing companies to act as agents for specific permissions or defining the scope of cooperation through service contracts. Both roles fall within the conventional settings of decentralized governance ecosystems and should not trigger the applicability of securities law.

Entrepreneurs must pay special attention to distinguishing single asset tokens from company-backed tokens like FTT, which are closer to securities attributes. Unlike native tokens that confer control and ownership over digital assets, tokens like FTT represent a claim on a company's off-chain income, with their value entirely dependent on the issuing entity: if the company performs poorly, holders have no recourse; if the entity goes bankrupt, the tokens become worthless.

Company-backed tokens precisely create the rights imbalance that securities law aims to address: holders cannot audit off-chain income, veto corporate decisions, or change service providers. The core contradiction lies in the asymmetry of power; such holders are entirely subject to the company, forming a typical securities-like relationship that should fall under regulatory scrutiny. Entrepreneurs adopting the single asset model must avoid such structural designs.

Even with the "single asset" model, companies may still need off-chain income to maintain operations, but related funds can only be used for cost expenditures and cannot be used for dividends, buybacks, or other value transfers to token holders. If necessary, funds can be obtained through treasury allocations or token inflation approved by holders, and control must always remain with token holders.

Entrepreneurs may raise several defenses, such as "no public sale means no capital input" or "no asset pool means no joint enterprise," but including "non-securities relationships," these claims cannot ensure avoidance of current legal applicability risks.

Open Questions and Alternatives

The new era in the crypto industry presents exciting opportunities for entrepreneurs, but this field is still in its early stages, and many issues remain unresolved.

One core question is: can we avoid securities law regulation while completely abandoning governance mechanisms? Theoretically, token holders could hold digital assets without exercising any control. However, if holders remain entirely passive, this relationship may evolve into a category subject to securities law, especially if the company retains some control. Future legislation or regulatory rules may recognize a governance-free "single asset" model, but entrepreneurs must currently adhere to the existing legal framework.

Another question concerns how entrepreneurs handle initial financing and protocol development within the single asset model. While mature frameworks are relatively clear, the optimal path from startup to scaling remains unclear: how can entrepreneurs raise funds to build infrastructure without equity for sale? How should tokens be allocated when the protocol goes live? What type of legal entity should be adopted, and should it be adjusted as development progresses? These details and more questions await exploration by the industry.

Additionally, some tokens may be more suitable for classification as on-chain securities. However, the current securities regulatory system has nearly stifled the survival space for such tokens in decentralized environments, where they could otherwise release value through public chain infrastructure. Ideally, Congress or the SEC should promote the modernization of securities law, allowing traditional securities like stocks, bonds, notes, and investment contracts to operate on-chain and seamlessly integrate with other digital assets. But until then, regulatory certainty for on-chain securities remains elusive.

Path Forward

For entrepreneurs, there is no one-size-fits-all standard answer for the design of token and equity structures; only a comprehensive weighing of costs, benefits, risks, and opportunities. Many open questions can only be gradually answered through market practice, as only continuous exploration can validate which models are more viable.

The purpose of writing this article is to clarify the choices currently facing entrepreneurs and outline potential solutions that may emerge with the evolution of crypto policies. Since the advent of smart contract platforms, ambiguous legal boundaries and stringent regulatory environments have consistently constrained entrepreneurs from unleashing the potential of blockchain tokens. The current regulatory environment has opened up a new exploratory space for the industry.

We have constructed a navigational map above to help entrepreneurs explore directions in this new field and proposed several development paths that we believe hold significant potential. However, it should be clear that the map is not the territory itself; many unknowns await industry exploration. We firmly believe that the next generation of entrepreneurs will redefine the application boundaries of tokens.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles