CoinW Research Institute Hot Report: Analysis of Uniswap's Major Buyback Proposal, Can UNI Trigger a Value Reassessment?

Uniswap's latest buyback proposal has attracted significant attention from the market, but public opinion is highly focused on the buyback mechanism in the proposal. If the buyback mechanism is activated in the future, will it lead to a long-term parabolic growth in the price of UNI tokens?

Uniswap's latest buyback proposal has attracted significant attention from the market, but public opinion is highly focused on the buyback mechanism in the proposal. If the buyback mechanism is activated in the future, will it lead to a long-term parabolic growth in the price of UNI tokens?CoinW Research

The latest buyback proposal from Uniswap has attracted significant attention in the market, but public opinion is highly focused on the buyback mechanism within the proposal. If the buyback mechanism is activated in the future, will it lead to a long-term parabolic increase in the price of UNI tokens?

1. Uniswap's Major Proposal: In-Depth Analysis

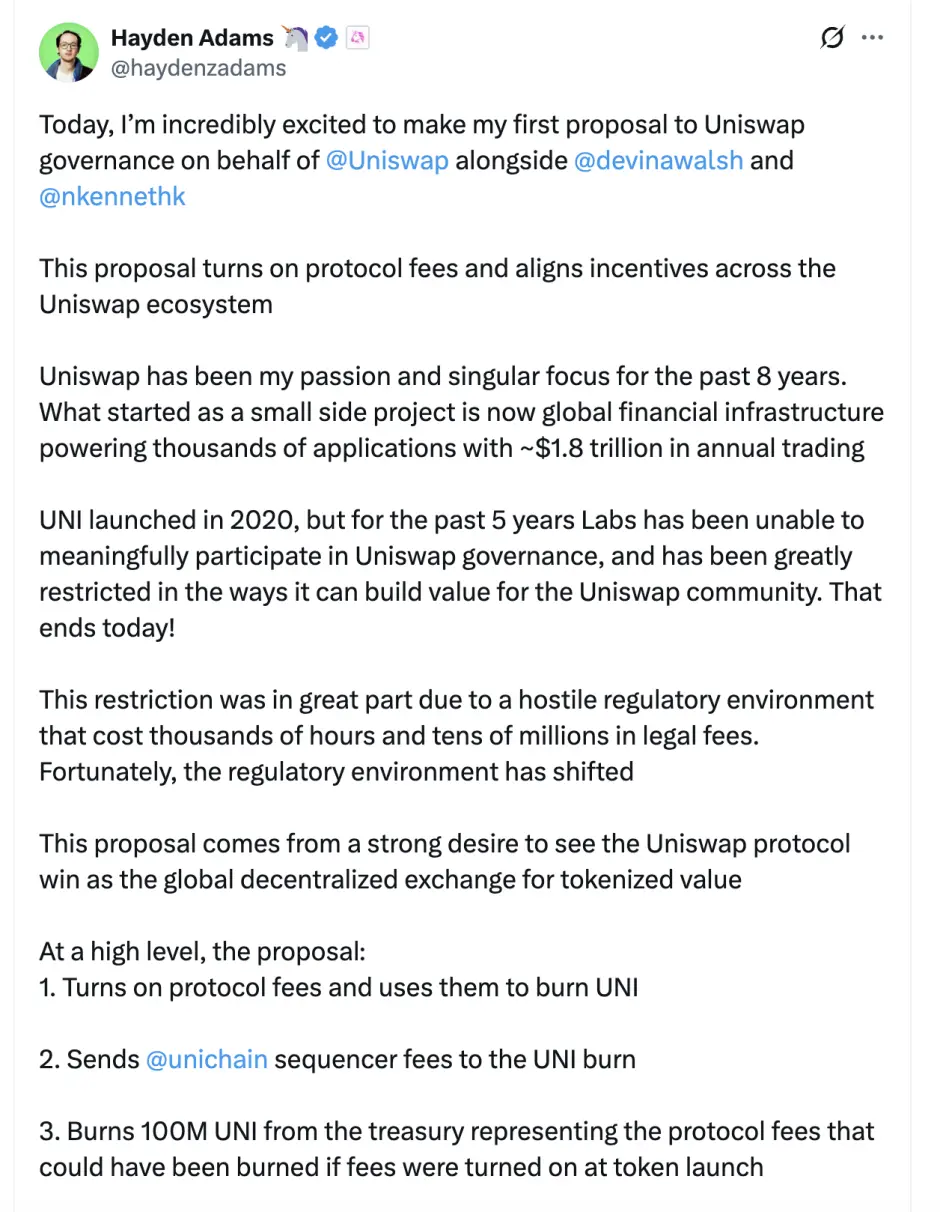

Uniswap CEO Hayden Adams recently announced its first governance proposal, which includes measures such as enabling protocol fees, burning UNI tokens, and increasing Unichain fees, shifting the UNI token towards a deflationary model. If the proposal is approved, the Uniswap protocol is expected to generate approximately $460 million to $510 million annually for the buyback of UNI, which will provide strong support for the token price. The specifics of the proposal are as follows:

- Enable protocol fees, with all protocol-side revenue used for the buyback and burning of UNI.

This is the core value capture mechanism of this proposal. It fundamentally changes the UNI token model, transforming it from a purely governance token into a "productive asset" supported by direct cash flow. This is similar to how publicly listed companies buy back their stock using profits, providing long-term and solid value support for the token price and driving it into a "deflationary appreciation" flywheel. This is the essence of value capture. UNI will transition from a governance token with no cash flow to a "productive asset" supported by direct income, akin to stock buybacks.

- Unichain sequencer fees incorporated into the burn pool.

This move aims to consolidate the value generated by the entire Uniswap ecosystem onto the UNI token. Sequencer fees are inherent revenues from the Unichain Layer 2 blockchain, and incorporating them into the burn pool means that UNI's value will no longer rely solely on DEX trading operations but will be deeply tied to the prosperity of the entire Uniswap ecosystem (including its public chain), broadening its value base.

- One-time destruction of 10 million UNI (retrospective destruction for historical fee-free periods).

This is a strong deflationary signal and a measure to boost market confidence. The one-time destruction accounts for 16% of the total supply, which can immediately enhance the scarcity of the remaining tokens. The logic of "retrospective compensation" aims to fairly reward early supporters and attempts to "compensate" for the lack of returns for holders in the past, which is expected to have a significant short-term stimulative effect on market sentiment.

- Launch of PFDA: Offering traders "fee discounts" through an auction format while keeping MEV revenue within the protocol.

This is an innovative mechanism that achieves two goals at once. By auctioning off fee discount rights, it cleverly recovers the MEV value that was originally captured by third-party searchers back into the protocol. Ultimately, this portion of revenue will feed back into the UNI buyback, enhancing the robustness of the entire economic model.

- v4 Aggregator Hook: Aggregating external DEX liquidity and collecting protocol fees.

This means that Uniswap is evolving from a "liquidity provider" to a "liquidity aggregation layer and fee gateway." Even if trades do not occur in Uniswap's own liquidity pools, as long as they are routed through its Hook, the protocol can capture fees. This greatly expands Uniswap's chargeable market and represents a strategic breakthrough for its revenue ceiling.

- Unified fee standards: Interfaces/wallets/APIs will no longer charge additional fees, and the fee collection standard will be unified at the protocol level.

This move is intended to solidify the core position of the protocol layer and the moat of its business model. It prevents various front ends (such as official websites and third-party interfaces) from engaging in "zero-fee" infighting for competition, which would erode the revenue base of the entire ecosystem. Unified charging ensures the visibility, predictability, and stability of protocol revenue, which is an important guarantee for the long-term healthy operation of the economic model.

- Governance and organization: Merging Labs and the foundation, with a budget of 20 million UNI per year for growth.

This reflects Uniswap's pursuit of balance between short-term financial returns and long-term ecological development. The merger can enhance decision-making efficiency, while establishing a clear growth budget indicates that the team is not solely focused on the current token price but is committed to continuously investing in developers, liquidity, and other ecological construction to ensure the protocol remains vibrant and competitive in the next decade.

- Asset migration: Unisocks liquidity will migrate to Unichain v4, and the LP position will be burned.

This operation has more strategic symbolic significance. It indicates that the team is cleaning up old assets and fully redirecting resources and attention towards the next-generation strategy centered on Unichain and v4. It can be seen as a "metabolism" of the ecosystem, symbolizing a break from the old model and a concentrated effort to build the future.

Image source: Uniswap founder (Hayden Adams)

Researcher's perspective: The core of this proposal lies in constructing a value flywheel of "protocol revenue → buyback and burn → token deflationary appreciation." If it can operate smoothly, it will provide continuous cash flow discounting and price support for UNI.

2. Proposal Approval: Buyback Estimation and Protocol Revenue Analysis

We conducted estimations based on historical data and publicly available proposal parameters. This proposal involves a one-time destruction of 10 million tokens (16% of the total), with the core assumption being a daily buyback trading volume of 0.05%. That is, protocol fees (0.3%) - LP rewards (0.25%) = buyback (0.05%).

- Core revenue source analysis:

Core DEX business: Based on an annual trading volume of approximately $1 trillion for V2 and V3 versions, it is estimated that an annual protocol revenue of $500 million can be generated at a 0.05% fee rate.

v4 aggregator business: As an incremental source, it is expected to contribute 10%-20% of the core trading volume, potentially bringing in $50 million to $100 million in annual revenue.

PFDA and MEV capture: Although important innovative revenues, they are currently difficult to quantify accurately and are not included in this estimation. Unichain sequencer fees: Still in the early stages of development and relatively small in scale, they are also not included.

- Annual buyback fund summary:

Conservative scenario (only counting core DEX business): Annual buyback funds are approximately $500 million.

Optimistic scenario (including v4 aggregator revenue): Annual buyback funds are expected to be between $550 million and $600 million.

Researcher's perspective: Based on market consensus and this report's estimations, a daily protocol fee of 0.05% for buybacks is expected to achieve an annual deflation rate of 1.5%-2%. At the current trading volume level, the funds available for Uniswap to buy back UNI annually are estimated to fall within the range of $500 million to $550 million, which is a relatively conservative estimate. This equates to providing the market with continuous buying support of $35 million to $42 million per month, which constitutes solid support for mid- to long-term value.

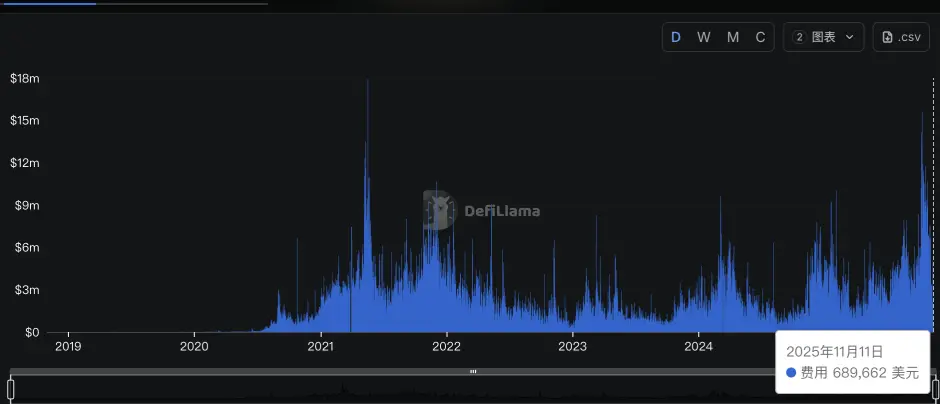

3. Market Reaction: Huge Buyback Expectations Drive Price Surge

In response to this proposal, various market participants quickly provided positive feedback. Alexander, CEO of Dromos Labs, the development team behind the leading DEX in the Base ecosystem, Aerodrome, pointed out that based on Uniswap's current trading volume, approximately $460 million in fees is expected to be used for buybacks and burns annually, which will become a strong and sustainable buying support for the $UNI token.

CryptoQuant CEO Ki Young Ju also noted that the fee conversion mechanism could drive Uniswap's price to rise parabolically. He analyzed that even when only considering versions v2 and v3, the protocol's annual trading volume reaches $1 trillion, estimating that the value of UNI burned each year will be around $500 million. Furthermore, the trading platform only holds $830 million in UNI, meaning that future unlocking selling pressure is relatively limited. Driven by this optimistic expectation, UNI surged nearly 50% within hours of the proposal's announcement.

Data source: defillama

Researcher's perspective: This proposal undoubtedly establishes a "hard bottom" for UNI's long-term value. Its core mechanism is: in the short term, creating a deflationary shock by one-time destruction of 10 million UNI (16% of circulation); in the long term, relying on continuous buybacks of approximately $38 million per month (annualized $400-$500 million) to provide stable buying support. This dual deflationary model provides strong support for the price.

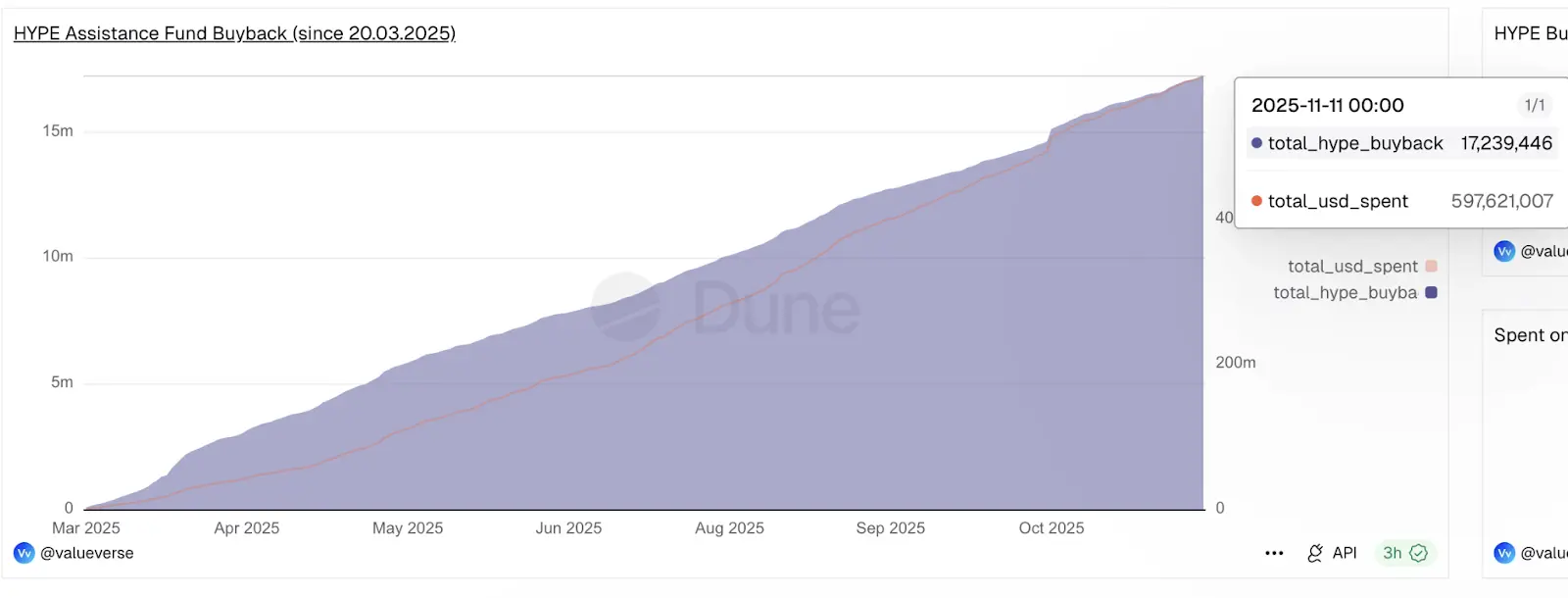

4. Competitive Comparison: Buyback Strength Ranks Among the Top

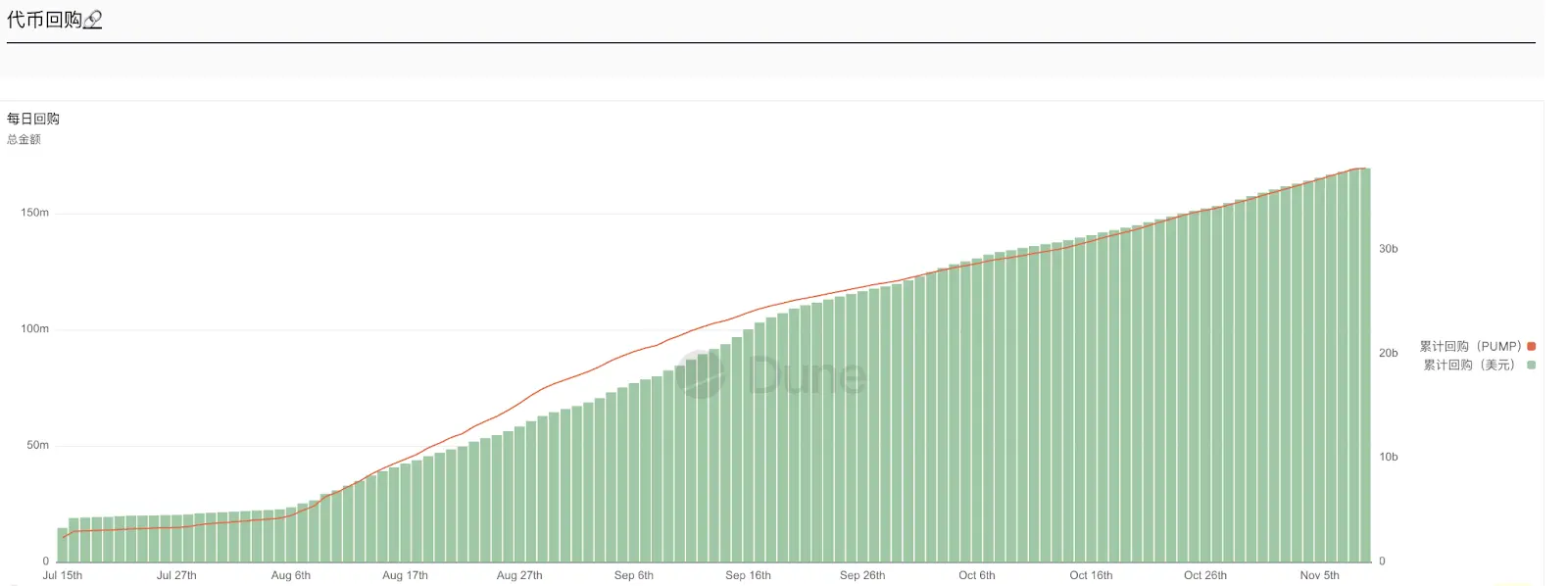

According to the proposal mechanism, Uniswap plans to split the original 0.3% LP fee, with 0.25% still going to liquidity providers, while 0.05% will be allocated to the protocol for UNI buybacks. If calculated based on its approximately $28 billion annual fee revenue, this means the protocol can generate about $38 million in dedicated buyback funds each month. This scale places it in a strong position among tokens with buyback mechanisms: not only significantly surpassing PUMP ($35 million/month) but also approaching the current highest HYPE ($95 million/month).

Image source: DUNE (HYPE)

Image source: DUNE (PUMP)

Researcher's perspective: Previously, UNI's massive trading volume could not bring direct benefits to its token holders. However, the annual buyback plan of several hundred million dollars is equivalent to opening a continuous "shareholder return." This not only has the potential to catch up with competitors but also represents a return of value to its token holders.

5. Future Outlook: Success Depends on the Anchor of Liquidity Providers (LP)

If this proposal from Uniswap is approved, it will bring long-term benefits to UNI, effectively establishing a "bottoming mechanism" for the token price. However, its success entirely depends on one core aspect: whether liquidity providers (LP) will stay.

Successful path: The proposal reduces LP fees from 0.3% to 0.25% (a 17% reduction). LPs will only remain if new revenues from PFDA and MEV internalization can fully compensate for their losses. Stability of LPs ensures the depth of the liquidity pool and the trading experience, allowing protocol fee revenue to continue, and the buyback and burn "bottoming" mechanism to operate healthily.

Risk path: Conversely, if LPs withdraw due to declining revenues, it will lead to reduced liquidity, loss of trading volume, ultimately shrinking both protocol revenue and buyback funds, making the bottoming mechanism untenable.

Therefore, for ordinary users, two points need to be emphasized. Short-term: Governance voting results and contract launch timing. Long-term: LP retention rates and liquidity pool depth, whether the $38 million monthly buyback is stable, the actual effects of PFDA and MEV internalization, and changes in competitors' market shares.

Risk warning Risk warning

Risk warning Risk warning