From market makers withdrawing funds to CME exerting pressure, Hyperliquid is standing at the crossroads of regulation and liquidity

The narrative of Hyperliquid has changed; it is no longer just a crypto-native perpetual trading platform, but is transforming into a 24-hour operation that covers on-chain prices of both crypto assets and traditional assets.

The narrative of Hyperliquid has changed; it is no longer just a crypto-native perpetual trading platform, but is transforming into a 24-hour operation that covers on-chain prices of both crypto assets and traditional assets.Recently, Hyperliquid has once again become the focus of market attention. On one hand, according to on-chain data, there has been a large-scale withdrawal of funds from the Wintermute and Auros Global related market-making addresses on the Hyperliquid platform, with the total amount approaching nearly $100 million; on the other hand, traditional exchanges such as CME and ICE have begun to push U.S. regulators to pay attention to Hyperliquid, especially regarding the price discovery and regulatory boundary issues brought by perpetual contracts for traditional assets like crude oil, stock indices, and Pre-IPO.

In the past, the market's understanding of Hyperliquid was more focused on the on-chain order book, extreme trading experience, and the expansion of Perp DEX market share. However, as mainstream market makers begin to reduce their exposure and traditional exchanges start to exert public pressure, the narrative surrounding Hyperliquid has changed. It is no longer just a crypto-native perpetual trading platform but is evolving into a 24/7 operating on-chain price discovery system covering both crypto and traditional assets.

In the following text, CoinW Research Institute will analyze the liquidity pressure, growth logic, and institutional risks currently faced by Hyperliquid, using the changes in addresses related to Wintermute and Auros Global as a starting point, combined with Hyperliquid's current trading data and the background of CME and ICE pushing for regulation, and further explore where this on-chain perpetual giant may head in the future.

1. Two Major Market Makers Withdraw Funds, Hyperliquid's Liquidity Faces Stress Test

The core of this event comes from Hyperinsight's monitoring of Hyperliquid's institutional LP addresses. According to Lookonchain's disclosure on May 18, against the backdrop of recent market volatility, two major institutional liquidity provider addresses on the Hyperliquid platform have shown synchronized large-scale withdrawal behavior, with an estimated total amount close to $100 million.

Among them, the Auros Global related LP address quickly closed all its perpetual positions on the Hyperliquid platform and transferred approximately $6 million to Binance. Previously, this address had provided liquidity for about 175 tokens on the platform, with the liquidity scale related to BTC once reaching approximately $45 million. Meanwhile, the Wintermute related address also significantly reduced its market-making exposure on Hyperliquid. Hyperinsight's comparison with previous data found that its liquidity provision for BTC and ETH decreased by about 90%, from approximately $40 million to about $4 million.

However, it should be noted that the Wintermute and Auros Global addresses mentioned here are labeled addresses marked by third-party monitoring such as Hyperinsight and Lookonchain, and are not officially confirmed by the two companies.

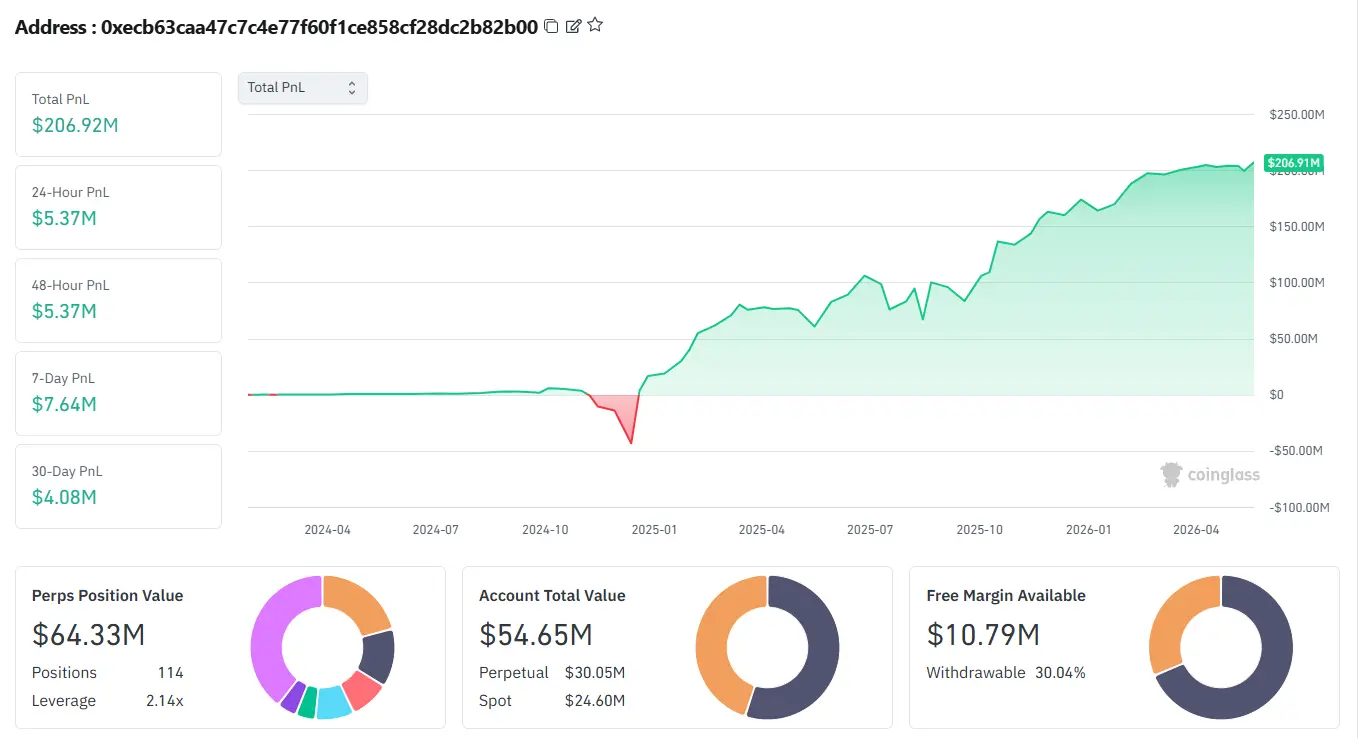

Wintermute labeled address: 0xecb63caa47c7c4e77f60f1ce858cf28dc2b82b00

Auros Global labeled address: 0x023a3d058020fb76cca98f01b3c48c8938a22355

Further data from coinglass shows that as of May 19, the value of the perpetual account for the Wintermute labeled address was approximately $54.65 million, with a nominal perpetual position of about $64.33 million, still holding 114 perpetual positions. The Auros labeled address is even more pronounced, with a nominal perpetual position of 0 and an account value of about $898,000.

Source:++https://www.coinglass.com/hyperliquid/0xecb63caa47c7c4e77f60f1ce858cf28dc2b82b00++

Thus, this event cannot be simply understood as "the two major market makers completely withdrawing from Hyperliquid." More accurately, the Auros labeled address is closer to exiting perpetual market-making exposure, while the Wintermute labeled address is still participating in trading, but its risk budget, inventory structure, and quote depth may have changed. This distinction is important. If both institutions were to completely exit simultaneously, it would mean that professional market-making capital is beginning to reassess the risk-reward ratio of Hyperliquid.

2. Mainstream Coin Liquidity Has Not Disappeared, But Capacity to Absorb Is Thinning

However, in the crypto market, the withdrawal of market makers often does not immediately reflect in the candlestick chart, nor does it necessarily lead to an immediate widening of the bid-ask spread. Especially for mainstream assets like BTC and ETH, even if some institutional LPs reduce their quotes, other traders, arbitrage bots, and the platform's internal liquidity mechanisms may still maintain a tight first-level spread. Therefore, users may not immediately perceive a decline in liquidity in their daily trading. But this does not mean that the impact does not exist. The real changes often occur in market depth, impact costs, and the recovery ability during extreme conditions.

The role of market makers is not just to provide bid and ask quotes but to offer short-term inventory buffering during unilateral market fluctuations. When there are large buy or sell orders or continuous liquidations, the willingness of top market makers to place orders on both sides of the market determines whether prices can be smoothly absorbed in a short time. If this portion of institutional capital withdraws, even if trading remains smooth during normal times, once pressure conditions arise, the market is more likely to experience slippage, price jumps, and chain reactions of liquidations.

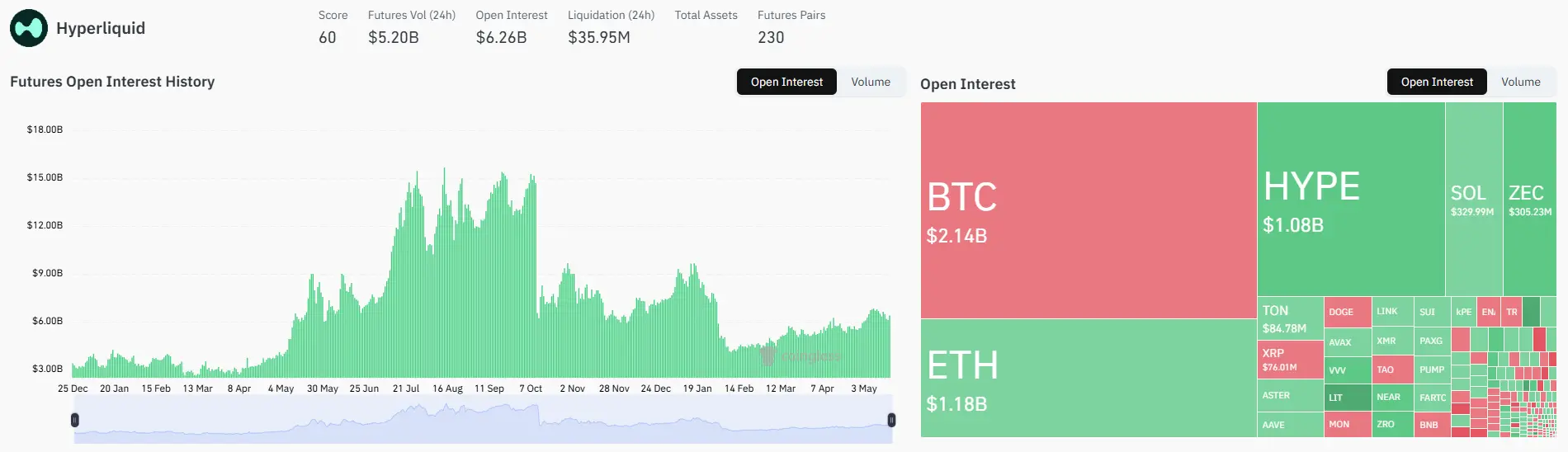

The current trading data at the platform level for Hyperliquid remains impressive. According to coinglass data, as of May 19, 2026, the platform has launched 230 perpetual contract markets, with a 24-hour nominal trading volume of approximately $5.2 billion and an open interest of about $6.26 billion. Among them, BTC, ETH, and HYPE remain the main trading varieties. On the surface, Hyperliquid is still one of the most liquid perpetual contract platforms on-chain.

Source:++https://www.coinglass.com/exchanges/Hyperliquid++

However, it is important to note that total trading volume on the platform and real liquidity are not the same thing. Trading volume reflects how many transactions have occurred in the market, while liquidity reflects how many transactions can still be absorbed at low cost in the future. The former can be amplified by volatility, leverage, and high-frequency trading, while the latter relies more on market maker inventory, capital costs, and risk preferences.

Therefore, what is truly worth paying attention to regarding the withdrawal of market makers is not whether Hyperliquid's trading volume will significantly decline in the short term, but rather that its liquidity structure is undergoing changes. In the past, Hyperliquid relied on excellent product experience and institutional LP support to form trading depth close to that of centralized exchanges. However, when core LPs actively reduce their market-making exposure for mainstream assets like BTC and ETH, it indicates that the platform's liquidity is not entirely endogenous and still relies on external professional capital for continuous support.

This also means that although Hyperliquid is an on-chain trading platform, its underlying liquidity logic is not entirely decentralized. The order book model still requires professional market makers to bear inventory risks, rather than relying primarily on passive liquidity pools like AMM. When market makers' risk preferences decline, the platform may still maintain high trading volumes on the surface, but its vulnerabilities in extreme conditions will be magnified.

3. Hyperliquid's Growth Is No Longer Just About Crypto Perpetual Growth

From a purely crypto-native perspective, Hyperliquid's success is not difficult to understand. It is based on an on-chain order book, providing a trading experience close to that of centralized exchanges, while constructing a valuation logic for exchange-like assets through HYPE buybacks, fee capture, and ecosystem expansion. For a considerable period, the market's core understanding of Hyperliquid has been "on-chain Binance" or "on-chain Perp DEX."

However, it appears that Hyperliquid is no longer just a perpetual trading platform for crypto assets but is entering the traditional asset trading field through its unique mechanisms. Traditional asset perpetual contracts such as crude oil and silver have begun to rank among the top trading volumes on the platform, sometimes even occupying important positions in the top ten trading volumes on Hyperliquid. This is crucial. One of the most imaginative aspects of Hyperliquid may not be simply moving BTC and ETH perpetuals on-chain, but transforming the "market closure time" of traditional markets into tradable assets.

Traditional financial markets do not operate 24/7 without interruption. During weekends, holidays, and sudden geopolitical events, traditional exchanges like CME and ICE may be closed. However, risk itself does not stop because exchanges are closed. Wars, sanctions, oil route disruptions, central bank statements, and political events can all occur while traditional markets are closed. At this time, the market still needs a place to express expectations, hedge risks, and form price references.

Hyperliquid has found a new growth entry point in this gap. During the geopolitical conflict between the U.S. and Iran, while traditional markets were closed, the WTI crude oil perpetual contracts on Hyperliquid could still be traded in real-time, reflecting price shocks before traditional markets reopened.

This means that Hyperliquid's narrative may have expanded from "crypto asset trading" to "continuous pricing of global risks." It is not just an on-chain casino or another Perp DEX, but is attempting to become a price discovery layer during the closure of traditional markets.

From this perspective, Hyperliquid's value does not entirely stem from the idea of decentralization but from its practicality. When traditional markets close, it remains open; when macro risks cannot wait for the next trading day, it provides a place for immediate price expression. This demand is real and explains why traditional asset trading has rapidly grown on Hyperliquid.

4. From Crude Oil to SpaceX, Hyperliquid Is Expanding Its Business Radius

Hyperliquid's rapid expansion into traditional asset trading is closely related to the HIP-3 mechanism. According to official information, HIP-3 allows deployers to create new perpetual contract markets after staking a certain amount of HYPE. Deployers can define market parameters, oracle sources, leverage limits, and necessary settlement rules.

This mechanism is significant for platform growth. It effectively opens up the ability to launch trading pairs from the internal teams of centralized exchanges to some extent to external market deployers. As long as someone is willing to bear the costs and provide market design, Hyperliquid can theoretically expand rapidly into more asset classes. This transforms it from a crypto perpetual platform into a scalable on-chain derivatives base.

At the same time, Hyperliquid's latest launch of HIP-4 further opens up new product boundaries. Unlike HIP-3, which mainly focuses on perpetual contracts, HIP-4 leans towards Outcome Trading, i.e., prediction markets and event contracts. Such contracts are typically priced and settled around the outcomes of real-world events, such as whether a price reaches a certain range or whether a macro event occurs. In other words, HIP-3 allows Hyperliquid to expand into more perpetual assets, while HIP-4 further enables it to enter the fields of prediction markets and event trading.

However, problems also arise here. Perpetual contracts are not simple spot trades, especially when the underlying assets expand from cryptocurrencies to crude oil, stocks, Pre-IPO, and other real-world assets, the issues the platform faces become more complex. When HIP-4 further introduces prediction markets and event contracts, the regulatory scope that Hyperliquid touches may extend beyond derivatives trading itself to more sensitive areas such as event contracts, gambling, election predictions, sports outcomes, and macro event trading.

In other words, the more successful Hyperliquid's growth, the more complex the regulatory issues it faces. It is no longer just an unlicensed trading platform but is becoming a market experiment that moves the most difficult-to-enter, highest-threshold, and most controversial price discovery aspects of traditional finance onto the blockchain.

From a product perspective, this innovation is highly attractive. In the past, ordinary traders could hardly participate in price discovery for unlisted companies like SpaceX, relying only on rumors from secondary markets, private equity valuations, or public markets after listing for indirect judgments. The emergence of on-chain Pre-IPO perpetuals allows the market to continuously price unlisted assets at an earlier stage. Meanwhile, if HIP-4 further develops, it may also allow users to express their judgments on macro events, market outcomes, and real-world events through prediction markets.

However, from a regulatory perspective, this also means Hyperliquid is entering a more sensitive area. Because Pre-IPO assets are not simple crypto assets, their prices often involve information asymmetry, non-public financing, qualified investor restrictions, and securities issuance rules; while prediction markets are not ordinary trading varieties, their outcome determinations, event designs, and participant scopes have long been under regulatory controversy. Once these on-chain prices are widely referenced by the market, they are no longer just speculative contracts but may become external price signals that influence private market expectations, macro event judgments, and even real asset pricing.

5. CME and ICE Pressure, Essentially a Struggle for Price Discovery Rights

At the same time, CME and ICE are pushing the CFTC and U.S. legislators to strengthen regulation of Hyperliquid. Their concerns mainly focus on several aspects: the current anonymous trading model of Hyperliquid may bring risks of market manipulation and sanctions evasion; the rapidly growing crypto and commodity-related trading on the platform may affect key market price discovery, including crude oil; and without customer identification and trading monitoring, regulators find it difficult to confirm participant identities and trading motivations. On the surface, this is a regulatory questioning of on-chain derivatives platforms by traditional exchanges. But at a deeper level, it resembles a struggle for price discovery rights.

CME and ICE have long held important trading and clearing infrastructure for global commodities, stock indices, and interest rate derivatives. Their value comes not only from facilitating trades but also from benchmark prices, liquidity networks, clearing credit, and regulatory recognition. When Hyperliquid begins to form on-chain prices for crude oil, stock indices, Pre-IPO, and even event contracts during traditional market closures, it effectively touches the core moat of traditional exchanges.

This is also why the regulatory pressure on Hyperliquid has rapidly intensified after the growth of traditional asset trading. If it were just a crypto-native Perp DEX, traditional exchanges might not pay such close attention. But when it begins to serve as an immediate trading venue for weekend oil prices, geopolitical conflicts, stock index expectations, and private asset valuations, the issue shifts from "whether a DeFi project is compliant" to "who is qualified to generate prices when global markets are closed."

Hyperliquid's response to this is also noteworthy; it emphasized in its comments submitted to the CFTC that on-chain trading records are publicly available in real-time, and all orders, transactions, and settlements are traceable, thus theoretically offering higher transparency than traditional markets. At the same time, 24/7 trading can reduce traditional market opening gaps, allowing the market to reflect information more continuously.

This response is not without merit. On-chain transparency can indeed reduce some risks of opaque trading and provide complete data for post-event investigations. However, transparency does not equate to compliance. Regulators are concerned not only about whether trades can be seen but also about whether participants can be identified, whether abnormal trades can be intercepted, whether sanctioned entities are excluded, whether market deployers bear obligations, and who is responsible for maintaining market order during systemic events.

It is also worth noting that CME itself is accelerating the enhancement of 24/7 trading capabilities. CME's official information shows that its crypto futures and options are set to enter a 24/7 trading mode on May 29, 2026; additionally, CME plans to launch products like Nasdaq CME Crypto Index Futures. In other words, traditional exchanges are not opposed to 24/7 trading itself but are demanding that on-chain competitors bear similar compliance costs while incorporating this capability into a regulated framework.

Source:https://www.cmegroup.com/markets/cryptocurrencies/24-7-crypto-trading.html

Thus, the conflict between Hyperliquid and traditional exchanges is not simply a confrontation between new and old finance but a collision of two market orders. One order emphasizes openness, transparency, 24/7 operation, and global unlicensed access; the other emphasizes access, monitoring, clearing, licensing, and accountability. The former is more efficient, while the latter incurs heavier institutional costs. However, when trading targets enter crude oil, stock indices, Pre-IPO assets, and prediction markets, institutional costs are difficult to circumvent in the long term.

6. Deeper Reflections

Is Hyperliquid the next-generation exchange of on-chain finance, or a rapid expansion beyond regulatory boundaries? From the short-term trading data, it remains in a strong cycle, with trading volume, open interest, HYPE attention, and the expansion of traditional asset trading all indicating that market demand is real. However, when viewed over a longer period, the withdrawal of market makers and the pressure from CME and ICE may be exposing a deeper issue: the on-chain trading infrastructure is entering the heart of traditional finance, but the corresponding responsibility structure has not matured in sync.

6.1 From Crypto Exchanges to Macro Price Discovery Layers

Hyperliquid's early competitive focus was on how to achieve a better perpetual trading experience on-chain. It addressed internal issues within the crypto market, namely how users could obtain low latency, high liquidity, and a rich variety of trading pairs without relying on centralized exchanges.

However, with the advancement of HIP-3 and HIP-4, Hyperliquid is entering another phase. It is no longer just serving crypto assets but is beginning to serve macro risks, private asset expectations, and real-world event outcomes. Crude oil prices, stock index fluctuations, geopolitical events, Pre-IPO valuations, prediction markets, and traditional market closure windows may all become sources of its growth.

This is also where it is most imaginative. The time structure of traditional financial markets does not adapt to the current speed of information dissemination. Information spreads in real-time, risks occur in real-time, but many official trading venues for assets are not open in real-time. Hyperliquid provides an alternative outlet, allowing market participants to continue expressing expectations during traditional market closures.

But this also means that it is no longer just a product issue but a market order issue. If a platform only allows users to trade MEME or crypto perpetuals, its impact remains primarily within the crypto circle; but if it begins to influence oil prices, stock indices, and macro asset expectations, it will naturally come under the scrutiny of regulators and traditional exchanges.

6.2 The Liquidity Illusion Behind Scale Growth

Hyperliquid's current data remains impressive, but the larger the platform scale, the more caution is needed regarding the liquidity illusion. Growth in trading volume does not necessarily mean the market is healthier, especially in high-leverage perpetual markets, where trading volume is often amplified by volatility, liquidations, high-frequency arbitrage, and repeated turnover.

To some extent, liquidity withdrawal does not necessarily mean institutions are turning pessimistic. For market-making institutions, periodically reducing exposure may also be to retain some space for more cost-effective liquidity deployment in the future. But the key question is whether there is still enough professional capital willing to bear counterparty risk when unilateral market conditions arise. The changes in Wintermute and Auros related addresses indicate that institutional market makers have begun to reassess this issue. They do not deny Hyperliquid's product capabilities but have raised higher demands for future risk compensation.

As regulatory uncertainty rises, traditional asset trading becomes sensitive, and the platform is publicly scrutinized by CME and ICE, market makers need to consider not only trading profits but also address exposure, compliance inquiries, sudden exits, and tail events. Market-making capital naturally chases returns but is also extremely averse to unpriced risks. Once a certain type of risk cannot be effectively measured by models, the most direct reaction is to reduce positions, withdraw orders, and decrease quote depth.

Therefore, the core of this event is not whether Hyperliquid's liquidity will collapse immediately but whether its liquidity costs may begin to rise. In the future, if Hyperliquid wants to maintain depth and continue providing market makers with a high-return, high-growth, low-friction environment, it may need to offer market makers higher returns, clearer rules, or lower institutional risks. Otherwise, the larger the platform's trading volume, the more pronounced the liquidity gap may become in extreme conditions.

6.3 Responsibility Reconstruction in Open Markets

The attractive aspect of Hyperliquid lies in its lowering of the barriers to market creation and asset trading. However, as market creation becomes more open, the boundaries of responsibility will also become blurred.

In traditional exchanges, when a new futures contract is launched, it typically undergoes strict product design, regulatory review, risk control models, clearing arrangements, and market monitoring. In an on-chain environment, the responsibilities between market deployers, oracles, market makers, protocols, and users are fragmented, and no single entity may bear full responsibility for the final risk.

This may be acceptable in the realm of crypto-native assets, as participants generally assume high risks and self-responsibility. But in traditional assets and prediction markets, the situation changes. Crude oil, stock indices, and Pre-IPO prices have externalities; they not only affect speculators but may also influence expectations in the real market; while event contracts and prediction markets involve outcome determinations, participant scopes, and real event pricing issues. When on-chain prices begin to be observed, referenced, or arbitraged by external parties, regulators will demand clearer chains of responsibility.

This is also an issue that Hyperliquid cannot avoid in the future. It can continue to emphasize on-chain transparency and the efficiency gains of 24/7 trading, but if it cannot answer "who is responsible for market quality, who is responsible for abnormal trading, who is responsible for access review, and who is responsible for clearing extreme risks," then its expansion into traditional assets will always remain in a gray area.

7. Conclusion

The controversy surrounding Hyperliquid does not mean the story is over; rather, it indicates that it has truly entered the sights of the traditional financial system. In the past, discussions about Hyperliquid were more about whether an on-chain perpetual trading platform could replicate the efficiency of centralized exchanges; now, discussions about Hyperliquid are about whether an unlicensed on-chain market is qualified to participate in the price discovery of crude oil, stock indices, private equity, and even real events.

This is also the most noteworthy aspect of this round of market maker withdrawals. The changes in Wintermute and Auros related addresses do not necessarily represent a denial of Hyperliquid's product capabilities. On the contrary, professional market makers often know best where liquidity is, where trading volume is, and where profits lie. What they are truly re-evaluating is the new regulatory risks, reputational risks, and tail exit risks that Hyperliquid faces as it transitions from a crypto-native exchange to a global price discovery layer.

From this perspective, Hyperliquid's biggest challenge in the future may not be whether trading volume can continue to grow, but whether that growth itself will change its risk nature. If growth mainly comes from crypto-native assets like BTC, ETH, and SOL, it remains a high-efficiency on-chain trading platform; but if growth increasingly comes from real assets like crude oil, stock indices, SpaceX Pre-IPO, and prediction markets, it must answer the long-standing questions faced by traditional finance: who is qualified to create markets, who is responsible for price quality, who bears responsibility for abnormal trading, and who maintains order during extreme conditions.

Therefore, the core contradiction for Hyperliquid going forward is not a simple conflict between decentralization and regulation, but a rebalancing between open price discovery and institutional responsibility. Its most valuable aspect lies in proving that global risks can be traded in real-time on-chain; its most dangerous aspect is that once this price begins to be referenced by external markets, it cannot forever remain within the narrative of "code is law."

Hyperliquid is entering a more challenging phase; in the past, the market focused on whether its on-chain order book met demands in terms of efficiency, depth, and experience. Now, the real test lies in whether it can introduce clearer identity, compliance, and responsibility mechanisms while maintaining openness and on-chain characteristics, thereby meeting the requirements of traditional finance for market structure and regulation. Whether it can achieve such a transformation will determine whether Hyperliquid ultimately remains a leading Perp DEX or becomes a core variable in the next generation of financial market structures.

Risk warning

Risk warning