Depth | Will the free lunch last - What does liquidity mining bring to the DeFi ecosystem?

This article provides a quick overview of liquidity mining in DeFi and delves into the reasons behind its rapid adoption and forecasts its future prospects.

This article provides a quick overview of liquidity mining in DeFi and delves into the reasons behind its rapid adoption and forecasts its future prospects.This article was published on July 28, 2020, by Dong Xinshu, Zheng Bohan, Momir, and Xiao Rui.

Suddenly, as if a spring breeze came overnight, thousands of voices began to discuss DeFi. Out of nowhere, DeFi, once questioned as a pseudo-demand, has started to be discussed with anticipation. What exactly is DeFi? Do you really understand it? We believe that the main logic behind decentralized finance (DeFi) is to create financial products and protocols using smart contracts running on the blockchain, allowing us to create a more open, transparent, and fair market, better suited for financial democratization and innovation.

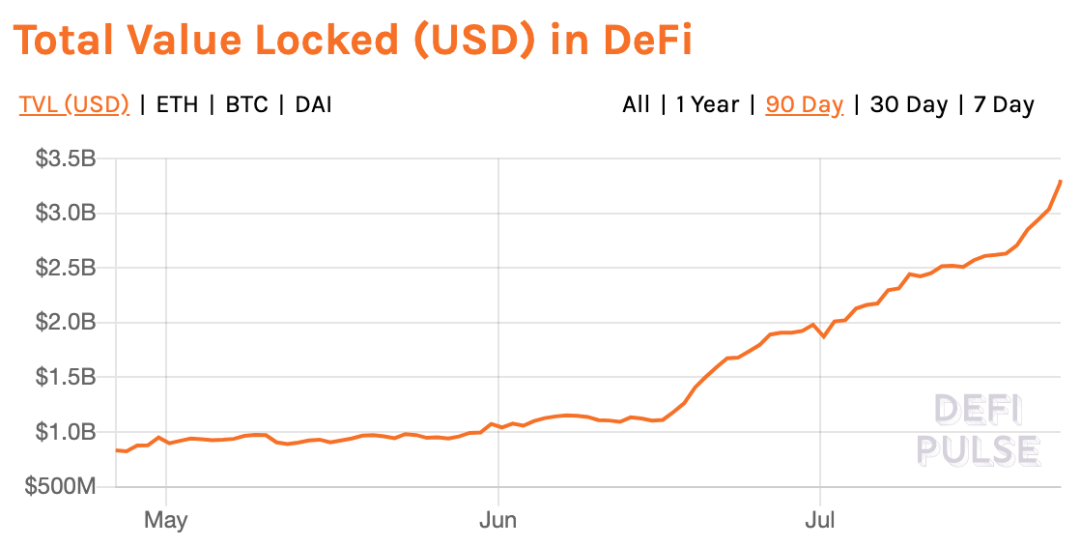

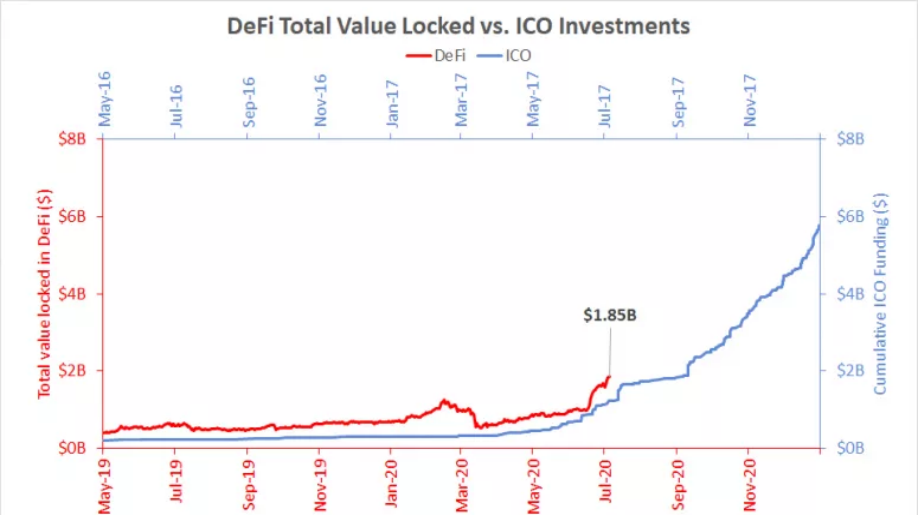

The trading volume of DeFi has been growing significantly throughout 2019, and as we entered 2020, its total locked value experienced the first sharp exponential growth period.

Recently, with the trend of market recovery, early DeFi projects have sprung up like mushrooms after rain. We believe that the main driving force behind the faster implementation of DeFi is the concept known as liquidity mining, which was first applied to Compound and then to other DeFi protocols.

In this article, we provide a quick overview of liquidity mining in DeFi, then delve into the reasons behind the rapid adoption of liquidity mining and predict its prospects.

First, let's take a look at the market size of DeFi. As of July 27, 2020, the total value locked in DeFi was $4 billion. This number may not seem large, but just three months ago, the DeFi market was only $600 million, and it has grown sevenfold in three months. We believe this is an impressive achievement even in the rapidly developing blockchain field.

Overview: Why Liquidity Mining Has Emerged

Simply put, liquidity mining describes users providing "liquidity" to the market in some way while receiving additional incentives beyond interest, thereby increasing the activity and usage of the product. However, at a higher level, this concept is very similar to other incentive programs (like Uber's ride incentive program), because both ultimately aim for users to spontaneously continue using their products to achieve network effects. However, liquidity mining in DeFi has some fundamental and unique features. Here, we first attempt to provide a proper definition of DeFi liquidity mining and explain its scope.

We believe that not all liquidity incentive programs are liquidity mining. In this report, we follow these two simple criteria:

- A project has its native governance token;

- The protocol layer uses the governance native token to reward its liquidity-providing users to incentivize them to use its products.

Based on these criteria, projects like Uniswap, which reward liquidity providers with protocol layer fees, will not be included in this report.

The following chart lists the current liquidity mining situation in DeFi, where Compound dominates the market, and the remaining share is divided among several scattered projects (Curve, bZx, and mStable).

The amounts in the chart represent the monthly allocation of liquidity mining by the project, with prices calculated as of July 9.

Data Source: CoinMarketCap

I. Starting with Traditional Lending, The Surge of DeFi Lending and Liquidity Mining

The types of DeFi markets vary, including lending, automated market makers, decentralized exchanges, derivatives, insurance, oracles, and prediction markets.

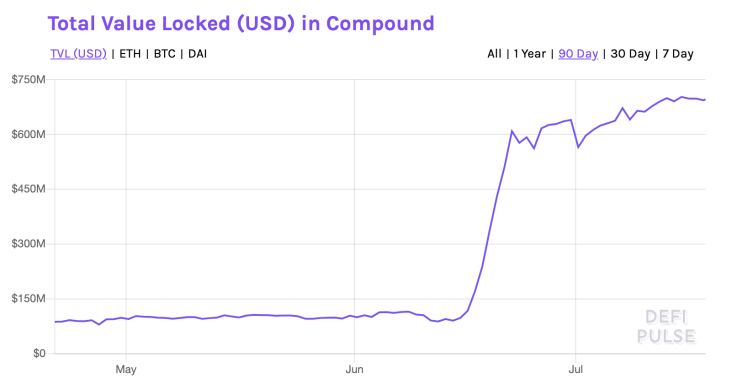

Lending protocol platforms can be said to be the most popular and fastest-growing area of DeFi, and they were the first to launch liquidity mining programs. Most DeFi lending projects offer traditional collateralized loan products, where users can deposit assets into the lending platform's treasury and borrow other assets against their collateral. Users earn interest income by providing collateral, while also paying interest on borrowed assets. According to DeFi Pulse, the popular DeFi lending platform Compound is currently one of the dominant projects in the DeFi market, contributing 19% of the total locked value (as of July 23, 2020).

In traditional finance, creating a bank that provides lending services requires a significant amount of capital. In the world of DeFi, this money is primarily provided by a market that is entirely automated and carefully arranged by smart contracts. Therefore, the rules for lending without trusting any intermediaries (such as banks) have been established and will be executed by the blockchain. However, to guide this process, projects need to propose revolutionary methods to attract holders of idle assets to supply them.

In practice, many DeFi lending protocols have begun to use the concept of asset pools to allow smart contracts to automatically adjust interest rates based on the supply and demand of different assets. Compared to centralized lending projects, DeFi lending can offer competitive interest rates. However, DeFi lending has steep learning curves, operational inconveniences on cryptocurrency wallets, and technical risks, which may prevent enough users from providing liquidity to DeFi lending pools, thereby reducing interest rate advantages. Worse, this adverse interest rate may cause users to move assets elsewhere, further depleting the funding pool and ultimately creating a vicious cycle.

On the other hand, liquidity mining could greatly drive the DeFi lending market in a positive direction, especially when the returns from liquidity mining exceed interest rate fluctuations. This article will explain how liquidity mining works through an analysis of Compound.

II. The First Project to Add USDT as a Protocol Asset: Compound

Compound is a pioneer of liquidity mining. It began distributing its governance token COMP on June 15, 2020. Since the introduction of this yield-generating new product, more crypto users have poured assets into the DeFi market.

Source: Coindesk

For Compound, the core of the governance token is the right to vote on proposals to update the protocol. Since the project operates automatically via smart contracts, this voting right is the only way to change how things work in the product. Compared to governance models in the traditional world, the COMP token is like a document granting voting rights in a legislative body.

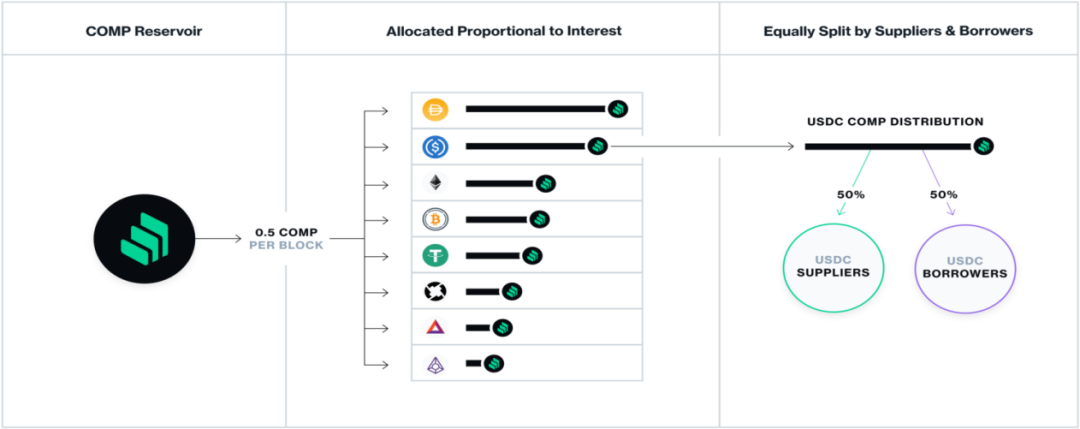

0 1, How Does Compound's Liquidity Mining Work?

Source: Compound Medium

In Compound's liquidity mining, a total of 4,229,949 COMP tokens will be placed into a "pool" contract and distributed equally (50/50) to depositors (i.e., liquidity providers) and borrowers. The tokens will be fully automated in distribution over four years. Currently, 0.5 COMP will be distributed per Ethereum block (which means 2,880 COMP are issued daily). Compound users can earn COMP based on the value of their assets simply by lending/borrowing digital assets through the system.

Once the COMP tokens accumulated by an address reach 0.001, any subsequent transaction on the Compound platform will automatically transfer the pending COMP to the user. If the accumulated COMP tokens are less than 0.001, users have the right to manually claim COMP.

Recently, overseas communities have taken to calling liquidity mining "Yield Farming," which not only refers to trading on Compound to earn COMP but also represents strategies for using cryptocurrencies to create maximum returns.

Examples of Yield Farming include:

- Moving funds to higher-risk lending pools for better yields.

- Adopting different trading strategies. For example, arbitraging in other protocols, collateralizing borrowed assets to borrow other assets, and reinvesting the newly borrowed assets back into the lending pool for higher returns.

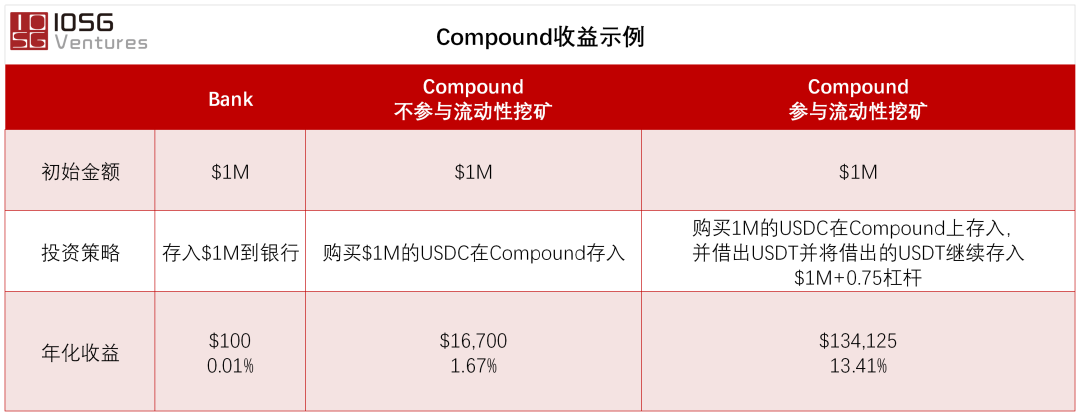

Data: COMP price on July 9, 2020, $184.64 USD; USDC deposit APY 1.67%, USDT borrowing APY: 8.62%, USDT deposit APY: 2.1%, USDC COMP APY: 3.65%, USDT COMP borrowing APY: 13.03%; USDT COMP deposit APY: 3.92%; Chase's annual deposit rate of 0.01% announced on July 3, 2020.

Note: This model does not consider time costs, inflation, and other macro factors. This model does not account for complex investment logic and transaction fees. In comparison, the risks of bank deposits differ from those in DeFi lending protocols, and the comparison results have not been adjusted for risk; this comparison is for general reference only and does not constitute any investment advice.

III. The Block Effect of DeFi Protocols Emerges, Liquidity Mining Protocols Surge

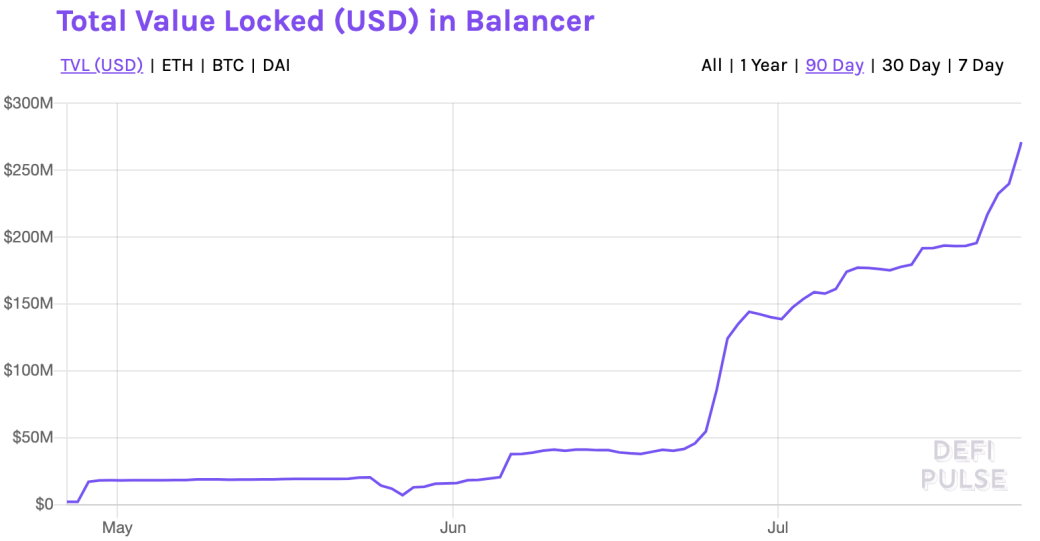

In addition to the lending market, liquidity mining has also gained increasing attention in automated market maker (AMM) projects. To provide effective low-slippage trading, AMMs rely on the depth of liquidity pools. Therefore, introducing liquidity mining in this area is straightforward. The two most prominent projects applying liquidity mining in AMMs are Balancer and Curve. Since June 1, 2020, liquidity providers on Balancer have been able to "mine" BAL tokens. In the first month after the BAL distribution began, the total locked value on Balancer increased by 680%!

Source: DeFi Pulse

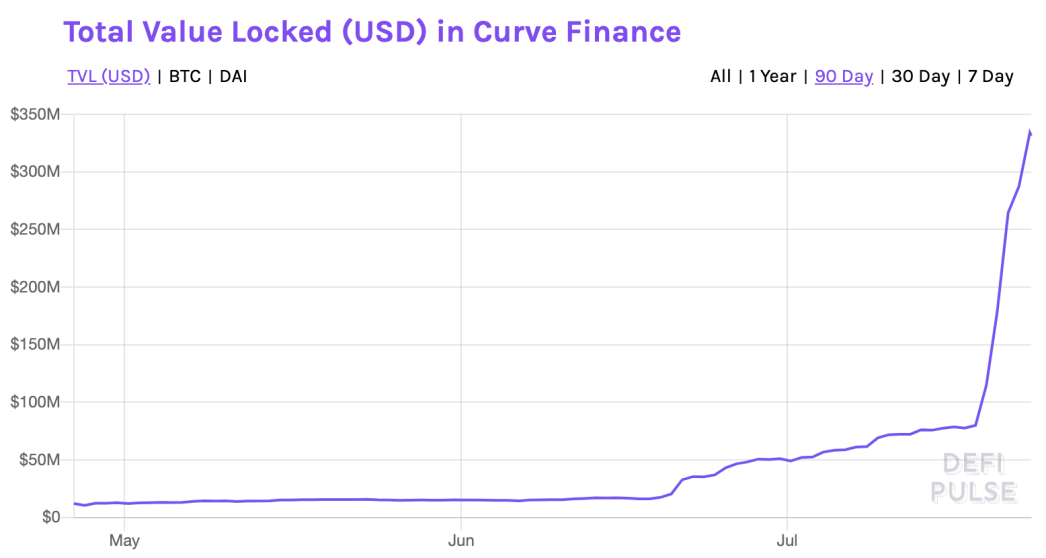

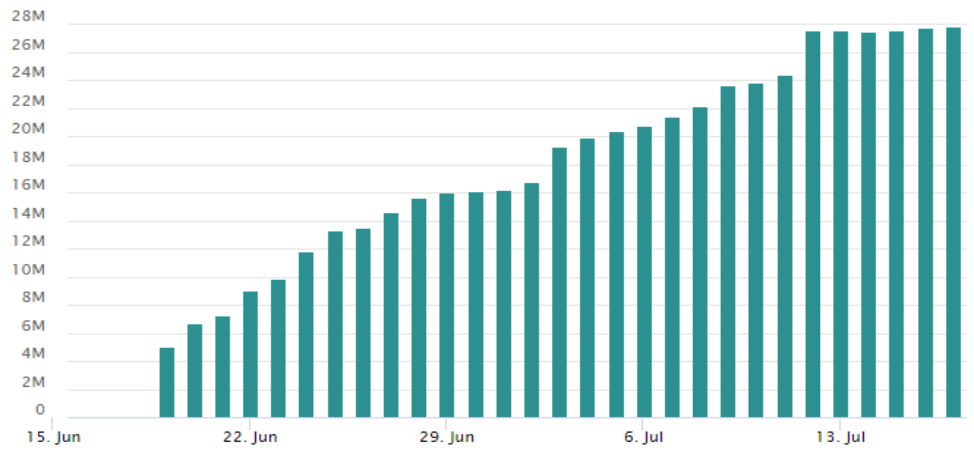

On the other hand, Curve plans to start issuing CRV tokens around the end of July, with tokens distributed retroactively to all liquidity providers based on their contributions and the duration of their contributions in the Curve liquidity pools. As shown in the figure below, Curve has recently attracted a large amount of deposits.

Source: DeFi Pulse

The table below compares the main DeFi projects offering liquidity mining (as of July 23, 2020):

Data Source: CoinMarketCap, CoinGecko

DeFi projects have generated many methods to call upon mining idle tokens worth hundreds of millions of dollars lying in wallets. Liquidity mining has attracted a significant portion of funds in a relatively short time. Before the introduction of liquidity mining (in June), only about $135 million was locked in the Balancer and Curve liquidity pools, but as of July 23, this value exceeded $1.175 billion.

IV. Reflecting on the Essence: Why Has the Explosive Growth of Liquidity Mining Occurred, and Is It Sustainable?

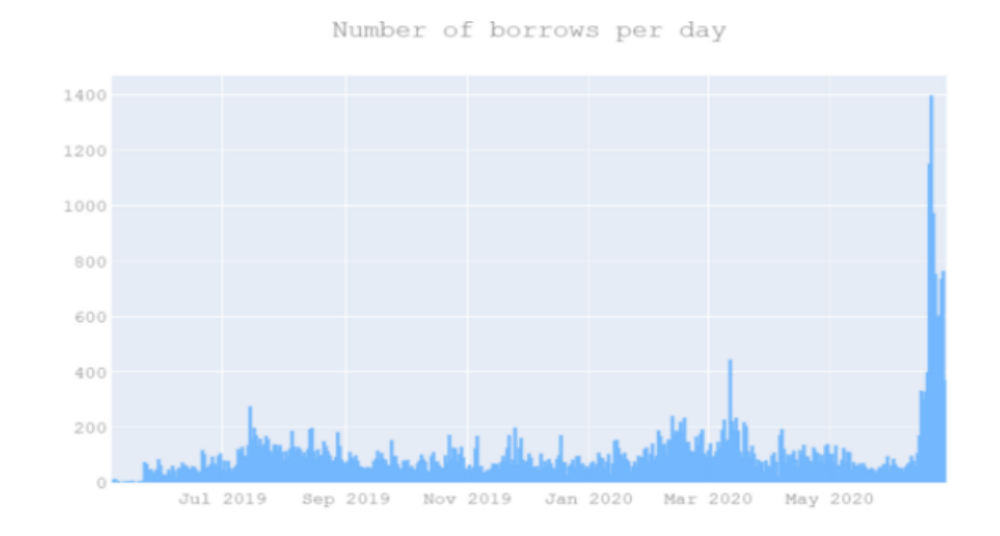

First, we believe that the reason for such explosive growth is due to the uniqueness of the COMP reward distribution, which allows borrowers to also earn 50% of the total COMP distribution by borrowing on Compound. Simply put, borrowers can earn COMP tokens just by borrowing!? Sounds perfect, right? This has led to a significant surge in borrowing (as shown in the figure below), further driving up interest rates, making supplying funds on Compound more attractive in the short term.

Source: Alberquilla

Perhaps another potential factor for the price increase of governance tokens like COMP is that users are using "Total Value Locked" (TVL) as a valuation method for DeFi projects.

Taking yearn as an example. On July 17, 2020, the locked value (TVL) of yearn on Curve was about $8 million. Three days later, as of July 20, 2020 (Monday), this number had increased to $147 million. The increase in TVL drove the price of its governance token YFI, which surged from an initial valuation of $30 to $2,374.

CoinGecko research analyst Daryl Lau pointed out that in the case of "liquidity mining," the value of the project is reflected through the token price itself, which has also given rise to a form of "pseudo-Ponzi economics." The rise in token prices encourages more people to lock assets on the platform, thereby increasing TVL. High TVL further boosts token prices, creating a cycle. We believe this cycle will not last, as this valuation method is not mature.

0 1, Some viewpoints suggest this will be a zero-sum game?

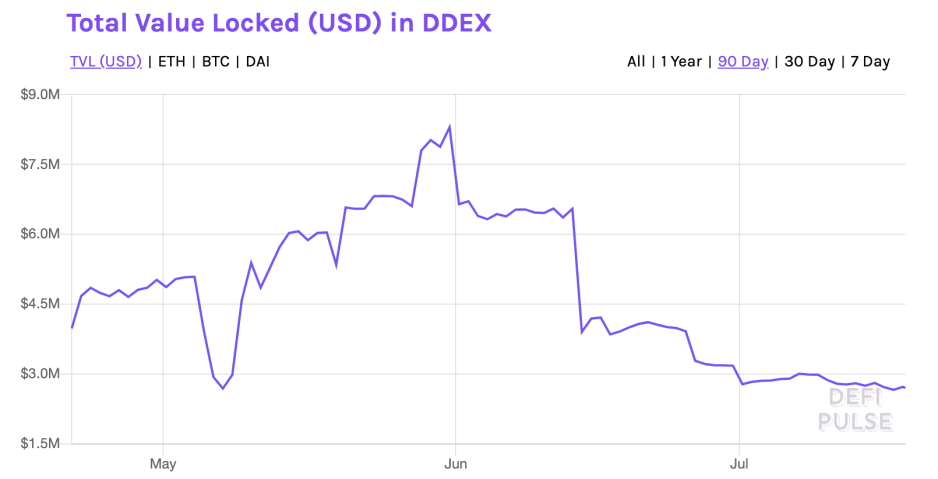

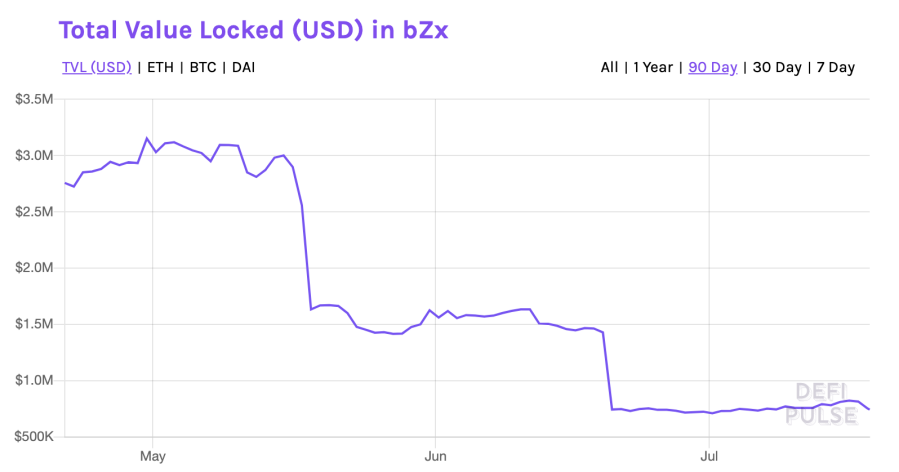

The total value locked in DeFi surged from around $1 billion in early June to about $2 billion in early July, with a significant portion of the new funds allocated to Compound. Additionally, by observing the total locked value of other lending protocols, we found that after June 15 (when COMP distribution began), the total locked value of protocols like Maker, InstaDapp, DDEX, Nuo Network, and bZx showed a noticeable decline. Maker and InstaDapp quickly recovered a few days later, but other protocols have yet to recover from the decline.

Source: DeFi Pulse

Source: DeFi Pulse

Source: DeFi Pulse

Does this mean that DeFi funds are flowing toward a specific direction/project cluster? We believe this is possible. If so, these projects must be based on sustainable models; otherwise, they will pose systemic risks to the entire DeFi.

As of July 23, the top five DeFi projects (Maker, Compound, Aave, Synthetix, and Curve) controlled 78% of the total value locked in the DeFi market. Considering that many projects share some commonalities with leading DeFi protocols (for example, Maker, Yearn, RenVM, Curve, and Compound are interconnected), if one of these leading projects experiences a negative event related to smart contracts or oracles, it could trigger a domino effect across the entire DeFi.

Since DeFi is still a nascent market, such adverse events, once they occur, may take a long time for the entire ecosystem to recover.

02 Can Borrowers Continuously Earn Returns by Borrowing, or Will the Free Lunch Last Long?

It is evident without expert analysis that the high returns borrowers earn on Compound are unsustainable.

If we assume that these incentives will continue to attract new users, then over time, as the user base grows exponentially, the share each user receives will diminish as the rewards remain fixed.

COMP was designed solely as a governance token. It is akin to purchasing stock in a company, which grants you voting rights but has no immediate dividend plan. Currently, the largest voting rights are controlled by large institutions like a16z and Polychain Capital.

As of July 23, purchasing each vote-capable COMP token costs about 158 yuan, but each COMP token only provides 0.00001% of voting rights and has no cash inflow (dividends).

Tokens that provide concrete economic benefits to holders are easier to value; however, the valuation of non-dividend governance tokens can be highly subjective.

Currently, the valuation of COMP seems to contain speculative factors. We believe that in the long run, before the governance layer of COMP decides to provide some form of dividends to COMP token holders, the present value of COMP is likely to approach the intrinsic value of the token (voting value).

Moreover, we believe the following situations could exert additional downward pressure on the COMP market, making corrections to such speculative valuations likely to accelerate:

Adverse market events leading to excessive liquidations, which could prompt speculators to sell COMP en masse;

Any form of market panic, including general technical risks associated with smart contracts; and

More likely, speculative holdings may lead profit-seeking holders to choose other higher-yield projects, triggering a decrease in liquidity and COMP prices.

Thus, when and how liquidity mining in DeFi projects will find a medium- to long-term balance point, and whether it will still attract yield-seeking users at that time, remains an interesting question.

0 3 There Is Nothing New Under the Sun---What Can We Learn from the FCoin Example?

If we take a step back, the first high-profile project to experiment with liquidity mining in the cryptocurrency field might be FCoin. FCoin is a Chinese cryptocurrency exchange that launched an incentive program in May 2018, distributing its platform token to reward users who traded on the platform.

A total of 10 billion FT (FCoin token) were issued, with 51% allocated as rewards. Additionally, it distributed 80% of daily trading fees in BTC to users who held FT continuously throughout the day.

As a result, by the end of June 2018, FCoin's daily trading volume exceeded $5.6 billion, surpassing the combined trading volume of the top ten exchanges. Nevertheless, when FCoin announced a delay in FT payouts, the price of FT plummeted from $1.25 to $0.66. This indicated that most users trading on FCoin were doing so to profit from FT rewards, creating a massive bubble in FT's price.

Ultimately, the platform was shut down in February 2020, failing to pay users between $67 million and $125 million.

We believe there is a key distinction between DeFi and FCoin's liquidity mining. The failure of FCoin was largely due to misappropriation of funds and a lack of community governance, making it resemble a scam. In contrast, liquidity mining in DeFi has traceable token distribution, and the use of funds is entirely governed by smart contracts and is transparent.

Moreover, FT mining encouraged wash trading, which has no real value, while liquidity mining incentivizes the provision of liquidity, bringing genuine value to market depth.

Nevertheless, we believe the aforementioned differences do not necessarily alleviate the concerns we discussed earlier regarding token valuation, nor do they indicate that the current liquidity mining in DeFi will continue to thrive. However, we believe that the inherent transparency and value-creation nature of DeFi liquidity mining can provide a fairer competitive environment for all participants, allowing us to explore sustainable development paths that were impossible in the case of FCoin.

04 What Can We Learn from Traditional Finance? The Case of Jet.com

Jet.com (founded in 2014) is a startup with a business model similar to Amazon. It raised $80 million in early 2014, but they believed attracting new users was more important than securing funding. Therefore, they launched an equity reward program for new user registrations.

The company decided to hold a competition where the participant who introduced the most new users could win 100,000 shares of the company stock, while the second to tenth place participants would each receive 10,000 shares. This equity reward program ultimately succeeded in bringing in 350,000 new registered users.

To earn the stock, participants effectively spent their own money on marketing and advertising to ensure new users could register through their personal referral links. These participants worked like employees and had a strong motivation to grow the business.

The winner, Eric Martin, spent $18,000 to attract 8,000 new users and earned 100,000 shares. Subsequently, Jet.com was acquired for $3.3 billion, and Eric made $10 million.

First, we want to know what we can learn from Jet.com's success story. We believe that aligning the long-term interests of the project with those of users is key to maintaining sustainability.

The current liquidity mining in DeFi resembles a game played by users. People engage in liquidity mining not because they are betting on the company's success, but because they focus on short-term profit opportunities.

Eric from the Jet.com case mentioned, "I felt like I was tied to the success of the company." This is because he had to wait until the company went public or was acquired by another company to cash out, thus maintaining aligned interests with the company.

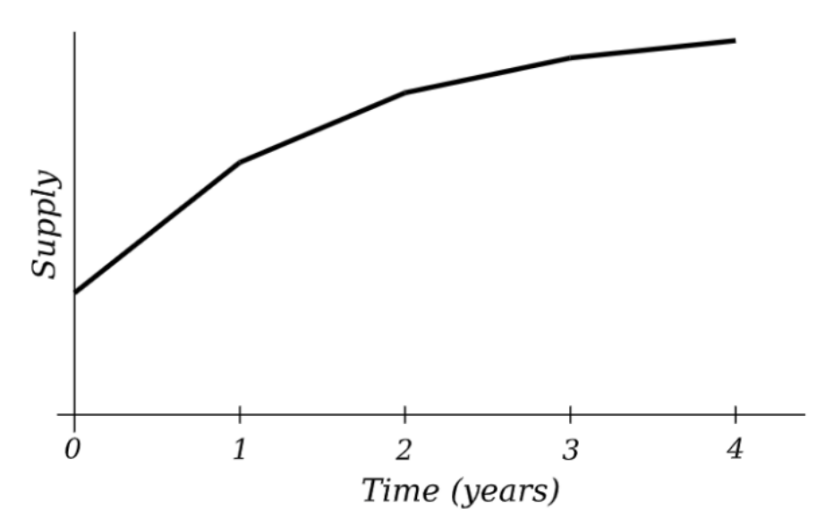

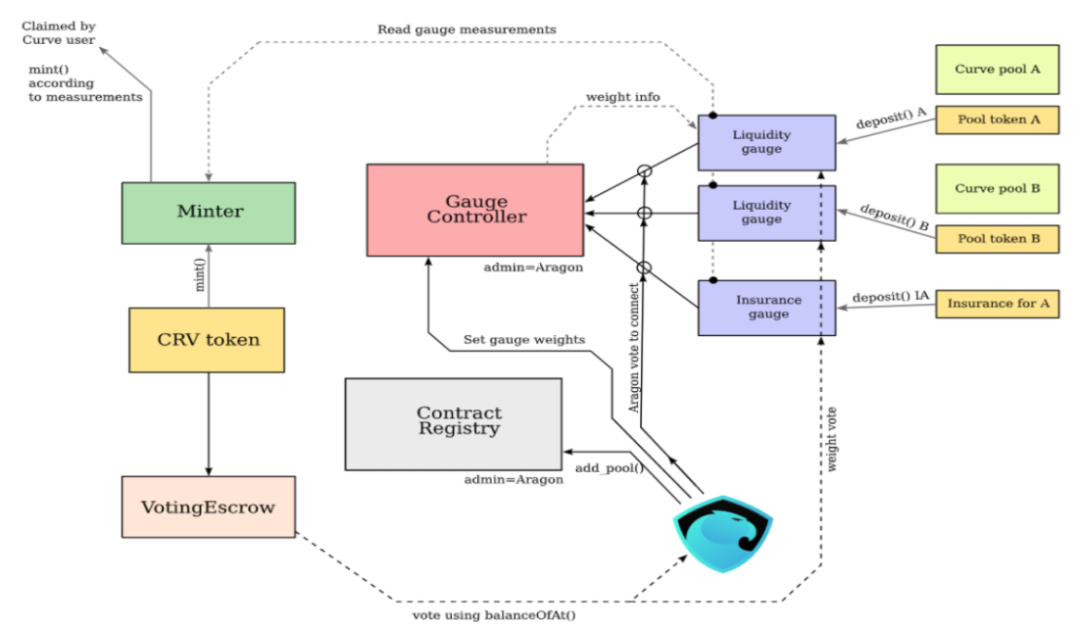

Therefore, we believe that if DeFi projects wish to maintain long-term alignment of interests with users and token holders, some form of lock-up period is necessary. Fortunately, we have seen some projects moving in this direction. For example, Curve Finance announced that users who lock their CRV tokens will be able to increase their share of holdings fivefold in inflation, as the project hopes to create natural lock-up behavior through this incentive.

Currently, the proposal for the lock-up plan is: the total supply of CRV proposed is 1 billion, which will gradually expand to a maximum of 3.33 billion. The inflation rate for the first year will be set to the highest, after which the inflation rate will decrease, but the total supply will gradually expand over time, indicating that early token holders will gain the most benefits.

Similarly, they will also use time-weighted voting, allowing users who lock tokens to have more governance weight than new users. For example, the voting weight of one token locked for four years is equivalent to that of 200 tokens locked for one week, thus alleviating the model where one token equals one vote (which greatly favors those with substantial funds).

Source: Curve Github

By doing this, Curve ensures that its stakeholders will have aligned interests with the protocol for the foreseeable future, setting an example for other projects.

05. Summary: What Have We Learned So Far to Sustain Liquidity Mining?

We hope that different DeFi projects can maintain continuous development, as these protocols are highly interconnected and provide great composability in DeFi. Given this, we believe that switching from one protocol to another will be quite easy for most users, and in this case, innovation capability and a cohesive community will ultimately play a key role in determining a protocol's long-term success.

Innovation is not just a one-time event but a continuous process. The most innovative protocols will seize the extreme positions. We believe that despite the high composability of DeFi protocols, ultimately, a few projects will capture the vast majority of users and be heavily aggregated by other projects, becoming the "backbone" of the DeFi space.

A strong and cohesive community is crucial for the sustained success of DeFi protocols, as almost everything is dynamically changing in innovation, adaptation, and development.

Due to its decentralized nature, DeFi projects will ultimately be driven by their communities, which will take ownership and guide the direction of the projects. The community is especially important for nascent fields like DeFi, as every project competes for the best talent to support and drive it.

The fully community-governed model of the yield aggregator Yearn demonstrates the power of decentralized community governance.

In the days following the launch of the Yearn token YFI, it was realized that its founder Andre had the ability to mint tokens at any time. Therefore, he also handed over control of the governance contract to the community (including nine community members, such as Calvin Liu from Compound). As of the afternoon of July 27, 2020, YFI had proposed a total of 32 proposals, with 3 already passed, while the remaining proposals were in voting/discussion. In this short week, the enthusiasm of YFI community members was very high. More rarely, founder Andre Cronje did not allocate YFI tokens to himself, and these actions have allowed the project to transition to community governance at the fastest pace.

On the other hand, the community also changed the voting mechanism. Because the initially designed "98% yCRV / 2% YFI" pool used BPT, it caused an imbalance in voting weight, as yCRV requires staking stablecoins to earn, which allows users with large amounts of stablecoins to potentially mint a large supply of YFI through a single proposal. Therefore, the community improved this mechanism, establishing a voting structure led by YFI.

In the future, the yearn protocol will also expand into trading, futures, liquidation, and other areas. We also look forward to more projects innovating between sustainable business models and maintaining decentralization, truly building a BTC in the DeFi space.

The Future Outlook of Liquidity Mining, New Opportunities Brought by Protocol Layer Interactions

- Will more projects join liquidity mining?

Given the importance of liquidity in the DeFi space, the emergence of innovative liquidity incentive programs is not surprising. Considering the amount of funds attracted by Compound, we expect more projects to launch liquidity mining incentives. For example, the project bZx, which has recently been struggling to retain users (with total locked value dropping from $1.5 million before Compound initiated liquidity mining to $750,000 after COMP distribution began), has also announced a liquidity mining plan.

- What about bringing BTC into DeFi?

More broadly speaking about liquidity, we are closely watching projects that attempt to bring Bitcoin liquidity into DeFi. After all, Bitcoin remains the most liquid cryptocurrency (market cap > $1.7 trillion), so we cannot ignore the enormous potential of integration. We expect a steady flow of idle Bitcoin to flow into DeFi due to attractive yields.

Such projects include the sBTC pool on Curve, which allows holders of renBTC, sBTC, and wBTC to participate in liquidity mining. This project attracted deposits worth over $25 million within a month of its launch, and we expect this growth to continue.

Total Deposits in Curve's sBTC Pool

Source: Curve Finance

- Oracles Can Also Engage in Liquidity Mining

"On-chain oracles" are becoming a hot topic in the oracle industry, with the Nest protocol being a good example.

In the NEST system, some "miners" report prices to the system for mining. These "miners" are somewhat like liquidity providers in the Uniswap system. They need to input the quoted assets into the quoting contract according to trading pairs and provide a trading pair quote, which anyone can take.

At the same time, this quote must undergo market arbitrage testing. In other words, if the miner's quote has a price difference with mainstream exchange prices, this price difference will be exploited by arbitrageurs, and the remaining unfulfilled order quotes can be considered accurate.

Since on-chain oracle projects like Nest Protocol may require more quotes, we believe that the idea of liquidity mining will also be a potential mechanism for these projects to attract users and enhance their market liquidity.

- How to Best Utilize Liquidity?

We believe that the blockchain community will shift from solving liquidity issues to having sufficiently deep liquidity to output. Therefore, it is crucial to start building bridges from blockchain to the real world. After all, our goal is not to make blockchain an island, but to ensure that decentralized infrastructure and applications benefit the daily work and lives of ordinary people.

Aave's credit delegation and other initiatives provide a possible way to bridge this gap, allowing Aave users to delegate their credit on the blockchain to anyone based on legal agreements. This will enable those without blockchain knowledge to participate in DeFi and other blockchain applications.

It is important to note that in this case, liquidity pools do not bear any additional risks, as the conditions of the collateral remain unchanged. This is just one of many potential use cases connecting DeFi with real-world financial needs, and we believe this is a field with immense investment potential.

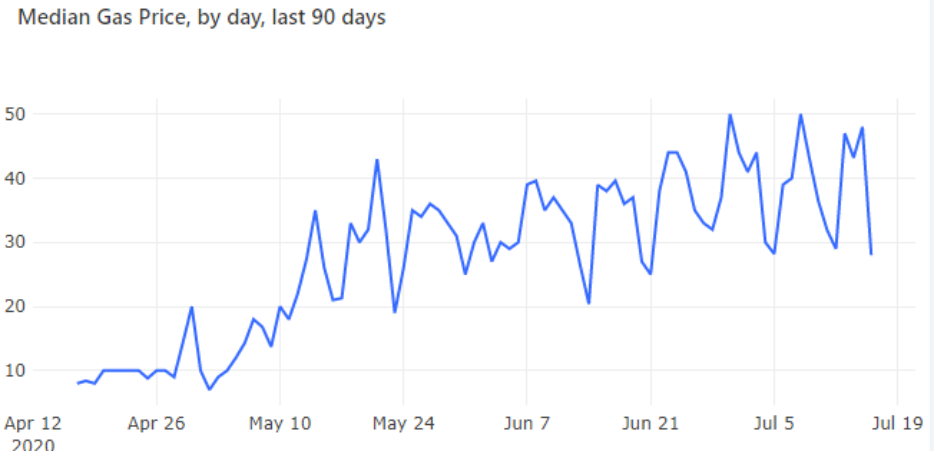

- Obstacles Along the Way---Gas Fees and Complexity

While users have enjoyed good returns through liquidity mining, we often hear complaints about high gas fees. This is especially true for highly integrated protocols like Curve, which reinvest liquidity pool funds into lending protocols like Compound or Aave.

This brings additional returns to liquidity providers but also results in multiple transaction fees. On the other hand, as the complexity of DeFi applications increases, the risk of liquidation during adverse market events may be exacerbated by excessively high transaction fees.

We believe that current liquidity mining will refocus attention on the infrastructure layer, and projects that can improve Ethereum's scalability without compromising user experience will become the next winners.

Source: Dune Analytics

As the DeFi market continues to grow, its complexity will also increase, so we believe that the demand for products that can alleviate the complexity of user interactions with DeFi protocols will continue to rise.

Such projects include user aggregators that enable "one-click" access to all DeFi protocols (like Instadapp, Argent, Gnosis Safe), which will see growth and may play an important role in attracting new cryptocurrency users.

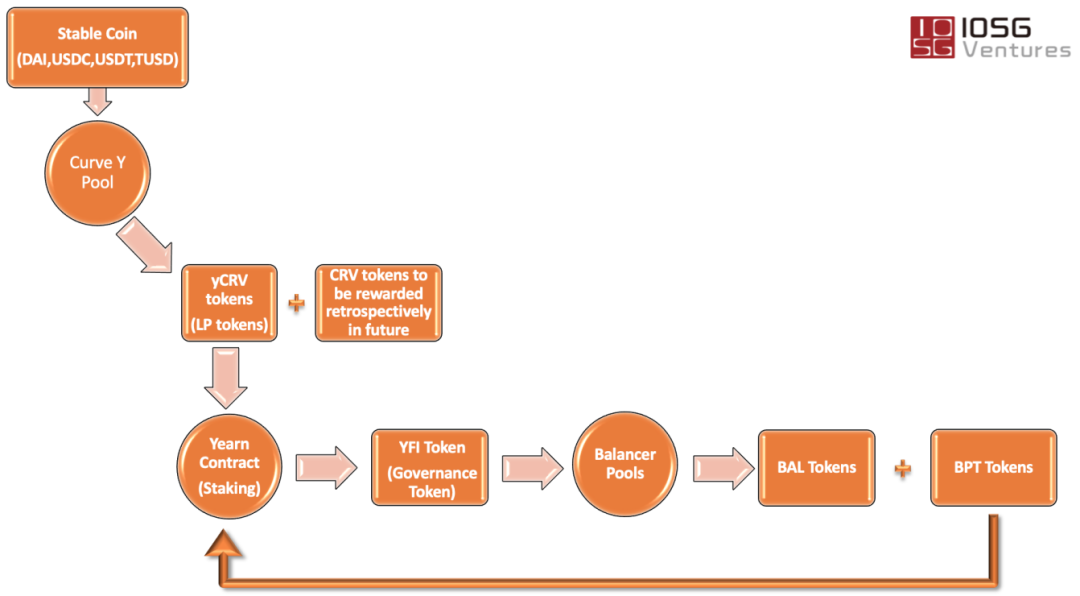

While more and more protocols are joining the liquidity mining craze, finding the most profitable opportunities is not easy. We believe that more projects will develop products similar to yield aggregators to help users enhance their yields. The following diagram shows how yearn interacts with multiple DeFi projects.

We can see that yearn effectively integrates many protocols in the DeFi space to maximize returns for liquidity providers and deeply bind the interests of products and users through governance tokens.

We expect to see more projects focused on yield optimization in the application layer of DeFi to attract traders who prioritize short-term interests.

Source: IOSG Ventures

Finally, the leap of approximately $1 billion in deposits within a month symbolizes that DeFi and the entire blockchain ecosystem are entering a period of heavy innovation. In the face of a global crisis, the significant growth of value built on blockchain may even persuade skeptics to reconsider implementing blockchain-driven innovation as part of the new normal.

The free lunch may last a long time, but it may not; however, what truly matters is that blockchain-driven technology and innovation continue to surprise us, bringing previously unlikely great use cases and application scenarios.

References

Babyt, (2020, June 23). Will Lending as Mining COMP Be the Next FCoin? Retrieved from Babyt: https://www.8btc.com/media/613150

ChainDD, (2020, July 22). Crazy DeFi: Developers Only One, Daily Surge of 40 Times. Retrieved from Sohu: https://www.sohu.com/a/408993344_100217347

Blockchain Network, (2020, June 26). "Lending as Mining" vs. "Trading as Mining." Retrieved from QKLW: https://www.qklw.com/specialcolumn/20200626/96144.html

Blue Fox Notes, (2020, July 27). YFI: The BTC in DeFi. Retrieved from Chainnews: https://www.chainnews.com/articles/919815546404.htm

Alberquilla, I. (2020, June 30). Are Compound DeFi Users Riskier Since COMP Rewards? Retrieved from Medium: https://medium.com/coinmonks/are-compound-defi-users-riskier-since-comp-rewards-885f0097407c

CHARLIE. (2020, July 17). What is YFI and How to Earn Them by Staking Your yTokens? Retrieved from Curve: https://guides.curve.fi/what-is-yfi-and-how-to-earn-them-by-staking-your-ytokens/

CoinMarketCap. (n.d.). CoinMarketCap. Retrieved from CoinMarketCap: https://coinmarketcap.com/

Cronje, A. (2020, July 17). Earning YFI curve.fi/y. Retrieved from Medium - iearn.finance: https://medium.com/iearn/earning-yfi-yxcurve-fi-53b5fd347f0f

Cronje, A. (2020, July 17). YFI. Retrieved from Medium - iearn.finance: https://medium.com/iearn/yfi-df84573db81

Dale, B. (2020, June 30). Compound Changes COMP Distribution Rules Following 'Yield Farming' Frenzy. Retrieved from CoinDesk: https://www.coindesk.com/compound-changes-comp-distribution-rules-following-yield-farming-frenzy

Dale, B. (2020, June 25). Some Numbers That Show Why Yield Farming COMP Is So Seductive. Retrieved from CoinDesk: https://www.coindesk.com/some-numbers-that-show-why-yield-farming-comp-is-so-seductive

Dale, B. (2020, June 23). Story from Tech Following COMP's Surge, DeFi Platform Balancer Begins Distribution of BAL Tokens. Retrieved from CoinDesk: https://www.coindesk.com/defi-platform-balancer-bal-token-distribution-compound-comp

Dale, B. (2020, July 06). What Is Yield Farming? The Rocket Fuel of DeFi, Explained. Retrieved from CoinDesk: https://www.coindesk.com/defi-yield-farming-comp-token-explained

Dao, C. (2020, June 1). Curve Dao Contracts. Retrieved from GitHub: https://github.com/curvefi/curve-dao-contracts/blob/master/doc/readme.pdf

Defiant, T. (2020, June 24). Top DeFi 'Yield Farmers' Share Their Secrets to a Profitable Harvest. Retrieved from Decrypt: https://decrypt.co/33279/top-defi-yield-farmers-share-their-secrets-to-a-profitable-harvest

Lau, D. (2020, July 25). Understanding YFI Core Highlights: Fair Distribution, Governance, and Value Capture. Retrieved from Chainnews: https://www.chainnews.com/articles/983977615143.htm

Leshner, R. (2020, Feb 27). Compound Governance. Retrieved from Medium: https://medium.com/compound-finance/compound-governance-5531f524cf68

Leshner, R. (2020, May 28). Expanding Compound Governance. Retrieved from Medium: https://medium.com/compound-finance/expanding-compound-governance-ce13fcd4fe36

Marias, C. P. (2019, November 1). Introducing Liquidity Mining. Retrieved from https://hummingbot.io/blog/2019-11-liquidity-mining/

Mengoulis, A. (2017, October 20). Would Someone Spend $18,000 to Win Your Contest? Jet Made it Happen. Retrieved from Viral Loops: https://viral-loops.com/blog/someone-spend-18000-win-contest-jet-made-happen/

PENG, T. (2020, Feb 18). Chinese Exchange FCoin Closes Down, Still Owes Users $125 Million. Retrieved from Cointelegraph: https://cointelegraph.com/news/chinese-exchange-fcoin-closes-down-still-owes-users-125-million

Pulse, D. (2019, September 3). Defi Pulse. Retrieved from What is DeFi?: https://defipulse.com/blog/what-is-defi/

Pulse, D. (2019, September 18). Zero to DeFi -- A Beginner's Guide to Earning Passive Income via Compound Finance. Retrieved from Defi Pulse: https://defipulse.com/blog/zero-to-defi-cdai/

Purdy, J. (2020). Real-World Liquidity Mining: Lessons Learned from Jet.com. New York: Messari.

Reed, E. (2020, June 1). Stock Market Bubbles: Definition and Examples. Retrieved from Smart Asset: https://smartasset.com/investing/stock-market-bubble

Risk warning

Risk warning Risk warning

Risk warning

Popular articles