Coinbase: DeFi locked value skyrockets 2500% in a year, regulatory issues still need attention

In the past quarter, both FinCEN and OCC have issued regulatory guidelines for crypto assets, but their attitudes are completely opposite.

In the past quarter, both FinCEN and OCC have issued regulatory guidelines for crypto assets, but their attitudes are completely opposite.This article is from the Babbit Information WeChat public account, authored by Overnight Porridge.

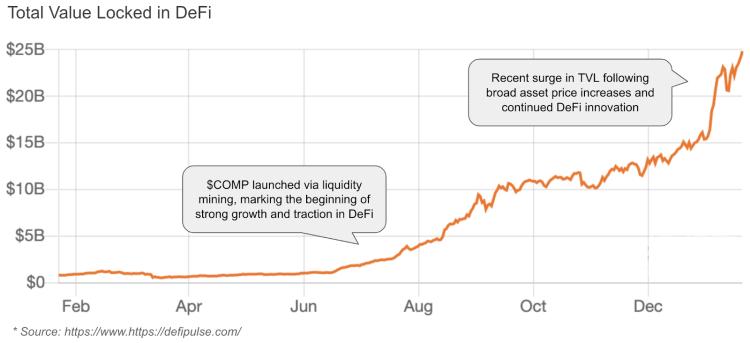

In the grand crypto bull market, DeFi continues to maintain a strong growth momentum. Since the summer of 2020, the total locked value (TVL) of DeFi projects has seen significant growth. We discussed the phenomenon of DeFi and yield farming in June 2020, but what has happened since then? In short, the rapid development of DeFi is still ongoing. As we pointed out last time, the phenomenon of yield farming continues to drive growth. This creates a virtuous cycle: yield farming mechanisms entice participants to increase capital → increase TVL → drive governance token valuations → expand yield farming incentives → continue this cycle.

Nevertheless, as part of the growth story, the true innovations in the DeFi space that have gone from 0 to 1 cannot be overlooked. These include synthetic assets (such as Synthetix, UMA, and Mirror), financial products that provide capital efficiency (such as Aave and Compound), open financial access (including flash loans and emerging remittance use cases), and composable protocols that layer DeFi projects, such as Yearn.

As of now, the total locked value of DeFi protocols has exceeded $25 billion, a year-on-year increase of 2500%, which is an incredible growth rate. Similarly, the number of DeFi users has surpassed 1.2 million (defined by the number of unique addresses accessing DeFi services). Mainstream DeFi protocols like Uniswap and Compound have between 200,000 and 500,000 users, while most other DeFi applications have user numbers ranging from 25,000 to 50,000.

Similarly, since July 2020, the trading volume of DEX has been experiencing strong growth. To date, the cumulative trading volume of DEX has surpassed that of most centralized exchanges, with all DEXs setting a record of over $10 billion in daily trading volume in January this year.

The trading volume is driven by the growth of DeFi, as well as factors such as the broader crypto bull market. This includes the acquisition of new long-tail DeFi tokens and effective exchanges between highly correlated assets (such as stablecoins).

However, today's DEX primarily settle trades on the Ethereum blockchain, which can be constrained by high gas prices during periods of high demand. The launch of Synthetix on Optimism (a rollup-based scaling solution) has sparked ongoing interest in scaling solutions, marking a significant milestone.

While looking at the main indicators is encouraging, the fact is that the pace of movement in DeFi is so fast that no one can accurately track it. Here are some interesting themes we have discovered:

DeFi projects are embracing composability: New DeFi projects either introduce new primitives or bundle existing primitives to create new products. We can think of these primitives as Lego blocks, six months ago, we were designing and building individual blocks. Today, we are combining these individual blocks into cars, planes, and castles.

DeFi projects are starting to band together: DeFi projects are grappling with key issues such as moats, defensiveness, and revenue growth. Most projects seem to include open community collaboration, believing that the community will create moats (you can't fork a community). This accurate vision initially led to governance tokens and yield farming phenomena, which have now evolved into creative partnerships and collaborations, most notably in Sushiswap's 2021 roadmap.

Scalability is becoming a bottleneck, but solutions are on the way: As the Ethereum base layer continues to scale, some protocols are publicly exploring integration with Layer 2 networks or other blockchains. Significant progress is expected in 2021, especially regarding Ethereum rollups.

Regulatory uncertainty affects development: Meanwhile, the SEC's lawsuit against Ripple and the CFTC's lawsuit against BitMEX indicate that regulators are closely monitoring crypto assets and are beginning to charge the largest participants in the space. We have reason to see regulators paying more attention to DeFi projects, and this uncertainty will continue to be influenced by regulatory jurisdictions.

Speaking of regulation…

Two Aspects of Regulation

In the past quarter, both FinCEN and OCC have issued regulatory guidelines for crypto assets, but their attitudes are completely opposite.

FinCEN is responsible for compliance with KYC/AML laws, which is particularly important for crypto exchanges like Coinbase ("VASP - Virtual Asset Service Provider"). Crypto asset exchanges need to verify their customers' identities (KYC) and use blockchain forensic tools to investigate crypto transactions to ensure that deposits do not come from potential illegal sources.

FINCEN recently proposed amendments to the FBAR regulations of the Bank Secrecy Act, specifically targeting crypto assets and VASPs. In summary, under the new amendment, U.S. citizens must report their holdings of crypto assets and transactions exceeding $10,000, regardless of where these crypto assets are held. In essence, the amendment will require U.S. individuals to report holdings of cryptocurrencies exceeding $10,000 in foreign accounts and require crypto exchanges or wallets to store customer information related to any transactions over $3,000 and report any transactions exceeding $10,000 to FINCEN.

Additionally, the announcement had a limited comment period of only 15 days during the U.S. holiday season, making it difficult for crypto service providers to respond.

Many crypto asset service providers (Coinbase, Fidelity, Square, CoinCenter, ErisX, etc.) have strongly opposed the proposed rules, emphasizing the rushed nature of the proposal and the lack of time.

Since then, the Treasury has extended the comment period, and with the new administration in place, the future remains uncertain.

The Office of the Comptroller of the Currency (OCC) is an independent agency of the Treasury tasked with helping to "charter, regulate, and supervise banks," and it has taken a different stance in its recent guidance:

Federal banks can operate public blockchain infrastructure [January 2021];

Federal banks can participate in stablecoin activities [September 2020];

Federal banks can custody crypto assets [July 2020];

With this series of positive guidance, it is clear that national banks can now participate in the crypto economy through custody and settlement. Notably, the guidance released in January 2021 legitimizes public blockchains as settlement infrastructure, effectively treating blockchains as equivalent to ACH or SWIFT.

In other words, federal banks can act as large validators on the blockchain (like miners), or more practically, banks may ultimately settle transactions using Bitcoin, Ethereum, or stablecoins.

Ultimately, this is the first step in the regulatory actions needed to connect the crypto economy with traditional financial infrastructure. It is also worth noting that while the OCC is a federal regulatory agency, it is not the only regulatory body. Additionally, adoption will take time - blockchain is still relatively new and lacks some core functionalities (such as privacy and scalability), but this is a promising development.

It is commendable that the U.S. Treasury subsequently extended the comment period, and this proposal may become stalled under the incoming Biden administration.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles