Reviewing Venus's coldest day, a $200 million liquidation revelation

What can we learn from this event?

What can we learn from this event?This article is an original piece by Chain Catcher, authored by Loners Liu.

Malicious Short Selling, Big Players Dumping?

In the early hours of May 19, Beijing time, the price of the token XVS from the lending protocol Venus on BSC began to experience a dramatic surge, rising from a low of $70 to a peak of $144 in less than a few hours. However, the price subsequently saw a massive decline, dropping to a low of $31, a decrease of 78% from its high.

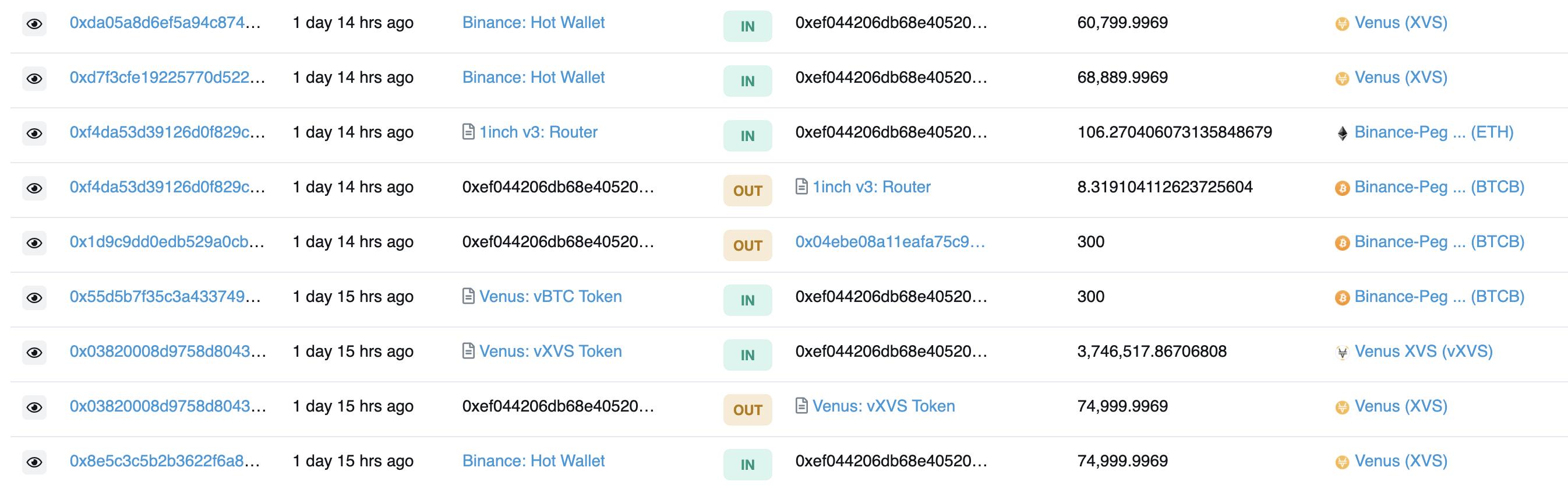

According to a community user-provided address for a large holder: 0xEF044206Db68E40520BfA82D45419d498b4bc7Bf, which is also the largest holding address for vXVS (the deposit certificate for XVS collateralized in Venus), it can be observed from the records of this address on BscScan that this address started purchasing XVS tokens in large quantities on-chain and on Binance at midnight on the 19th. Due to the insufficient liquidity of XVS in the market, the large volume of purchases in a short period led to a further increase in price.

Crypto KOL Wang Dayou stated on Weibo that this large holder collateralized nearly 2 million XVS at a high price (estimated around $140) and then borrowed 4,100 bitcoins and 9,600 ethers, amounting to an estimated debt of $200 million, which subsequently led to a chain liquidation.

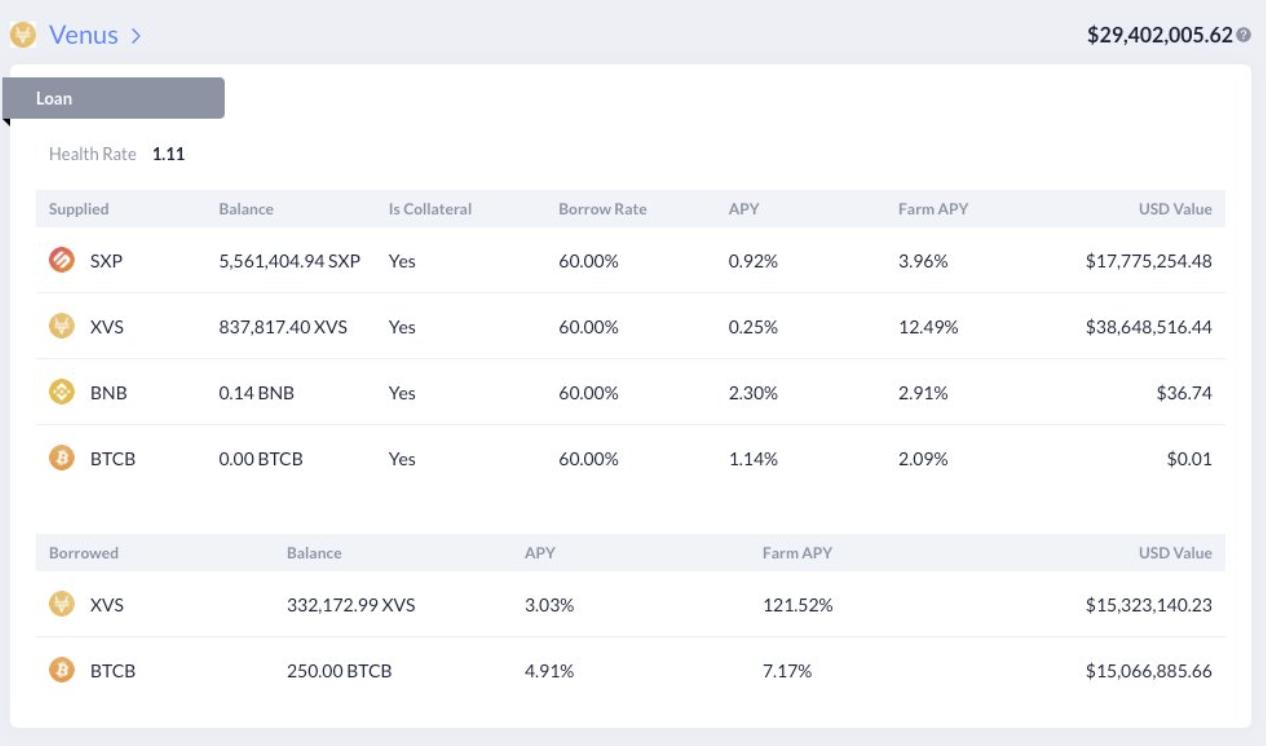

The main driving force behind this incident in the community is that the collateralization rate of XVS is 80%, a setting that comes from the recently passed VIP-22 proposal on May 8, which increased the borrowing factors for certain collateral assets, such as mainstream coins BTC, ETH, BNB, XVS, and its development team's token SXP, as well as stablecoins USDT, BUSD, and USDC. The proposal explained that this action was taken because these assets have sufficient liquidity, which can enhance the capital utilization of Venus and strengthen its competitive advantage.

Although increasing the collateralization rate can improve capital utilization, it also raises the risk of the Venus system, as an 80% collateralization rate means that a 14% drop in the collateralized asset could trigger system liquidation.

In DeFi lending systems, there is generally a concept of a health factor, which is usually related to the account's loan amount and collateral. It can be expressed as: Health Factor = ∑(Collateral * Liquidation Threshold) / (Loan Amount + Loan Interest)

When the health factor < 1, it will trigger the DeFi lending system to liquidate the collateral of that user's account. Liquidating individual users is to avoid systemic financial risks; therefore, borrowers will face penalties from the system, while liquidators will receive certain rewards. The recently passed VIP-19 proposal on May 3 even increased the incentive for liquidators from the original 10% to 15%, further encouraging liquidators to participate in this liquidation. Since the process of the collateralized asset XVS rising from $70 to $140 was a personal operation, the market did not have much consensus, which led to a sharp decline in the collateral's price during the liquidation process, resulting in a final bad debt of $100 million.

So, is it an oracle issue? Compound previously faced a liquidation of $90 million due to using a single DAI price from Coinbase, so Venus also changed its original price feed from Band to Chainlink in proposal 22. In this incident, both on-chain and on the exchange, the price indeed reached that level.

Not Just Once

The entire liquidation process lasted several hours. By observing the previous transaction records of this address, it can be found that as the first XVS holding address, it has been continuously supplying XVS, then borrowing XVS, and repeating this cycle until the borrowing limit was exhausted, with no risk of liquidation. According to the token economic model of the Venus platform, 79% of the total XVS token supply will be reserved for community mining, with 35% allocated to the lending pool, which is distributed to users who collateralize assets and earn interest, and another 35% allocated to the lending pool, which is distributed to users who lend assets and pay interest. Due to the borrowing limit on XVS, most of the XVS was borrowed by this large holder, while enjoying an annualized return of 121%.

In the latest proposal, the official reduced the output of XVS and instead used a portion of VRT as incentives, which was officially passed on May 16. This was also mentioned in the 2021 roadmap. It may be that this large holder is not optimistic about the future market and wants to quickly offload their assets, but due to the significant depth difference in XVS, large-scale selling could easily lead to asset depreciation. However, because of the depth difference, they chose to raise the price in a short time to achieve a successful strike.

Such tactics remind one of a cross-chain asset protocol Canno token on the Binance Smart Chain that was publicly sold on Swipe Wallet (the development team behind Venus) in January this year. Subsequently, Venus officially tweeted that it would launch and support the CAN token. After that, the price of CAN was raised to $0.35 on DEX, and due to the lack of liquidity, it only took a few dozen ETH.

Then, 448 million CAN flowed into the Venus platform, collateralized at a price of $0.35 (totaling $157 million), borrowing 3,000 bitcoins and 7,000 ETH, along with other assets, leading to approximately $100 million in bad debt for Venus.

What Can We Learn from This Incident?

Once again, due to collateralizing assets with insufficient liquidity and raising the collateral price to borrow at a high point, it seems that the project parties have not learned anything from such incidents.

First is the choice of collateral. In traditional financial markets, bank presidents and boards have sufficient power to choose the types of collateral assets. This is precisely why regulatory bodies exist. After the famous Anbang Group acquired Chengdu Rural Commercial Bank and entered the board, it began to have the bank sell its own insurance, then deposit the premiums back into its own bank. Under such nested structures, a financial empire of 20 trillion was completed, and of course, we all know the final outcome: mismatched terms led to a liquidity crisis, and what begins this way must end this way.

If a project party can freely choose a certain collateral, then the decentralized world becomes a paradise for wrongdoers, as there is no regulation here, and they can even engage in self-dealing. To some extent, project parties and large holders have become another center. As a community governance project, it should hand over the choice of collateral to the community after the project matures, while also establishing mechanisms to prevent large holders from engaging in wrongdoing.

For different collateral types, reasonable deposit and borrowing limits should be designed. For collateral with depth differences, when borrowing tokens with strong liquidity, the collateral coefficient needs to be reduced accordingly.

Secondly, while a high collateralization rate can bring higher capital efficiency, it is essential to fully consider the price volatility of the collateral and market trading volume. After completing the VRT snapshot, the price of XVS dropped by 30% in a short time. In comparison, well-known lending protocols on Ethereum, such as Aave and Compound, have maintained their collateralization rates around 60%, not to mention that both have sufficiently dispersed token circulation and market depth far greater than XVS.

Moreover, in liquidation, various possible situations should be considered. For example, the lending protocol Liquity, although the collateralization rate is 110% (generally 150%), implements a liquidation process based on a stablecoin pool. This mechanism provides a natural way: if a loan's collateral value drops below the minimum collateralization rate, the collateral can be directly handed over to the acquirer, allowing the system to use their presence to stabilize the funds in the pool and recover the debt from the borrower. In this way, any surplus collateral or excess collateral becomes the profit for the acquirer or the loss for the borrower.

At the same time, during the price feeding process of oracles, whether more dimensional indicators can support, such as trading depth and trading volume, rather than just providing prices. The core factors determining the stability and robustness of oracle node pricing are: the depth of CEX market and participant structure, as well as the capital utilization efficiency of DEX. The deeper the CEX market and the richer the participant structure, the more representative the obtained prices will be, making wrongdoing and manipulation more difficult. Conversely, when CEX market depth is insufficient, it will also face issues such as exchange wrongdoing and market manipulation.

Additionally, for collateral with poor depth, lending platforms should also consider the time factor. For instance, MakerDAO, to prevent attacks during the price feeding process, the MakerDAO Oracle Security Module (OSM) delays the release of new reference prices by one hour. Of course, in a rapidly declining market, faster oracle pricing can significantly reduce the risk of bad debts.

In summary, DeFi is still a very emerging industry. Every risk attack it undergoes lays the groundwork for larger capital amounts in the future. Learning lessons from each incident and applying them to the next version enhances the overall security of the DeFi world and prevents systemic risks. This is the main wealth that this incident leaves us with.

Risk warning

Risk warning Risk warning

Risk warning