How do cryptocurrencies reconstruct the internet-native economy?

How creators and communities utilize cryptocurrency tokens to design internet-native economies.

How creators and communities utilize cryptocurrency tokens to design internet-native economies.The author of this article is Patrick Rivera, a software engineer at Mirror.xyz, and it has been translated by Wang Dashu and Gu Yu.

The internet-native economy based on cryptocurrency tokens is becoming the focus of attention for more and more crypto protocols, communities, and creators.

Recently, Patrick Rivera, a software engineer at the Ethereum-based content crowdfunding platform Mirror.xyz, wrote about how creators and communities can leverage cryptocurrency tokens to design internet-native economies. He elaborated on how NFTs can play their role from perspectives such as identity and belonging, status, personal significance, relationships, collectibles, and superpowers, making it a valuable read.

An important and frequently discussed idea in the cryptocurrency space is to help creators and communities establish their own internet-native economies. A key component of these economies is tokens, which gained a bad reputation during the ICO craze a few years ago but have always been a fundamental unit of value in the crypto economy. They serve as a mechanism to incentivize participants in decentralized networks (users, developers, investors, and service providers) and are considered a breakthrough in the design of decentralized networks.

On a simple level, tokens are just code that exists on a global peer-to-peer network called the blockchain. Unlike other forms of currency, they are digitally native and programmable, protected by crypto wallets and private keys.

Tokens fall into two main categories: fungible and non-fungible. As more and more creators and communities establish their own crypto economies, fungible tokens will be used for exchanging goods, storing value, and making collective decisions; non-fungible tokens (NFTs) will be used to create new business models centered around collectibles, rewards, achievements, etc. — granting people identity, status, and a sense of belonging.

All the best crypto protocols, social applications, online communities, and marketplaces need to deeply understand the interaction between fungible and non-fungible tokens to create their own internet economies. Why do we need internet-native economies?

Most traditional economies are designed without considering the internet. As a result, modern economies face many issues:

1) Limited access. Globally, about 1.7 billion adults do not have bank accounts. This limits people's ability to start businesses, fund projects, and take entrepreneurial risks.

2) Inefficiency. High fees for credit card transactions and remittances, along with high-interest loans, make it difficult for low-income communities to participate in the economy.

3) Low transparency. Banks operate under complex structures, making it hard for outsiders to understand their financial health and risks. Citizens are downgraded to believing that the government will maintain economic value through monetary policy, capital controls, and FDIC insurance, but we have seen that this approach does not always work.

These limitations reduce economic growth and widen inequality. As more economic activities move online, we need internet-native tools to build a productive economy. Many people do not have bank accounts but do have a smartphone with internet access. This is where crypto networks come into play. They provide the cryptography (security without third parties) and economic building blocks for modern forms of production, distribution, trade, and consumption.

1. Two Forms of Fungible Tokens

Traditionally, money has three main purposes: a medium of exchange to facilitate trade; a store of value to preserve wealth over a specific period; and a unit of account for measuring value.

Economies invest funds in productive assets such as factories, scientific research, technology development, and public infrastructure to drive economic growth. To enhance enjoyment, consumers also purchase relatively "non-productive" goods, such as flat-screen TVs and high-end wallets or sneakers.

The crypto economy follows a similar dynamic. Currency circulates through issuance policies and is reinvested along a spectrum of productive and non-productive assets. For example, the code that runs the Bitcoin network is programmed to issue 21 million bitcoins, rewarding miners who protect the network and allowing bitcoins to be transferred directly among parties for various scenarios.

On the Ethereum network, tokens are primarily issued through the fungible ERC20 standard; goods are mainly issued through the non-fungible ERC721 standard, and tokens issued under the ERC721 standard are commonly referred to as NFTs.

In addition to being a form of internet-native tokens, the programmable nature of ERC20 tokens also supports two other use cases: utility and governance. As we delve deeper into the classification of tokens, we can see these use cases more clearly.

1) Utility Tokens

Utility tokens are fungible tokens that unlock functionalities within smart contracts or off-chain systems (like Discord communities). Utility tokens are difficult to execute off-chain, so they are often most valuable when their functionalities are fully executed on-chain through smart contracts.

When designing a utility token system, it is necessary to consider the following questions: What core problem are we trying to solve? For whom are we solving it? How do we help them solve it in a positive way?

Some use cases for utility tokens, along with the resulting crypto economy, include automated and trust-minimized lending.

In the past, executing trading strategies (like short selling and leveraging) in a decentralized/trust-minimized manner was impossible because traditional exchanges required a centralized counterparty to assume credit risk and provide services like clearing and settlement.

To achieve decentralized lending on a blockchain like Ethereum, protocols require traders to deposit tokens into smart contracts as collateral to unlock lending capabilities. Tokens used as collateral for decentralized loans are a case of utility tokens because they unlock automated functionalities within smart contracts.

Compound is a case of a lending protocol built on Ethereum. To obtain a loan, users must first deposit one of the approved collateral tokens that have been passed through governance voting. Currently, the protocol supports tokens like ETH, DAI, USDC, BAT, and UNI. By depositing collateral, borrowers can unlock lending capabilities.

Traders use Compound to take leveraged long positions on ETH. For example, they might deposit ETH as collateral, borrow stablecoins like USDC or DAI, and purchase more ETH. You can do something similar for short positions. If loan interest is not paid on time or the value of the underlying collateral drops to a certain extent, automated bots known as Keepers will incentivize the liquidation of positions by taking a cut of the transaction fees.

2) Governance Tokens

Governance tokens represent a percentage ownership of voting rights. Most community members find it difficult to keep up with the latest developments of specific protocols, so most protocols allow token holders to delegate their votes to trusted representatives.

When designing a governance token system, it is necessary to consider the following questions: What public goods should our community manage? How should governance tokens be issued? How do we design a fair, flexible, and transparent governance system?

Next, using parameter settings and upgrades as examples, let’s review some cases of governance tokens.

Crypto networks are supported by smart contracts that execute logic responsible for calculating interest rates in lending protocols, implementing automated issuance policies for stablecoins, or determining exchange rates for token trades.

When a smart contract is first deployed to the Ethereum network, it may contain multiple admin privileges to limit vulnerability risks. Once the smart contract has been sufficiently tested in production, admin privileges are typically removed to ensure that the core team cannot arbitrarily update the protocol.

However, many times protocols still require upgrades and improvements. In Uniswap, UNI holders can vote to initiate proposals for protocol fees, redirecting 0.05% of transaction fees to UNI holders instead of LPs. In Compound, COMP token holders can vote on the collateral ratios for new tokens.

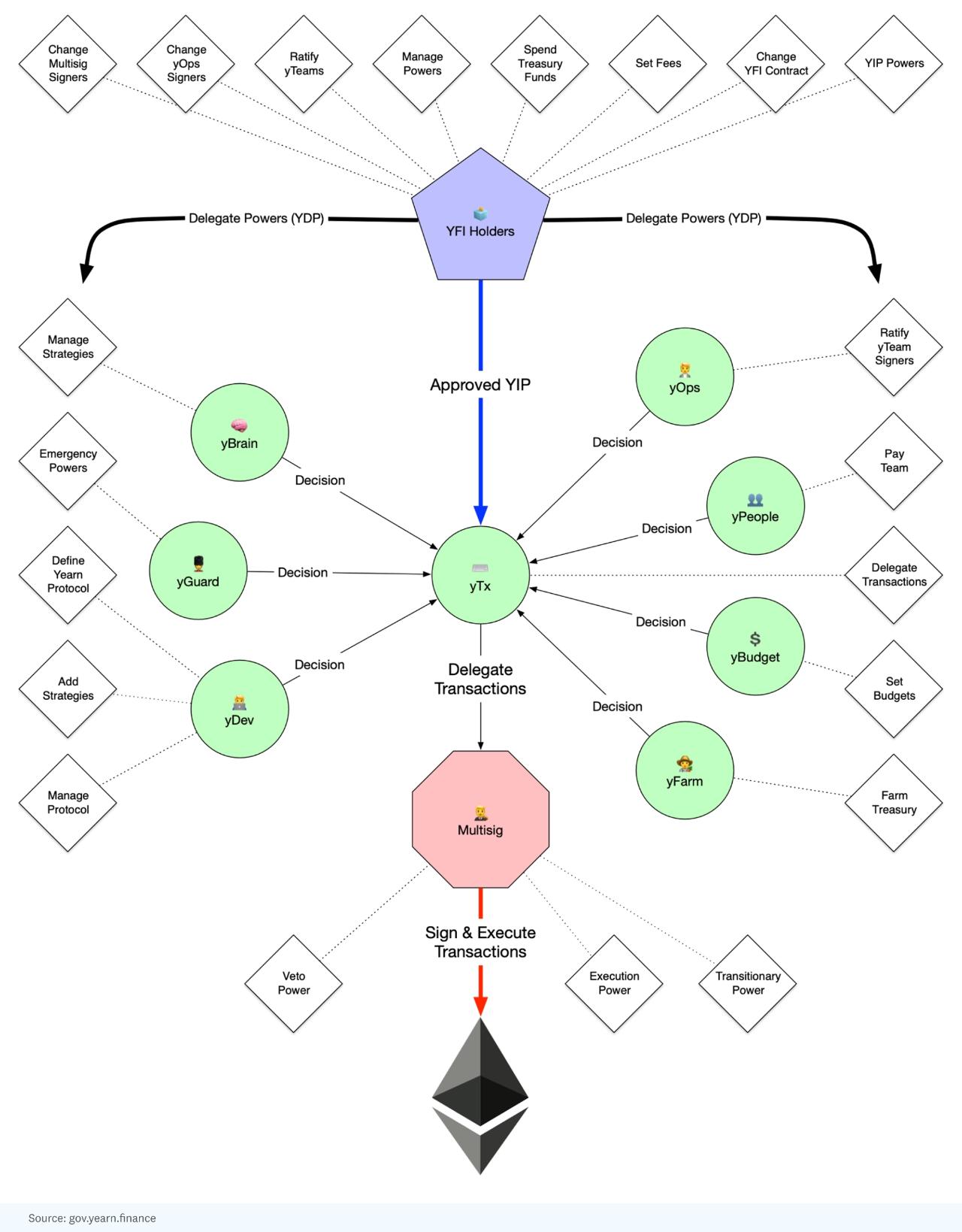

Recently, the YFI community proposed a cutting-edge decentralized governance system, with the latest proposal suggesting that YFI holders elect committees for specific areas such as budget control, development roadmap, and investment strategy.

As all the above examples show, fungible tokens are excellent tools for exchanging goods, storing value, and coordinating online communities. Economies, companies, and protocols need business models to fund their growth. Additionally, people need tools to build relationships and feel a sense of purpose, which is where NFTs come into play.

2. Non-Fungible Tokens (NFTs)

NFTs are unique digital tokens stored on the blockchain. We have seen a lot of activity and excitement in this space, but to focus on the bigger picture, there are six main reasons people value virtual goods: identity and belonging, status, personal significance, relationships, collectibles, and superpowers.

Let’s take a closer look at how each of these applies to NFTs in the crypto economy.

1) Identity and Belonging

A sense of identity and belonging is cultivated through a shared history and a sense of storytelling. Religious communities are masters at creating a sense of identity and belonging.

CryptoPunks are quasi-religious icons in the crypto community. By owning a CryptoPunk, you indicate your willingness to hold this artifact and be part of the CryptoPunk community, as well as your unwillingness to sell it at a high price. HODLers signal their identity by changing their profile pictures to their CryptoPunk. Some even delete their CryptoPunk profile pictures after selling them to signify a loss of identity.

2) Status

Status is driven by price and scarcity. Whether it’s a Louis Vuitton bag or a Lamborghini, status signals are a core part of human nature. On social media, status often comes from follower counts and engagement metrics like likes, shares, and retweets.

These metrics are essentially just virtual currencies that exist in company databases. But they are inefficient because it’s hard to convert likes and followers into cash. Therefore, business-savvy creators use social media as a potential customer base for their actual businesses, such as brand e-commerce, merchandise drops, courses, etc.

But what if you could directly exchange likes for money?

I believe that crypto-native social applications will create a new form of "non-fungible likes," akin to badges and in-game items in video games. For example, Snap's Spotlight program pays creators for popular content. But this is an opaque process.

In contrast, crypto-native social applications could allow consumers to vote on their favorite content, rewarding the highest-voted creators with NFTs and allowing these NFTs to redeem a percentage of a prize pool. The process would be community-driven and independently verifiable, as it would be completed on-chain through crypto tokens and smart contracts.

Today, top creators receive inefficient virtual currencies (like likes/followers) and cash rewards from centralized platforms. In the future, creators will establish a new form of identity through these community-driven NFTs, which they own through their private keys and can directly exchange for money.

3) Personal Significance

Personal significance is driven by emotional value and customization. Many people have a baby toy, trophy, or ring that holds special meaning because of the story behind it. The fasting app Zero rewards users with badges for certain milestones, such as a 24-hour fast or five consecutive days of intermittent fasting.

Similarly, crypto protocols can issue NFTs to commemorate milestones and achievements based on on-chain activity. For example, Rabbithole collaborates with leading DeFi protocols to create tasks that people can complete to receive special NFTs or protocol tokens. This provides a fun way for people to engage with the crypto industry by completing on-chain tasks for special NFTs.

Another example is Uniswap's v3 protocol. Whenever a liquidity provider (LP) deposits into a pool, the protocol transfers an automatically generated NFT to the LP based on various factors, such as which pool they deposited into and the range on the liquidity curve.

4) Relationships

In Japan, businesspeople exchange gifts to build trust and show respect. On Twitch, viewers send tips and purchase gifts to indicate their affinity, hoping to create a buzz. In the crypto economy, tipping and gifting may become core primitives for building online relationships.

Web 2.0 is about socializing — following, liking, commenting. Web 3.0 is about socializing + economic graphs — the NFTs you purchase, the projects you invest in, the social tokens you earn. Company profiles on Crunchbase are early examples of economic graphs. For most startups, you can see who funded them, how much they received, and when the funding rounds occurred.

Since all transactions on crypto networks settle on-chain, we will be able to build rich economic relationships into social applications, online communities, and marketplaces. We will provide a crypto-native version of Crunchbase for creators, communities, and various creative projects. At Mirror, we showcase these economic relationships of tokenized crowdfunding that support creative projects like novels, newsletters, and creator residencies.

While there is certainly a risk of over-financializing relationships, many people have talked about the close connections that develop through these economic graphs.

Another way NFTs enable new types of relationships is through peer credentials. Today, the main sources of certification come from university degrees, companies you've worked for, social media influence, and letters of recommendation. These are inefficient forms of certification: they are either not very specific or require a lot of time and effort to clarify (in the case of references).

But what if you could send a "top backend engineer" NFT to the best backend engineer you've ever collaborated with? Or a "very helpful venture capitalist" NFT for a board member? The benefit of these badges as NFTs is that you can prove they come from specific individuals and that they are scarce (for example, you only distributed three of them). I would prefer to hire someone based on the recommendation of someone I respect rather than a fancy degree.

I believe that NFTs like these will enable new types of relationship graphs that we can use to build better recommendation systems for job postings, content, dating apps, and more.

5) Collectibles

Whether it’s Beanie Babies or Pokémon cards, collecting taps into our innate desire for status and competition. For crypto projects, the key is to make collectible collections clearer and more readable. NBA Top Shot achieves this through their Showcase feature. They provide simple tools for creating collections and displaying them on your profile page:

One idea we are excited about at Mirror is the "digital bookshelf." What if you could collect content not by liking it but by purchasing it at different price/rarity levels (like gold, silver, bronze) and then display your collection on your public profile? NFTs allow creators to offer digital goods at different prices, and as Chris Dixon mentioned in his article "NFTs and a Thousand True Fans," this can lead to better monetization over time.

In addition to helping creators improve their monetization methods (which many have already discussed), I believe NFT collectibles will also usher in a curator economy.

What if Spotify audiences voted on playlists, and top curators received a mix of cash and Spotify stock? What if Pinterest compensated top users in the same way it does top engineers?

As more digital media defaults to NFTs, I believe that curators of top songs, videos, newsletters, podcasts, etc., will be able to package their NFT collections and earn royalties based on licensing and engagement. A brand-new curator economy will emerge.

6) Superpowers

Long ago, in a distant metaverse, the gaming industry realized that one of the most effective monetization methods was to grant users "superpowers." These included the ability to skip levels and gain advantages to win matches faster.

Dating apps have consistently been among the highest-grossing apps in the world, following a similar approach. The superpowers of dating apps include more swipes and higher visibility, leading to more matches.

LinkedIn also follows this approach, offering more searches and advanced analytics to premium subscribers, enabling them to find jobs or hire suitable candidates faster.

In crypto, NFTs can grant premium users special abilities, such as serving as arbitrators in popular communities. So why make it an NFT? The benefit is that NFT owners cannot be pulled by centralized entities. Instead, smart contracts will execute terms based on independently verifiable logic.

Depending on the governance mechanism, the community can decide who becomes an arbitrator, what privileges they have, and what constitutes a reasonable removal reason. The community decides who gets "superpowers" and who does not, rather than a centralized entity.

3. Conclusion

In summary, crypto networks support secure, transparent, internet-native economies. The fundamental unit of value in these economies is tokens. Fungible tokens can be used for currency, utility, and governance. Meanwhile, non-fungible tokens are digital assets that enable new business models and can grant people identity, status, and a sense of belonging.

There are still challenges to realizing a crypto economy everywhere, such as high transaction fees and cumbersome usage barriers, but over the past decade, crypto has transformed from a fringe activity into something that more institutions, technologists, and entrepreneurs are beginning to take seriously.

In the past decade, we have seen cryptocurrencies, crypto finance (DeFi), and crypto art. Soon, we may have crypto social networks, crypto commerce, crypto companies, and more.

When considering how to design a crypto economy, I often think of this quote from Ethereum co-founder Vitalik Buterin: "For me, the goal of crypto is never to eliminate the need for all trust. Rather, the goal of crypto is to give people access to cryptographic and economic building blocks, allowing them more choices about whom to trust."

The next decade will be about using these economic and crypto building blocks to design a new generation of transparent and fair internet-native economies.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles