BIS Report: Why is the Complete Decentralization of DeFi Considered an Illusion?

DeFi still has vulnerabilities.

DeFi still has vulnerabilities.Source: Bank for International Settlements Official Website

Authors: Wenqian Huang, Andreas Schrimpf

Compiled by: Nianqing, Chain Catcher

Editor's Note: Recently, the Bank for International Settlements published a report titled "DeFi Risks and the Decentralization Illusion," which discusses the decentralized attributes of DeFi in detail.

The article argues that there is a "decentralization illusion" in DeFi, as the need for governance makes a certain degree of centralization inevitable, and the structural aspects of the system lead to power concentration. If DeFi becomes widespread, its vulnerabilities could undermine financial stability. These issues could be severe due to high leverage, liquidity mismatches, inherent interconnections, and the lack of buffers like banks.

Particularly in light of recent frequent security incidents in DeFi and ongoing doubts about DAO governance, the decentralization issue in DeFi has garnered significant attention in the industry, with discussions about whether to pursue complete decentralization and whether it can be achieved.

In fact, Andre Cronje, the founder of the well-known DeFi project YFI, also tweeted that it is time to retire the term "decentralized finance (DeFi)," stating, "We are not decentralized, and conservatives will continue to try to use this concept as their 'attack' vehicle. 'Open finance' or 'web3 finance' may be the most accurate."

Below is a partial compilation of the article by Chain Catcher:

The "Decentralization Illusion" in DeFi

DeFi claims to be decentralized. So do the blockchain and its supported applications, which are designed to operate autonomously, meaning that even if the algorithm's results are incorrect, they cannot be changed.

However, the idea that DeFi can be completely decentralized is merely an illusion. A key principle of economic analysis is that firms cannot design contracts that cover all possible events, such as interactions between firms and employees or suppliers. Centralization allows companies to handle such "contract incompleteness" events. In DeFi, a similar concept is "algorithmic incompleteness," making it impossible to write code that comprehensively covers all unforeseen circumstances.

The principle of contract incompleteness has significant practical implications. All DeFi platforms have centralized governance frameworks that outline how to set strategies and operational priorities, especially concerning new business lines. Therefore, all DeFi platforms have a centralized element, typically revolving around the holders of "governance tokens" (often platform developers), which is not much different from company shareholders.

This centralization element can serve as a basis for viewing DeFi platforms as akin to corporate legal entities. Although the legal framework is still in its early stages, since mid-2021, decentralized autonomous organizations (DAOs) managing many DeFi applications have been permitted to register as limited liability companies in Wyoming, USA.

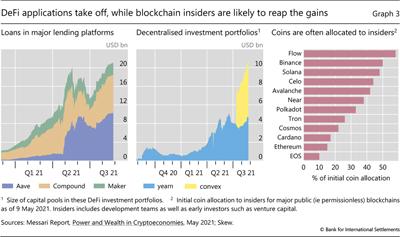

Moreover, some characteristics of DeFi have led to major holders having significant influence. For instance, miners need to receive certain rewards to package transactions, ensuring that there is no fraud in the transactions. Blockchains based on proof-of-stake mechanisms aim to enhance scalability, allowing miners to stake tokens to the block network for a chance to win the next block and receive rewards. Since the related operational costs are mostly fixed, this setup naturally leads to centralization. Many blockchains also allocate a large share of their initial tokens to insiders, exacerbating the centralization issue (as shown in the chart on the far right of the figure below).

Figure 1

Centralization can lead to collusion and limit the vitality of the blockchain. This increases the risk that a small number of miners can gain enough power to alter the blockchain for financial gain. Additionally, large holders may clog the blockchain with "wash trades" between their own wallets, significantly increasing transaction fees. Another concern is that miners can run large orders in advance to gain higher trading profits. Although similar preemptive actions occur in traditional finance, regulators have corresponding penalties. These rent-seeking behaviors detrimental to investors could undermine the future appeal of DeFi.

Despite discussions about changes to governance protocols, particularly regarding controlling collusion, such changes do not fundamentally alter some of the centralized flaws in DeFi.

Vulnerabilities and Spillover Channels

Although DeFi is still in its early stages, the services it offers are similar to those provided by traditional finance and exhibit common vulnerabilities. The fundamental mechanisms leading to these vulnerabilities—leverage, liquidity mismatches, and the interplay of profit-seeking activities and risk management practices—are well-known in the existing financial system. However, some characteristics of DeFi may exacerbate instability. In this section, we first focus on the role of leverage and operational risks in stablecoins due to liquidity mismatches, and then discuss spillover channels from traditional intermediaries.

Leverage

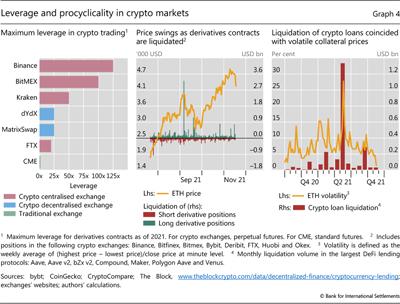

DeFi is characterized by the ability to obtain high leverage from lending and trading platforms. While loans are often over-collateralized, in one scenario, borrowed funds can be reused as collateral in other trades, allowing investors to build increasingly large risk exposures for a given amount of collateral. Trading derivatives on DEXs also involves leverage, as agreed payments occur in the future. In the established financial system, the maximum allowable margin expressed in indices is higher than that of regulated exchanges (as shown in the left chart of Figure 2). Unregulated crypto CEXs allow for higher leverage.

The high leverage in the crypto market exacerbates procyclicality. Leverage allows for the purchase of more assets with a certain amount of initial capital. However, when debt ultimately needs to be reduced (e.g., due to investment losses or collateral depreciation), investors are forced to sell assets, putting further downward pressure on prices. This procyclicality can be amplified by typical trading behaviors in the early stages of market development—such as the significant role of momentum trading, which exacerbates price volatility. Additionally, since the stability of the system depends on its weakest link, the inherent interconnectivity between DeFi applications can also amplify disasters.

DeFi's financial intermediaries rely entirely on private support, namely collateral, to reduce risk and facilitate decentralized trading. Therefore, there are no buffers in DeFi that can intervene during periods of stress. In contrast, in traditional finance, banks serve as resilient nodes that can expand their balance sheets (by issuing bank deposits, a widely accepted medium of exchange) through lending or purchasing distressed assets. The resilience of banks depends on their access to the central bank's balance sheet.

Figure 2

During the crypto market crash in September 2021, the instability of leverage became increasingly apparent. The forced liquidation of derivative positions and loans on DeFi platforms coincided with price plummets and surging volatility (as shown in the middle and right charts of Figure 1).

Liquidity Mismatches and Operational Risks of Stablecoins

Stablecoins are inherently fragile, intended to anchor a fixed face value through various types of reserve assets, but this design leads to a mismatch in the risk profiles of these assets (underlying collateral) and stablecoin liabilities. This fragility is similar to that of traditional intermediaries, such as funds, where investors expect to redeem cash at face value. However, stablecoins, contrary to their name, cannot serve as a substitute for cash due to the lack of a "no-questions-asked" status.

The fragility of stablecoins is determined by their design. Tokens backed by illiquid short-term securities (such as commercial paper) exhibit liquidity mismatches. Furthermore, companies backed by unstable collateral (such as crypto assets) face market risks, as asset prices can quickly drop below the stablecoin's face value. Although over-collateralization can offset such risks, it may be depleted when volatility surges.

Liquidity mismatches and market risks increase the likelihood of investor runs. The viability of stablecoins depends on investors' trust in the value of the assets, but transparency and lack of regulation can easily erode this trust. If investors do not trust these assets, they will quickly redeem stablecoins for fiat currency. In turn, this first-mover advantage can trigger a run, leading to the liquidation of collateral. Moreover, the evaporation of trust in stablecoins could have widespread implications for DeFi. Cross-investor and cross-platform transfers can become very cumbersome and costly, directly impacting the "liquidity" that is a key feature of DeFi.

Connections to the Traditional Financial System

Although DeFi and the traditional financial system are currently separate, the increasing connections between the two in the future, especially regarding bank assets, liabilities, and the activities of non-bank institutions in both systems, will lead to spillover effects.

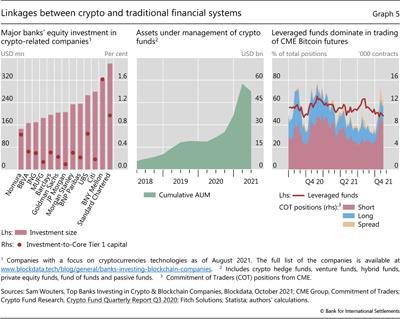

Overall, conservative regulatory actions currently limit banks' participation in the crypto ecosystem. In terms of assets, banks have limited risk exposure in loans and equity investments. By the end of 2021, large banks' equity investments in crypto-related companies ranged from $150 million to $380 million, accounting for only a small portion of their capital (as shown in the left chart of Figure 3). On the liability side, some banks may hold certificates of deposit or commercial paper due to stablecoins, allowing them to obtain funding from DeFi. Therefore, a run on stablecoins could create funding shocks for banks, similar to the familiar implications of a run on money market funds.

Additionally, traditional non-bank investors are increasingly interested in DeFi and the broader crypto market. Currently, these investors mainly include family offices and hedge funds, which generally obtain credit from major dealers through wholesale brokerage. Some valuable crypto funds (including those focused solely on DeFi and diversified funds) have seen their assets grow from $5 billion in 2018 to $50 billion in 2021 (as shown in the middle chart of Figure 3).

As an emerging asset class, more and more people are beginning to participate in crypto trading, with leveraged investors (including hedge funds) now being the main participants in Bitcoin futures trading on the Chicago Mercantile Exchange (as shown in the far right of the figure below). In the future, there may be more intermediaries and infrastructure that engage in business in the crypto market (including DeFi) while participating in traditional finance. This could strengthen the connections between traditional systems and crypto systems. The recent popularity of Bitcoin futures-based ETFs is a signal of the market's rise.

Figure 3

Related Policy Considerations and Conclusions

The DeFi ecosystem is still rapidly evolving and improving. Currently, it is mainly applicable to speculation, investment, and arbitrage of crypto assets, rather than use cases in the real economy. The limited application of anti-money laundering and know-your-customer (AML/KYC) provisions, combined with transaction anonymity, exposes DeFi to illegal activities and market manipulation. Overall, the fundamental task of DeFi—reducing the commissions of centralized intermediaries—seems yet to be achieved.

History shows that the future of new technologies is limitless, but their early development is often accompanied by bubbles and market imperfections. With improvements in blockchain scalability, large-scale tokenization of traditional assets, and most importantly, security guarantees and appropriate regulation that can enhance trust, DeFi can still play an important role in the financial system.

The growth of DeFi has raised concerns about financial stability. One concern is leverage-driven procyclicality, stemming from changes in collateral values and related margin fluctuations. As collateral prices fall, profit margins increase during crises, leading to frequent downward price spirals that can spill over into other parts of the financial system. Of course, due to the independence of the DeFi ecosystem, so far, rapid deleveraging events have not affected markets outside the crypto world.

Another concern points more directly to one of the main building blocks of DeFi: stablecoins. If risks are not well managed, stablecoins can easily experience runs, undermining users' ability to transfer funds within the DeFi ecosystem. Furthermore, once stablecoins sell reserve assets, it could create funding shocks for companies and banks, potentially impacting the broader financial system and economy. These risks are exacerbated by users viewing stablecoins as a medium of exchange, even though they are neither central bank money nor commercial bank money.

Since the main challenges facing DeFi are similar to those in traditional finance, existing regulatory principles can serve as guidelines. The fundamental principle of "same risk, same rules" should apply equally in the crypto market, especially regarding regulatory arbitrage. From a systemic perspective, policy measures should guide DeFi participants to internalize the costs generated by leverage procyclicality. To address the operational risks of stablecoins and their broader potential impacts, policymakers can draw on banking regulatory rules, current securities regulations aimed at strengthening the prudent framework for investment funds, and international risk management standards for payment infrastructure. Similarly, in focusing on market integrity and illegal financial activities, relevant agencies should expand their scope to cover DeFi.

The decentralized nature of DeFi inevitably raises the question of "how to implement policies." We believe that complete decentralization in DeFi is an illusion. In fact, there is a group of stakeholders within the DeFi ecosystem that is already attempting to make decisions and manage to maintain their ownership interests. The governance protocols relied upon by this group should become a necessary reference point for regulatory decision-makers to curb some of the issues arising from DeFi. Thus, regulatory safeguards will not only ensure the innovative potential of DeFi but will also benefit the entire financial market.

Related Recommendations:

"New York Times Commentary: When DeFi Incidents Are Frequent, Does 'Code Is Law' Still Hold?"

Risk warning

Risk warning Risk warning

Risk warning