Where does the value of ETH come from? A comprehensive analysis from asset logic to business strategy

The path of ETH value flow: from "maximizing fees" to "maximizing value delivery."

The path of ETH value flow: from "maximizing fees" to "maximizing value delivery."*Authors: Konstantin Lomashuk, Artem Kotelskiy, *XiaMiPP(Odaily)**

Editor's note: Recently, U.S. publicly listed companies have begun to "reassess" Ethereum. SharpLink Gaming plans to invest up to $1 billion in purchasing ETH as a strategic reserve through stock sales; BTCS has also purchased 3,450 ETH for approximately $8.42 million. These movements may be sending a clear signal: ETH is transitioning from "on-chain fuel" to "enterprise-level strategic asset."

From a developer community experimental platform to the infrastructure of DeFi, and now to long-term allocation in corporate finance, Ethereum's role is undergoing profound changes. In this wave of value reassessment, how should we understand the technological logic and economic model behind ETH?

Odaily Planet Daily has translated and refined a deep article co-authored by early Ethereum investor and Lido co-founder Konstantin Lomashuk and Cyber•Fund research director, Princeton mathematics PhD Artem Kotelskiy, titled "Ethereum Roadmap: The Root Chain to Becoming the 'World Computer'." This article systematically reviews Ethereum's development trajectory, protocol evolution, scalability path, and its positioning in the Rollup era, attempting to answer a key question: Why is ETH worth being "held long-term"?

Note: Due to the length of the original text, the translator has made some cuts and optimizations to enhance readability without affecting the original meaning.

DeFi: The First Product-Market Fit (PMF) Found by Ethereum

From its inception, Ethereum has aimed to create a globally shared, trustless computing platform. After ten years of development, it has evolved from an early technical experiment into the core foundation of decentralized finance (DeFi), blockchain space markets, and on-chain application ecosystems.

To understand how ETH has reached its current state, we must start from a key turning point—the product-market fit (PMF) of DeFi. This coincided with the bear market from 2018 to 2020, during which protocols such as ERC 20, Uniswap, DAI, Aave, and Compound emerged one after another, gradually transforming Ethereum into a self-custodial, composable, permissionless financial system. The explosion of DeFi is a natural alignment of technological innovation and market demand.

The "DeFi Summer" of 2020 marked the peak of this phenomenon, with total value locked rapidly increasing, and on-chain transaction volume surpassing centralized exchanges for the first time, revealing the network value of ETH. However, the subsequent high transaction fees also exposed Ethereum's scalability bottlenecks, laying the groundwork for future technological transformations.

The Value Turning Point of ETH: From EIP-1559 to The Merge

If DeFi showcased Ethereum's practical value, then the two upgrades of EIP-1559 and The Merge provided the logic for ETH's long-term value.

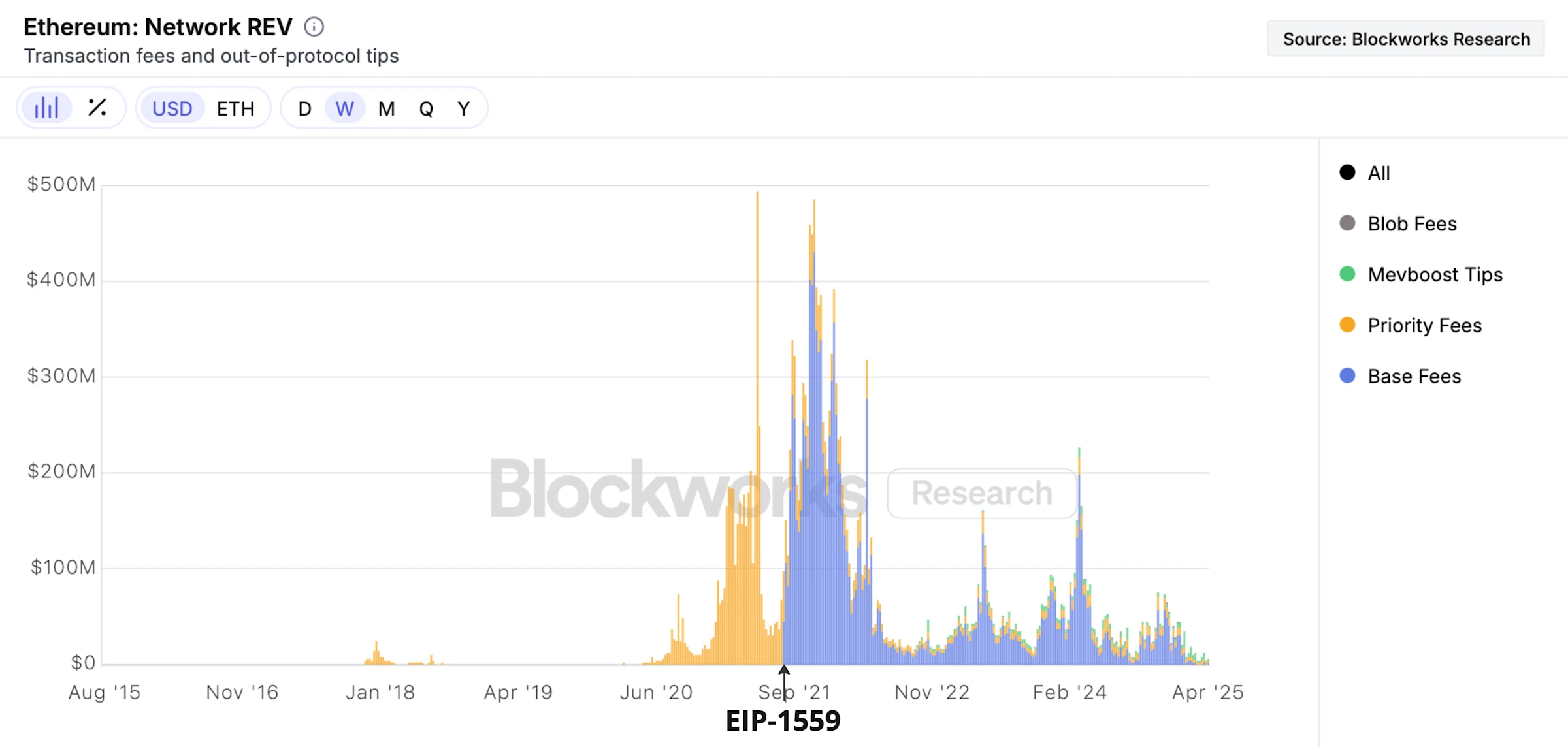

In 2021, EIP-1559 was introduced, fundamentally changing Ethereum's fee mechanism. The original "priority gas auction" model was replaced by a base fee, and the portion of fees paid by all users no longer went to miners but was directly burned. This means that the more active the network, the more ETH is burned, reducing inflationary pressure and strengthening the value support of ETH.

The indigo section shows that ETH began to achieve "value backflow" through the burn mechanism.

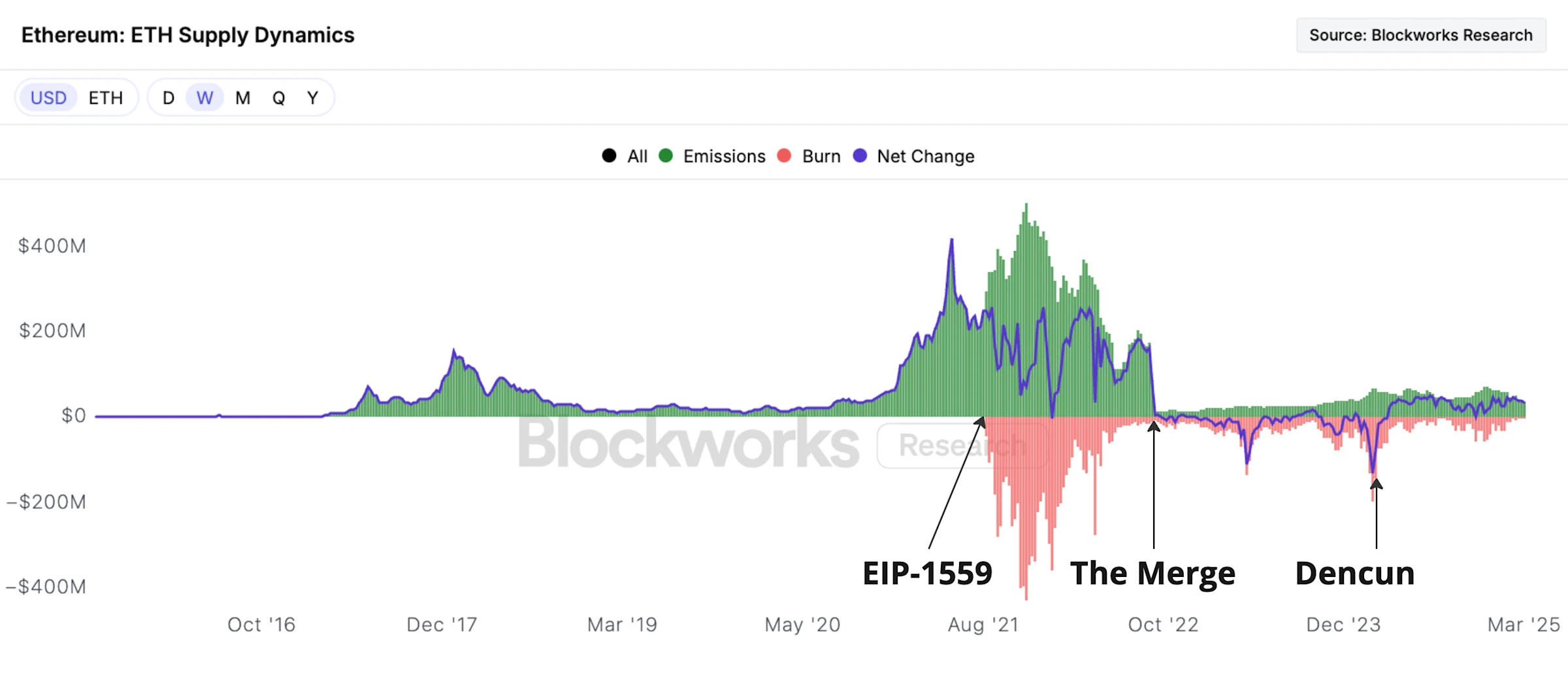

In September 2022, Ethereum completed a historic upgrade: the consensus mechanism switched from proof-of-work (PoW) to proof-of-stake (PoS), marking the official implementation of "The Merge." This transformation was technically challenging yet crucial—it reduced Ethereum's energy consumption by 8000 times and lowered the annual issuance rate required for network security from 4% to less than 1%.

After this, the "net inflation rate" of ETH turned negative for a considerable period.

Green represents the weekly new issuance of ETH, orange represents the weekly burn amount of ETH, and blue represents the net difference between the two.

Long-Term Belief in the Rollup Era: Cooperation or Parasitism?

Scalability is Ethereum's core challenge. Faced with the trilemma of decentralization, security, and scalability, Ethereum ultimately chose the Rollup solution. Rollups execute transactions off-chain, only writing state changes and data to the main chain, ensuring the security of the main chain while significantly increasing transaction throughput.

This also transformed Ethereum from a simple "execution platform" to a "security layer + data availability layer," forming a "Rollup-centric" scalability path.

However, Rollups are not just a technological change; they also alter the logic of ETH's value flow. In the past, users paid fees directly to the main chain, but now most transactions are completed through Rollups, reducing the direct transaction demand on the main chain. Rollups earn revenue by reselling block space, but since the Cancun upgrade, their direct fee expenditure on the main chain has significantly decreased, sparking discussions about "parasitism." In fact, Rollups serve more as "business extensions" of Ethereum, relying on the security and data services of the main chain, bringing in more users and transactions.

Although the transaction demand on the main chain has decreased, the expansion and upgrades of the main chain are still actively progressing, aiming to increase processing capacity by a hundredfold or even a thousandfold in the coming years, providing stronger security and data support for L2. Rollups and the main chain together form a complementary ecosystem, both dividing labor and collaborating, laying the foundation for Ethereum's sustainable development in the future.

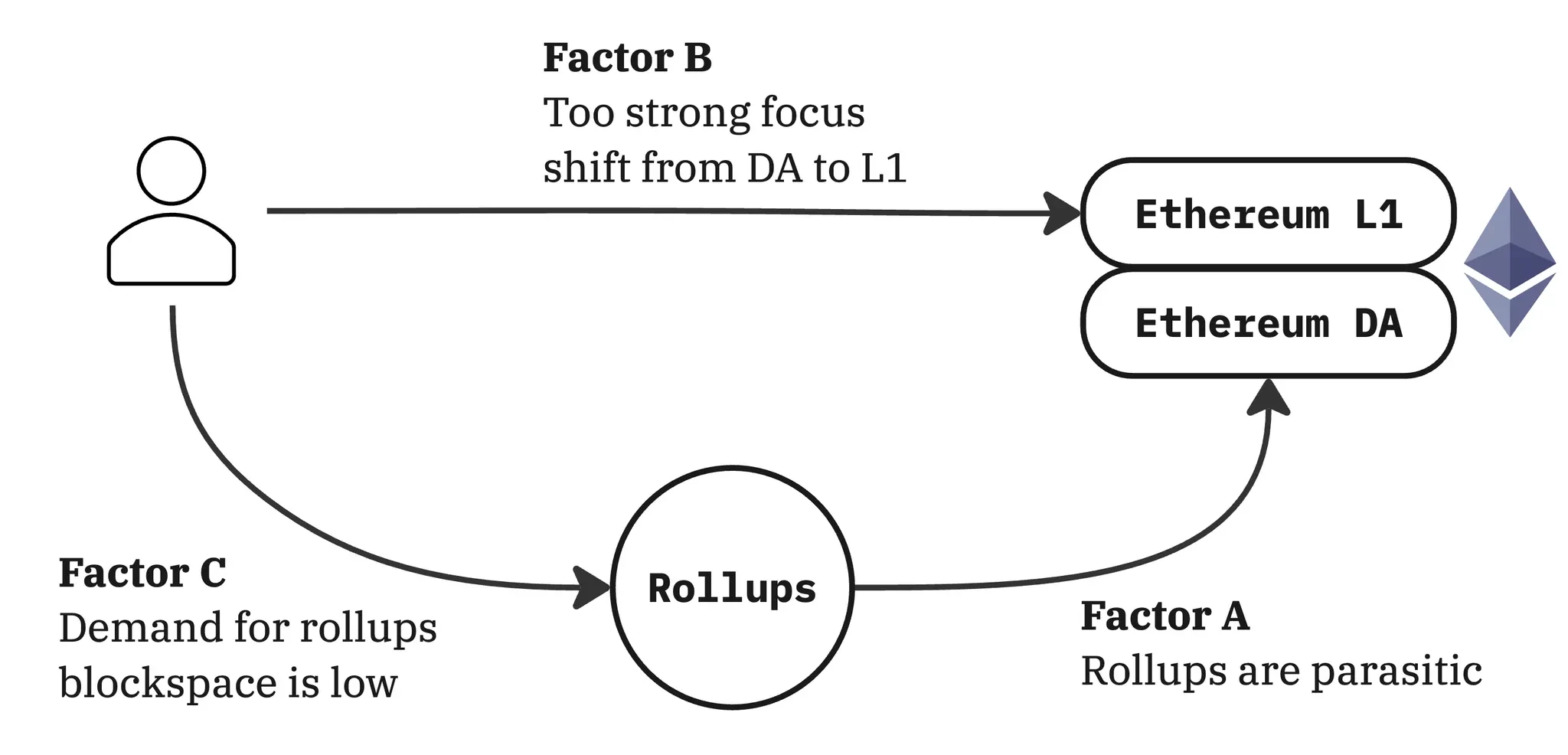

Current Indicators of Ethereum: Crisis and In-Depth Factor Analysis

Since the collapse of FTX in 2022, the crypto industry as a whole has maintained growth, but ETH has significantly lagged behind Bitcoin (BTC) and Solana (SOL). The price of ETH is highly correlated with Ethereum network fees, and since 2022, fee growth has been sluggish, especially compared to the 2018-2022 cycle and the current performance of Solana, revealing significant revenue pressure. The main reasons are threefold:

Factor A: Rollup "Parasitism"

Although Rollups profit from user fees, they have not yet returned sufficient value to the Ethereum mainnet.

From the data, this factor exists but currently has a minor impact on overall revenue. The total weekly revenue of Rollups is only in the millions of dollars, and their fees are low, partly because Rollup sequencers can support gas limits far exceeding those of the mainnet, so they do not need to charge users high fees like L1 networks.

More importantly, it is still early to question whether Rollups have not given back to the mainnet. In fact, the Ethereum community has "unexpectedly" adopted a strategy of providing data availability (DA) space to Rollups for free to attract as many aggregation layers as possible, and this "subsidy" has proven to be a correct approach for early ecosystem building.

Factor B: Shift of L1 Strategic Focus to DA, Marginalizing Mainnet Development

Since the launch of the Rollup route, Ethereum's strategic and user growth focus has almost entirely shifted towards Rollups, while the expansion and maintenance of the mainnet have been relatively neglected.

This bias is indeed true to some extent. When Ethereum was addressing the issue of high mainnet fees, it chose to bet on Rollups for the future, and this "all-in" strategy overlooked the potential of L1 itself. Looking back now, as the fragmentation issues of Rollups have gradually emerged and we have found feasible L1 scalability paths (such as access lists and the development of zkEVM), it seems that the strategic underinvestment in L1 may have been excessive.

However, it must be acknowledged that this judgment is based on hindsight. The Rollup route was a pragmatic move in response to the congestion issues of the mainnet at the time, while solutions like zkEVM were still far from realization. Therefore, it was difficult to reasonably allocate resources between L1 and DA at that time.

Moreover, even if we now have a clear path to increase L1 gas limits by 100 times, achieving performance above 10,000 TPS and supporting a comprehensive public chain computing platform will still inevitably require some form of horizontal sharding. In this context, the choice of a Rollup-first strategy at that time was still a reasonable decision.

Factor C: Rollup's DA Demand Has Not Yet Surpassed Mainnet's DA Supply

This is the most critical and overlooked deep issue: the demand for data availability space (DA) from Rollups has not yet substantially exceeded Ethereum's supply.

Rollup sequencers are highly efficient in packaging transactions for upload to the mainnet, achieving very high compression rates, which leads to them consuming far less blob space than theoretical values. Additionally, some user activities in this cycle (such as meme coin trading) have also been diverted to Tron and Solana.

Before the Pectra upgrade (May 7, 2025), with an assumption of 3 blobs per block, Ethereum's DA supply is approximately 210 TPS. Until November 2024, this supply will exceed market demand. Even if demand rises afterward, the blob gas prices indicate that they have not significantly increased, suggesting that demand has not yet outstripped supply. Recently, Pectra has doubled the blob target to 6 per block, further increasing DA supply, far exceeding actual demand.

Therefore, Factor C is actually the fundamental variable affecting Factors A and B. Once Rollup's demand for blob space truly exceeds supply, blob fees will enter a market discovery phase, leading to a qualitative change in the overall fee structure of the Ethereum network.

How to Evaluate the Value of ETH? The Business Logic of Ethereum

Is ETH a productive asset or a currency? We firmly believe that ETH should primarily be a productive asset and secondarily a currency.

The reason lies in the fact that Ethereum's strongest moat comes from its technological advantages: a trust foundation and stability tested over years, neutrality and censorship resistance brought by decentralization, a leading DeFi ecosystem, a high-quality research and developer community, and a strong network activity assurance mechanism. Ethereum is truly an unstoppable "global computer."

Secondly, as a productive asset reliant on technological adoption, the monetary value of ETH can be solidified and enhanced. While ETH as a currency can more easily cross technological iteration cycles, the most prudent path is to first establish Ethereum as a technological platform, ensuring its economic model is sustainable, and then the currency attributes will naturally emerge. Conversely, relying solely on "hype around ETH as currency" cannot establish a solid foundation.

In short, the price of ETH consists of three parts: the discounted value of future fees, monetary premium (as a store of value, medium of exchange, or even unit of account), and speculative premium (including cultural and meme value). Although the latter two have a significant impact, to strengthen all three, the key is to maximize the underlying network revenue, which is the foundation of ETH's value.

Ethereum's Long-Term Rollup Strategy: Why is it Correct? The Truth Behind the Competition with Solana

The reason Ethereum firmly chooses a "Rollup-centric" expansion route is clear: it is the only architectural design that can balance security, scalability, and neutrality.

From the perspective of technical supply, Ethereum is currently the most secure and decentralized smart contract platform. Through validating bridges and data availability layers (DA), Ethereum can "wholesale" the security of the main chain to Rollups, helping them build their own chains without needing to rebuild a trust system.

From the perspective of market demand, users ultimately do not care which chain they are using—they only care about "where transactions are the cheapest and safest." In the long run, the most rational choice is to become a Rollup, buying security, DA, and consensus, directly connecting to Ethereum. This will naturally create a market convergence phenomenon: Rollups will build their services around Ethereum's "neutral ledger," rather than dispersing to other isolated chains.

Ethereum vs Solana

Based on fee revenue in 2024, some believe Solana has begun to surpass Ethereum in the blockchain space market. However, Solana's strategy centered on hardware expansion carries high risks, with the network periodically experiencing overload issues. If blockchains are to realize their full potential, namely the large-scale migration of financial infrastructure on-chain, Solana will ultimately also need to turn to sharding for scalability, while Ethereum is already far ahead in security, Rollup infrastructure, and ecosystem adoption.

More critically, most on-chain activities on Solana stem from the Memecoin craze. Data shows that such transactions once accounted for over 50% of its DEX trading volume. However, Memecoins are a short-term, zero-sum phenomenon—once the hype fades, their "high-income" myth is difficult to sustain.

In contrast, Ethereum focuses on high-stickiness scenarios like DeFi, where these protocols are driven not by frenzied speculation but by the on-chain migration of real financial behavior.

The most significant and important difference: Solana's validating nodes are centralized, while Ethereum has the most diverse staking network globally. This decentralization itself is the strongest moat.

Issues with the Rollup Strategy

If the Rollup route is correct, and Ethereum's long-term future is bright, why is ETH's price performing poorly?

On a technical level, the biggest flaw of Rollups is the lack of default interoperability, leading to state fragmentation, which severely affects user and developer experience.

On a business level, the key issue is that Ethereum has not clearly communicated the commercial strategy for Rollups:

Short-term adoption strategy: How to drive rapid growth for Rollups?

Long-term moat: Why won't Rollups turn to other data availability platforms?

The Commercial Strategy of Rollups: Expansion, Differentiation, and Moat

1. Ethereum should prioritize expansion and continuously provide ample and low-cost data availability (DA)

The technical network market that Ethereum operates in is highly competitive and rapidly changing, and the ultimate winner will enjoy strong network effects. In this environment, the correct strategy is to provide high-quality products and rapidly expand the user base at extremely low or nearly free prices, which is also the growth path of most successful tech networks.

Therefore, Ethereum must keep the price of data availability (DA) low, minimizing the entry barriers for Rollups. After the Cancun upgrade, Ethereum provided a capacity of 3 blobs, and in the short term, supply exceeds demand, effectively suppressing prices. This strategy, although not intentionally designed, has yielded good results.

2. Solve Rollup interoperability to enhance user and developer experience

Interoperability is the biggest shortcoming of Ethereum in the Rollup era. Fragmentation severely impacts users and developers, and solving interoperability is key to unifying experiences and narrowing the gap with integrated chains, while also building a liquidity moat.

The community is actively promoting solutions such as ERC-7683 for instant medium-scale asset cross-chain swaps and 2-of-3 OP+ZK+TEE hour-level large asset cross-chain bridges.

3. Differentiation strategy and moat building

Ethereum needs to achieve differentiation in DA services to attract marginal Rollup customers while building a moat to lock in ecosystem clients.

Key moats come from three major network effects: trust, liquidity, and composability. Currently, the demand for cross-Rollup composability is not clear, with the main value concentrated in trust and liquidity, both of which will naturally extend from Ethereum L1 to the Rollup ecosystem after interoperability is resolved.

In terms of trust, Rollups enjoy the highest security guarantees through Ethereum DA, while independent chain security is weaker; Rollups adopting Ethereum DA continuously enhance their security, solidifying their moat.

In terms of liquidity, the institutional-level liquidity of Ethereum L1 is a crucial factor for Rollup choices. After integrating with Ethereum DA, Rollups can access the entire ecosystem's institutional liquidity, significantly improving capital efficiency and forming a solid moat.

Thus, the market will drive Rollups to use Ethereum DA to obtain the highest security and liquidity. Ethereum should strengthen these two advantages and attract institutional clients through branding and trust.

The Path of Value Backflow: From "Maximizing Fees" to "Maximizing Value Carrying"

When Ethereum expands data availability (DA) to the level of millions of TPS (such as through solutions like 2D PeerDAS), and the Rollup ecosystem voluntarily and firmly binds to Ethereum DA, Ethereum will gain significant fee revenue.

At the main chain level, the widespread adoption of DeFi and enterprise applications will become the main driving force, while the popularity of Rollups will further amplify this effect. Meanwhile, Rollups will also pay fees for interoperability and settlement services, contributing further revenue.

At the DA level, the key to achieving a sustainable economy lies in raising the minimum blob price. The specific approach is to monitor the overall revenue of Rollups and set a reasonable minimum price, ensuring that Rollups pass a certain proportion of value back to Ethereum.

For example, in the coming years, if Rollups capture the CeDeFi payment market, processing about 10,000 TPS with annual revenues in the billions, while Ethereum DA supply exceeds 10,000 TPS, the blob transaction fees, although not fully entering market price discovery, could be set at a minimum fee of 0.3 cents per DA transaction burned, bringing approximately $1 billion in annual revenue to ETH holders.

Further covering high-frequency trading markets, such as social, trading, and AI agent coordination, Rollups' TPS could reach the 30,000 level, generating DA fee revenue exceeding $10 billion, while transaction costs remain below one cent.

Such revenue is influenced by ETH prices and other factors, the minimum price needs to be dynamically adjusted, likely determined by community consensus, similar to today's gas limit mechanism. Future research should also delve into optimal pricing strategies for blobs, such as improving the correlation with Ethereum L1 fee markets. Additionally, as Ethereum transitions to zkEVM or RISC-V, new technologies like SNARK infrastructure will help enhance fee capture efficiency.

The key is that at this stage, we should not rush to extract value directly from transactions, but rather maximize support and promote high-value activities in Ethereum blocks and blob space. This will not only generate and enhance network effects but also help Ethereum seize the expanding block space market, solidifying its economic foundation. The path of value backflow is therefore very clear.

Risk warning

Risk warning Risk warning

Risk warning