a16z: What major problems will fintech solve in 2022?

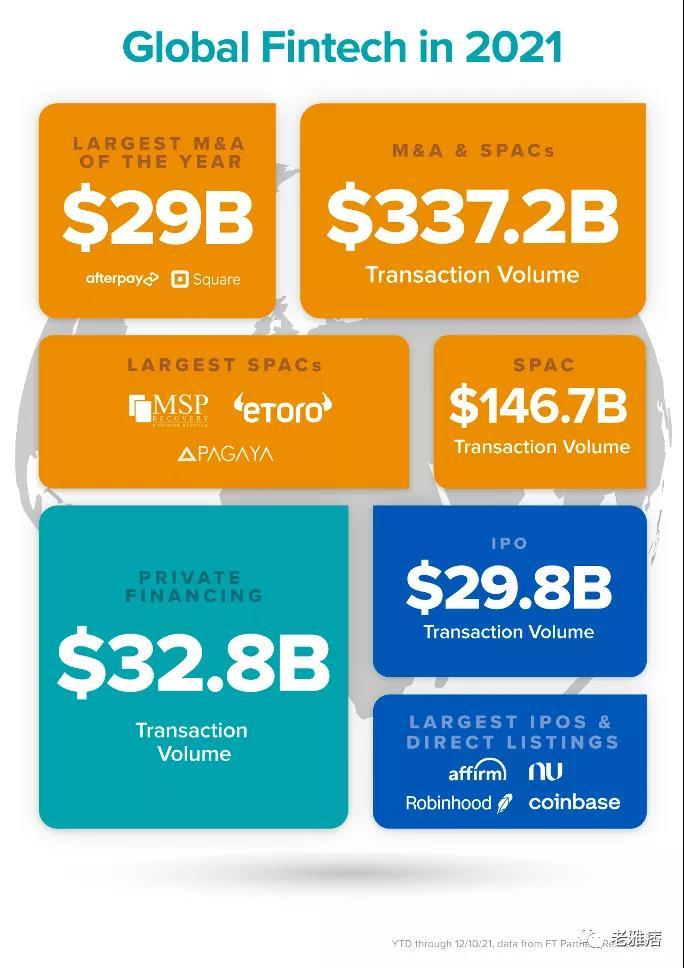

In 2021, financial services continued to have its moment—fintech fundraising exceeded all previous years; it was a big year for fintech IPOs.

In 2021, financial services continued to have its moment—fintech fundraising exceeded all previous years; it was a big year for fintech IPOs.Author: Lao Yapi

In 2021, financial services continued to have its moment—fintech fundraising surpassed all previous years; it was a big year for fintech IPOs; and large-scale fintech mergers and acquisitions reached historic highs. Before the end of the year, we saw one of the largest fintech IPOs, Nubank raising $2.6 billion (as the largest digital bank), one of the largest fintech acquisitions, Square acquiring Afterpay for $29 billion, Wise going public directly in the UK, Coinbase going public directly as a fintech/cryptocurrency service, and multiple fintech SPACs.

What major problems might fintech solve in 2022?

I. Fintech x Cryptocurrency

1. Low-carbon technology permeating all financial services

Twenty years ago, "Is it an internet company?" was a common question. Today, (almost) every company is an internet company. Ten years ago, "Is it a mobile company?" was a common but now outdated question. Similarly, we will soon stop asking "Is it a cryptocurrency company?" because most companies—starting from the broader financial services industry—will have a cryptocurrency component.

As cryptocurrencies occupy an increasing share of consumer mind space, financial applications are adding cryptocurrency products to further gain wallet share. For example, Robinhood started with stock trading and now facilitates some cryptocurrency trading; some neobanks allow customers to earn higher yields through DeFi (decentralized finance); and large banks are in the early stages of experimenting with cryptocurrency products. In 2022, we will see more cryptocurrency infrastructure being built for transfers, wallets, yield-as-a-service, custody, etc., so consumers can continue to integrate and manage their fiat and cryptocurrency financial lives. We will also see a wave of new fintech companies powered by backend cryptocurrency infrastructure, as well as what others call DeFi mullets (fintech in the front, DeFi in the back).

- Angela Strange, General Partner at a16z Fintech, and Sumeet Singh, Deal Partner at a16z Fintech

2. The web3 community will become a major political constituency in the U.S. midterm elections

As we close out this year, one in five U.S. voters now owns cryptocurrency. According to a recent poll we conducted, the future of web3 and the internet will influence how many people vote in the 2022 U.S. midterm elections.

Web3 voters are young and diverse. 79% of millennial voters, 73% of Hispanic voters, and 79% of Black voters are more likely to vote for candidates who support expanding web3. These voters largely came of age after the Great Recession, many from communities that have been overlooked in attempts to build generational wealth. They seek a meaningful alternative to the current financial system—one that allows them to have direct control over their funds and provides investment options for parts of society overlooked by traditional financial institutions.

So, what do these voters care about? They want policymakers to focus on regulations that combat bad actors and illegal activities while ensuring that regulations do not hinder economic opportunities for everyday Americans. They want policymakers to support and engage with our national technology strategy. They overwhelmingly believe that web3 can give consumers more control over their data. They believe web3 can strengthen America's technological leadership on the global stage. They also want the government to play a proactive role in supporting community-owned web3 platforms.

There is no doubt that web3 will be a significant part of next year's elections, and policymakers are quickly recognizing the stakes involved.

- Tomicah Tillemann, Global Crypto Policy Lead at a16z, and James Rathmell, Crypto Advisor at a16z

3. Community-centric social investment platforms

What do the GameStop saga and ConstitutionDAO have in common (besides Citadel's Ken Griffin)? They both illustrate that internet community participants want to collectively use their funds for a greater purpose—whether that purpose is running a distributed hedge fund or purchasing a copy of the Constitution.

In 2022, we will see multiplayer, community-driven social investment platforms leveraging this culture of collective action on the internet. We see many products being built here that are not similar to other social products; thus, they do not have features like leaderboards and trade tracking, but instead focus on new product primitives like asset pools, voting, and coordination to achieve collective investment, whether it be a distributed hedge fund, advancing social and environmental goals, or pooling funds to purchase collectively owned assets. These products will have clear advantages—given the multiplayer nature, embedded distribution; given that they can add fun, higher engagement.

- Sumeet Singh, Deal Partner at a16z Fintech

II. Fintech x Healthcare

Every healthcare company is a fintech company

As we mentioned earlier, fintech products enable vertical SaaS companies to diversify into new revenue streams. In the healthcare sector—a system that accounts for 20% of U.S. GDP—we see three areas where fintech capabilities can supercharge the industry in 2022: consumer payments and lending, provider practice capabilities, and insurance. Due to the third-party payment system in the U.S., healthcare payments are particularly complex, where providers bill for services, payers reimburse for those services, and consumers receive the services. Therefore, a universal solution like Stripe is unlikely to provide the full suite of features needed to support healthcare practices, such as regulatory compliance and health plan integration. This leaves opportunities for payment gateways and financing products specific to verticals, such as "buy now, pay later" (BNPL), helping consumers finance their medical bills and reducing the risk of bankruptcy due to unexpected medical expenses.

On the provider side, BNPL can improve collection rates, which can be as low as 20% in some areas. There are also emerging fintech products designed to help healthcare institutions normalize their business models to a "per member per month" (PMPM) arrangement by taking on risk and increasing billing capabilities for new service lines, diversifying revenue and profit streams.

Finally, the unbundling and rebundling of traditional health insurance has created new fintech platforms supporting the burgeoning development of new insurance products for individuals and businesses. These companies modularize underwriting, claims processing, provider network management, and utilization management capabilities, helping businesses manage the risk of their insured populations in a more flexible, affordable, and transparent manner.

As fintech enters the healthcare service and software space, we see the potential to reshape incentives and eliminate inefficiencies, paving the way for a more value-driven healthcare system.

- David Haber, General Partner at a16z Fintech, Julie Yoo, General Partner at a16z Bio

III. Fintech x Sustainability

Fintech moving towards net-zero carbon

Have you noticed that Google Maps now defaults to directing you on the most fuel-efficient route? Or that the "paperless billing" box on your bill has already been checked when you opened your account? This environmentally conscious configurability is making its way into the fintech space. Imagine a checkout experience where switching between debit cards, credit cards, ACH, PayPal, BNPL, and all the various payment methods available in 2021 shows which method has the least environmental impact for that specific merchant. Or better yet, it embeds a feature that allows you to add x dollars at the time of purchase to offset the emissions of whatever path you choose. Improvements in emissions data infrastructure and technology are making this scenario rapidly possible. As companies like Patch, Capture, and Wren make it easier for businesses and consumers to understand their climate footprints and take action, payment providers, neobanks, logistics companies, and more may embed carbon offset options into their products.

However, it remains to be seen what will incentivize consumers to choose more environmentally friendly products or delivery methods over those that may be more convenient. Just as the eco-friendly route on Google Maps may actually be the slowest, today, green choices in business are often the most expensive. Startups at the intersection of climate and fintech must create new incentive structures that make eco-friendly choices not only more responsible but also more affordable and rewarding than their traditional counterparts. Think higher interest rates, lower fees, better returns, or reduced costs.

One of our favorite case studies around creative incentive adjustments in this space comes from Powerledger, a blockchain platform for peer-to-peer energy trading, and Carlton United Brewery in Australia. When Carlton set a goal to be powered entirely by renewable energy by 2025, they partnered with Powerledger to create an eco-friendly beer drinker loyalty program: exchanging excess energy for beer kegs. Carlton's customers can sign up to receive beer delivered to their homes in exchange for the excess energy generated by their home solar panels.

- Mark Andreesku, Deal Partner at a16z Fintech

IV. Trends in the Fintech Space

1. Overcoming rising CAC through partnerships and product-led growth

In recent years, we have seen meaningful inflation in digital customer acquisition channels (FB and GOOG) due to increased competition and changes like Apple’s ad tracking making attribution harder. To further fuel competition, the vast majority of fintech companies have focused on the same customer characteristics (subprime), offering the same products (like banking, investing, lending), and a growing array of customer subsidies to join (free money on the internet!). So, in 2022, how will companies differentiate themselves in the face of increasingly fierce competition and constrained digital acquisition channels?

We believe there are two answers— the best companies will grow through products that are suited for product-led growth, or partnerships representing non-inflationary distribution opportunities.

On the product side, we see today’s products turning into tomorrow’s primary products; simply offering a bank or brokerage account is no longer enough to stand out, as new APIs make it exceptionally easy to integrate core banking functionalities (like saving, spending, lending, investing) into almost any application experience. Instead, products that capture consumer imagination will remix these fundamentals in new and interesting ways, leveraging community, cryptocurrency, and commerce. In particular, we expect to see more multiplayer products driving product growth—money itself is a multiplayer game (medium of exchange!), but so far, financial products have largely been single-player games.

On the partnership side, we have seen Credit Karma partner with the Houston Rockets, Chime with the Dallas Mavericks, and Guideline with Gusto for distribution agreements and Melio with Intuit for distribution agreements. While these channels have price leverage and may increase prices over time, they represent the kind of predictability and volume in acquisition costs and supply that has been largely absent in recent digital marketing channels. Founders would be wise to take note of these examples—those companies that have historically been best at direct-to-consumer marketing are now seeking business development and partnerships for sustained growth, and we expect this trend to continue into 2022.

- Anish Acharya, General Partner at A16Z Fintech

2. More fintech will emerge in emerging markets

This year, emerging markets have seen explosive startup activity, record funding, and impressive exits. In particular, Nubank’s IPO is a watershed moment for Latin America and global fintech, representing a massive exit for the region and spawning a new generation of founders. 2022 will bring more investment and innovation growth for financial services across the entire emerging market. We may see several major trends in the types of companies that emerge.

Historically, emerging markets have had a lot of B2C fintech, and now we will see more B2B helping small businesses and enterprise clients digitize and optimize payments, pay employees more efficiently, procure supplies, handle accounting, insure themselves, and more.

Second, new modern APIs will enable companies to make payments, access bank account information, issue cards, bridge cryptocurrencies, verify identities, and more. Instead of needing to manually establish a one-time integration with traditional financial systems, companies will be able to plug into modern infrastructure, allowing them to launch new fintech products with less upfront cost. There needs to be enough demand to justify the new infrastructure, and we are already beginning to see that meaning in the ecosystem.

Third, the emerging business models will increasingly look to other emerging markets for inspiration rather than the U.S. and Europe. Based on existing user behavior, regulations, and stages of digitization, there are certain business models and feature sets that are better suited for the entire emerging market. For example, many homegrown B2B marketplaces (embedded with fintech) have emerged in India and Latin America that do not exist in the U.S. or Europe, partly because these marketplaces provide opportunities for small businesses in areas like credit and logistics, which tend to be particularly expensive and fraught with friction in emerging markets. We have already seen business models like super apps (including both consumer and enterprise) and community buying platforms thrive, as well as feature sets like investment apps starting with funds rather than stock trading.

We have seen the interconnectedness of entrepreneurs in these regions. We met founders building small business accounting infrastructure in São Paulo who regularly get advice from their counterparts in Jakarta via WhatsApp. Entrepreneurs in Lagos are looking to Karachi for inspiration on business models for their B2B marketplaces. The pandemic has accelerated many tech trends, but it has also significantly shrunk the world.

- Seema Amble, Partner at a16z Fintech; David Haber, General Partner at a16z Fintech; Gabriel Vasquez, Partner at a16z Fintech

3. Insurance MGAs refocusing on underwriting issues

The first wave of insurance startups mostly focused on moving historically offline processes online without touching most of the underwriting processes. With a long-term low-interest-rate environment, insurers are more willing to test new markets and strategies to find yield. Coupled with the lack of scale in the insurance startup ecosystem compared to other markets, many capability partners view new entrants as testing partners to learn and experiment with finding new profit strategies. As interest rates rise and the market hardens, refocusing on underwriting differentiation and profitability will become a priority, potentially driving acquisitions in the first generation of insurtech and new entrants focused on monetizing underwriting advantages.

- Joe Schmidt, Deal Partner at A16Z Fintech

Risk warning

Risk warning Risk warning

Risk warning

Popular articles