Will LUNA, based on the algorithmic stablecoin ecosystem, experience a death spiral?

The current situation of LUNA is like a giant door swinging on small hinges.

The current situation of LUNA is like a giant door swinging on small hinges.Author: 0xHamZ

Compiled by: 0x137, Rhythm BlockBeats

This article is organized based on the views published by DeFi researcher 0xHamZ on his personal social media platform, and is translated and organized by Rhythm BlockBeats as follows:

The current situation of LUNA is like a giant door swinging on small hinges, with $10 billion of "hot money" in the entire ecosystem, but a daily swap limit of only $100 million. So what could happen in the worst-case scenario?

Terra is a decentralized blockchain designed specifically for algorithmic stablecoins, operating between two tokens: UST and LUNA, where UST is the stablecoin pegged 1:1 to the US dollar, and LUNA is the governance token. The valuation of LUNA is essentially the present value of the fees generated over time from the use of UST. UST has no collateral backing it and relies solely on incentives to achieve its peg; to mint new UST, a corresponding amount of LUNA must be burned.

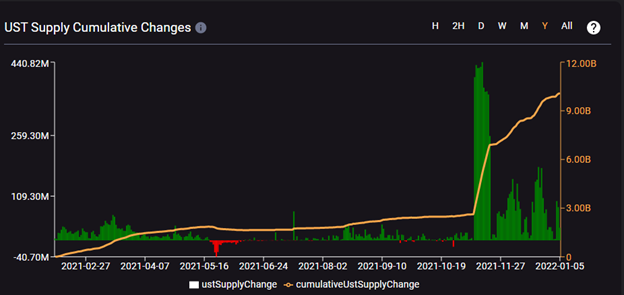

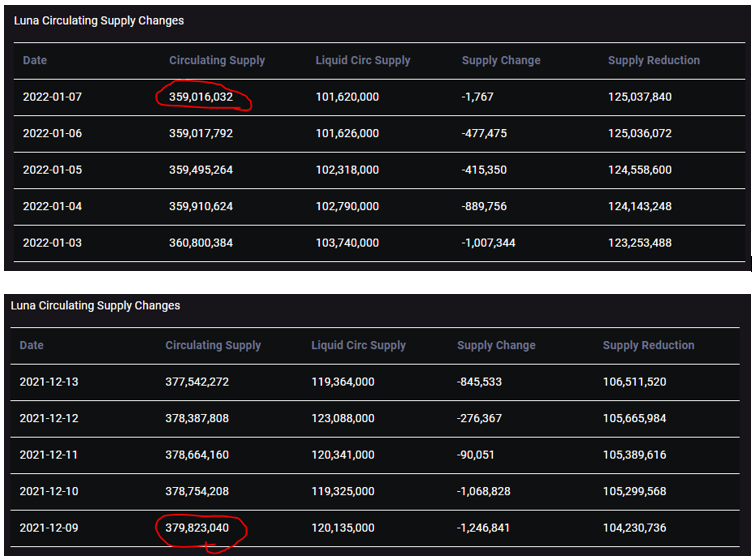

Recently, we have seen a parabolic growth in the adoption of UST, accompanied by a significant reduction in the circulating supply of LUNA, with nearly 5% burned in just one month.

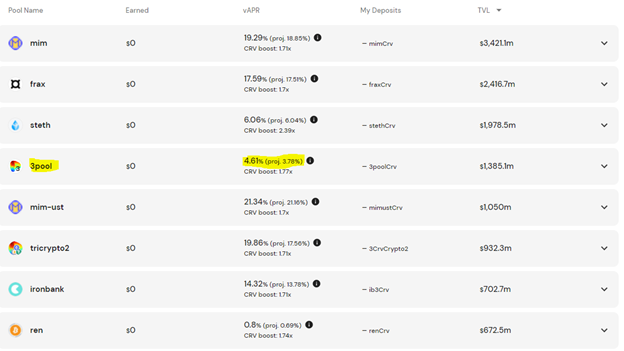

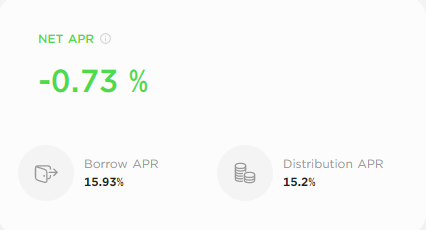

It is worth noting that 90% of UST adoption comes from deposits and borrowing services on Anchor (Terra's money market platform), as Anchor "guarantees" a 20% APY, which is highly competitive compared to other stablecoin yield farming opportunities on platforms like Convex. Who wouldn't want their stablecoin to "guarantee" a 20% return?

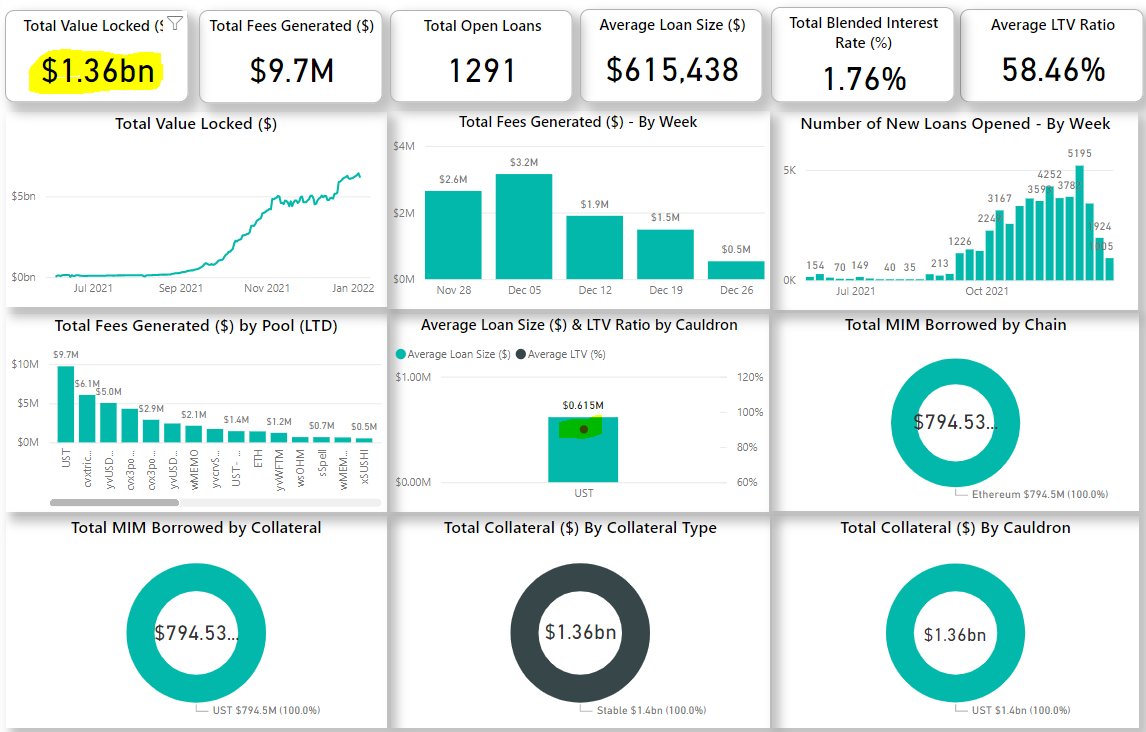

Another key to UST's growth is the Degenbox farming strategy on the Abracadabra platform, which added 1.4 billion UST and was immediately "sold out."

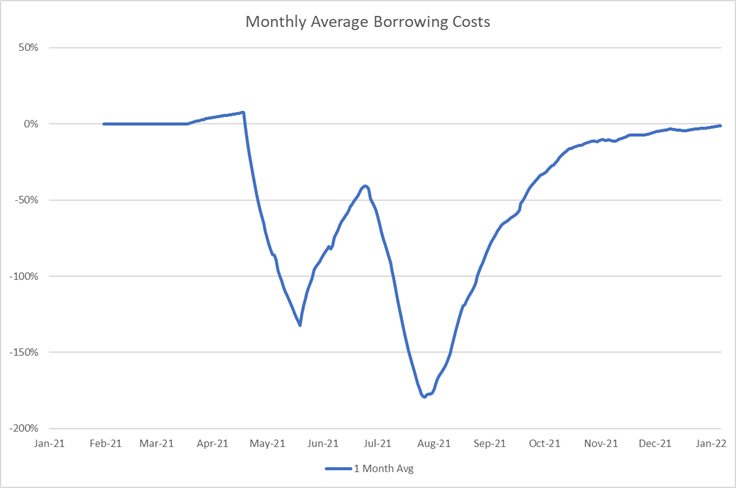

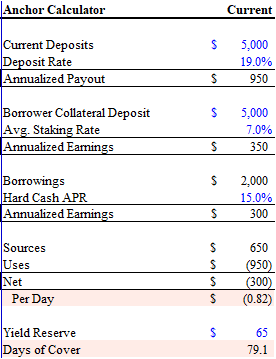

The savings yield for users on the Anchor platform consists mainly of two parts: the loan interest charged to borrowers and the staking rewards generated from the collateral deposited by borrowers (mainly LUNA). For most of 2021, the Anchor platform was essentially paying users to borrow UST, which incentivized borrowers to take out more UST, meaning more LUNA was burned, and its price would rise accordingly.

Currently, the cost of borrowing UST on Anchor is almost zero. This is great for LUNA, as the use of UST drives the burning of LUNA.

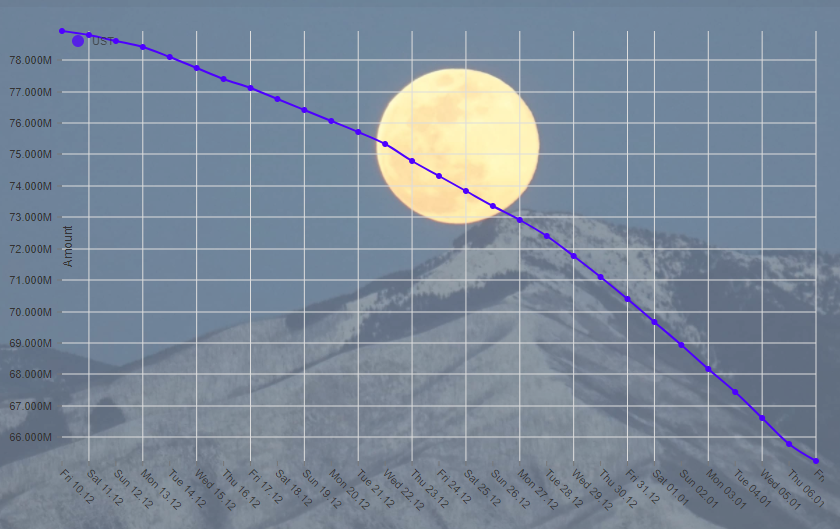

However, the current APY on savings accounts at Anchor is depleting the protocol's own savings. Anchor needs to find ways to lower its deposit interest rates or seek new methods to incentivize more borrowing.

Before Anchor adjusts its deposit and loan rates, depositors currently have only an 80-day protection period.

However, changing the deposit interest rate may cause funds to migrate to the ecosystems of other public chains. First, selling UST means that new LUNA needs to be minted, leading to a decrease in the price of LUNA. In this process, some borrowers' collateral may be liquidated, which would reduce the source of APY payments to savings users.

When borrowers take out UST, they need to deposit bLUNA generated by staking LUNA through LIDO. Given that the peg between the two is not very reliable, the ratio of bLUNA to LUNA becomes very important. For example, last May, you could exchange 100 LUNA for 110 bLUNA and burn it in about three weeks to receive 110 LUNA.

Given Anchor's leverage and maximum LTV threshold, when the price of LUNA falls to $55 and triggers liquidations, the ecosystem faces significant risks.

The Terra ecosystem has a daily UST/LUNA swap limit of only $100 million, with a cap of 0.5%. When larger-scale redemptions occur, the spread of UST will grow exponentially. Last May, there were 80 million LUNA/UST liquidations at peak, exceeding the redemption limit, causing the spread to soar to 7-8%. In this case, the peg of UST was effectively broken.

When UST falls below its peg, two arbitrage opportunities arise:

• Buy at $0.94 and sell at $1, arbitraging 6%

• Buy UST at $0.94, convert to 1 LUNA, sell LUNA for USDC, and repeat the process

Once the peg fails, the entire ecosystem can become self-reinforcing. If LUNA drops to around $50, the resulting liquidations and withdrawals could drive the price of LUNA further down to $35. At this point, the market cap of LUNA may be significantly lower than that of UST, creating a vicious cycle of minting and burning.

To reinforce this point, we can analyze the market volatility ratio of LUNA/UST. Currently, the correlation between the market caps of LUNA and UST is only 0.8 (highly volatile)!

In summary, the entire process would be as follows:

• Market volatility leads to a drop in LUNA's price

• The drop in LUNA's price leads to the liquidation of Anchor's collateral

• Redemptions exceed the $100 million cap, widening the spread

• The widening spread accelerates the drop in LUNA's price, causing UST's peg to fail

• Arbitrageurs buy cheap UST, redeem LUNA when the spread is favorable, and sell in the market, further driving down LUNA's price.

Risk warning

Risk warning Risk warning

Risk warning