Curve Empire Chronicles: A Leading Player in Enhancing Capital Efficiency

Curve.fi will become a cornerstone of DeFi, just like Uniswap, Maker, and AAVE, in the foreseeable future.

Curve.fi will become a cornerstone of DeFi, just like Uniswap, Maker, and AAVE, in the foreseeable future.Original Author: Bald GaoFlynn

Original Source: Mirror

Preface

Curve.fi --- The TVL King in the Defi World. Curve.fi is not a complex defi product in terms of functionality, but its derived ecosystem is intricate and is significantly impacting the entire Defi world with great energy. This article will review some history, explain the economic model of Curve.fi, and provide some personal analysis. In the foreseeable future, Curve.fi will become a cornerstone of Defi, just like Uniswap, Maker, and AAVE, and is a project that every Defi player should deeply understand.

The Basic Value of Curve.fi

Large-scale low-slippage stablecoin trading. From the very beginning, Curve has targeted the large-scale stablecoin AMM exchange market. Their unique algorithm ensures that slippage is extremely low most of the time, which has been detailed in many articles and can also be referenced in their white paper.

Stablecoin trading is the most suitable scenario for liquidity mining in the AMM field. The biggest problem with traditional AMM mechanisms for liquidity providers is impermanent loss. In simple terms, the situation where the prices of the two tokens in the AMM are relatively stable and have a large trading volume is the most suitable for AMM liquidity mining.

A truly decentralized central bank issues a sufficiently consensus-driven, payable stablecoin, which has always been the LAUGH TALE of all idealistic Crypto heroes. Here, I do not intend to elaborate on the progress related to stablecoins, but the conclusion is that Curve.fi provides an incubator for the development of stablecoins. During the long transitional phase, various innovative stablecoins can use Curve to anchor their initial value and buy time for the development of their project scenarios. As a bridge between these stablecoins, Curve will become a long-term Defi infrastructure, and the trading volume of these stablecoins is the foundational value of Curve.fi.

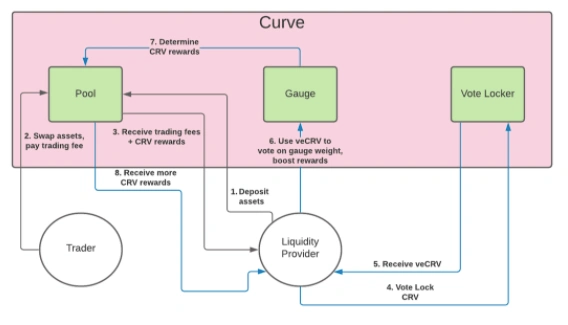

The merits and flaws of the veCRV mechanism

The merits and flaws of the veCRV mechanism

Introduction to the veCRV Mechanism

Collect 50% of the transaction fees from the Curve protocol, with the fee distribution divided according to the proportion of veCRV held.

Vote Power. The voting power of veCRV is very simple; it is proportional to the locking time. veCRV will decay over time, so to maintain sufficient voting power, one must continuously refresh the locking time.

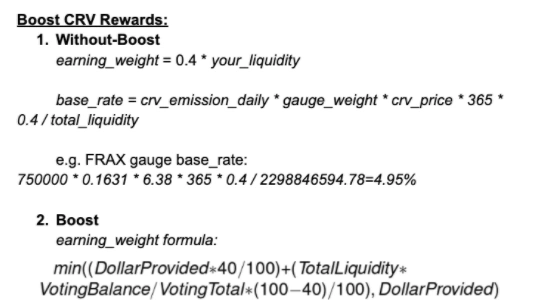

Boost Mechanism. Boost is an acceleration mechanism for liquidity mining. Without boost, the base for liquidity mining is only 40%. Only by holding a sufficient amount of veCRV can one achieve a boost multiplier, up to 2.5x, in a linear increase mechanism. The specific algorithm can be referenced in the formula in the image below:

Boost Calculation Formula

Basic Mechanism of Curve

Why veCRV Changed Everything

Time -> Consensus -> Value

The veCRV mechanism has finally been unearthed through the test of time. All consensus requires the accumulation of time. How to accumulate value through time is the simplest method of Curve.fi: locking, and quantifying the value of the lock --- voting power. In fact, increasing voting power through locking is not a new concept, but why did veCRV succeed? It mainly relates to the synergy with the boost mechanism. Users have a very direct reason to compete for CRV: more votes mean more rewards, which is the foundation of the veCRV game. This feature allows project teams to almost permanently lock a portion of CRV to maintain their power on Curve. At the same time, this veCRV also counters the situation where users buy large amounts of tokens for voting and then sell them off after voting, thus stabilizing the token price.

Flaws of veCRV

The voting mechanism + boost mechanism is the basis of the game, but veCRV itself is non-transferable, meaning that voting rights only belong to the address that staked the CRV. The boost mechanism also only exists at that address. An address providing liquidity must also hold a sufficient amount of CRV to maximize returns. Essentially, this mechanism is not a major issue; Curve hopes that all liquidity providers are also competitors for the CRV token. Once liquidity providers understand this game, they will compete to buy and lock CRV to exercise their voting rights in their respective pools.

However, problems still arise in reality. Due to pre-mining and early-stage inflation being too rapid, later on, users find that to achieve the maximum boost, an excessively large amount of CRV is required. This leads to a division between large CRV holders (whales) and retail liquidity providers, resulting in the veCRV mechanism becoming a flaw and marking the beginning of the optimization platform wars that will be introduced next.

The Multi-Dimensional War of the Curve Universe

The wars surrounding Curve have never ceased since its inception. As more participants join, the battles have become grand and have begun to extend to all corners of Defi. Next, we will introduce several dimensions of the war.

The War of Curve.fi Yield Platforms

The previous discussion highlighted the unreasonable design of the veCRV non-transferable system and early project operation issues, leading to stratification among CRV holders and liquidity providers. Seizing the opportunity, Yearn provided its own solution, particularly with Yearn's yveCRV, which dominated for a long time before Convex. They leveraged their advantage in CRV quantity to accelerate yields, attracting user deposits, and re-locking 10% of mining rewards into the Curve gauge to continuously increase their boost capability. This is the source of the excess returns promised to users.

Subsequently, Curve.fi core member Julien Bouteloup presented his solution: StakeDAO, and the competition officially began. Through voting in the Curve DAO, StakeDAO became the second CRV custodial protocol to obtain the Curve governance whitelist (SmartWalletWhitelist) after Yearn.

Here, it is worth mentioning Curve's SmartWalletWhitelist. This is a special mechanism because veCRV on contract addresses can break the transfer restriction. To prevent abuse of this privilege, Curve established this whitelist mechanism, and to date, only Yearn, Stake DAO, and Convex are on the list. The authority to add to the whitelist is firmly held by CRV core whales.

The Council of Elders in the Curve Empire, the 9 most powerful individuals

Following this is the current king: Convex. The mechanism of Convex is a key focus. Convex uses the cvxCRV scheme to tokenize and bond the non-transferable voting rights of veCRV. By permanently converting CRV into cvxCRV and locking it on the Convex platform, newly issued CVX tokens proxy these CRV voting rights, establishing a liquidity pool for cvxCRV close to a 1:1 ratio with CRV, providing a certain exit path. These factors give CRV holders a strong incentive to deposit CRV into Convex.

In this war, StakeDAO ultimately chose to support Convex, transferring its CRV into Convex to help it achieve initial accumulation. At the same time, Convex attracted the vast majority of CRV users, capturing over 50% of veCRV and winning the final battle of the optimization platforms.

The mechanism of Convex has repaired the economic model of Curve.fi. Although from the author's perspective it is not perfect, it is already an excellent solution. The author believes that CRV and CVX should essentially have a better integrated solution, but this view can only be proven by history. In the following chapter on liquidity wars, the far-reaching impact of Convex will be discussed.

The Stablecoin Trading Volume Offensive and Defensive Battle Between Curve.fi and Uniswap

Recently, Uniswap V3 also launched a 0.01% fee scheme, with a very clear goal of targeting Curve.fi's stablecoin foundation and large-scale stablecoin exchanges. However, due to the relatively low fee revenue, although the overall TVL is still not as high as the 3CRV pool, it has posed a significant threat in transactions below one million dollars.

The essence of the battle for dominance among DEXs is the trading share of major cryptocurrencies: BTC, ETH, and the three major stablecoins in 3CRV. Curve.fi's counter-strategy is very clear. In the reality where it cannot compete with Uniswap in the long-tail effect of altcoins, it has chosen the most reasonable strategy: a low-slippage AMM solution for mainstream coins, launching its own algorithm for the ETH/BTC/USDT Tricrypto Pool. Is Tricrypto Pool a better AMM solution? It remains to be seen, but as a defensive strategy, the current TVL and daily trading volume of Tricrypto V2 can be said to have exceeded expectations, and we look forward to better performance from Tricrypto.

The Liquidity Leasing War Among Stablecoin Projects

After discussing the wars of optimization platforms and stablecoin trading volume, we arrive at a more grand battlefield: the liquidity leasing war among stablecoin projects. The first two wars were like battles for the construction rights of an arena, and now it is the war of the gladiators.

During the DeFi frenzy in 2020, various projects completed liquidity deployment through a dual-pool model. However, the dual-pool model became a deadlock in the later stages of DeFi summer. To compete for liquidity, projects had to raise yields to astonishing levels, making the inflation rate of tokens difficult to control, and under the pressure of large whales selling, they rapidly collapsed. This led to a critical issue: project teams did not have enough time to build a true value consensus for their project tokens and could not distribute tokens equitably.

After the basic value of CRV transaction fees reached consensus, stablecoin projects discovered that they could share the entire platform's fees through veCRV while securing more valuable liquidity through sufficient voting power. Additionally, the characteristics of locking time + voting power decaying over time further ensured the rise in token prices. These characteristics are the foundation for projects to compete for value.

Convex, the true driving force behind the Curve liquidity war, has intensified the Curve war to a boiling point. Therefore, we will review some of the product mechanisms of Convex:

Convex separates the voting rights and revenue rights of veCRV by permanently converting CRV into cvxCRV. CRV becomes a transferable eternal bond through cvxCRV. Compared to before, users can earn most of the original veCRV revenue (after Convex deducts 10% of CRV revenue) without locking while also earning CVX; the voting rights of veCRV are transferred to vlCVX ------ locked CVX.

CVX voting rights proxy. Long-term CVX holders can vote by locking CVX for 16 weeks and can also transfer voting rights to specific addresses, making the bribery voting mechanism easier to execute.

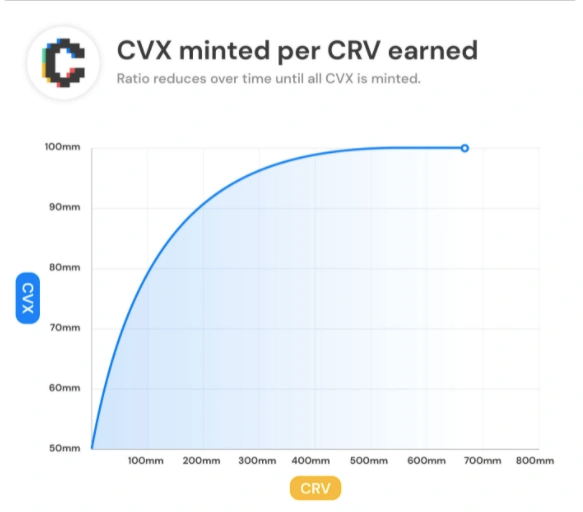

The minting curve of CVX will gradually decrease after claiming CRV revenue, meaning that CVX will gradually deflate as CRV increases. This means that as CRV continues to be absorbed, the voting power controlled by each locked CVX will increase over time, indirectly representing a fundamental value of CVX.

CVX Mint Algorithm

Many people describe Convex's relationship with Curve as a nesting doll, but the author prefers to see it as a repair and enhancement. Although Convex has absorbed a significant portion of Curve's market value, it has greatly liberated Curve's energy and completed the construction of the arena. Especially after cvxCRV and CVX separated the revenue rights of CRV, warlord projects can focus on the competition for voting rights on Convex, striving for greater benefits for their users, while ordinary users only need to choose to provide liquidity or convert CRV into higher-yielding cvxCRV bonds while selling their voting rights.

How Warlords Achieve Victory in the War

Vote, vote, vote!!

From the initial veCRV to the later CVX and then to bribing votes, the means by which warlords compete for voting rights are constantly increasing. Currently, the main methods include:

Purchasing CRV and obtaining voting rights through unlimited locking.

Purchasing CVX and obtaining voting rights through unlimited locking.

Bribing votes by purchasing votes from retail users with their own tokens.

Ultimately, the cost of voting rights is what these warlords are most concerned about. The value of each veCRV can actually be calculated, and holding CVX allows one to derive the current value of one CVX in terms of how many veCRV votes it represents based on the ratio of vlCVX to the total amount of CRV held by Convex. Therefore, projects can strategize based on the cost of these methods. In the long run, as long as competition exists, it will continue to drive up the prices of CRV and CVX to a balanced state.

It is worth mentioning the bribery voting platforms bribe.crv.finance and Votium. The former targets veCRV holders, while the latter targets CVX holders. Their existence is very simple; they serve as independent voting agents, collecting users' idle voting rights and distributing bribery tokens on behalf of project teams.

Who is Competing for Governance Control of Curve?

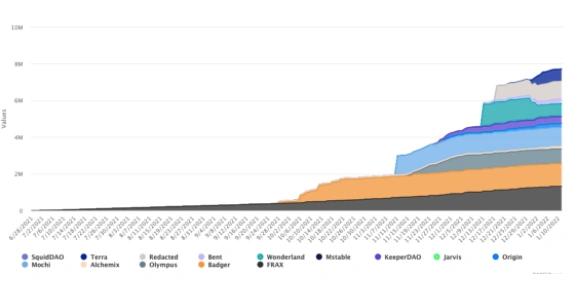

Currently, the main warlords are large algorithmic stablecoin projects, with some guerrilla teams from derivative and peripheral services continuously joining the fray. The chart below indicates that the number of participants is constantly increasing their arsenal: CVX.

Data from https://daocvx.com/

Frax/Fxs

Frax, as an established DeFi project, has finally blossomed after years of deep cultivation and is also one of the earliest projects holding continuous CVX. Frax can be said to be the most influential representative in the stablecoin field, closely tied to Convex, which has opened a special area for Frax. At the same time, FXS has also launched its own veFXS model, demonstrating a strong style both in the stablecoin field and as a participant in Curve.

Spell/Mim

Abracadabra, a yield-bearing asset stablecoin project that claims to completely defeat Maker, has its stablecoin MIM. Under the strong leadership of its founder Daniele and his Frog Nation, and leveraging the once extremely high APY of Convex, it has created the largest liquidity pool since Convex's inception ------ the MIM/3CRV pool. It can almost be said that MIM is a successful representative of establishing a foothold in this war by utilizing Curve.

UST

Terra, as a bright supernova in the Cosmos ecosystem, attempts to conquer the world with its unique stable native token ------ UST. UST is relatively unique. It is evident that Do Kwon has great ambitions, and he and Daniele have teamed up to bind two non-traditional collateralized stablecoins together. With the prosperity of the Terra ecosystem and its rising ranking, UST has gained significant financial strength to compete for the throne of stablecoins. Recent data shows they have begun to accelerate their layout in Convex, purchasing over 600,000 CVX at the start of 2022.

Ohm/Redacted

Ohm, as a non-traditional algorithmic stablecoin, currently cannot establish pegged pools on Curve for liquidity. However, the close relationship between Ohm and Frax is well-known. The Ohm community recognized the role of Curve and Convex early on and proposed increasing CVX bonds in OIP-43 to increase CVX holdings in the treasury, preparing for future competition.

With the backing of Ohm, the Redacted (BTRFLY) protocol has entered the war as an optimization strategy on top of Convex, using the Ohm mechanism to issue bonds that attract a large amount of CRV and CVX, helping users better leverage their CRV and CVX yields. They refer to Curve as L1, Convex as L2, and themselves as L3. They have successfully attracted a large amount of CRV and CVX, securing a position in the voting competition. What surprises BTRFLY will bring in the future remains to be seen.

Other key players in the war include Tokemak, Fei/Tribe, Originprotocol, Dopex, and many more. Due to space limitations, this article will not elaborate on the participants in the liquidity war, but there will be opportunities to analyze the strengths of each participant in detail.

Where will this war lead the future of Defi?

The various wars surrounding Curve have already gone through several rounds of battles, and the war has just begun to warm up. Here are some possible development directions:

- The territory of the Curve Empire will continue to expand, and the wars will become even more intense.

Curve V2 is highly likely to be the key that pushes this war into the entire Defi world. Curve V2 is an AMM trading solution for non-stablecoins. Once the permission to freely establish Factory Pools is opened, it could become a significant event that changes the course of Defi history. Because the next participants in the CRV war will not only be algorithmic stablecoin projects; all major Crypto projects will ultimately be drawn into the competition. From a game theory perspective, if project teams do not enter the battle and secure sufficient voting rights before their competitors, they risk allowing their competitors to gain more liquidity through Curve and win the war. Therefore, the foreseeable battles will become extremely intense.

Will Uniswap V3 also propose its own liquidity mining plan in the future? Will it turn into a situation where Curve is on the offensive and Uniswap is on the defensive? Currently, Uniswap V3's liquidity mining suggestions are already under construction. When these happen, what new impacts will they have on the Defi world? We will wait and see.

- The Flourishing Development of the ve Model

The ve model is profoundly influencing the governance structure of the entire Defi ecosystem. Compared to the weak governance structures of other projects, veCRV governs the most critical affairs of Defi projects ------ financial distribution in a relatively reasonable manner. Many related and new projects are attempting to ve-ify their governance rights, including FXS, which has launched veFXS to promote the integration of Frax and other Defi projects. Additionally, AC's recent proposal of ve(3,3) is also an attempt to innovate and experiment with ve. In the dark forest of blockchain, power struggles are always evolving and brutal. The whales that dominate the top of the Crypto world will certainly generate new struggles at the governance rule level. The evolution of the ve model is worth looking forward to.

- The Scene Wars of Stablecoins

Stablecoins are ultimately created to serve as anchors for other trading scenarios. The liquidity wars are merely a means to buy time for scenario expansion, with Frax representing an aggressive expansion into various trading pairs, including cross-chain and collaborations with various new trending projects like TempleDAO and Ohm. Moreover, there is currently a phenomenon of alliances among stablecoin projects. Ultimately, whoever wins the scene wars will be able to challenge the current three giants of stablecoins at their roots.

- A New Battlefield for Derivatives?

After the Dopex options protocol has attracted considerable attention, the market has shown strong interest in how the derivatives market can participate in this grand battle. It is highly likely to become a new tool for stablecoin warlords to compete for voting rights. The author will continue to track developments in this area.

Conclusion

The eternal theme in Defi is the evolution of capital efficiency. The members of the Curve ecosystem, including itself, are all leading players in enhancing capital efficiency, which underscores the importance of emphasizing this ecosystem. I hope this article can maximize the understanding of the Curverse's shape for Defi players. For more discussions on the possibilities of Curve, feel free to reach out to the author via Twitter FlynnGao.

Risk warning

Risk warning Risk warning

Risk warning