Messari: An In-Depth Analysis of the Operational Mechanism and Development Status of the Algorithmic Stablecoin Project Frax Finance

Frax Finance's governance token surged over 10 times last year, making it one of the most successful algorithmic stablecoin projects in the market. What is the reason behind this?

Frax Finance's governance token surged over 10 times last year, making it one of the most successful algorithmic stablecoin projects in the market. What is the reason behind this?Author: Ryan Malden, Messari

Original Title: "FRAX: A Fractional-Algorithmic Stablecoin"

Compiled by: Web3er Liu, Chain Catcher

DAI, created by MakerDAO (pegged 1:1 to the US dollar), can be considered one of the first and most successful stablecoins. Launched in 2017, DAI is now used throughout the DeFi ecosystem for lending services or as a treasury reserve token for projects. DAI is minted when collateral is placed into the smart contracts of the MakerDAO protocol. To add a layer of stability, MakerDAO requires DAI to be over-collateralized, which reduces DAI's capital efficiency.

Between 2018 and 2020, as more users and platforms adopted stablecoins to earn yields, many protocols utilized stablecoins to expand digital products, with DAI, USDT, and USDC becoming more common stablecoins in DeFi. However, USDC has inherent centralization risks as it relies on the US dollar, while MakerDAO's DAI is largely minted against USDC as collateral. Regardless, the adoption of MakerDAO's DAI and the platform itself has drawn attention to the necessity and growth potential of stablecoins in the Web3 ecosystem.

Before FRAX launched on the Ethereum mainnet on December 21, 2020, stablecoins were either fully collateralized (like DAI) or fully algorithmic (without collateral backing). Frax Finance first announced in May 2019 (then known as Decentral Bank) that the project was a "fractional-algorithmic stablecoin" protocol. The project was created by Sam Kazemian, Jason Huan, and Travis Moore. FRAX aims to be "the world's first decentralized stablecoin, where a portion of the supply is backed by collateral and a portion is maintained by an algorithm."

FRAX is the first stablecoin to combine fully collateralized (like MakerDAO's DAI) and fully algorithmic stablecoin design principles to create a new scalable, trustless stable on-chain currency. FRAX is pegged 1:1 to the US dollar, attempting to maintain an exchange rate of 1 FRAX = 1 USD.

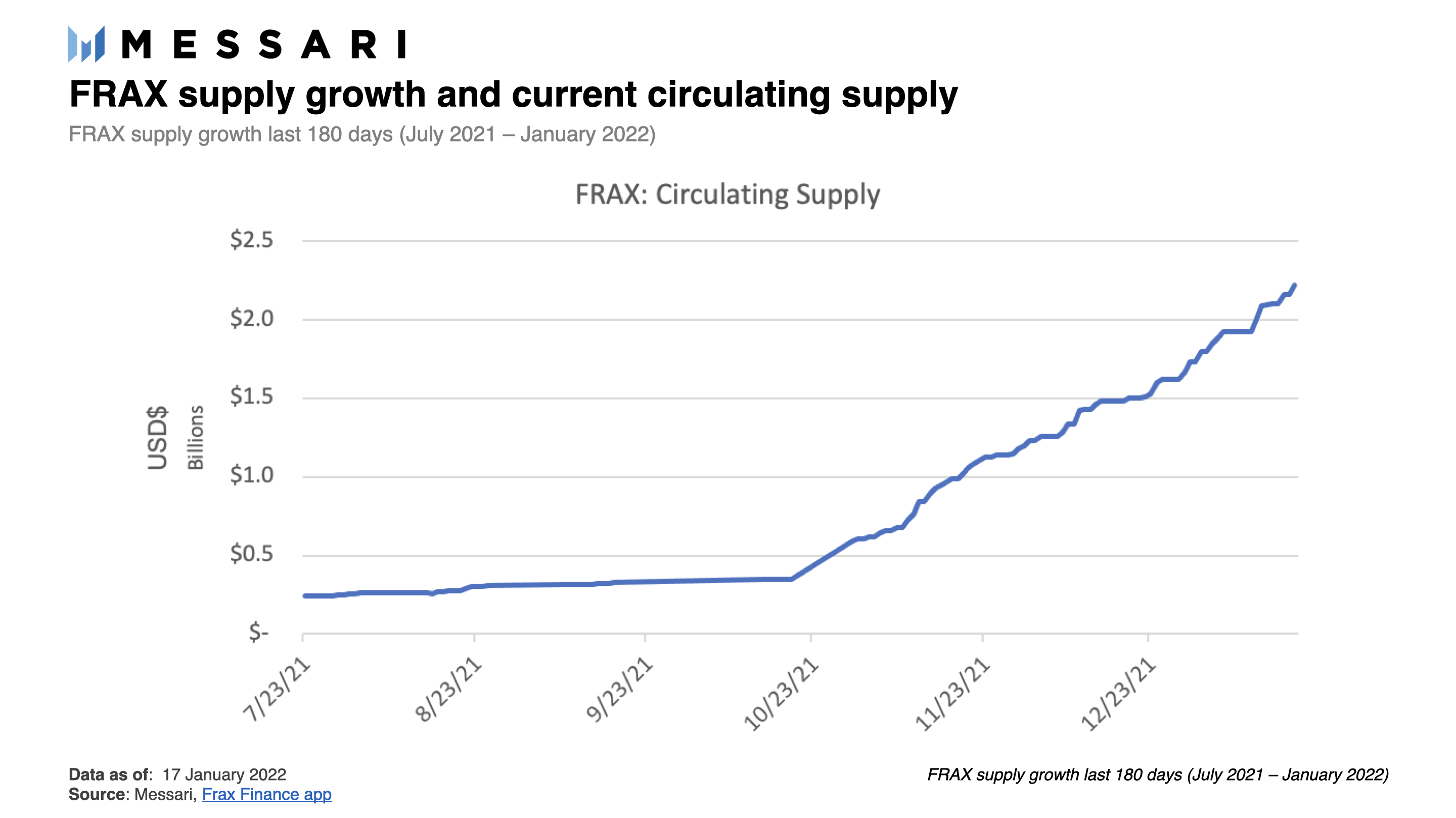

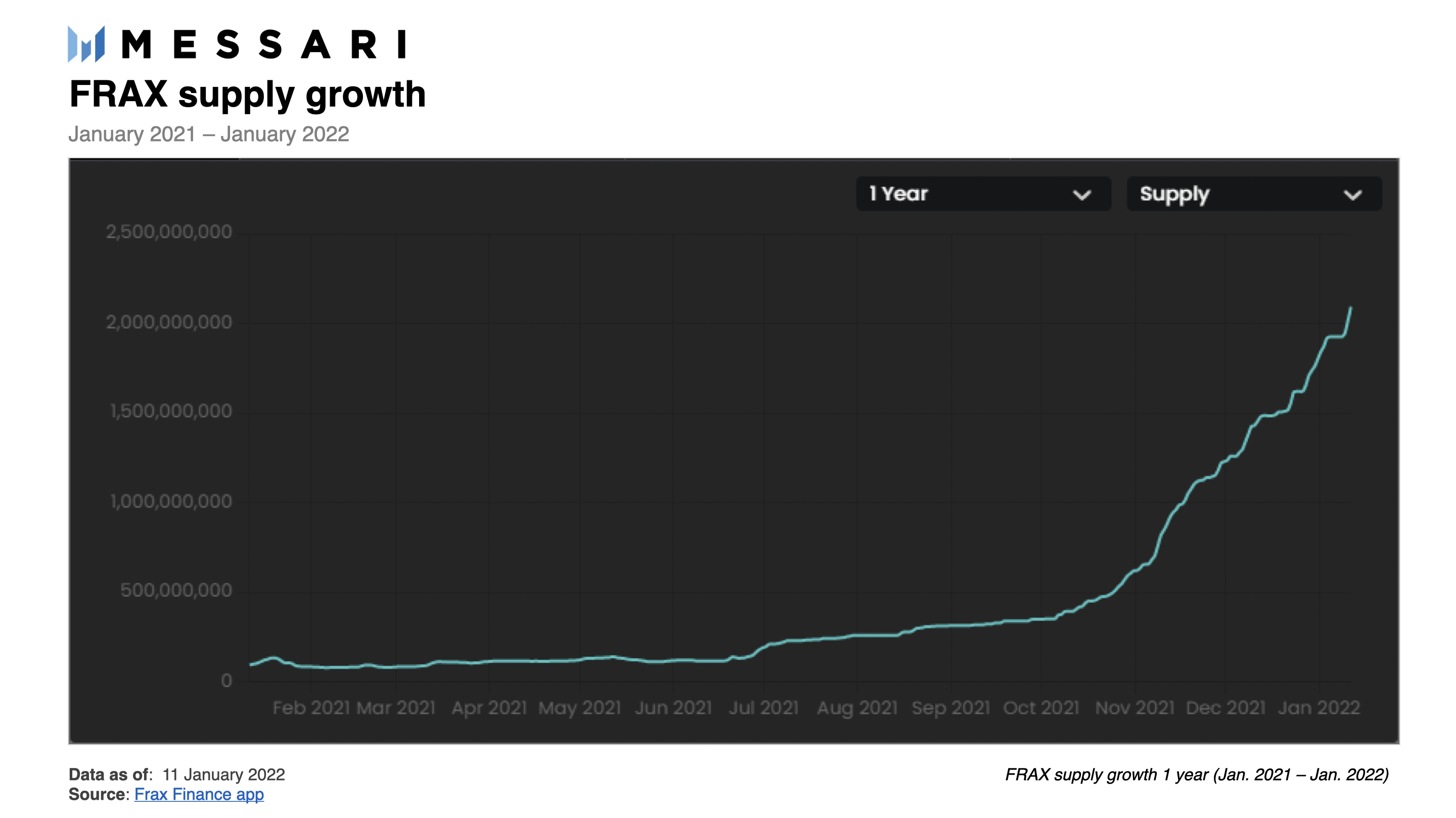

The growth of FRAX has been remarkable. In Q4 2021, with the release of Frax v2, FRAX gained massive adoption and interconnectedness within the entire DeFi system. As of January 25, the Frax project’s liquidity pool, through the AMO (Algorithmic Market Operations) launched by the team in early Q4 2021, averaged $500,000 in daily revenue (annualized at about $180 million). During the same period, the supply of FRAX surged from under $500 million to an astonishing $2.6 billion.

Understanding the Frax Protocol

In the initial phase, FRAX was 100% backed by collateral, meaning that minting FRAX tokens required only placing collateral into the minting contract. Currently, Frax is in a phase of using partial collateral, meaning that minting FRAX requires depositing appropriate collateral and FXS tokens into the Frax protocol.

While the protocol aims to accept any type of cryptocurrency as collateral, Frax will primarily accept stablecoins to maintain low volatility, facilitating a smooth transition to a phase with lower collateral ratios and higher algorithmic adoption. As FRAX evolves and the system's rate increases, incorporating unstable tokens like ETH and BTC into future protocol liquidity pools will become easier and safer.

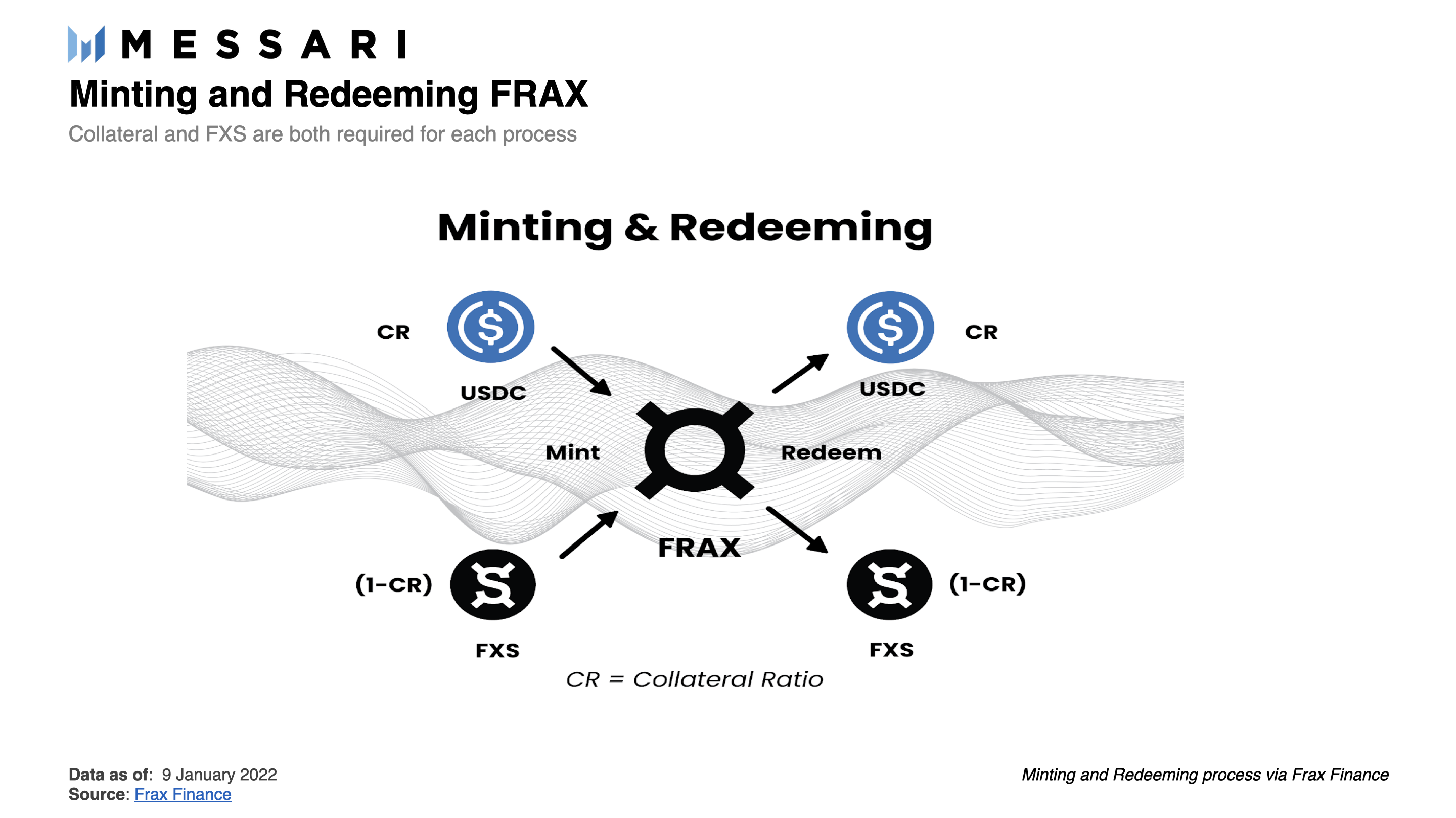

The Frax protocol implements a dual-token system: the stablecoin FRAX and the protocol governance token FXS. This dual-token system allows FRAX to be supported by both collateral and algorithms (which manage the burning and redemption of FXS). When collateral and FXS are deposited into the FRAX protocol contract, FRAX will be minted, with the amount of collateral required to mint 1 FRAX determined by the collateral ratio. The collateral ratio of the Frax protocol determines the proportion between the collateral and algorithmic mechanisms that support 1 dollar of FRAX.

For example, assuming a collateral ratio of 80%, this means that 1 dollar of FRAX is backed by 80% collateral (like USDC) and 20% by the algorithm that manages the supply of FXS. Whether minting or redeeming, the Frax protocol adheres to the collateral ratio, ensuring that every 1 dollar of FRAX is backed by 1 dollar of value.

Pegging stability is key for all stablecoins. FRAX maintains its 1:1 exchange rate with the US dollar through deep liquidity pools. The largest of these is the Curve FRAX3CRV pool. As of now, the FRAX3CRV pool contains approximately 1.3 billion FRAX, and this depth of liquidity allows FRAX to be swapped with other stablecoins with low or no slippage. As part of the Frax v2 protocol, the Curve AMO ensures the FRAX3CRV pool remains sufficiently deep by automatically supplying excess collateral and FRAX to the FRAX3CRV pool, further enhancing the stability of the FRAX token (more details in the AMO section below).

The prices of FRAX/FXS/collateral are calculated as a time-weighted average of the relevant token pairs on Uniswap and the ETH/USD price from the Chainlink oracle. The Chainlink oracle allows the protocol to access the real price of the dollar against various tokens, rather than just the average price of stablecoin asset pools on Uniswap. This keeps FRAX stable against the dollar itself, providing greater resilience, rather than merely pegging to the weighted average price of other stablecoins.

Frax is a protocol based on randomness, allowing the market to determine its collateral ratio over the long term. The Frax protocol does not attempt to estimate the market-acceptable collateral ratio; instead, it allows the collateral ratio to fluctuate, determined by the market to price each FRAX token at 1 dollar.

Token Model and Token Appreciation

The total supply of the FXS token is initially set at 100 million. As more FRAX is used in the DeFi ecosystem, the asset value of FXS holders will continue to increase, as minting FRAX requires burning FXS (thus reducing the supply of FXS and increasing the asset value for FXS holders). As the value of FXS rises, the price stability of FRAX will also increase, creating a positive feedback loop for anyone borrowing or lending FRAX for DeFi transactions.

The Frax protocol also allows investors to become liquidity providers by creating FRAX/FXS or FXS/ETH pools on Uniswap to generate token exchange fee income. The protocol has also implemented a voting escrow (ve) governance token mechanism. This mechanism is similar to Curve's veCRV governance token, with modifications made by the Frax protocol (more details below). Additionally, Frax has developed a unique protocol feature called Algorithmic Market Operations, or AMO. This mechanism further drives FXS holders to accumulate profits.

Performance Upgrades: veFXS and Frax v2 AMOs

veFXS and cvxFXS

Shortly after the project launched in 2020, FXS holders were allowed to lock their FXS tokens to generate veFXS and receive special incentives, governance rights, and profits from AMO (Algorithmic Market Operations). The ve mechanism is popular across several DeFi protocols. FXS holders are eligible to lock their FXS tokens for up to 4 years, with longer lock-up periods yielding more rewards for veFXS holders. However, it should be noted that veFXS tokens are non-transferable.

Moreover, veFXS holders can participate in the usage of the Frax weighting system, influencing or directing FXS into different Frax weighters (token pools)—similar to the mechanism of the Curve protocol and its weighting system. veFXS users can directly use FXS in one or more Frax weighters. Once all FXS is released, the weighters will influence the inflation rate of the FRAX stablecoin to continue rewarding liquidity providers.

Recently, Convex partnered with the Frax protocol to further adjust the incentive mechanisms of both protocols, particularly by locking veFXS in the CVX protocol. Before delving into this partnership, it is important to understand Convex's position in the DeFi ecosystem.

Convex launched in May 2021, aiming to create an entry point for earning CRV rewards through its native token CVX, thereby enhancing CRV incentives and simplifying the CRV lock-up process for liquidity providers and stakeholders. Consequently, Convex began actively attracting CRV and veCRV tokens upon launch. By early summer 2021, it became the largest holder of veCRV tokens in the "Curve War." Curve Finance rewards liquidity providers with CRV tokens, while governance rights over the protocol can influence CRV rewards for different token pools. By the end of 2021, Convex had established itself as a major shareholder with dominant governance rights over Curve.

As Convex is the primary owner of veCRV tokens, DeFi protocols began collaborating with Convex to gain access to governance rights and related benefits allocated to veCRV holders (who determine the CRV incentives for different token pools on Curve every 10 days).

Currently, Frax holds a 19% share of CVX, giving it strong governance rights within the Convex protocol, allowing it to be considered a representative of veCRV governance rights and guide future CRV incentive distributions.

The collaboration between Frax and Convex brings additional benefits to veFXS holders. veFXS holders can lock their veCVX in the Convex protocol in exchange for cvxFXS. The veFXS deposited at this time will be permanently locked, and the operation is irreversible. All cvxFXS holders will receive future airdrop rewards of FPI (Frax Price Index) tokens. In the future, a cvxFXS/FXS token pair will be created so that the protocol and users can exchange cvxFXS. As of now, the staking and reward mechanisms for cvxFXS are still under development and have not been finalized.

Frax v2: AMO

Frax v2 introduced the Algorithmic Market Operations module, abbreviated as AMO. AMO creates a smoother operational process for Frax by automatically managing the liquidity of FRAX and its collateral within the DeFi ecosystem. The Frax AMO automatically reallocates collateral or FRAX to capital-efficient locations based on the collateral ratio, further promoting the growth of FRAX. Frax has implemented several key AMOs: FXS 1559, Collateral Investor, Curve AMO, Uniswap v3, and FRAX lending.

FXS1559 is the internal rule that all AMOs must adhere to. The FXS1559 function calculates the excess assets in the Frax system above the collateral ratio and uses those excess assets to buy back and burn FXS. Until October 2021, FXS1559 stipulated that 50% of excess assets would be used to purchase and burn FXS (creating profits for FXS holders by reducing supply), while 50% would be directly given to veFXS holders. In October 2021, Frax passed a proposal to distribute all AMO revenues and profits to veFXS holders. This change further incentivized FXS holders to lock their FXS in the Frax protocol in exchange for veFXS rather than holding FXS.

The Collateral Investor AMO utilizes idle USDC collateral from the Frax asset pool across various DeFi protocols, such as Aave, Compound, and Yearn. This AMO will automatically lend or reclaim collateral as the collateral ratio changes. As the collateral ratio decreases and more FRAX is algorithmically supported, the Collateral Investor AMO will automatically send collateral to the aforementioned protocols, generating additional USDC revenue for veFXS holders. If the collateral ratio rises and more collateral is needed to support FRAX, the Collateral Investor AMO will act in reverse, reclaiming collateral to the Frax asset pool based on market pricing to maintain the required collateral ratio for Frax. Since its implementation, the Collateral Investor AMO has generated $63.4 million in profits for veFXS holders.

The Curve AMO transfers idle USDC collateral or new FRAX into the Curve FRAX3CRV pool to create more liquidity and anchor FRAX with other stablecoins. The FRAX3CRV pool collects trading fees, CRV, and other LP rewards (by placing CRV LP into Yearn, StakeDAO, and Convex protocols). Trading fees and LP rewards will be used to reward veFXS holders, while CRV rewards will enhance the liquidity rewards of the FRAX3CRV pool. Similar to Frax's AMO, as the collateral ratio changes, FRAX and USDC will be added to (when the collateral ratio decreases) or removed from (when the collateral ratio increases) the FRAX3CRV pool to ensure FRAX receives the appropriate proportion of collateral support.

The Uniswap v3 AMO (or liquidity AMO) utilizes FRAX and idle collateral by providing liquidity on Uniswap v3, offering liquidity for trading other stablecoins or exchanging FRAX. Since the AMO can enter any LP pool on Uniswap v3 and mint FRAX against it, the Uniswap v3 AMO can scale to other stablecoins and other more volatile collateral on Uniswap v3. The trading fees generated from the liquidity provided by the AMO can be reclaimed to reward veFXS holders. Like other AMOs, as the collateral ratio changes, FRAX and collateral can be added or reclaimed from its LP position on Uniswap v3.

The FRAX Lending AMO allows FRAX to be placed in token lending markets like Aave, enabling anyone to obtain FRAX by paying interest rather than through the basic minting mechanism. The collateral provided in these protocols will support FRAX. The mechanism used here is very similar to Maker's D3M function, where the supply of DAI expands or contracts in the lending market based on current borrowing demand. The FRAX Lending AMO carries risks, as FRAX is supported by collateral held by other protocols, but the protocol can mitigate this risk by controlling the amount of tokens entering the lending market directly.

Among these AMOs, the Collateral Investor AMO has brought the majority of profits to Frax Finance. As shown in the figure below, since its implementation in October 2021, the Collateral Investor has accumulated approximately $75 million in profits.

Currently, there are other AMOs in preparation, such as Collateral Hedge and integration with Tornado Cash. These AMOs will also adhere to the same principles that all AMOs must follow. As FRAX is adopted as a stablecoin in more DeFi protocols, AMOs may continue to evolve and iterate.

Market Overview

Frax Finance operates in the stablecoin market, which is primarily dominated by fiat-backed stablecoins like USDC and USDT. Algorithmic stablecoins have recently seen tremendous growth, particularly FRAX, whose market capitalization has increased by nearly 530% since October 2021. This trend may continue as the broader ecosystem requires stablecoin liquidity to match its scale growth, and algorithmic stablecoins like FRAX can fill this gap with their automated market operations (AMO).

However, FRAX is not the only algorithmic stablecoin intending to expand its supply in the DeFi space. Stablecoins like FEI and UST have also seen rapid growth recently, with UST's market cap hovering around $10.6 billion, while FEI's market cap grew by about 50% in the last quarter (Q4 2021). Stablecoins are evolving and growing at an astonishing rate, such as the merger of the Fei and Rari protocols, through which Fei seeks to further integrate its stablecoin FEI into the DeFi system by leveraging Rari's lending market.

Regarding algorithmic stablecoins, it is unlikely that the market will reach a "winner-takes-all" state. As the entire stablecoin market and DeFi products develop, Frax and other similar stablecoin protocols may continue to grow together. From a systemic perspective, FRAX has performed exceptionally well in maintaining its peg and has demonstrated the powerful efficiency of algorithmic stablecoins. Now, with its supply having grown and deep FRAX liquidity in place, it seems that only a catastrophic (ecosystem-wide) event could disrupt it, and both FRAX and other robust stablecoins face this risk.

Roadmap and Other Partnerships

Multichain Universe

Frax aims for interoperability across multiple chains, with no closed Frax ecosystem on any single chain. For this reason, the protocol has a bridging system that allows it to maintain close connections and interchangeability across multiple chains. Importantly, the AMO functions and FRAX weighting system can be deployed on different chains, allowing FRAX to expand into new markets and chains.

As the Frax team states: "The Frax protocol is a multichain protocol with global state consistency across all smart contracts. The FRAX + FXS tokens are a single issuance version across all networks." Each blockchain has a standardized FRAX and a standardized FXS contract, referred to as "FRAX" and "FXS." These tokens are subject to expansion or contraction by the AMO controllers, allowing users to mint or redeem.

FPI: Frax Price Index Token

On January 1, 2022, Sam Kazemian tweeted that the Frax team has been researching the Frax Price Index Token (FPI), which will enable DApps to use FPI as an asset pegged to algorithmic stablecoins. Currently, not much information has been disclosed about the FPI project, but cvxFXS holders will receive FPI airdrop rewards.

Other Recent Partnerships: OlympusDAO and Ondo Finance

There are also other partners, such as the token swap between OlympusDAO and Frax Finance (OHM <> FRAX), to "further incentivize teamwork." The OlympusDAO team has been actively building a treasury filled with DeFi tokens and stablecoins, which can be bound to their OHM tokens. This allows OlympusDAO to create a complete market for the liquidity owned by the protocol.

Another recent partner is Ondo Finance. This partnership aims to create a product that Ondo calls "Frax-as-a-Service" or FaaS. The idea is that a new protocol will be able to deposit their native tokens into the Ondo treasury, and Frax and Ondo will match the deposited assets with an equal amount of FRAX, creating a liquidity pair. This allows protocols to immediately provide liquidity for their tokens, enabling users and protocols to deposit or withdraw funds without setting up liquidity mining programs. As a participant, Frax Finance will earn a 5% annual yield on the liquidity it provides.

Conclusion

Frax allows the market to determine the collateral ratio that should match 1 dollar of FRAX, and as demand for FRAX increases, veFXS holders will be rewarded and profit from AMO market-making, fully utilizing idle collateral. While FRAX and any tokens within the Web3 finance space carry risks, the innovative experiment of the partially algorithmic stablecoin of the Frax protocol has proven to be an incredible innovation.

Stablecoins with various design principles (DAI, FRAX, MIM, UST, etc.) add value to the cryptocurrency and Web3 ecosystem as they mitigate risks within the blockchain ecosystem. With a long-term vision, FRAX and FXS aim to integrate FRAX into key DeFi protocols. The novel design of the partially algorithmic stablecoin allows for the creation and configuration of capital-efficient stablecoins, and as the entire market continues to expand, FRAX should have the capability to achieve further growth.

Risk warning

Risk warning Risk warning

Risk warning