Finance is moving towards democratization and gamification

Social media, zero-commission brokers, and "financial democratization" how they will forever change the investment world.

Social media, zero-commission brokers, and "financial democratization" how they will forever change the investment world.Original Title: "Financial Gamification"

Original Author: Joseph Politano

Original Translation: Block unicorn

In December 2014, Robinhood launched on the App Store with the mission to "democratize finance for all." The company introduced zero-commission trading and relatively low account minimums to attract users who found traditional financial institutions too expensive and cumbersome.

This gamble nearly achieved incredible success—within two years, Robinhood's valuation surpassed $1 billion, forcing other brokers to significantly lower their commissions to compete. Today, Robinhood has over 22 million funded accounts and nearly 19 million monthly active users.

With the increase in social media usage and access to the financial world, investment and trading communities have sprung up across various social media networks: Fintwit (Financial Twitter), content creators on YouTube, and now-famous Reddit communities (like the WallStreetBets retail investor community).

People share investment ideas, discuss recent market trends, and post their incredible gains or devastating losses. The rise of the crypto economy has also fueled speculative enthusiasm across the digital community, with business moguls like Elon Musk becoming social media stars.

The pandemic led to extreme market changes while leaving many feeling bored, lonely, and with too much time on their hands, which only accelerated the development of online financial communities.

All of this peaked in January 2021 when the struggling video game retailer GameStop became the center of attention in the financial world. The story goes that hedge funds shorted the stock—borrowing shares and immediately selling them, betting that GameStop's stock price would decline.

Users on WallStreetBets saw the extremely high level of short interest (the number of shares sold short exceeding the number of shares available) as an opportunity. If they could drive up GameStop's stock price, short sellers would have to buy back at a higher price to cover their positions, leading to significant losses. Thus, they began buying up GameStop shares en masse, causing its price to soar while Wall Street hedge funds were betting against the company.

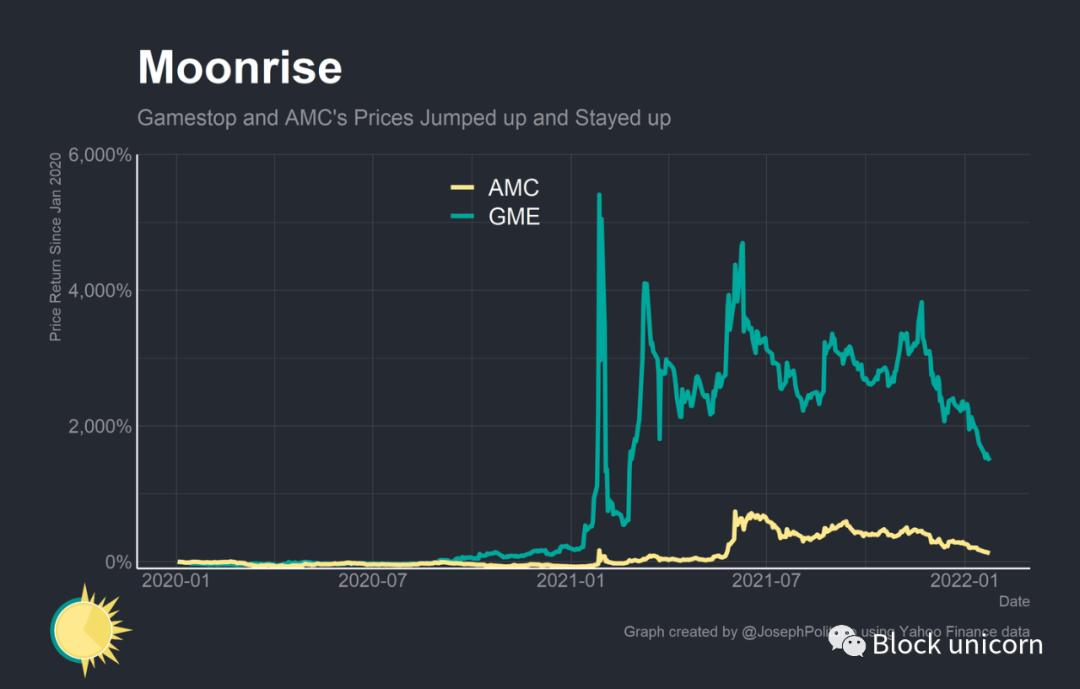

GameStop's stock price skyrocketed from $20 before the squeeze to nearly $500, and after its success, traders turned to other stocks with high short interest (like the struggling cinema company AMC). This continued until Robinhood and other brokers completely halted trading on GameStop, AMC, and several other "meme stocks"—effectively cutting off the momentum of the meme frenzy.

But this is just one story— to tell the story of this story, we must start from the beginning.

Financial Democratization

"Due to the impact of attention on buying and selling behavior, the technological advantage that allows investors to unite through easy-to-use apps seems to make profitable day trading more difficult rather than easier."

For the vast majority, trading is a money-losing proposition. Decades of academic research show that retail investors trying to pick their own stocks lag behind risk-adjusted benchmark indices, while those who trade frequently perform even worse. This should not be surprising—professional fund managers have consistently underperformed the indices, so why would ordinary people be able to beat the market?

The essence of the efficient market hypothesis is that, since asset prices reflect all relevant available information, investors cannot achieve reliable alpha (alpha refers to obtaining above-average returns).

Real-world markets cannot be perfectly efficient, but they are close enough that it is usually difficult to achieve alpha. Those who outperform major indices often do so because they take on additional risk (like Warren Buffett's value investing), uncover new information (like Renaissance Technologies' famous Medallion Fund), or simply get lucky.

Robinhood emerged at a time when low-cost passive index funds were sweeping through the financial world. The relatively poor performance of expensive actively managed funds, coupled with the rise of low-cost index fund providers like Vanguard, led to trillions of dollars in everyday retirement savings flowing into index funds.

Robinhood's mission was to break down the last barrier for ordinary people in the financial world: high trading costs and the difficulty of opening brokerage accounts. Traditional brokerage firms were uninterested in managing millions of accounts of $500 each, focusing instead on a small number of high-net-worth individuals. Many brokerage firms were clunky, charging high fees per trade, making them inaccessible to young, tech-savvy, and low-net-worth users.

"A large part of the appeal isn't that 'finance is fun,' but that trading stocks or cryptocurrencies seems like an easy way to make money. Clearly, I don't think that's true." Srivatsan Prakash (host of the Market Champions podcast)

However, bringing brokerage services to smartphones began to undermine the trend toward passive investing, as those trading on their phones were more likely to buy riskier, popular, and lottery-like assets. They were also more likely to chase past returns, succumbing to the well-known behavioral biases that hinder investor performance.

These effects may not be temporary—investors who started trading via phone began to exhibit similar behaviors on other platforms. Robinhood currently has 18.9 million monthly active users among 22.4 million total funded accounts, meaning most users frequently check their accounts—which also diminishes long-term returns. For many, active trading began to seem increasingly attractive—they could get rich quickly this way.

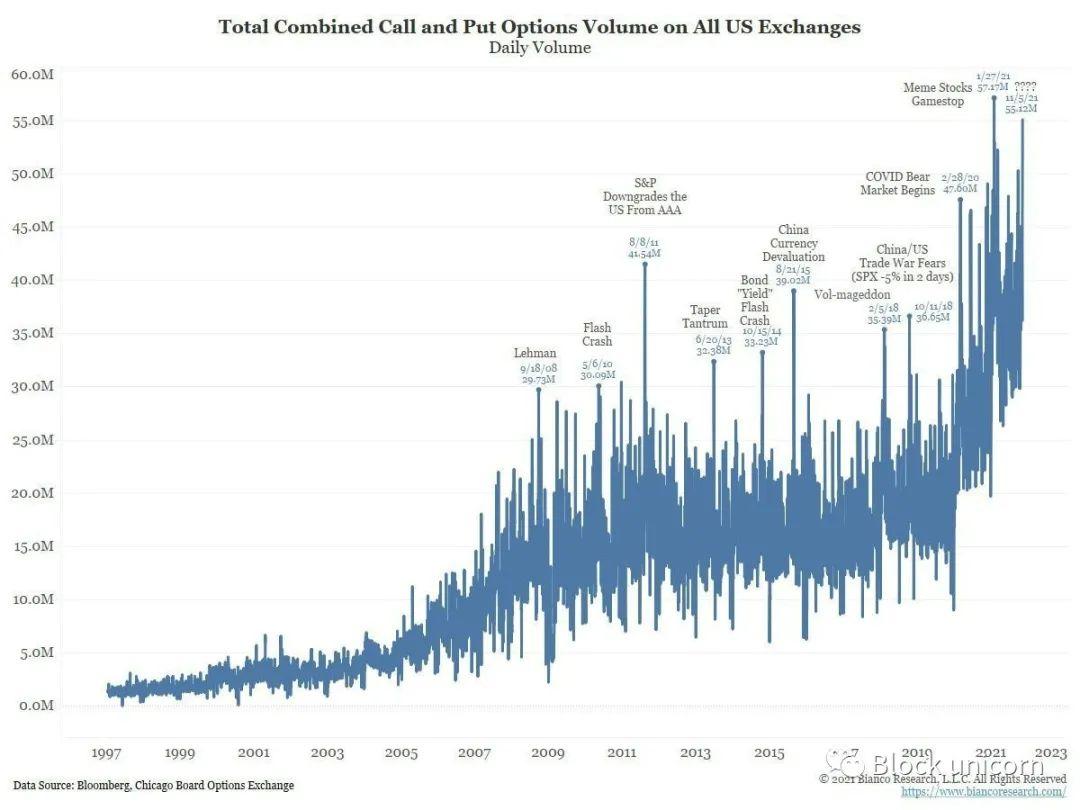

Over time, users of zero-cost brokers began to shift toward riskier, more volatile financial products. Put options and call options, typically used for hedging, were increasingly employed by retail traders to leverage bets on the movements of different stocks. The already turbulent cryptocurrency market saw an explosive growth of meme coins.

Crucially, Robinhood earns part of its revenue through payment for order flow (PFOF), where market makers compensate brokers based on how they guide trades. This process is legal, improves upon the high trading fees of past eras, and may be cheaper for users than other options.

But it still incentivizes Robinhood to encourage users to trade as frequently as possible and to trade riskier, less liquid assets that market makers are willing to pay more to trade. In the last quarter (Q4 2021), $164 million of Robinhood's transaction-based revenue came from options, another $51 million from cryptocurrencies, and $50 million from regular stocks.

The Meme of Finance

"Society has always been a meme war, but before it was fought with sticks and stones. However, the internet has undergone an arms race, trench warfare with meme-driven brains in many areas. They haven't captured all the fields of thought yet, but I'm worried that the meme gap will only widen."

CGP Grey, meme commentator. CGP Grey is an educational YouTuber with over 5.2 million subscribers.

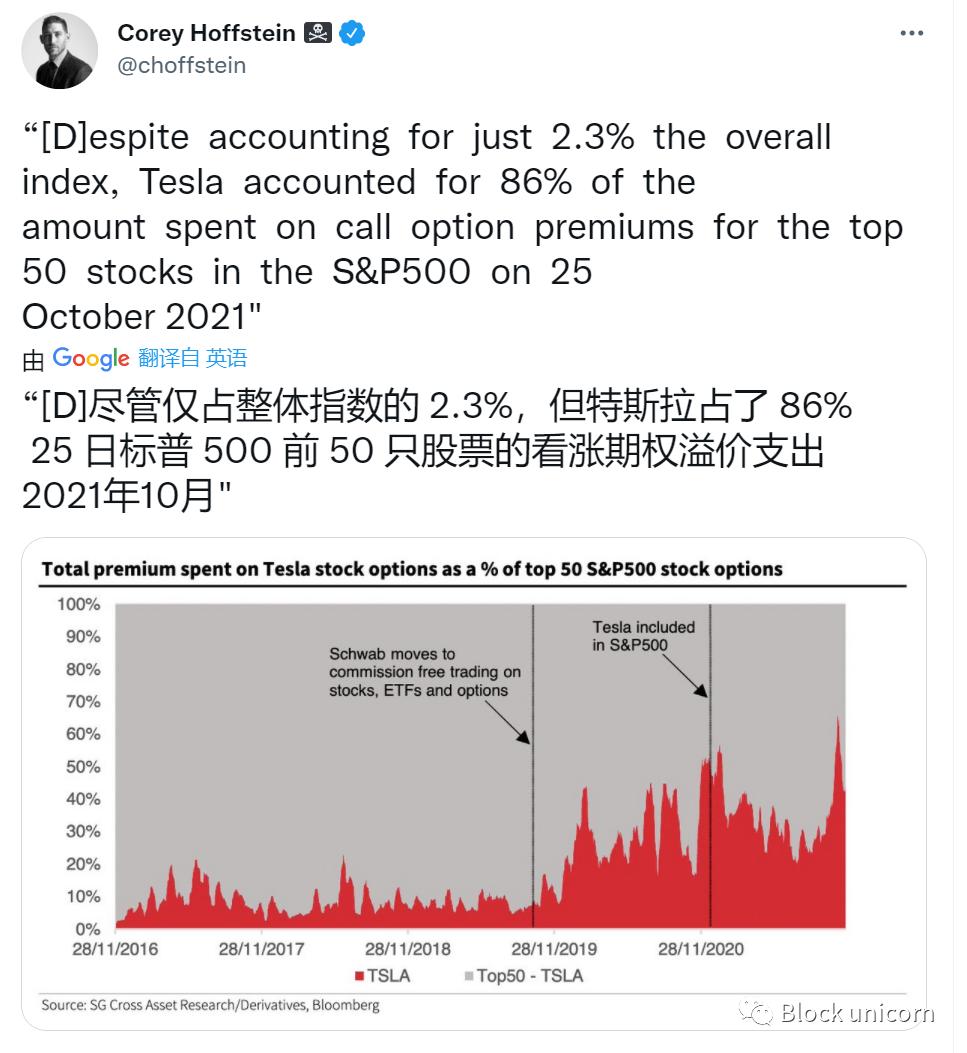

With the rise of retail investing and the popularity of social media, corporate executives and well-known investors have become social media stars (to a lesser extent, vice versa). Elon Musk, the Technoking of Tesla (Techno is a genre of electronic music, and this is his official title), is undoubtedly the biggest star in the world of financial social media, boasting an astonishing 71 million Twitter followers.

"The way finance works now is that the value of things is not based on their cash flow but on how close they are to Elon Musk."

Matt Levine (valuation analyst) on Elon Musk's market hypothesis

Elon's social media status has made him a market mover across the traditional and crypto financial worlds, with his tweets about GameStop, Dogecoin, Bitcoin, and his own company Tesla eliciting huge, immediate reactions in the financial markets. Many crypto projects were created with the explicit intent of riding the coattails of Elon on Twitter, while other public company CEOs tried to associate themselves with Elon’s social media fame as much as possible.

Elon Musk leveraged his social media fame to attract a highly loyal base of retail investors, using these loyal retail investors to achieve commercial success in a virtuous cycle. Tesla is now a company valued at nearly $1 trillion, but it has a very high price-to-earnings ratio of about 270.

In contrast, at the time of writing, Apple's price-to-earnings ratio is a mere 28, making Tesla a highly competitive company relative to profitable companies. This partly reflects high growth expectations, but it also reflects Elon’s unique ability to attract retail investor capital at sky-high valuations.

Tesla's stock price surged after a capital raise in December 2020, as the company raised funds at a valuation higher than today for the third time that year. Elon was able to use this cheap capital to rapidly scale actual production and leverage his social media fame to enhance Tesla's brand image and visibility.

Retail traders were emotionally invested in Tesla's success, thanks to their quasi-social relationship with Elon Musk (i.e., the one-sided relationship between media users and media figures). Their emotional connection made them stickier investors, willing to buy Tesla stock at high valuations.

Seeing this, other corporate executives and fund managers began to build their own social media followings. Michael Saylor of Microstrategy Inc built a following based on his company's Bitcoin purchases.

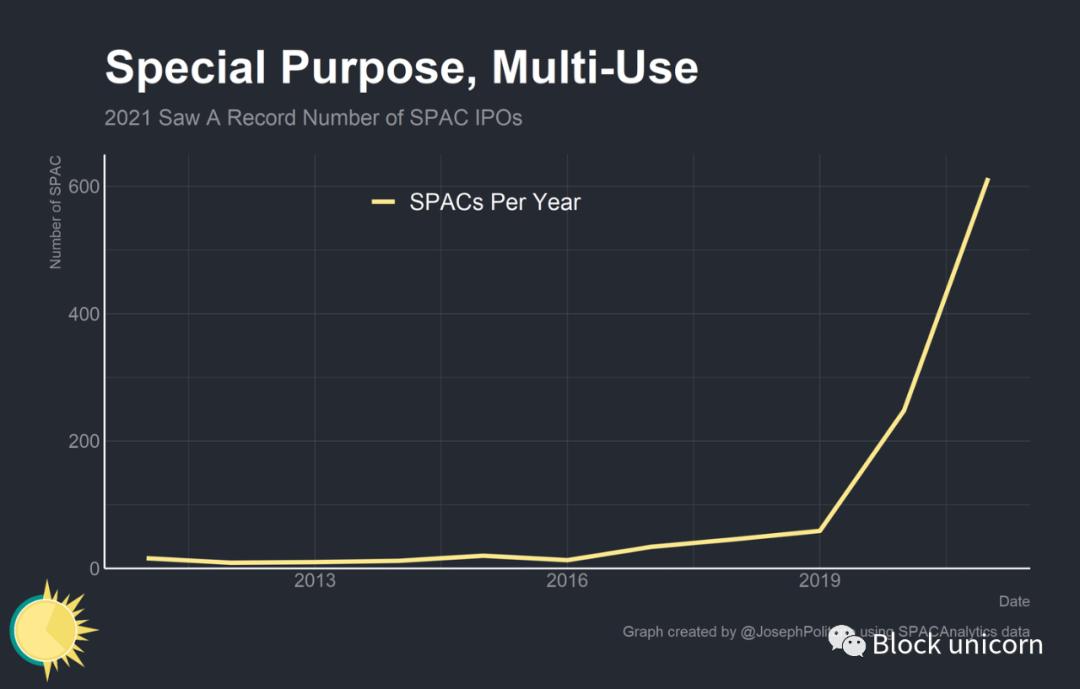

Cathie Wood (Wood's sister) built a following based on her "disruptive" investment fund, while Chamath Palihapitiya (CEO of Social Capital) built a following by taking private tech companies public through special purpose acquisition companies (SPACs).

"As young people, part of our reaction to memes is everything, so if this really becomes an investment style, I wouldn't be surprised." Kyla Scanlon (Twitter KOL)

The beauty and curse of social media is its ability to create narrative communities and quasi-social relationships. Humans are narrative, social, and tribal beings; we form communities based on in-groups and out-groups and learn from the stories told by members of our groups.

Memes are not just funny images; they are brief expressions of any complex idea that can be shared, imitated, and adapted—they are the lifeblood of narrative communication on the internet.

An effective meme defines an in-group and an out-group simply by who gets the joke (thus social media content delivery algorithms will show this joke to whom) and conveys complex ideas through familiar templates (think of how many people use the famous "Distracted Boyfriend meme" to comment on various situations).

Consider the recent crypto memes WAGMI (We All Gonna Make It) and NGMI (Not Gonna Make It). They clearly define an in-group ("we" who invest in cryptocurrencies or specific coins/projects) and an out-group ("you" who do not invest), telling narrative stories about both groups (whether you will achieve financial or social success based on their relationship with the coin/project, implying that future value will significantly increase).

The narratives of social media are the foundation for the explosive growth of SPAC usage in recent years. In a SPAC, a shell company is listed on a stock exchange to raise funds for a merger or acquisition of a private company. SPACs concentrate the characteristics and purposes of various financial products, including direct listings, overseas acquisitions, reverse mergers, and private placements.

They launch without a real subsidiary and must find a target for acquisition, relying on investors' trust in the SPAC founders to raise funds.

In the age of social media, those with large loyal digital followings (like Chamath Palihapitiya) can leverage their quasi-social relationships with fans to raise substantial funds for SPACs based solely on ideas and narratives.

Online communities form through the constant exposure to memes conveying similar narratives. Eventually, they begin to self-catalyze. Memes become increasingly popular, prompting previously uninterested individuals to engage with the community.

These individuals become firm believers in the core principles defining the community and begin to create and share more memes. These memes persuade more previously uninterested people to participate, and the cycle begins anew. This brings us back to GameStop and WallStreetBets.

Financial Gamification

Due to COVID causing unprecedented volatility in the stock market, and high-income individuals having time and money on their hands, WallStreetBets saw a sharp expansion in the early days of the pandemic.

It should not be forgotten that the subreddit also attracted many desperate individuals looking for ways to improve their financial situation, as well as many seeking community awareness after losing social interaction during the pandemic. The subreddit became notorious for traders who bet everything on risky trades, either winning large sums of money or (more likely) losing it all.

"Our brains are still adapting to this online space, and they process loneliness through the function of 'dude, all I'm doing is talking to people on Zoom all day.'" Cool Scanlon

In late 2020 and early 2021, a portion of Reddit's WallStreetBets community began to focus on GameStop. The company seemed to be making significant changes to its organization and strategy to address years of declining profits, and users of WallStreetBets (the retail investor community) saw the company's record short interest as an opportunity. They began injecting funds into the company's stock, attempting to squeeze the short sellers, and the rest is history.

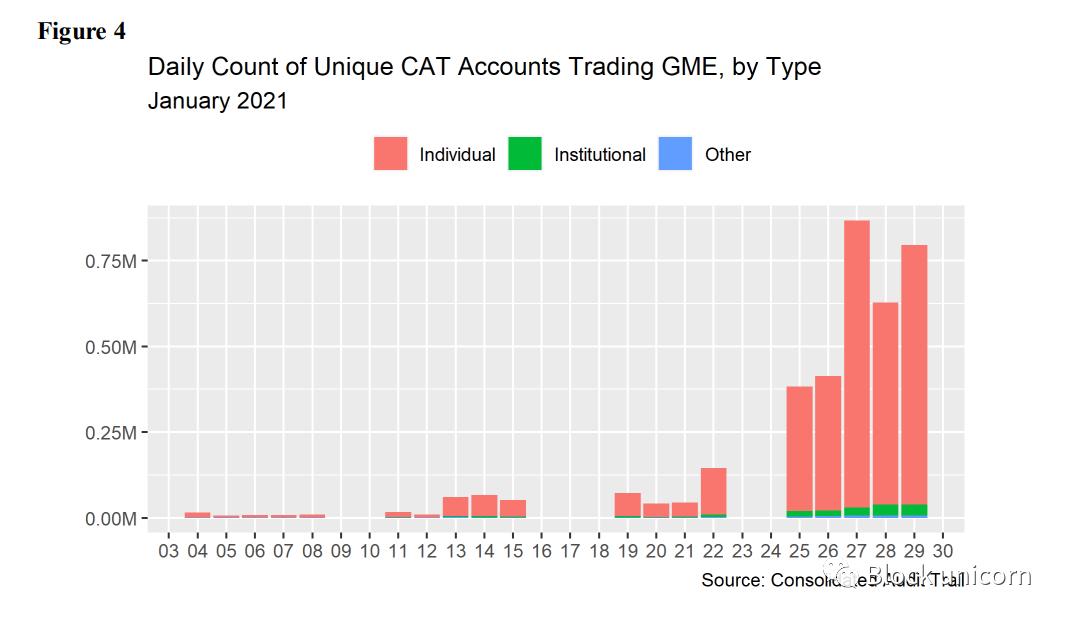

At the height of the frenzy, over 750,000 individual accounts were trading GameStop, drawing in the narrative (meme) that they were sticking it to the hedge funds by buying shares. If retail traders could push the price high enough, they could take down Wall Street's suits while making themselves rich.

This meme started with WallStreetBets but quickly spread: first to the rest of Reddit, then to Twitter and other social media platforms, then to television and mainstream media, and finally to the dinner tables of millions of Americans, and ultimately to the halls of Congress and the White House.

Social media influencers like Elon Musk further spread this meme, amplifying its impact by attaching their influence to the frenzy, which spread to other stocks—AMC, Blackberry, and other struggling retailers with high short interest.

"Whether driven by the desire to squeeze short sellers and profit from rising prices or by a belief in GameStop's fundamentals, what sustained the price for weeks was positive sentiment, not buying to cover GameStop stock appreciation." SEC staff report on the state of the stock and options market structure in early 2021

The beauty of social media is its ability to create narrative communities and quasi-social relationships. The curse of social media is that these narratives do not necessarily have to be fact-based, and these communities can be led astray by groupthink dynamics both within and outside the group.

The GameStop saga defined a clear in-group—an online community of forgotten ordinary Americans—and a clear out-group—the Wall Street suits that had drained the country. It established a clear narrative: by buying GameStop stock, you were sticking it to the hedge fund out-group and enriching the online in-group, and this meme led to GameStop's price exploding many shorts.

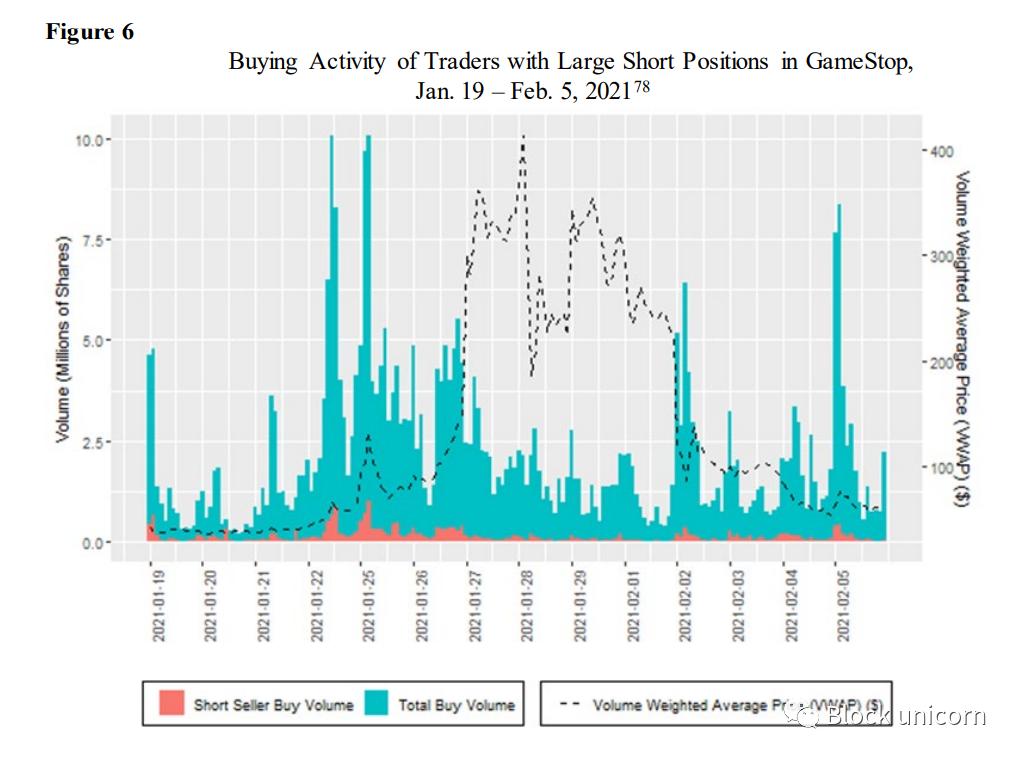

In fact, a report from the Securities and Exchange Commission (SEC) released after the GameStop incident showed that the buying volume from short sellers accounted for a small portion of total buying volume, and most short sellers had already capitulated long before GameStop reached its peak price. With additional pushes from some institutions, retail (individual) buying drove GameStop's stock price to historic highs.

The short squeeze was not the driving force behind GameStop's price increase; rather, it was the massive influx of retail funds that pushed the stock price up. Crucially, the sustained interest from retail traders kept GameStop's stock price so high—at the time of writing, the company's trading price is four times the pre-frenzy level and nearly twenty times the pre-pandemic level.

"One of the main drivers of the GameStop squeeze was the massive buying of call options, which led market makers to buy the underlying stock to hedge their call option holdings, thereby pushing the stock price up.

While staff did observe a significant increase in individual customer GME options trading volume, from $58.5 million on January 21 to $563.4 million on January 22, peaking at $2.4 billion on January 27, the increase in options trading volume was primarily driven by the purchase of put options, not call options.

Additionally, data shows that market makers were buying rather than selling call options, which is inconsistent with the GameStop squeeze." SEC staff report on the state of the stock and options market structure in early 2021

Just to dispel other myths, the GameStop squeeze was not the cause of the GameStop frenzy. The GameStop squeeze is slightly more complex than a short squeeze, but essentially involves traders buying call options (betting that the price of the underlying asset will rise), which forces market makers to buy the underlying asset to hedge the call options they wrote.

In buying the underlying asset, market makers push the price up, so retail traders buying enough call options can drive the price higher. This would force short sellers to buy the underlying asset to hedge their positions, thereby pushing the price up. However, retail traders were net buyers of put options, while market makers were net buyers of call options—this situation is inconsistent with the GameStop squeeze.

Finally, hedge funds or other financial institutions did not conspire to undermine the GameStop saga. When Robinhood and other brokers halted trading on the meme (here referring to GameStop) stock, it was not to protect the bottom line of financial institutions suffering losses from the squeeze.

Instead, extreme volatility forced clearinghouses to require Robinhood to post large deposits to cover the settlement period for meme stock trades. The deposit amount was ten times Robinhood's normal level, which the company simply could not pay immediately.

"When naked short selling occurs, the seller fails to deliver the securities to the buyer, and staff did observe a peak in GME failures to deliver. However, both short and long sales can experience failures to deliver, making it an imperfect measure of naked short selling. Additionally, based on staff's review of available data, GME did not experience persistent failures to deliver at the individual clearing member level.

Specifically, staff observed that most clearing members were able to clear any failures relatively quickly, that is, within days, and that most did not experience failures lasting multiple days." SEC staff report on the state of the stock and options market structure in early 2021

There was also no conspiracy surrounding failures to deliver; failures to deliver occur when one party in a trade contract fails to fulfill its obligations, and the conspiracy surrounding GameStop is that short sellers failed to deliver when they closed their positions, partially undermining the short squeeze. However, the vast majority of failures to deliver issues were quickly resolved, and after the initial market turmoil, failures to deliver sharply declined.

It seems a lot of ink has been spilled to debunk some of the erroneous theories surrounding the GameStop frenzy, but it is necessary to dispel the prevalent narrative that fundamentally misrepresents the entire situation.

The GameStop saga is not about short selling or sticking it to Wall Street—it is about millions of people being persuaded by a meme on the internet to gamble their meager funds on the stock of a dying video game retailer. Wall Street won because, despite a few hedge funds suffering massive losses, brokers, market makers, asset management firms, and other large financial institutions profited handsomely from the surge in trading volume. Retail investors lost due to the increased trading volume—lowering their returns—and were drawn into highly risky assets by the social media hype.

Ultimately, it is people's perceptions that matter, not the actual facts. As long as people believe this is "the retail versus institutional battle," they will not think too much about the facts.

Srivatsan Prakash

Crucially, the story of GameStop did not end when it faded from public view in early 2021. By January 2021, WallStreetBets had fewer than 2 million subscribers, which has since grown to nearly 12 million subscribers. The subreddits for GameStop and AMC, "Superstonk" and "AMCstock," have seen their subscriber counts rise to 730,000 and 450,000, respectively.

Their front pages often feature posts predicting a total collapse of the financial markets, the mother of all short squeezes (MOASS—another meme), and rapid increases in GameStop/AMC stock prices. They frequently promote conspiracy theories about financial firms, the Federal Reserve, and media organizations.

It is this highly focused niche internet community and the memes it believes in that keep GameStop's stock price elevated. Crucially, they are a community of loners—there have been discussion threads where Superstonk even collectively donated over $100,000 to the charity Toys for Tots this winter.

When WallStreetBets' subscribers nearly overnight increased from 2 million to 9 million, most new subscribers did not realize what was right and what was wrong. They came from Twitter or Instagram, often inspired by meme pages or their friends. These are the people I worry about.

Taylor Shiroff

Fundamentally, these individuals are victims of self-catalyzing, isolated internet communities, where users encourage each other to gamble on extremely speculative investments to their detriment.

Conclusion

"The market is no longer driven by fundamentals but by memes. It is no longer a metaphor but a living structure—the market." Kyla Scanlon

Many believe that a single event—such as a market crash, economic recession, or the end of the pandemic—will bring the meme trading frenzy to an end, but I fundamentally disagree. The primary driving force behind meme trading is the sociological power brought about by the social media age and the increased access to financial markets.

These processes have been accelerated by the economic forces of the pandemic era but began before the pandemic emerged. As the digital age progresses, corporate social media stars, online trading communities, and increasing access to financial services will become increasingly important. The meme trading frenzy will not disappear; it will simply shift from asset to asset, from platform to platform, seeking another narrative to latch onto. Even the memes themselves are dedicated to drawing traders into the frenzy.

"HODL" (Hold On for Dear Life) and "Diamond Hands" (those who sell only when they achieve their target returns) are both very popular memes, and despite their volatile value, they still hold financial assets. When those with quasi-social relationships with you and the online communities you frequent are constantly encouraging you to trade, it can be very difficult to exit.

I also do not believe that the meme stock frenzy fundamentally undermined the normal functioning of the entire financial market, although there is evidence that Robinhood day traders caused additional volatility in the stock codes they focused on, retail traders account for only a small portion of total trading volume.

Despite margin debt being at historical highs, it still represents a normal proportion of overall market value. The primary victims of the retail trading frenzy are the traders themselves, who may suffer lower returns due to their trading behavior.

"Consider whether gamified features and celebratory animations that may be designed to generate positive feedback from trading lead investors to trade more. Additionally, payment for order flow and the incentives it creates may prompt brokerage firms to find new ways to increase customer trading, including through the use of digital engagement practices." SEC staff report on the state of the stock and options market structure in early 2021

This retail trading frenzy has two main beneficiaries. First, financial institutions are deploying behavioral nudges and gamification to encourage their user base to trade more. Every trade a retail investor makes puts more money in their pockets; the riskier the trade, the more they earn.

The second beneficiary is those shaping the narratives on social media—due to a lack of better terminology—who create memes. Their ability to direct retail investor funds will become an increasingly important part of future corporate and fund strategies. The quasi-social relationships they build with their audiences give them a unique ability to leverage cheap capital to influence outcomes in the real economy—while enriching themselves.

In the age of social media, it is important to remember that you cannot escape propaganda. In this case, propaganda does not just mean political campaigns but any information that promotes a specific narrative.

The narratives formed on Twitter or Facebook may not be a top-down strategy for shaping public opinion, but the information flow from content delivery algorithms still shapes and is shaped by the viewpoints of its users—regardless of whether those viewpoints are accurate. Some memes are harmless, but others are deadly—in the fiercely competitive attention economy, it is becoming increasingly difficult to distinguish between the two.

The natural tribalism of human thought means that propaganda in the social media age is created in an extremely decentralized manner. There are millions of small communities with their own in-groups and out-groups, competing with each other to control the narrative. All social media influencers—yes, that includes me—have biases, flaws, and incentives that make them imperfectly trustworthy institutions. The only way to stay safe in the modern age is to confront your biases and sensitivities while continually challenging your sources of information.

The information provided in this article is for general guidance and informational purposes only. The content of this article should not be construed as investment, business, legal, or tax advice under any circumstances. We accept no responsibility for personal decisions made based on this article.

We strongly encourage you to conduct your own research before taking any action. While every effort has been made to ensure that all information provided here is accurate and up to date, omissions or errors may occur.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles