Is Solidly the new old story?

Is Solidly still a continuation of Curve and Olympus?

Is Solidly still a continuation of Curve and Olympus?Original Title: “Solidly: A New Bottle for Old Wine?”

Author: Sally Gu, IOSG Ventures

For a long time, a significant issue with the traditional AMM model has been the conflict between the protocol platform and LPs. This is because the yield for LPs does not actually correlate with the amount of liquidity provided. The depreciation of the market value of tokens issued by the protocol and the impermanent loss incurred by trading pairs during market fluctuations can expose LPs to the risk of "mining collapse." To address this zero-sum situation where the interests of the protocol and market participants are inversely related, Yearn's founder AC (Andrew Cronje) collaborated with Dani (Daniele Sestagalli), the founder of the well-known crypto community Frog Nation, to launch a new DeFi 2.0 protocol project called "Solidly," which quickly sparked a wave of discussion in the crypto community.

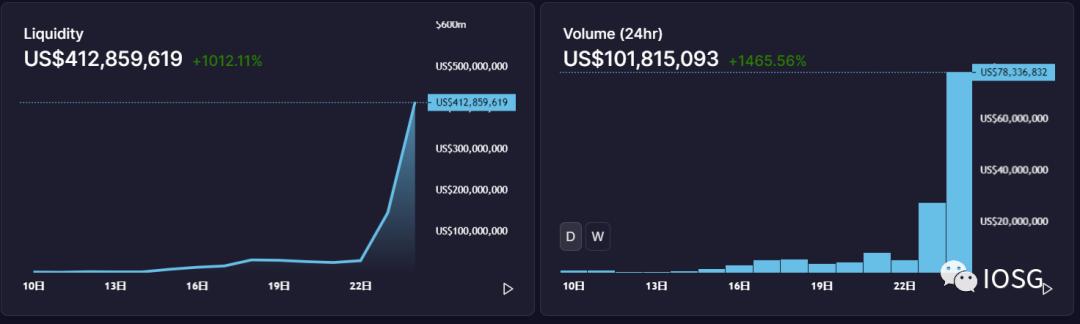

As of today, Solidly's TVL has exceeded $400 million, with a 24-hour trading volume increase of over 1300%. As more and more attention turns to this new protocol, we will deconstruct it in this article from the perspectives of its protocol mechanism and the vampire wars it has triggered.

Source: https://solidly.dev/home

Source: https://solidly.dev/home

What is Solidly: ve+(3,3)

The original form of Solidly is based on a new type of DEX project called ve(3,3) created by AC. Simply put, ve(3,3) is an economic structure based on Curve's veCRV, integrated with Olympus's (3,3) game theory, and optimized to create a token distribution mechanism.

veCRV: Voting <-> Liquidity

veCRV is a new type of token economic model created by Curve, and to understand it, one must first have a basic understanding of Curve. Curve is a DEX that uses the AMM model primarily targeting large-scale stablecoins, thus requiring LPs to provide trading pairs. In return, Curve rewards LPs with its CRV tokens and 50% of the platform's trading fees.

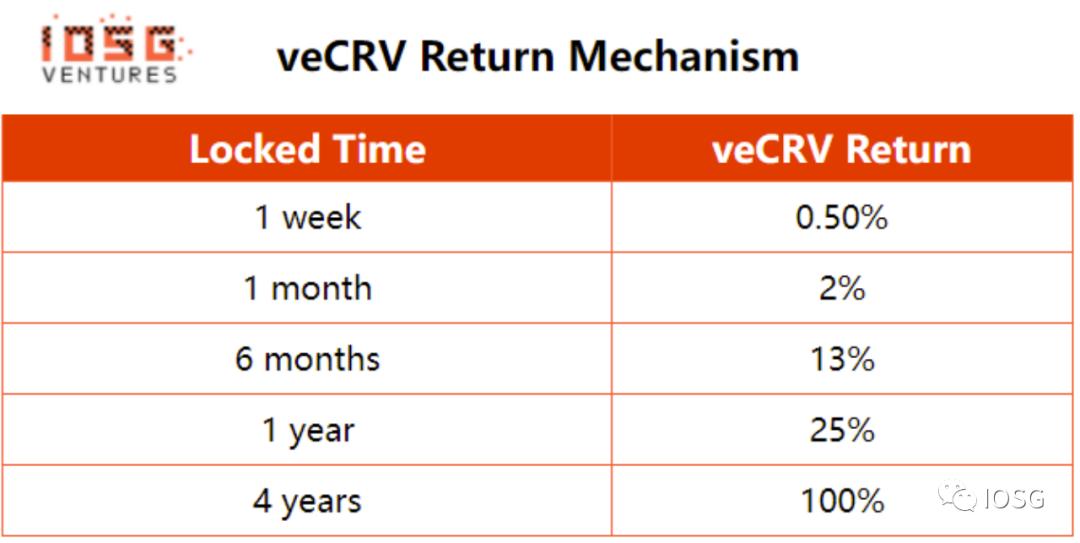

After receiving CRV, LPs can choose to stake the tokens on the platform (with a maximum lock-up period of 4 years), and the platform will return veCRV (ve: voting escrow) as proof of rights. The longer the lock-up period, the more veCRV is returned. We can think of this staking operation as purchasing equity in Curve; holding veCRV means holding equity. Long-term lock-up represents a deep trust in the platform, and the platform is naturally willing to reward loyal shareholders who hold for the long term rather than short-term speculators who only want to "mine, withdraw, and sell."

veCRV: Voting <-> Liquidity

veCRV is a new type of token economic model created by Curve, and to understand it, one must first have a basic understanding of Curve. Curve is a DEX that uses the AMM model primarily targeting large-scale stablecoins, thus requiring LPs to provide trading pairs. In return, Curve rewards LPs with its CRV tokens and 50% of the platform's trading fees.

After receiving CRV, LPs can choose to stake the tokens on the platform (with a maximum lock-up period of 4 years), and the platform will return veCRV (ve: voting escrow) as proof of rights. The longer the lock-up period, the more veCRV is returned. We can think of this staking operation as purchasing equity in Curve; holding veCRV means holding equity. Long-term lock-up represents a deep trust in the platform. The platform is naturally willing to reward loyal shareholders who hold for the long term rather than short-term speculators who only want to "mine, withdraw, and sell."

Source: IOSG Ventures

The Lock-up Reward Mechanism of veCRV

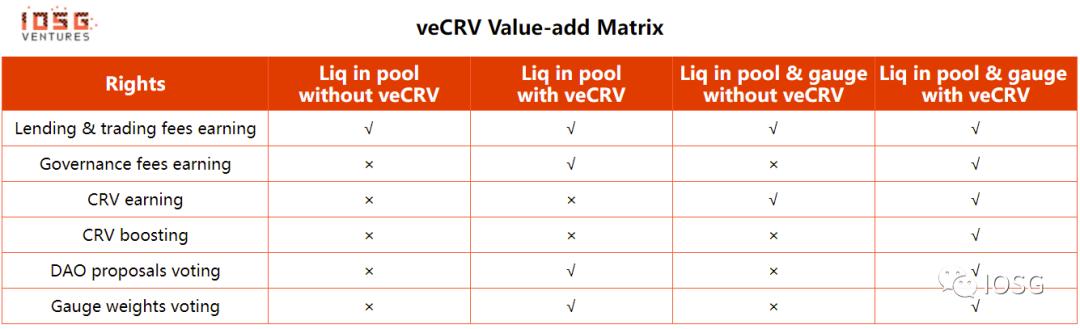

At the same time, holders of veCRV also have the right to vote on the distribution of rewards from the pool. This design is one of the most praised aspects of the ve model: incentivizing liquidity through voting. What we often hear about as the Curve war is actually a competition for the allocation of voting power. Because veCRV holders can vote to help their pools obtain a larger share of reward distributions. An increase in reward shares inevitably leads to more LPs entering, and with sufficient LP backing, the trading experience of the pool improves, and trading fees rise accordingly. In this positive cycle, veCRV holders can continue to benefit.

veCRV Reward Matrix (https://resources.curve.fi/faq/vote-locking-boost)

Current Defects of the veCRV Mechanism

However, the veCRV model is not without its flaws.

On one hand, the continuous issuance of CRV will dilute users' equity. As the equity share decreases, the value that veCRV holders can obtain will gradually diminish.

On the other hand, since veCRV is directly tied to the LP address, this proof of rights is non-transferable or tradable. The 50% trading fee as a reward is directly distributed to veCRV holders in proportion. Therefore, this greatly limits liquidity.

(3,3): Lock-up → Nash Equilibrium

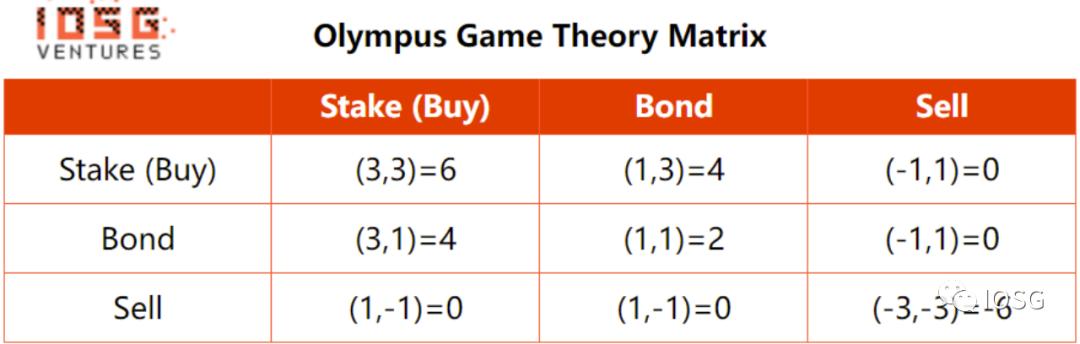

(3,3) is a Nash equilibrium concept proposed by the DeFi 2.0 protocol organization Olympus DAO after introducing game theory into its algorithmic stablecoin OHM. Before delving into the analysis of (3,3) game theory, it is necessary to briefly outline OHM's incentive mechanism. OHM's incentives mainly come in two forms: one is the bond mechanism, and the other is the staking mechanism.

In the bond mechanism, users can provide valuable coins such as BTC, ETH, etc., to the Olympus protocol in the form of LP to obtain OHM at a discount below the market price. This bond issuance is divided over 5 days, so the reason for the cheap bonds is similar to why some online shopping has low shipping costs—slow delivery means you have to wait longer to receive what you want.

In the staking mechanism, users can directly exchange valuable coins for OHM in the market and then stake OHM on the platform. After obtaining the valuable coins from users, Olympus will deposit them into the treasury, and the real value of one OHM equals the total value of coins in the treasury divided by the total issuance of OHM. If the real value of one OHM is 1 USDT, and the market price exceeds this point, the protocol will mint more OHM to balance the price and distribute the newly minted OHM proportionally to stakers, thus solving the share dilution problem present in the veCRV model. Therefore, according to Olympus's so-called rebase process, ideally, as long as users choose to stake long-term, the OHM balance in their positions can continue to grow through compound interest. However, if there is significant selling pressure on OHM in the secondary market, this flywheel cannot be sustained.

In summary, the Nash equilibrium proposed by Olympus is built upon these two incentive paradigms. According to traditional economic theory, Nash equilibrium refers to a strategy where two or more participants in a non-cooperative game achieve a maximization of mutual benefits. Poker enthusiasts can also understand it as GTO (Game Theory Optimal) in poker. According to Olympus's official documents, assuming there are two participants in the market, the three behaviors of both parties correspond to the following 9 outcomes:

Source: IOSG Ventures

From this matrix, we can see that both staking and discount bonds can bring positive returns to the protocol, while mutual staking is the optimal strategy that can achieve Nash equilibrium. Conversely, if participants take opposing stances and choose to sell, both sides will become losers in this game. However, in fact, whether in DeFi or at the poker table, everyone's ultimate goal is to win, and winning together is ultimately also about winning for oneself. Olympus introduced this mechanism to advocate for cooperation to achieve a win-win philosophy.

Innovation of Solidly: veNFT + Voting Power Optimization

Solidly deeply integrates the characteristics of the aforementioned veCRV and (3,3) models. On one hand, Solidly uses the ve mechanism to return veROCK (derived from the issued ROCK tokens) as proof of equity. On the other hand, Solidly introduces the (3,3) rebase staking paradigm, ensuring that the equity of stakers will not be diluted over time. However, on this basis, Solidly has also made several innovations:

1. Converting voting rights into NFTs to liberate liquidity. Recognizing the limitation that users cannot transfer veCRV after staking, Solidly has designed the returned veROCK in the form of NFTs, freeing users' rights to trade freely in the secondary market. After staking, Solidly users can transfer the NFT representing their equity to others, and any NFT holder has voting rights to decide the distribution of rewards.

2. Stakers receive 100% of trading fees but can only earn rewards from pools they voted for. Unlike Curve, where all veCRV holders can share half of the fees, veROCK holders can earn all trading fees, but only from the pools they voted for. Therefore, in this model, the act of voting becomes crucial. Ideally, all voting participants will vote for the pools that can generate the most fees to maximize their own interests, allowing those pools to receive the most reward distribution. If a staker votes for the wrong pool, they will receive no rewards or only very low fees.

3. Token distribution volume is adjusted based on TVL ratio. In Solidly's model, the number of tokens issued is inversely proportional to the total amount staked. Suppose the protocol initially has 5000 circulating tokens and can issue a maximum of 500 reward tokens per week; we can discuss three scenarios:

a. When the total staked amount is 0, all 500 reward tokens are issued. In this case, LPs are completely indifferent to fee income and only want to mine and cash out, often occurring when LPs lose trust in the protocol and are unwilling to hold equity.

b. When all 5000 tokens are staked, no reward tokens are issued. In this case, the protocol can sustain the entire system with the income from trading fees, so the best scenario for the protocol is for tokens to be staked as much as possible to avoid issuing reward tokens.

c. When the total staked amount is 2500, 50% of the reward tokens, i.e., 250 tokens, are issued. Since individual and protocol interests cannot completely align, this scenario is actually more common, with the staking ratio and token issuance often showing a dynamic balance within a certain range.

Airdrop-Triggered Vampire Wars

More talked about than Solidly's underlying protocol mechanism is the vampire wars it has triggered. On January 6, AC announced on Twitter that the issuance of Solidly tokens ROCK would be directly airdropped to the top 20 protocols with the largest lock-up amounts on the Fantom protocol (ultimately airdropping to the top 25 protocols). After receiving the airdropped tokens, these protocols can decide how to use them; they can choose to allocate veROCK to the community or use it to incentivize trading pools to earn returns for their own tokens. This short statement directly ignited vampire attacks between protocols on the Fantom chain and gradually evolved into a major battle. Just to compete for TVL and make it into the top 20 to receive the token airdrop, two DAOs—0xDAO and veDAO—were born:

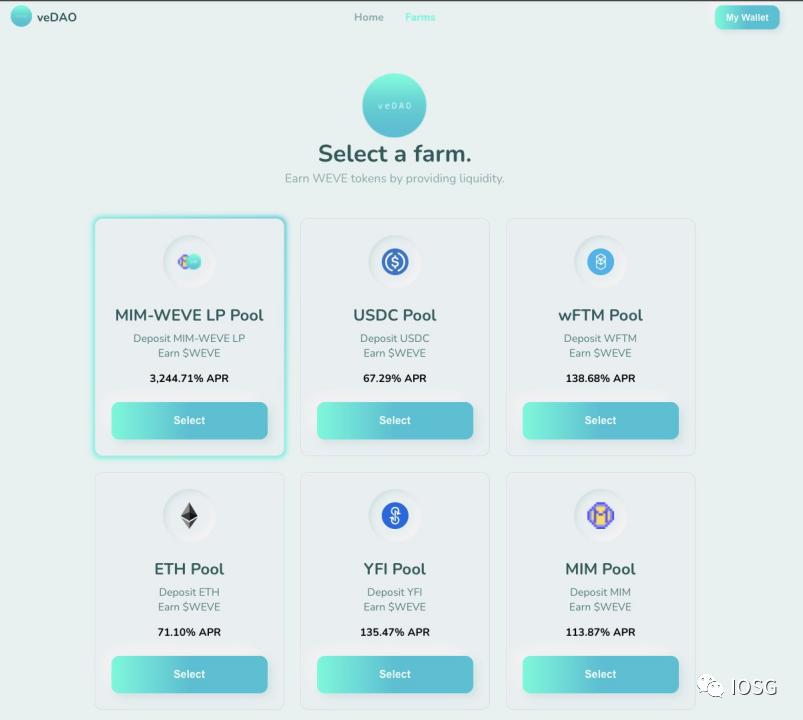

VeDAO: The Pioneer of Internal Competition

VeDAO was initiated by anonymous developers on January 19, with the very pure goal of attracting funds to seize TVL to meet the requirements for airdrop reward snapshots. Within just one day of its launch, VeDAO raised over $1 billion through token issuance, and its TVL on Fantom briefly surged to second place. The entire VeDAO website is quite simple, offering only a function to replicate Sushi MasterChef liquidity mining. Users can engage in this liquidity mining to earn WEVE tokens to participate in the governance of the DAO. VeDAO accumulates its TVL in a short time by exchanging WEVE for stablecoins and promises that all DAO members can jointly manage veROCK in the future and decide its allocation.

Source: veDAO

0xDAO: The Avengers

The emergence of VeDAO undoubtedly harmed the interests of other protocols on the Fantom chain. After being ruthlessly hunted by VeDAO, many Fantom OGs and native protocols decided to fight back. Five high-quality native protocols on Fantom—SpookySwap, Scream, Liquid Driver, Hundred Finance, and RevenantFinance—joined forces to form the Avengers, 0xDAO, to counterattack. 0xDAO mimicked VeDAO's strategy, promising to distribute all its OXD tokens to LPs. Holding OXD allows participation in decisions regarding the sale and distribution of veROCK, and within just a few days, it successfully raised $2 billion in TVL. Ultimately, 0xDAO lived up to expectations and won the war, securing the largest airdrop share with nearly 12% of the on-chain TVL locked.

Source: ve(3,3): An Introduction into the New and Ambitious Solidly Exchange (substack.com)

It is worth pondering where Solidly's future will lead. While innovating on the economic models of Curve and Olympus DAO and further releasing liquidity, we also see the hidden dangers in its current development:

1. Smoke rises again on the FTM chain. After the vampire wars for TVL ended, the airdrop winners led by 0xDAO and Solidex will set their sights on becoming the Convex of the Fantom chain, beginning to brew a new round of more intense veROCK wars.

2. Protocol innovation cannot escape the prisoner's dilemma. Although Solidly has optimized the game theory of (3,3), human nature is still difficult to withstand the test. Once the governance punishment mechanism of the DAO fails, participants often abandon win-win scenarios due to suspicion and fear. The sell-off of a single traitor can trigger a domino effect, plunging the entire market into the prisoner's dilemma and Hobbes's "war of all against all."

3. The value assigned to veROCK is still very limited. Although it can determine the future allocation of rewards, it is merely a relatively basic function. If these tokens are released indefinitely, the protocol may struggle to sustain its operations. Since its launch on February 10, Solidly has claimed that its DAO is researching and discussing this topic.

Is Solidly a beacon illuminating DeFi 2.0, or a beautifully packaged Ponzi scheme? We will continue to monitor its subsequent developments.

Risk warning

Risk warning Risk warning

Risk warning