Is everyone in the Web3 world a Marxist?

Is the era of large-scale hyper-financialization, anti-regulation, and artificial scarcity in web3 really Marxist?

Is the era of large-scale hyper-financialization, anti-regulation, and artificial scarcity in web3 really Marxist?Author: David Phelps

Translator: Block unicorn

"We are all Keynesians now." ------ Milton Friedman, 1965

"In a sense, we are all Keynesians now; on the other hand, no one is no longer a Keynesian." ------ Milton Friedman, 1966

There are many reasons to say that Web3 has made us all Marxists, perhaps none more absurd than the fact that Web3 OGs truly hate Karl Marx.

Take Nick Szabo, for example: a scholar, cryptographer, and Bitcoin inventor, occasionally rumored to be a sage, who laments that Marxism incites closed societies. Or to quote Szabo himself: "How sick can a sick brain become?"

Similarly, consider Ameen Soleimani, the creator of Moloch Dao, RAI, and span kChain—who is indeed one of the most innovative and influential thinkers in the field—he not only agrees with Szabo but argues that KGB psychological operatives believe that "America has been infected by the spiritual virus of Marxism." Soleimani writes: "When the poor are told what they want to hear—that they are equal to the rich—the seeds of social unrest are sown."

But it’s not just right-wing crypto figures who believe that Web3 is fundamentally anti-Marxist; the hyper-commercialization of crypto means that many leftists also understand crypto as an accelerated form of capitalism. "Crypto economics is in some ways the opposite of the commons: enclosure," Nathan Schneider recently wrote, because "what was once common has become ownable, tradable assets." For Soleimani, this hyper-financialization brings "things that were previously hard or impossible to buy and sell, from crypto computing power to real estate in digital games," and gives them value by artificially making them scarce, privatizing what could have been freely available to all.

Meanwhile, arguably the left's most important tech expert, Cory Doctorow, accuses DeFi of being "shadow banking 2.0," enriching 1% while posing significant risks to the economy. He writes: "If all the money is owned by the same number of billionaires, I don’t care how the banks are distributed." (In fact, about 0.01% of Bitcoin holders represent 27% of the wealth.)

So how blue ocean might we consider the idea that web3 could be a Marxist crypto pill? How can we draw such a conclusion?

Let me try to answer this first by way of example, or more precisely, another important question: Could communism be a DAO?

As early as October, I conducted an experiment by reposting three passages from Marx's German Ideology, replacing the term "communism" with "DAO," and you can judge for yourself how it works.

The original text reads: "Communists do not oppose selfishness, nor do they oppose selfishness selflessly or unselfishly… They are very clear that selfishness, like selflessness, is a necessary form of individual self-assertion. Throughout history, 'universal interest' has been created by individuals defined as 'private.'"

Note the claim relationship here: the collective can only operate well when it meets the self-interested needs and desires of its individual members, and never loses their sovereignty.

And this claim recurs.

The original text is: "The true intellectual wealth of the individual depends entirely on the wealth of his real connections; only then can independent individuals be liberated from the obstacles of various states and places. This comprehensive dependence will transform into control and conscious mastery of these powers through this communist revolution, which until now has ruled people as powers completely opposed to them."

Once again, the emphasis on individual sovereignty as the basis for collective liberation is contradictory.

This paradox is also the crux of Marxism's final tweet.

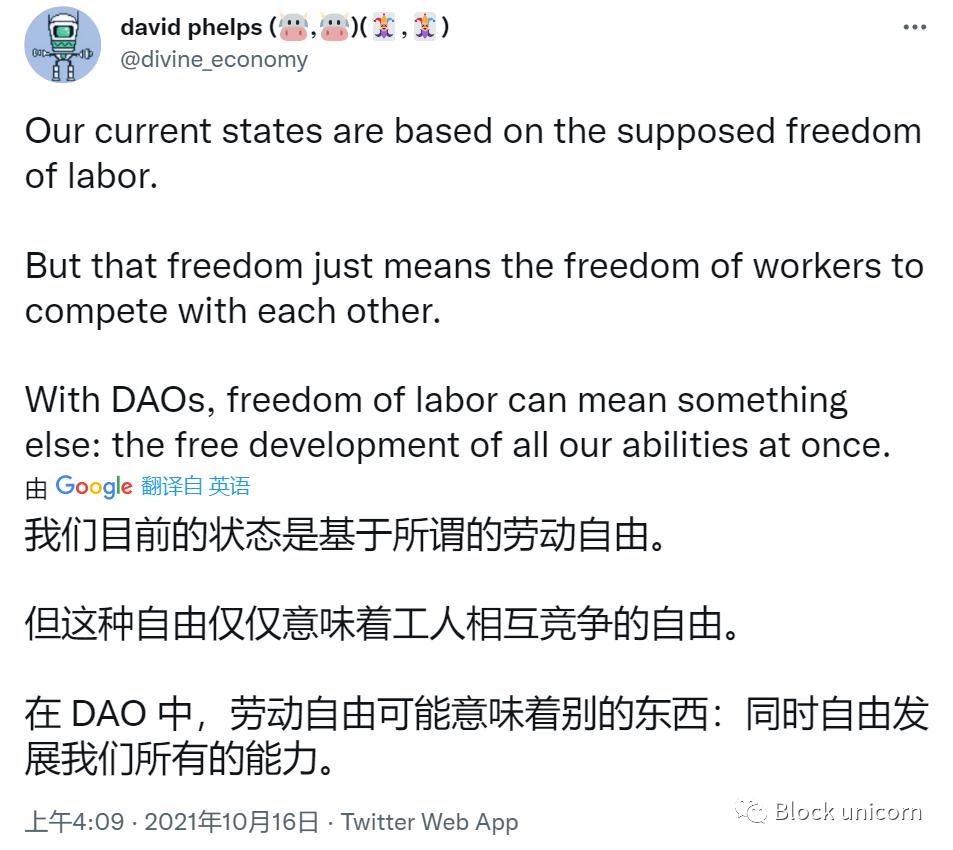

The original text: "The modern state, the rule of the bourgeoisie, is based on the freedom of labor. The freedom of labor is free competition among workers. (In contrast) the free activity of communists is the creative expression of the free development of all human abilities."

Once again, we feel the same claim: true collective freedom means liberating individuals to do as they please.

But more broadly, note that there is a claim here—that "Marxism" is not so easily simplified into applause-worthy solutions or nitpicking slogans, let alone the horrors of 20th-century national socialism. Because when we understand Marxism as dialectics rather than dogma, as a series of claims and paradoxes, we can grasp one of its main value points: it is a framework for addressing questions that may fundamentally have no answers.

Thus, for the purposes of this article, we will discuss three questions posed by Marx, all of which revolve around the claim relationship between individual sovereignty and collective cooperation, which currently constitutes the three main categories of Web3: NFTs, DeFi, and DAOs.

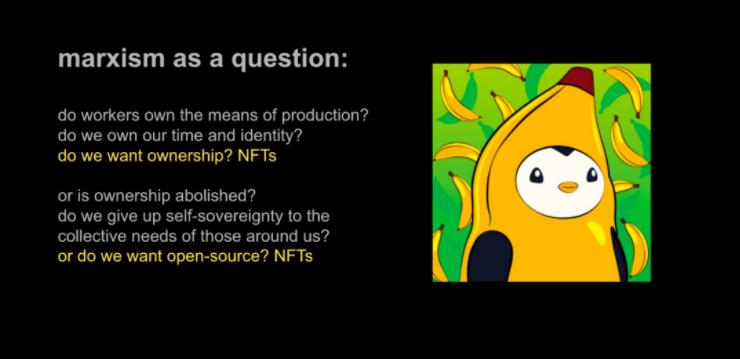

Question 1: Do workers own the means of production? Or is ownership abolished? (a.k.a. NFTs)

This is such an obvious question that it is hard to answer: does Marx universally advocate for the abolition of property and ownership in his writings? Or does he advocate for the redistribution of ownership to the proletariat, meaning they can own the means of production?

This question even runs through dogmatic documents like the Communist Manifesto, which awkwardly switches between wanting to abolish property and wanting to transfer property to the workers. Marx and Engels write in the Communist Manifesto that, in this sense, the theory of communists can be summed up in one sentence: abolition of private property.

This claim is troubled in the text, as Marx and Engels try to obscure it, explaining from different perspectives that communism is merely the abolition of private property (generally not property, don’t worry about the ordinary workers of the alliance!), and the real aim is to deprive the bourgeoisie of their ill-gotten gains. However, they do not have a good answer to whether they would destroy workers' property, merely arguing that, given history has done so, it is a meaningless point: "The development of industry has largely destroyed it, and it continues to destroy it every day."

This is clearly a rhetorical evasion of the question of workers' ownership—because although the Communist Manifesto boldly presents an anti-property stance, we can see Marx's paradox. For workers, owning the means of production means breaking free from all forms of ownership as we know it. "With the abolition of private property," he writes in the German Ideology, "people obtain the patterns of exchange, production, and their mutual relations, once again under their own control."

Conversely, Marx writes that trade is a system governed by supply and demand relations that rule the entire world—this relationship distributes wealth and misfortune to people, establishes empires and overthrows them, leading to the rise and fall of nations. What Marx fears is not the tyranny of kings, but the supply-demand relationship. In other words, supply and demand is an undervaluation of what is most important to us, whether food or love. Critics of NFTs will recognize the sentiment here: supply and demand gives value to goods not based on what they mean to us, but simply because of their scarcity in the market.

And now, what happens when workers control the means of production?

Marx and Engels' utopia:

"Once labor distribution begins, everyone has a specific, exclusive range of activities imposed on them. They are a hunter, fisherman, herdsman, or critic; if they do not want to lose their livelihood, they must remain so; whereas in a communist society, everyone can achieve in whatever they want to do, society normalizes general production, thus allowing me to do one thing today, another tomorrow, hunt in the morning, fish in the afternoon, herd cattle in the evening, and critique after dinner, just as I have thoughts, without becoming a hunter, fisherman, herdsman, or critic." ------ Marx and Engels, German Ideology

It turns out that the most important means of production is not factories. It is "time"; more importantly, our own self-awareness comes from having free time. These win us sovereignty over living the lives we want, becoming hunters, fishermen, herdsmen, and critics, rather than being defined by our roles in profit-making.

But again, note that there is a claim here about the roles of individuals and the collective—if we are all doing what we want to do, how does the social collective operate? Who fixes the sewers and takes out the trash? If we live in small, sustainable communes, perhaps these are unnecessary; Marx merely suggests that "society regulates general production."

But whose society is it?

Rather than trying to answer this question directly, I wonder if we can reconstruct it in more familiar terms. Because we might argue that this claim—whether to abolish ownership or to let workers own the means of production—actually reflects a deeper claim. Should we aspire to individual sovereignty, to have our own identity, or in today's terms, to own our data and reputation? Or, if we give up this selfish sovereignty to better support each other and the collective needs of society, would each of us fare better?

In fact, we can distill these questions into a profound claim at the core of Web3:

Do we want ownership of the products of our labor, or do we want them to be open-source and available for anyone to use?

One way to understand this claim relationship is to understand the creator economy of the past decade. Stepping back, we can see that the creator economy is a precursor to Web3 culture, not only a product of permissionless user-generated content (TikTok, Twitter) but also a product of the general trend toward the gig economy and freelancers, who engage in any work they like and earn from their work.

This may sound like the creator economy has culturally shifted us toward a belief that artists should own the means of production: what is a TikToker if not a Hollywood celebrity who owns the means of production? What is a hype house if not a prototype? But we also remember that the creator economy is actually a product of free labor, prioritizing mass participation over the monetization of "100 true fans."

Stepping back, we can see that the creator economy is actually the pinnacle of the gig economy's failure, which has dominated for 40 years with the promise of worker sovereignty and the reality of worker isolation. Initially, freelancing was an attractive proposition for businesses, allowing them to pay on demand—or more precisely, to pay as little as possible—just as David Harvey pointed out in the context of postmodernity: "Employers take advantage of weakened union power and the surplus labor pool to push for more flexible work arrangements and labor contracts." Ironically, the creator economy has also proven to be the destruction of those traditional companies, as the hierarchy of corporate ladders has disappeared in the face of a new ideology of working for oneself.

But in a world where 35% of American workers are gig workers, this promise of whimsically becoming fishermen, hunters, and critics also means giving up stable income and the structural support of responsibilities, as freelancers have less safety net than ever, and fewer claims to worker rights—because they are on their own.

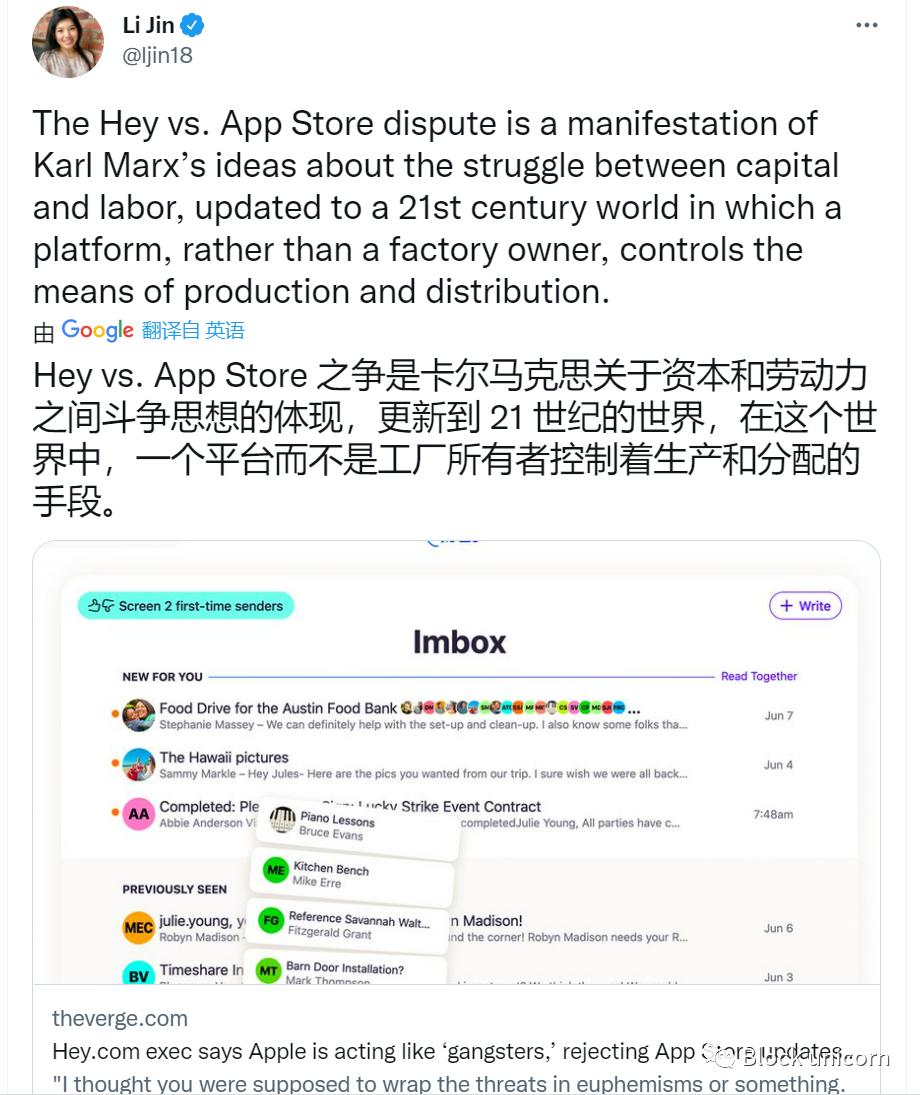

Similarly, the creator economy promises us a Marxist vision where anyone can successfully become an artist, but only if they operate through platforms that profit excessively from the workers who make them successful. This is true for Uber drivers and TikTokers alike. We might say this is the cost of freelancers going open-source: their work is used for free by anyone, while the platforms they operate on remain isolated and deeply monetized.

In other words: freelancers gain open-source, but platforms gain ownership.

So what is the answer? It could be argued that Web3 is a response to the failures of corporate ladders and economic polarization, one side isolated companies, the other side freelancers in open markets. This is where we return to Marx. Because the promise of independent sovereignty only works if there is indeed a "society" to "regulate general production," allowing us to hunt and fish at will. Only when we are also willing to sustain each other for the collective good can we own our work.

Clearly, DAOs are one answer we will return to later—a kind of willing state as a company, allowing us to earn all the income from our work while sharing it without permission and abolishing personal ownership of it.

But a simpler model is NFTs.

On one hand, NFTs represent creators finally getting paid directly for their work. On the other hand, this ownership is clearly built on a social structure of infinitely replicable open-source JPEGs.

In other words, NFTs show us what it means for creators to own the means of production (their art) and capture all the value they produce, even if the work itself is not private property at all, but open to everyone.

NFTs abolish ownership to make it applicable to creator-workers.

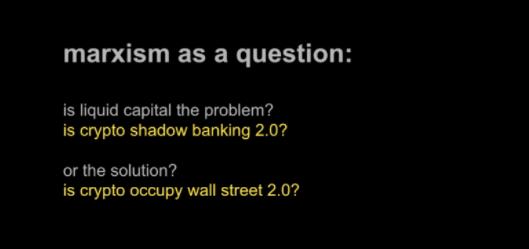

Question 2: Is liquid capital a disease or a cure? (a.k.a. DeFi)

The ownership question is far more than just an asset question. It is also a question of whether we should own our money, rather than the power of central institutions like banks or even governments, which have funded everything from subprime mortgages to wars with it. Or does this pave the way for what we call rollercoaster sovereignty—massive financial abuse, money laundering, hacking, scam artists, and extreme volatility without government oversight?

In other words, are we our own best financial custodians?

More strictly, we ask whether liquid capital is at the core of capitalism's contradictions, or a solution to capitalism's deepest problems? This liquid capital is what Marx referred to as "circulating capital" in Grundrisse, easily convertible to cash and easily convertible to commodity capital. Marx wrote that this liquid capital "is indifferent to every specific form, and can strip or adopt any of them as equivalent incarnations." In other words, like a ghost assuming the form of the commodities it possesses, liquid capital can take any form, not limited to one use case, nor even confined to one specific domain.

In contrast, let us isolate some key characteristics of fixed capital, which cannot be liquidated, and see why liquidity might help solve some of capitalism's main challenges.

Fixed Capital:

- Infrastructure (machinery, factories, airports).

- Generally single-purpose (measured by use value).

- Requires huge upfront costs from loans.

- Requires significant investment to build and maintain inventory.

- Absorbs surplus value (the company's price for goods is higher than manufacturing costs).

Note that fixed capital is at the core of some of the most predatory aspects of capitalism's history: overcharging for work, underpaying workers, constantly servicing loans that are too high to meet interest rates by producing more and more currency through ever-increasing production for things that do not yet exist.

On the other hand, liquid capital does not face these issues.

Liquid Capital:

- No geographical limitations.

- Can represent any item or commodity.

- Usable for any purpose.

Fully liquid liquid capital does not face the friction and costs of time and place, such as depreciation, backlog, and upfront costs that require significant funds, which must be repaid at a premium later.

Thus, when we define liquid capital in this way, we might consider it as something else: digital currency.

Digital Currency:

No geographical boundaries.

Can represent any item or commodity.

Usable for any purpose.

In other words, can digital currency or cryptocurrency become a solution to real-world scarcity?

Not so fast, as there is another view that this "pure capital," this capital divorced from the real world or practical use, is valuable precisely because it facilitates loans, surplus value, backlogs, and all other aspects of the system. As David Harvey wrote in Marx's Capital, liquid capital "emerges when money is put into circulation to obtain more money." Its purpose is to breed more capital, binding us to a world where we often have to work for less than our wages to generate more value to repay loans that do not yet exist.

So what happens when fully liquid capital is unbound by time, space, government regulation, or the tracks of TradFi (traditional finance), and can be deployed anywhere in the world at anyone's whim? Can online operations allow liquid capital for the first time in history to not have to service fixed capital? Or, as NFT critics say, does this mean we need to rebuild the scarcity dynamics that underpin supply and demand economics to give digital products value?

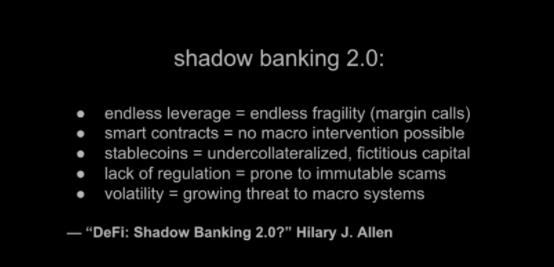

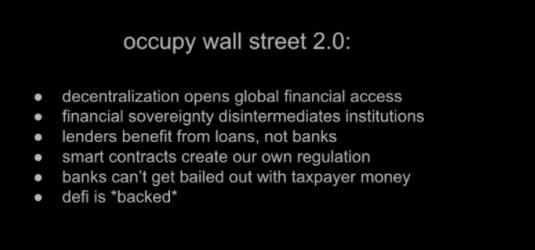

In other words, are we creating a shadow banking 2.0 with all the dangers of unregulated criminal behavior, or are we creating Occupy Wall Street 2.0?

Recently, Hilary J. Allen made a very compelling argument that the economy of liquid currency will lead to the proliferation of capitalism. Endless liquidity means over-leveraging is easier than ever, and what makes things financially more dangerous is the lack of a federal bank to support potential cascading margin calls. If every transformative technology has experienced massive financial bubbles, and when expectations exceed innovation, these bubbles drag down the economy, then we can only guess how terrible the crash will be when the next generation of technology itself can engage in large-scale, unregulated lending.

But there is also the opposite argument.

Because we can also say that liquid capital enables financial sovereignty, as we no longer need intermediaries that benefit from our funds. It turns out that financial sovereignty applies to anyone who deposits money in a bank, just as it applies to workers. Returning to the labor paradigm, we might imagine that just as workers' wages are far below the value they provide to factories, our savers' wages are also far below the value we have historically provided to banks—though we also have to pay the government to alleviate hardship funds.

The foundation of DeFi is that we no longer need to pay for the failures of banks, rather than for their successes. Because now, we can fulfill the role of lenders ourselves. In the traditional banking model, you would deposit $1 in the bank, and the bank would lend it to someone else, so you and another lender each have $1, while the bank actually earns your money by generating $2 in the economy, making you an unwitting, involuntary, and unprofitable lender to others. (I am simplifying, but this is the principle of the money multiplier and bank runs.) This is impossible in DeFi; you can provide liquidity to the market yourself, or if you wish, deposit $1 and then receive a synthetic token representing its value. Now there are also $2 in the economy, but one is fully collateralized, and the other belongs to you.

This is what we mean by DeFi being supported, although it is clear that in the real world, we are heading toward a future of under-collateralized loans and generating crypto loans for fixed capital, but financial sovereignty brings us volatility because it allows us to become our own lenders and market makers—and to be losers without a state.

This raises a question: perhaps we should create money out of thin air to stabilize the economic system? This brings us to the final part, about DAOs.

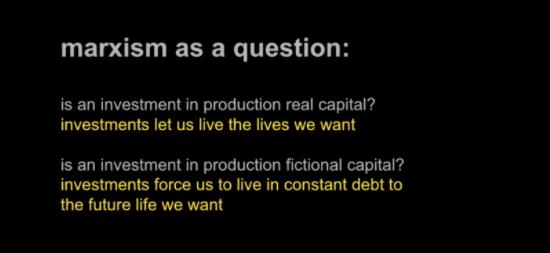

Question 3: Can investments allow us to live the lives we want? Or do they force us to live in perpetual debt?

Investing with any expectation of returns is putting money into the world, hoping for more money to come out—which raises the question, where does it come from? What generates this new value?

Exploiting the poor and expropriating land are two answers, although Marx's legacy is often intertwined with the former, but in much of Capital, he primarily focuses on the third question: debt. For Marx, debt is fictitious capital: an obligation to future money that does not formally exist, but the debt itself is voluntarily formed. For example, I mentioned last year in "Ray Dalio, Marxist" that if I lend my friend $5, and they write me an IOU, I might now use that IOU as collateral, or even as currency for other friends—so now $10 replaces $5, and with interest, even more.

We might think Marx would condemn the entire capitalist enterprise system, viewing it as a guessing game built on IOUs, where once the IOUs are fulfilled, the economy collapses. But in fact, Marx makes a crucial distinction here: for Marx, investment in companies—stocks—represents real capital precisely because they are not IOUs that can "exist twice" as loans and currency.

Stocks in companies like railroads, mines, shipping, etc., represent actual capital, that is, the capital invested and operated in railroads, mines, shipping, etc., or the amounts shareholders advance for the capital used in that enterprise. This does not exclude the possibility that these may be pure scams. But this capital does not exist twice, once as the capital value of ownership (stock), and once as the actual investment in or to be invested in these enterprises. ------ Marx, Capital, Chapter 29

Note the distinction between debt and investment; with debt, your $5 loan is always worth $5 (plus interest), so your IOU easily becomes currency or collateral. However, for investment, your $5 cannot be viewed as $5 whenever you like: its value is determined by the market, and over time it may rise or fall. In other words, investment differs from debt because it does not guarantee you a return in any form, which requires the funds to exist twice, first as a quantity to be repaid (IOU), and second as a quantity being used or lent (the loan itself).

More importantly, investments are not what Marx referred to as "fictitious capital," because they are not "interest-bearing capital," which Marx defined as "the accumulation of claims to production, the accumulation of market prices." To perfectly embody this "fictitious capital," Marx points us to government bonds: because bonds require interest to be repaid, and in reality, they cannot be used to generate themselves, they are essentially money created out of thin air. (For those who associate Marx with the specter of 20th-century national socialism, or who think he advocated for an omnipotent government to regulate businesses at any time, his shadows on states should wake us up here.)

However, there is a small trap in the public market, and a larger trap in the private market. Because where does the valuation of this stock come from? Well, it comes from the expected future returns of a company we hope performs well.

Thus, we are essentially making money out of thin air. If I invest $2 million in your company at a $20 million valuation, my $2 million is real capital, but the other $18 million is merely a mythical entity created out of thin air, from which we hope to earn value through future monetization. These valuations are like debt, a claim on future output.

This is not important for Marx because traditionally there has never been a way to leverage these claims or use them as capital: as long as the IOU cannot be traded as its own currency, money will not exist twice.

But in DAOs, this suddenly changes, because now we have replaced stocks with tokens, and we can trade, purchase, or invest with these tokens (assuming the SEC allows us to do so).

But there is another, even greater significance at play—DAOs allow anyone anywhere to create tokens that are essentially claims on future value and raise funds from anyone they like. Now, anyone can enjoy the benefits of fictitious capital without needing to actually repay interest.

We can begin to see the risks that DAOs bring to the financial system. Many of these investments will not return their valuations, and the democratization of finance provides huge opportunities for fraudulent or even failed projects, allowing investors who cannot conduct due diligence to profit.

But even so, by allowing us to create our own currency, DAOs can help us innovate and invest in ways that would never have happened before Web3. Owning your work is one thing. Being able to fund the work you want to do is another—it enables real worker collectives to control funding, eliminating the barriers between labor and capital. Because now you can imagine DAOs "investing" in each other by exchanging tokens to support each other's projects. Replacing the traditional investment ecosystem, where one side is capital (investors) and the other side is labor (founders), DAO-to-DAO (DAO to DAO) token swaps mean both sides represent.

In other words, DAOs embody all the tensions we discussed above: between worker sovereignty and giving it up to the collective, between liquid capital that enables us to achieve financial self-sufficiency and pushes us toward a world that only sees the illusion of future investments and returns, between real capital invested in the projects we create and fictitious capital that funds future value with that money. If there are no clear answers to these paradoxes, at least there are multiple-choice options.

It is this optionality that seems particularly, well, Marxist. In an era of massive hyper-financialization and billions in venture capital, this may be the true significance of DAOs, and the real reason why even venture capitalists now speak like Marxists under the shadow of corporate and gig economies: the great goal of Web3 is not only to give builders financial sovereignty over what they are building, but to allow everyone to build according to their own will.

Special thanks to Li Jin and the comments and edits from Bhaumik Patel and Tom White.

Risk warning

Risk warning Risk warning

Risk warning