X to Earn: A Formal Challenge to the Death Spiral

After the death spiral of STEPN, it will stabilize at a value during the flat period that is higher than Axie.

After the death spiral of STEPN, it will stabilize at a value during the flat period that is higher than Axie.Author: Andy, IOSG Ventures

Editor: Elaine, IOSG Ventures

Introduction

Since the rise of Axie Infinity, numerous Axie-like Play to Earn games have emerged like mushrooms after rain. However, after Axie showcased a spectacular death spiral roller coaster in the crypto and gaming circles, no P2E game has yet been able to match Axie's captivating story: insufficient market cap, lack of popularity, insufficient creativity, or simply not being ready.

As a result, Axie's P2E not only taught a lesson to other blockchain games but also inspired the non-blockchain gaming market: if Play to Earn can become so popular, could other X to Earn (X2E) models also have potential? In the past two months, the market has finally seen another exciting X2E product after Axie: STEPN.

I will summarize the product introduction, which has been reiterated in other research reports, in one sentence: STEPN is a Move to Earn game where users purchase running shoe NFTs to earn tokens - currently, STEPN has 1 million users and 300,000 DAU, with the governance token's market cap skyrocketing from 8 million at IEO to 20 billion in less than two months.

As this article is published while STEPN is still in its growth phase, many who have entered the market or are observing from the sidelines, including other X2E entrepreneurs, are closely watching one question: When will STEPN reach its peak and begin its death spiral? It is understandable that under Ponzinomics, the death spiral is an unavoidable topic in the market.

However, as the market continues to heat up with X2E, we should not avoid discussing the death spiral; instead, we should actively understand what the death spiral represents and how to challenge the shadow of the death spiral to sustain the project long-term. What kind of operations and philosophies can maximize long-term value for users, project parties, and investors under the shadow of the death spiral? Therefore, at this moment when STEPN is gaining immense popularity and before more X2E products arrive, I will use the cases of Axie and STEPN to present several viewpoints that I hope will be helpful to the market regarding the death spiral itself.

Without further ado, here are the conclusions:

Although the death spiral is inevitable for Ponzinomics, this article aims to clarify the following points:

First, the outcome of the death spiral is not death, nor does it signify the failure of the product; rather, it is the process of returning from the madness of X2E to the fair value of the product itself. The latency period before this process can vary in length, the speed of decline when it occurs can be fast or slow, and the fair value to which it returns can be high or low.

As the first successful X2E project, Axie has gone through many trials and errors, demonstrating the possibilities, limitations, and challenges that future products will face over long-term operations. This has allowed us to see projects like STEPN striving for innovation by learning from the essence of these experiences - X2E is evolving.

What we expect from the evolution of X2E is a more restrained period of madness, a slower cooling-off period, and a higher fair value return line - this is what I believe STEPN has the potential to achieve.

More importantly, it is essential to ultimately achieve making users who recognize the fair value of the project mainstream, allowing utility value investors rather than speculators to reap most of the benefits. (Recognizing that participating in such projects is not simply investing 10 to earn 20, but investing 10 not only brings the utility value of the project itself but also returns an additional 3; and for users who persist, the additional rewards can reach the possibility of returning 10 or even 20.)

In future narratives, the economic sources beyond Ponzinomics are what I look forward to in X2E, as they have more stories and space than the current P2E in blockchain games: for instance, we recently discussed an early Bike to Earn project (MOTE by Sweetgum Labs, interested investors are welcome to communicate) that mentioned the monetization of carbon emissions and the return flow economy.

For example, a person who originally drove 10 kilometers to work every day could switch to biking, saving 4 tons of carbon emissions in a year, and with one ton of carbon emissions currently valued at 80 euros in Europe, it theoretically means that a person could monetize over 300 euros annually to flow back into the economic system, and future increases in carbon prices will enhance this mechanism's potential. Although there will certainly be significant feasibility challenges (such as whether carbon trading markets recognize its carbon emission qualifications), I am very eager to see X2E products striving towards this direction of returning to the external economy.

Sunk Costs and Unexpected Returns

1. Acceptance of Sunk Costs in Investment Losses

Let’s start with an example: most people are familiar with gym memberships; the story of someone working out three times a week in the first month and then only once every three weeks in the tenth month is likely also familiar. If you find yourself reigniting your motivation after your membership expires and going through the same cycle again, then you and I are family. Why do we allow ourselves to repeatedly invest significant costs but surrender to low self-discipline, allowing this cycle to continue? Is it not like those who fail in one cycle forget the lesson and vow "next time for sure," only to embark on the same path again?

A key mindset is the tolerance for sunk costs: signing up for a gym membership is an investment in one's physique and health (utility), and after the excitement fades, the cobwebs on the membership symbolize the willpower declaring this investment a failure and reconciling with the sunk costs.

It may not feel significant, so let’s quantify it roughly: a gym membership costing over 5000 RMB was originally intended to encourage you to run 3 times a week for 5 kilometers each time, but if you only persisted for the first two months, the original investment return of 5000 RMB recognized at purchase would be 13 kilograms, while the final return would be 2.3 kilograms, resulting in an ROI of 15% → Most people’s reaction here is likely "sorry, I’ll try again next time," and they sign up again. However, imagine if this were the ROI for those investing in the stock market or blockchain; would they still say "I’ll try again next time"? For investment losses, it is easy to see that people have a low tolerance for sunk costs in financial investments, while compared to that, the tolerance for sunk costs in utility (physique/health/happiness, etc.) investments is significantly higher.

2. STEPN: Is it your financial investment software or utility investment (fitness) software?

Unexpected Returns for STEPN Investors: Here’s an example that many STEPN players might resonate with: a friend who experienced Axie entered the market about a month ago, initially intending to make money just like when playing Axie, but found that running was less mentally taxing than gaming and lacked the resistance of "wasting time playing games." Thus, they chose STEPN for the same time investment; however, after a month of running daily to earn GST, they discovered that the meaning STEPN brought them changed from their initial expectations: they initially focused on how quickly they could break even and how much they could earn daily (financial return), but later they were unexpectedly shocked by the non-financial returns they had previously overlooked: the change in mental state from exercising for 40 minutes daily, the shift from being lazy at home after work to exercising with family, the change of losing two pounds after years of failed weight loss, and becoming more concerned about their health.

For this friend, STEPN was inherently a running + earning project, and users naturally had expectations for both sides upon entering. However, the micro-level participation process included a crucial mindset shift: coming in with the primary goal of financial returns, but after a prolonged period of persistence, they experienced a change in mindset, recognizing and appreciating the non-financial returns STEPN provided, which is the utility returns. This is precisely what Axie Infinity lacked. We often say that the endings of Ponzi games are all death spirals, but the aforementioned mindset shift in STEPN may become a significant factor in rewriting the outcome.

Inevitable Death Spiral Does Not Mean Death

1. First, define three types of players:

Lucky Type A Players, Worried Type B Players, and Observing Type C Players: The friend mentioned earlier entered the market a month ago and is about to break even - we can refer to these players who have broken even (or are about to) as Lucky Type A Players - since the game mechanism does not set a lifecycle for shoes, Type A players can continue to earn indefinitely as long as they are willing to persist after breaking even. After observing Type A players, two core questions arise for Ponzinomic products:

1) Can players who have not yet broken even still break even? How long will it take? We can temporarily call these players Worried Type B Players.

2) Can friends who have not yet entered the market still join? We can temporarily call these players Observing Type C Players.

Here, it is clarified that Type A, B, and C players are not fixed users but rather classifications of user groups at a specific time point, which can be converted for individuals: Type B players will become Type A after spending some time breaking even, and Type C players will become Type B after entering.

2. How will STEPN's death spiral differ from Axie Infinity?

It is undeniable that Ponzinomics cannot avoid the death spiral, but I believe that despite both experiencing a death spiral, STEPN and Axie's experiences and outcomes will have three interesting distinctions (again, not investment advice): 1) The latency period of STEPN's death spiral may be longer; 2) The chain reaction speed of STEPN's death spiral may be slower; 3) The post-death spiral plateau of STEPN may have greater prospects. Let’s discuss these in detail.

1) The latency period of STEPN's death spiral may be longer (Warning! Theoretical analysis, not investment advice):

Axie:

a. Axie embraced guilds and experienced explosive, unnatural growth - only 15% of players were individual users, while 85% were guild users who could participate in SLP production without owning Axie. Guilds provided hands-on tutorials to bring in new players, allowing them to quickly start earning within a short time, with guild management directly arranging optimal yield strategies for a large number of rapidly joining guild players to maximize SLP output.

b. A large number of guilds and hired players maintained a much higher extraction efficiency from the economic system than natural players: At this time, guild players did not belong to the A, B, or C player categories mentioned in the STEPN analysis, but were simply hired mercenaries, maximizing the extraction of benefits from Axie Infinity. This extraction efficiency was significantly higher than that of the same number of naturally growing individual players. The rapid extraction allowed guilds and mercenaries to taste the sweetness and continue to expand, while the rapidly growing Sky Mavis did not intervene much in this high-efficiency value extraction, or rather, the momentum of the guilds did not allow Sky Mavis to hit the brakes, so the high-efficiency value extraction and rapid unnatural growth represented a shorter Ponzi product lifecycle. Ultimately, we saw AXS, which started gaining momentum in early July 2021, reach its peak in early November, officially entering the death spiral.

c. Guilds and mercenaries may be the chronic poison Axie had to swallow: What if there were no guilds? Could Axie have extended that four-month period to six months or even ten months through natural growth? Or if there were no guilds, would Axie have attracted new blood due to insufficient growth, leading to an earlier halt? I do not have a definitive conclusion, but I tend to believe that Axie could not rely on natural growth and had to swallow the bitter pill of guilds - traditional gamers are not very willing to spend high prices to endure such a dry and simple game, and in developing countries like the Philippines, without the help of guilds, the complex cryptocurrency system naturally creates barriers that deter many users with lower learning and economic capabilities, making guilds almost a necessary choice for Axie, even if they know it may have economic consequences.

STEPN:

a. Firmly maintaining natural growth, combating cheating, rejecting guilds, and having no leasing: At the time of writing, the official announcement had just reached 300K DAU, and a significant difference from Axie is that these 300K DAU are essentially real players with "one person, one machine, one account" - no guilds, no leasing, requiring players to learn how to use cryptocurrency themselves and pay out of their own pockets, making it difficult to cheat. Under the strict monitoring and crackdown by STEPN officials, achieving unnatural growth is extremely challenging. Founders Jerry and Yawn have repeatedly expressed their commitment to natural growth, and the only leasing feature related to unnatural growth mentioned in the white paper has been confirmed by Jerry in my specific inquiry to be opened only much later, and confirmed that it will not be opened within six months.

b. The project party is also very restrained in operating the token economy: The invitation mechanism of STEPN somewhat alleviates the issue of excessively rapid entry speed, and the introduction of gems and box-opening gameplay is increasingly consuming GST. Recently, the added demand point for the governance token GMT is also indirectly relieving the pressure on GST, and more functions will be added to GMT in the future. It can be seen that the project party behind the game has borrowed and innovated multiple methods from traditional games and P2E cases to maintain the stability of the token economy, trying to extend the short path that Axie took.

c. Wealthy, eager-to-learn real players, and high-quality new players brought in from outside the circle: This persistence and restraint lead to a user base that has undergone two layers of screening: They are wealthy (the entry fee is indeed not cheap, and they must pay out of their own pockets), and they have learning ability/knowledge (the STEPN software does not have lengthy introductions for new users; players need to learn how to understand the wallet's usage and logic themselves - Jerry mentioned that survey results show that 30% of users are using decentralized wallets for the first time).

d. If the project party wants, they can choose to open the valve for unnatural growth at any time to delay the arrival of the death spiral (though it won’t happen in the short term): Although we see rapidly growing user data with the naked eye, this data is already the real users growing under the project party's restraint, and the value extraction efficiency from the economic system is far less than that of Axie guilds, even if it slowly begins to grow weakly in the later stages. If STEPN wants to open the valve to lower the user selection threshold, I believe that in the later stages, unnatural growth could also somewhat delay the start of the death spiral.

2) The chain reaction speed of STEPN's death spiral may be slower:

Axie:

a. Although the death spiral is a chain reaction, Axie's decline was not a cliff-like drop: In fact, when we look at AXS's market cap after the death spiral began, although it was a chain reaction, it was not a cliff-like drop. The original break-even speed was extended during the decline, but if users are willing, they can still grind slowly to break even, although this is a painful process, as the enjoyable gameplay time of the game itself is limited, and the later process of slowly recovering costs for financial returns is torturous.

b. Since assets do not provide much meaning (utility) beyond financial investment, selling is a simple and clear choice: For most users, aside from the gold farming aspect, the game does not hold much significance. In other words, if you, as a real user, really invested your money to play Axie, aside from the goal of breaking even, the enjoyment/utility brought by the game itself is too low, leading you to feel only the frustration of decreasing financial returns during the death spiral, making the most rational choice to escape early, and you are likely to choose this rational course of action. Because there are many people in the game who think like you, this is also why the speed of collapse caused by the death spiral, while not cliff-like, will not be slow either.

STEPN:

a. Users recognize the utility returns beyond financial returns during participation: Reflecting on the story of my friend at the beginning of the article - primarily participating in STEPN for financial investment, but gradually realizing the utility (physique/health/happiness) investment returns during the process. Returning to the part I mentioned at the start of the article: for investment losses, it is easy to see that people have a low tolerance for sunk costs in financial investments, while compared to that, the tolerance for sunk costs in utility (physique/health/happiness, etc.) investments is significantly higher - so in the context of STEPN, how does this additional tolerance manifest? Let’s analyze this specifically:

b. Unlike Axie, STEPN provides a choice for some users who recognize utility returns not to sell: So a key question arises: Suppose you invested $1000 at the peak of the death spiral and persisted in running daily for a month, only to find that the break-even goal that previously took 50 days has now been extended to a year or even longer, but suddenly you realize you have gained so many utility returns beyond financial returns, what will you do?

Quickly sell all your assets to stop losses and return to a lazy life of staying at home without exercising?

Affirm your persistence and utility returns during this period, realizing that the desire to break even has slowly transformed from an investment expectation into a commitment to help yourself persist, thus deciding not to sell/sell less, and extending the break-even timeline from two months to a year or even more, slowly recovering your costs?

Or, as long as you are willing to continue exercising, you can become healthier, eventually break even, and start earning net profits; while choosing to sell will lead to direct financial losses and, without external motivation, slowly give up a very good habit. I believe if you see this question and start considering your choices, rather than making a quick and singular choice like Axie users, then the decline during STEPN's death spiral may be slower than Axie's.

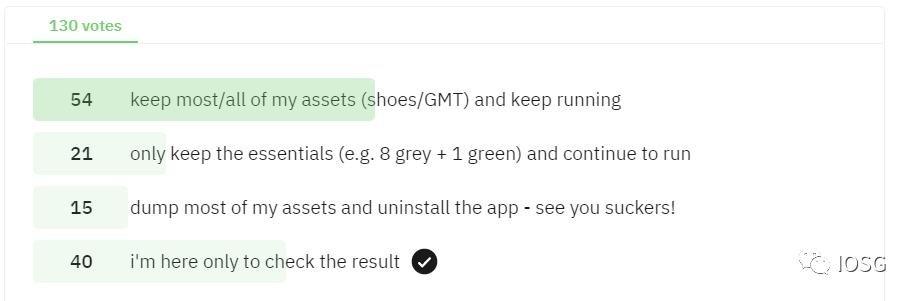

c. Surveys show that 83% of users expect not to flee during the death spiral: Let’s look at another example, which is a user survey I posted on STEPN's Reddit (as shown below): When STEPN enters a death spiral like Axie, what will you do with your assets? My initial expectation was that most people would choose to sell all their assets and leave, but the final result was that 60% chose not to sell GMT and shoes and prepared to continue running, while 23% chose to keep key shoes (like 1 gray or 1 green 8 gray), and only 17% chose to sell everything:

This survey, of course, has no legal effect, so although those who say they won’t sell now may still sell when prices start to drop, I believe the survey results are not something we would see in Axie. This means I believe the selling pressure after the death spiral begins will likely be lower than in Axie, the slope of decline will be slower, and the negative impact on the break-even cycle will be smaller compared to ordinary blockchain games, because some users will make a certain shift towards utility investment during participation, leading to a reduced sensitivity to original investment returns and a greater focus on utility returns.

3) The post-death spiral plateau of STEPN may have greater prospects:

Axie:

a. The result of the death spiral is not death, but rather a gradual revelation of the product's fair value to the market: After experiencing a significant drop during the death spiral, AXS's market cap has stabilized at around 3 billion for nearly three months now, with Axie's price dropping to a more accessible level of around 50 dollars each. The entry threshold for players is now lower, but the break-even cycle remains long. However, because the utility return (game enjoyment) provided by the game itself is limited, players aiming for break-even and net profit will still feel tormented.

Moreover, for the 85% of total players who are guild mercenaries, Axie's yield has already dropped below that of real-world jobs, leading to a decrease in participation. Conversely, the genuine players who were previously interested in trying Axie but found the entry fee too high, namely the "Observing Type C Players," now have the opportunity to come in and try. This means that the death spiral has allowed Axie to move past the rapid expansion promotional phase and finally have a chance to welcome real players. The prolonged break-even cycle for guilds and the reduced income for mercenaries are unhappy, but the decline caused by the death spiral has provided opportunities for genuine players who need to enjoy the game.

My colleague Alex and I both believe that P2E is not the goal, but rather a customer acquisition method (UA) - Axie's story indirectly confirms this theory in an immature way: The P2E frenzy allowed Axie to skip the cold start and user acquisition steps, enabling it to quickly gain substantial funding, users, and opportunities to refine the product early on. After experiencing the death spiral, the entry threshold has returned to the fair value of the game itself, allowing genuine players (rather than speculators) to participate and replace.

STEPN:

a. STEPN's post-death spiral will also stabilize at a higher plateau value than Axie, with more users and a larger market: When the price of the cheapest gray shoes drops from $1000 to, say, $100, although the break-even cycle is long (e.g., a year), the investments of players who cannot persist will become sunk costs for those who do, but as long as you persist, the system will reward you for breaking even.

Because when the investment drops from $1000 to $100, players will be more tolerant of their sunk costs, leading to more people unable to persist, collecting more sunk costs, thus forming a relatively stable balance, similar to the current stabilized price of AXS. At this point, STEPN has transformed from a money-making project into a betting agreement: spending $100 to buy a project that supervises your persistence in running, and as long as you persist, not only can you recover that $100, but you can also continue to earn steadily. How does that sound?

b. Clones can sustain for a while but cannot become a long-term solution, and will not affect STEPN's long-term value: Smart partners might ask, if I can find a clone to continue running and earn more, why should I stay on STEPN?

I think we can look at Axie: the number of clones cannot compare to Axie, but what are the results of Axie's clones? While some can make money, their cycles are shorter, their market caps smaller, and the requirements for truly profitable players are exceptionally high: they need to deeply learn which projects have high yields, who is running the market, whether they entered early enough, and when to cash out - indeed, there will be a wave of STEPN users sensitive to financial returns trying to make money with clones, but ultimately, clones will die down, leaving these individuals hurt, yet with the exercise habit, they will return to the time-tested, lower-yield but stable STEPN; and this is just for users sensitive to financial returns, while users who focus more on utility returns are less willing to spend so much time and energy risking clones.

This is also the biggest difference between STEPN users and Axie users - Axie's guild players need to use this money to live, how can they not maximize their returns with their utmost effort? Coupled with STEPN's social attributes and other narratives, as well as the ability to attract resources and capital flows beyond Ponzi economics (such as e-commerce, carbon emissions, brand partnerships, etc.) and the narrative capabilities of the founders, along with the authenticity and high quality of users, I believe STEPN may become a brand that can stand the test of time even more than Axie.

Conclusion

Although the death spiral is inevitable for Ponzinomics, the purpose of writing this article is to clarify the following points:

First, the outcome of the death spiral is not death, nor does it signify the failure of the product; rather, it is the process of returning from the madness of X2E to the fair value of the product itself. The latency period before this process can vary in length, the speed of decline when it occurs can be fast or slow, and the fair value to which it returns can be high or low.

As the first successful X2E project, Axie has gone through many trials and errors, demonstrating the possibilities, limitations, and challenges that future products will face over long-term operations. This has allowed us to see projects like STEPN striving for innovation by learning from the essence of these experiences - X2E is evolving.

What we expect from the evolution of X2E is a more restrained period of madness, a slower cooling-off period, and a higher fair value return line - this is what I believe STEPN has the potential to achieve.

Moreover, it is essential to ultimately achieve making users who recognize the fair value of the project mainstream, allowing utility value investors rather than speculators to reap most of the benefits. (Recognizing that participating in such projects is not simply investing 10 to earn 20, but investing 10 not only brings the utility value of the project itself but also returns an additional 3; and for users who persist, the additional rewards can reach the possibility of returning 10 or even 20.)

In future narratives, the economic sources beyond Ponzinomics are what I look forward to in X2E, as they have more stories and space than the current P2E in blockchain games: for instance, we recently discussed a Bike to Earn project (MOTE by Sweetgum Labs, interested investors are welcome to communicate) that mentioned the monetization of carbon emissions and the return flow economy.

For example, a person who originally drove 10 kilometers to work every day could switch to biking, saving 4 tons of carbon emissions in a year, and with one ton of carbon emissions currently valued at 80 euros in Europe, it theoretically means that a person could monetize over 300 euros annually to flow back into the economic system, and future increases in carbon prices will enhance this mechanism's potential. Although there will certainly be significant operational and pricing challenges, I am very eager to see X2E products striving towards this direction of returning to the external economy.

Final Thoughts

Having discussed the advantages I believe STEPN has over Axie, I want to emphasize again that this is not investment advice, as the operation of the project depends significantly on the decision-makers and major participants - STEPN's ability to collaborate with the three major exchanges and the generosity of whales during market manipulation demonstrate many strengths beyond the fundamentals of STEPN.

Ultimately, the development direction of STEPN will still depend on the balance of various important factors within the project and the volatile market. The above analysis is based on the information currently available, speculating on some potential nodes and prospects STEPN may experience in the future. How it ultimately unfolds, let us wait and see.

Risk warning

Risk warning Risk warning

Risk warning