A Comprehensive Understanding of the Comeback Journey of Algorithmic Stablecoin UST

This article attempts to answer how Terra became so successful? How fast is UST growing compared to its competitors? What risks does the protocol face?

This article attempts to answer how Terra became so successful? How fast is UST growing compared to its competitors? What risks does the protocol face?Original Title: "The Comeback Journey of UST"

Written by: Ben Giove, Bankless Analyst

Compiled by: Nan Feng, Unitimes

In the unpredictable market environment of 2022, stablecoins took center stage.

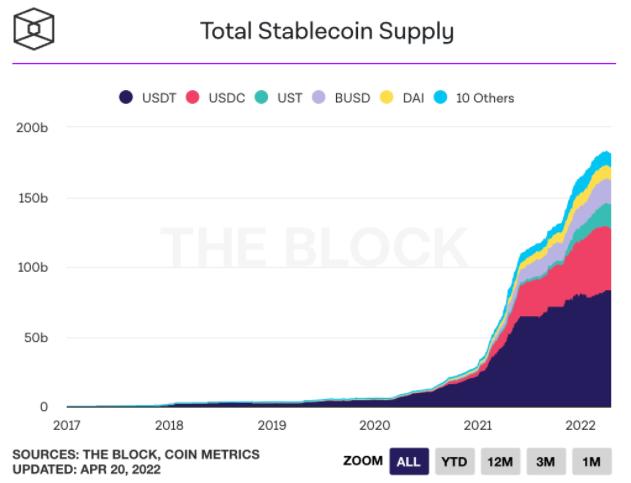

Stablecoins play a very valuable role in the crypto space because they allow holders to retain "cash" within the ecosystem while leveraging the financial superpowers of blockchain and DeFi. Stablecoins are also one of the fastest-growing verticals in the crypto space, with a total market capitalization growth of 115% over the past year and a staggering 2950% increase since January 2020.

Above: Growth of major stablecoin supplies. Source: The Block

Recently, the most notable player in the stablecoin space has been Terra's UST, which is the third-largest stablecoin by market capitalization, with a supply exceeding $17.7 billion. UST is powered by the Terra blockchain and its native asset LUNA, which has grown over 15,100% since early 2021, with a market cap of approximately $34 billion, ranking eighth among all crypto assets.

This certainly raises a question: How did Terra become so successful? How fast is UST growing compared to its competitors? What risks does the protocol face?

The following will attempt to answer these questions.

1: How UST Works

First, let’s dive into UST so we can better understand how it operates, how it achieves stability, and the role LUNA plays in it.

UST is an algorithmic stablecoin pegged to the US dollar. To mint UST, users must burn an equivalent value of LUNA (i.e., $1:$1); similarly, to redeem LUNA, users must burn an equivalent value of UST. This means UST is not backed by external collateral assets but relies on market incentives to maintain its stability.

Let’s understand how this mechanism works through a simple example.

Suppose the price of UST is $1.01, which is above the $1 peg. This indicates that the demand for the UST stablecoin exceeds its supply. In this case, to lower the price of UST, arbitrageurs are incentivized to burn $1 worth of LUNA to mint new UST, capturing the profit from the $0.01 difference between UST's target peg (i.e., $1) and the current price (i.e., $1.01).

When UST trades below the $1 peg, there are similar arbitrage opportunities, indicating that the supply of the UST stablecoin exceeds demand. If UST's price is $0.99, arbitrageurs will be incentivized to burn UST to mint $1 worth of LUNA, pocketing the difference. This will reduce the supply of UST, helping its price rise back to the $1 peg.

While this mechanism is relatively simple, it has proven to be very effective in expanding UST's supply so far.

UST has high capital efficiency because it does not require any collateral support to mint new UST, making it more convenient for supply growth compared to other stablecoin designs (like over-collateralized stablecoins). Stablecoins like DAI, which are based on over-collateralization, rely on the growth of debt demand. This mechanism of UST has also proven to effectively keep UST's price close to its peg, as the protocol's volatility has never exceeded $0.02 since the collapse in May 2021.

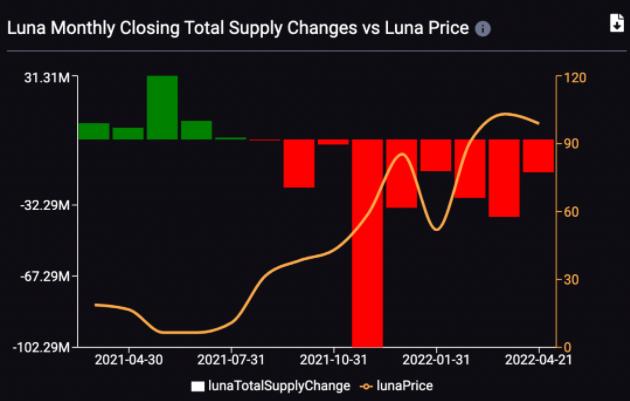

Another key insight from this mechanism is that it links the value of LUNA to the demand for UST. All else being equal, as demand for UST increases, more LUNA will be burned, putting upward pressure on its price. Conversely, if demand for UST decreases, LUNA will be minted to meet user redemptions, putting downward inflationary pressure on its price.

Above: Monthly total supply changes of LUNA (bar chart) vs. LUNA price (yellow curve). Source: Smart Stake

While this mechanism is highly reflexive, it places LUNA in a position of being entirely dependent on the growth of UST demand, leading to LUNA being in a deflationary state for nine consecutive months, as shown in the chart above.

2: LUNA and the Terra Blockchain

As mentioned above, Terra is a stablecoin protocol and also an L1 (Layer 1) blockchain protocol.

The network is built on the Cosmos SDK and uses Tendermint Proof-Of-Stake (PoS) as its consensus mechanism, with validators securing the network by staking LUNA. Terra recently achieved compatibility with IBC (Inter-Blockchain Communication), allowing it to facilitate asset exchanges with all other blockchains in the Cosmos ecosystem.

While the maximum number of validators on Terra is capped at 130, LUNA holders can delegate their assets to validators in the network, allowing smaller holders to participate in the staking process. Unlike other PoS blockchains, LUNA stakers can only earn gas fees and swap fees, as the network does not offer LUNA inflation staking rewards.

Editor’s Note: According to the latest official statement from Terra, all transactions on the Terra network incur gas fees. Additionally, all transactions involving stablecoins incur extra fees, known as swap fees, which include the "Tobin Tax" and "Spread Fee," depending on the type of transaction. Specifically, the Tobin Tax refers to the fee charged by the network for transactions between stablecoins (e.g., swapping UST for KRT) through the Terra protocol, with most stablecoins charging a fee rate of 0.35%, while MNT has a tax rate of 2%; the Spread Fee refers to the fee charged for swaps between stablecoins and LUNA (e.g., swapping UST for LUNA), with a minimum fee of 0.5%. In extremely volatile market conditions, this fee rate is adjusted to ensure the stability of the protocol. These fees are distributed to LUNA stakers in the network as rewards for each block. See: https://docs.terra.money/docs/learn/fees.html

LUNA validators have governance rights over the system, voting on network upgrades and parameter changes. The most recent significant vote was for the Columbus-5 upgrade, where LUNA stakers removed the UST minting tax (i.e., the fee incurred when minting new UST). To reach a quorum for voting, at least 40% of LUNA stakers must participate in the proposal vote, and at least 66.6% of voters must agree for it to pass.

Validators also play another key role in the system, as they are responsible for voting on the exchange rate between LUNA and UST (i.e., the price of LUNA). Terra does not rely on third-party oracle systems like Chainlink but uses LUNA validators as its oracles, incentivizing them to vote correctly on the price of LUNA. In return, these validators receive a portion of the swap fees between UST and other stablecoins, as well as between UST and LUNA.

By using its own sovereign blockchain and an internal oracle network, Terra achieves decentralization, as it does not rely on any external entities to keep the system running.

3: Adoption & Growth Strategies

As discussed by Terra founder Do Kwon, the core idea behind UST's growth strategy is to emphasize creating utility and demand for UST, which helps establish strong network effects.

Here are some strategies Terra has already implemented.

1. Anchor & Terra DeFi

One of the most successful ways Terra has increased the utility and usage of UST is through Anchor. As a money market on Terra and Avalanche, Anchor allows UST holders to deposit UST assets and earn a fixed yield of 19.46% APY. Users can also use staking derivatives of L1 assets from the Terra or Avalanche chains (currently including bLUNA, bETH, bATOM, and wasAVAX) as collateral to borrow UST.

The staking rewards accumulated from these L1 assets, combined with the interest paid by borrowers in the Anchor protocol, help generate part of the 19.46% interest rate paid to depositors in the Anchor protocol, with the difference made up by what Anchor calls the yield reserve, which currently holds over $267 million in UST.

Above: Growth of TVL (Total Value Locked) in the Anchor protocol. Source: DeFi Llama

The deposit yield provided by the Anchor protocol is significantly higher than the typical yields offered by other major money market protocols, which has helped Anchor attract $15.2 billion in TVL, making it the first major demand driver for UST.

However, Anchor may pose risks to UST's stability, as the proposed yield reduction for the protocol and the daily decrease of $4 million in the yield reserve may lead to the reserve being completely depleted in about two months, potentially causing capital outflows from the Anchor protocol and triggering large-scale redemptions of UST.

While Anchor currently accounts for 75.9% of the $20 billion TVL in Terra DeFi, there are other DeFi protocols on the Terra network that also have significant appeal, such as the decentralized exchange Astroport and the synthetic asset protocol Mirror, which together hold over $2.5 billion in TVL. The ability for UST to function within these other Terra-native protocols can help offset potential supply shocks that may occur when Anchor's yield decreases.

2. Aggressive Multi-Chain Expansion

Another way Terra generates demand for UST is by increasing its supply and utility across many other blockchains. By leveraging cross-chain bridge solutions like Wormhole, Terra has successfully established liquidity for UST on networks such as Ethereum, Avalanche, Solana, and Fantom.

Particularly on Ethereum, Terra has achieved significant integration, which could make UST one of the largest stablecoins on the Ethereum chain, with UST's supply on the Ethereum network exceeding $755 million at the time of writing.

For example, Terra recently announced a proposal to create a 4pool on the decentralized exchange Curve, which will consist of four stablecoins: UST, FRAX, USDC, and USDT. This pool aims to become the foundational trading pool for this DeFi's most liquid DEX (i.e., Curve), replacing the current foundational pool 3pool (composed of DAI, USDC, and USDT).

Terra and Frax, the two major stablecoin issuers, are collaborating with the [Redacted] Cartel on the 4pool initiative, and at the time of writing, they collectively hold a significant amount of CVX tokens, which are the governance tokens of Convex Finance, controlling the vast majority of Curve's native token CRV. As a result, the 4pool has already launched on the Fantom blockchain, where it has over $31 million in TVL, and it seems to have a solid opportunity to change the competitive landscape of Curve liquidity.

In addition to Curve, Terra has begun integrating with other Ethereum DeFi protocols, such as Rari Capital's Fuse, which is a permissionless money market protocol where Terra is injecting UST liquidity into the Fuse pool.

3. Forex Reserve Fund

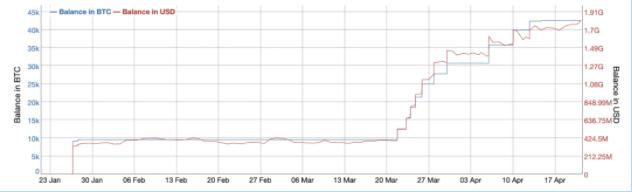

Another recent factor driving Terra's growth is the establishment of the "Forex Reserve" fund. The Terra ecosystem development organization Luna Foundation Guard (LFG) announced on February 23, 2022 (see below), that this nonprofit organization has raised $1 billion by selling LUNA tokens from major entities like Three Arrows Capital and Jump Crypto, aiming to accumulate Bitcoin (BTC) as a backing to help maintain UST's peg.

At the time of writing, the reserve fund currently holds over $1.81 billion in BTC, with a goal of ultimately reaching $10 billion and diversifying into other crypto assets, such as starting a $100 million LUNA/AVAX token swap with Avalanche's developers Ava Labs. This means that as of now, UST has received support from 15-16% of other crypto assets.

Above: Growth of BTC held by the Luna Foundation Guard (LFG) address. Source: BitInfo Charts

The reserve fund has helped support its price in the cryptocurrency market and has driven demand for UST, likely due to boosting confidence in UST's ability to maintain its peg and meet redemption demands, as UST's market cap has grown by 45% and LUNA's price has increased by 81% since the announcement of the reserve fund's creation.

4: The Status of UST

Now that we understand how UST operates and the drivers behind its adoption, let’s look at some on-chain metrics to see how this stablecoin compares to its competitors.

1. Circulating Supply & Market Share

UST's supply has experienced an incredible explosive growth over the past year, increasing by over 987%, with its circulating supply exceeding $17.7 billion at the time of writing. As shown in the chart below:

Above: Growth of UST stablecoin supply over the past year. Data Source: The Block

This makes UST the third-largest stablecoin, behind USDT and USDC. Considering that the other two stablecoins (i.e., USDT and USDC) are backed by fiat reserves and issued by centralized entities, this makes UST the largest decentralized stablecoin in all of cryptocurrency, with a scale more than double that of its closest competitor, DAI.

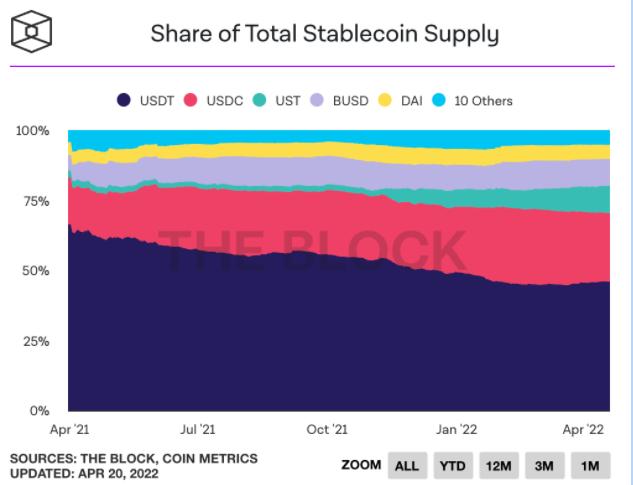

UST's market share has surged dramatically over the past two quarters. The protocol currently accounts for 9.8% of the total stablecoin supply, an increase of more than four times from 2.1% since October 2021. As shown in the chart below:

Data Source: The Block

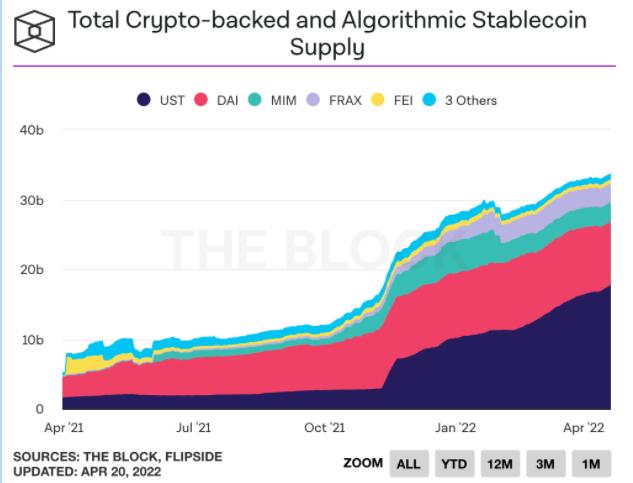

UST's competitive positioning relative to other decentralized stablecoins highlights its astonishing market share growth. According to The Block, UST accounts for the majority of the decentralized stablecoin supply: UST's supply makes up 52.7% of the total supply of $33.6 billion among the eight largest crypto-backed stablecoins and algorithmic stablecoins. This is more than double the 19.9% it held in October 2021. As shown in the chart below:

Data Source: The Block

2. Growth Rate

As indicated by its growing market share, UST has been growing at a faster rate than its competitors. A closer look at these growth rates reveals just how significant the differences are.

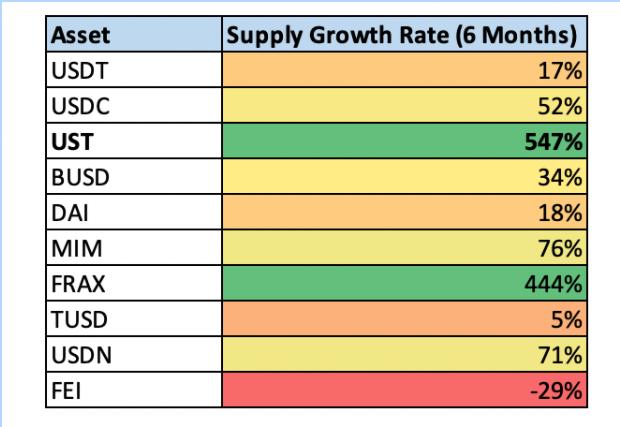

The chart below shows the supply growth rates of the top ten stablecoins by market capitalization over the past two quarters, including centralized stablecoins, decentralized stablecoins, fiat-backed stablecoins, crypto-backed stablecoins, and algorithmic stablecoins. As we can see, UST's growth rate over the past six months has far outpaced the other ten stablecoins, with its supply growing by 547%. During this period, only two stablecoins expanded at a rate exceeding three digits, the other being FRAX.

Data Source: CoinGecko

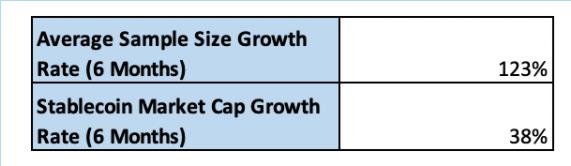

This means that UST's growth rate over the past six months has been 4.4 times faster than the average growth rate of the ten selected stablecoins and 14 times faster than the overall growth rate of the stablecoin industry.

Data Source: CoinGecko

In this rapidly expanding and long-term growth stablecoin space, UST has proven itself to be the fastest horse.

5: Risk Factors

Now that we have highlighted UST's tremendous growth and the keys to its success, let’s take some time to emphasize some risks the protocol faces.

1. Inflationary Death Spiral

Perhaps the biggest risk Terra faces is the so-called "death spiral," similar to what has occurred with stablecoins like Iron Finance. This situation includes a run on UST (i.e., large-scale redemptions), often resulting from the stablecoin trading below its peg, which other algorithmic stablecoins have encountered. If this occurs, LUNA will be minted at increasingly higher prices, causing more UST holders to lose confidence and further inflate the supply of the asset until it loses all value.

2. Limited Number of Validators

As mentioned above, the degree of decentralization of UST depends on the Terra blockchain network that protects this stablecoin. Given that Terra only supports 130 validators, this could be a centralization vector if the protocol faces significant regulatory scrutiny.

3. Anchor Yield Reduction

If the deposit yield at Anchor decreases, leading to outflows of UST from the Anchor protocol, then the stablecoin will face redemption risks. If UST holders choose to allocate their funds elsewhere, it could trigger inflation.

4. Competition

The competition in the stablecoin space is fierce. Terra will need to continue developing and iterating on the protocol and build its network effects to defend its competitive position.

6: Conclusion

As the largest decentralized stablecoin, UST has swept through the crypto world. With the local asset LUNA accumulating value through market demand for UST, along with an aggressive strategy that drives demand, utility, and builds network effects with astonishing growth rates, Terra seems poised to continue its lunar advantage.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles