Lightspeed India, Southeast Asia's Web3布局

Does the transition of the internet from Web 2.0 to Web 3 mean that many current aspects of working through the internet need to be rebuilt for Web 3?

Does the transition of the internet from Web 2.0 to Web 3 mean that many current aspects of working through the internet need to be rebuilt for Web 3?Source: Insights from LightSpeed India Partners

Compiled by: Alpha Rabbit

Original link: ([https://medium.com/lightspeedindia/lightspeeds-india-sea-crypto-landscape-7038eaa473e](Original link: https://medium.com/lightspeedindia/lightspeeds-india-sea-crypto-landscape-7038eaa473e))

In 2020, from the perspective of the crypto market, the overall market was on an upward trend, especially in September, where investors from markets such as the US, India, Southeast Asia, and South Korea played a certain role in driving the market, with BTC prices peaking in October 2021. The global monthly trading volume of crypto also saw a significant increase in 2021, rising from $27.1 billion in Q1 2020 to $79.3 billion in Q4 2020, peaking at $X billion in May 2021, as shown in the figure below.

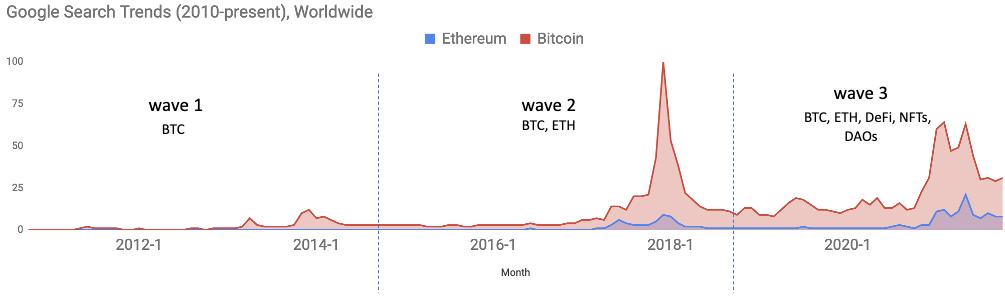

Historically, observing the cryptocurrency ecosystem, the market has experienced peaks and undervaluation, having gone through two waves, which included much speculation and noise. Currently, at the end of 2021, I believe we are in the midst of a third wave. However, one point to note is that throughout this historical process, beneath all the speculation and noise, there has been a meaningful ecosystem quietly and gradually maturing.

Therefore, over the past few years, we believe that opportunities in the crypto space have expanded into other areas. Specifically, we see a range of highly diversified opportunities, including region-specific opportunities, as well as NFTs, gaming, DAOs, DeFi, wallets, blockchain infrastructure, and many more. Overall, new changes are emerging, such as shifts in the attitudes of capital, talent, and regulatory bodies in certain regions towards this rapidly rising field, indicating that we are entering a new phase.

- From the trend of global capital markets, more capital is flowing into Web3 than ever before, with large global companies gradually raising significant funds. For example, FTX ($1.3 billion), BlockFi ($350 million), Paxos ($300 million), Blockchain.com ($300 million), and BitSo ($250 million). Regional leaders like Pintu in Indonesia ($35 million), CoinDCX in India ($110 million), and CoinSwitch ($300 million) also raised substantial funds in 2021.

Globally, over $8 billion in investments flowed into cryptocurrency and blockchain companies in the first half of 2021, compared to only about $400 million for the entire year of 2020. This expansion is partly due to the diversification of capital regions and institutions, particularly with a strong growth in funding in India, where crypto founders raised over $500 million by November 2021, compared to only $37 million in 2020.

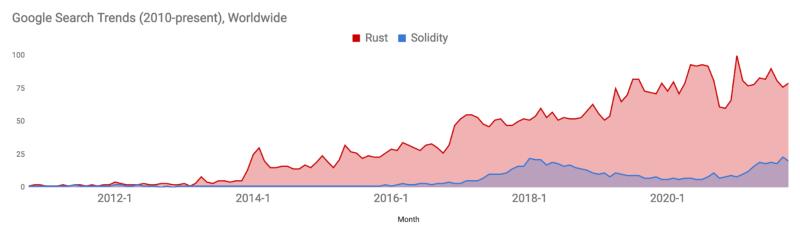

- In terms of talent, the Web3 space is beginning to attract experienced and new developers, allowing for more and higher quality code to be written in a shorter time frame. Globally, the development of Rust and Solidity is generally positive, and notably, India has become a breeding ground for blockchain talent.

On LinkedIn, there are currently over 10,000 "Blockchain Developer" job vacancies in India, compared to 30,000 in the US. A few years ago, this number was only over 100.

- In countries and regions such as the US, Asia, India, and Indonesia, regulation in the crypto space has become an important focus for mainstream institutions. In India, the regulatory environment in 2021 is different from that in 2018, when cryptocurrency exchanges faced scrutiny. However, current players like CoinSwitch and CoinDCX have begun to invite Bollywood stars as brand ambassadors. Indonesia has taken a stance on planning a regulatory framework for crypto, and the Indian Supreme Court's attitude towards the crypto space has also seen some changes.

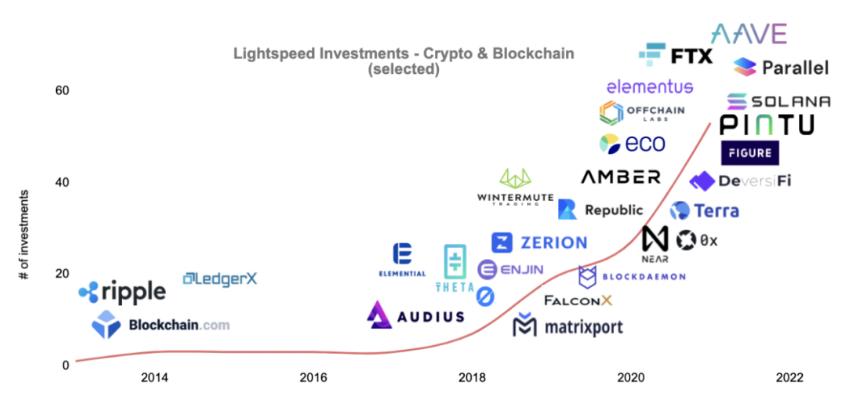

LightSpeed India has been active in this category since 2013, starting its crypto investments with Blockchain.com. Blockchain.com is a leader in global crypto services and a leading BTC wallet, accounting for over 35% of all BTC on-chain transactions.

Since then, LightSpeed India has directly or indirectly invested in over 50 leading companies, covering all categories of Web3 projects, including brokers, market makers, and exchanges worldwide, such as Pintu, Amber, Wintermute, and FTX; DeFi products like Aave, 0x, Zerion, and Parallel; as well as L1 and L2 solutions like NEAR, Theta, Terra, OffChain Labs/Arbitrum, and more.

LightSpeed is a global investor, but this article will focus on LightSpeed's specific work and market map in India and Southeast Asia, which are among the most active places for crypto and blockchain technology. While advanced crypto economies like the US are shifting from retail trading to more institutional trading, there is still significant room for Peer-to-Peer trading provided solely by DEXes (decentralized exchanges) and CEXes (centralized exchanges) in emerging cryptocurrency markets.

Certain regions have many favorable conditions, including currency depreciation and poor stock market performance over the past few years, leading many young people to choose emerging fields. According to Chainanalysis's 2021 Global Crypto Adoption Index, Vietnam and India ranked first and second, respectively, with Pakistan, Thailand, and the Philippines also in the top 15.

Blockchain Infrastructure

The core feature of blockchain is essentially a unique database, and additionally, immutability, trustworthiness, open-source, and openness are characteristics of blockchain. Therefore, they encounter similar issues as other databases: scalability, security, performance issues, etc.

However, in the early stages of blockchain development, we could only write a few transactions to the blockchain ledger per second. As the ecosystem has expanded, the speed has significantly increased, and today, each new transaction on the main Layer 1 is much faster, indicating development and progress.

Moreover, during periods of on-chain congestion, the cost of each transaction (the "GAS fee") increases. To address this issue, many companies are developing new Layer 2 and sidechain solutions that batch write transaction data to the main blockchain. This approach helps reduce congestion and lower gas fees. Polygon and Arbitrum are examples of L2/sidechain solutions within the Ethereum ecosystem.

While L2 addresses the scalability and cost issues of the underlying L1 blockchain, some new L1s are also being established to meet different needs running on the blockchain.

Today, Ethereum has the largest developer community and user stickiness in the world, with around 400 applications built on Ethereum by the end of 2021. However, as other Layer 1s continue to attract developers to build applications on their networks, this, in turn, will continue to draw users into new networks.

Binance Smart Chain (BSC), Solana, Avalanche, and Cosmos. Each L1 blockchain architecture has unique advantages; Ethereum was the first open-source blockchain to offer smart contract functionality and has optimized for security; Polkadot has optimized for cross-chain communication; BSC has optimized for low fees; Avalanche has optimized for time-to-finality; and Solana has optimized for high transaction volumes.

Other specialized use cases, such as blockchain gaming (or "NFT gaming"), also necessitate the development of dedicated L1s. For example, Axie Infinity: a popular gaming company based in SEA recently relaunched their game from Ethereum to their own sidechain, Ronin, to reduce transaction fees and improve performance (Note: despite some recent issues with Ronin, this innovative exploration cannot be denied).

Insights from LightSpeed India Partners

L1 alternatives and L2 solutions, along with other components of Web3, are key areas of infrastructure that can bring more interesting cases to the blockchain.

As different L1s and L2s scale, a broad blockchain infrastructure/middleware and development tools will build a true ecosystem that can provide integration for the mutual transfer of assets, information, and communication. This is also currently one of the most active areas for investment.

With the transition of the internet from Web 2.0 to Web 3, does this mean that many parts currently working through the internet need to be rebuilt for Web 3?

Does this mean we need to rebuild the entire web 2.0 stack? From all the hardware, to storage and network infrastructure, operating systems, databases, middleware, and finally applications?

Perhaps not necessarily, but we will certainly need a hybrid architecture of general and special-purpose designs to allow Web 3 products to gradually evolve from Web 2.0. We have already seen many innovations in the database layer of Web 3—L1 and L2. In terms of storage, Web 3 is moving towards decentralized platforms like Filecoin, Arweave, and Arcana Network. Various parts of network infrastructure are gradually becoming decentralized. For example, ENS and Handshake are building decentralized DNS. Applications like Audius, BitClout, and Braintrust are respectively building decentralized versions of Spotify, Twitter, and Upwork.

Blockchain infrastructure is the core and key opportunity for building this emerging ecosystem. With the token/economics of the crypto space, it is finally possible to adjust incentive mechanisms across all levels of Web 3 and address trust and quality issues in a decentralized manner. We look forward to seeing innovations of this kind:

For example:

How can analytics and artificial intelligence be brought into effective decentralized (and often crypto) datasets?

How do we search and index this new world?

How do we solve distribution issues?

Every user in Web 3 now holds dozens (or hundreds) of tokens in a range of wallets, with complex passwords, and uses dozens of dApps?

How many communities and DAOs can one person actually participate in?

These are some fundamental questions that will be answered in the next decade, and we will firmly support founders who are tackling these challenging challenges.

About NFTs

One of the simplest ways to understand NFTs: a blockchain-native file format, but it further inherits the typical attributes of blockchain assets: ownership, earliest ownership/transaction flow records, and the value lineage associated with the asset— all of which are public and transparent.

NFTs can be seen as a way to tokenize various digital and physical assets and place them on the blockchain, characterized by NFTs being a new way for people to showcase in the digital world.

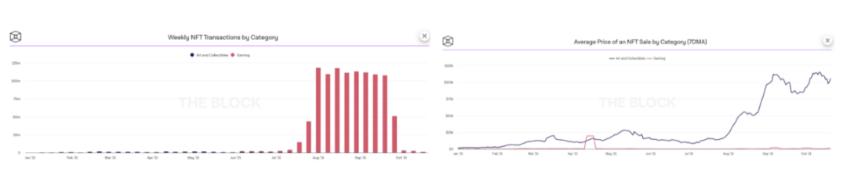

NFTs have existed since 2015, but the market has recently become quite lively. OpenSea, the world's largest NFT marketplace, surpassed $10 billion in cumulative trading volume in October 2021. Notably, OpenSea only crossed $1 billion in cumulative trading volume in July 2021, marking an astonishing growth. Typically, we see NFTs being used in digital art (created and generated by artists), pop culture (old memorabilia sold as NFTs), sports moments (top shots from the NBA), gaming, and even life experiences (creators recording unique one-off videos for fans). As shown in the figure, while NFT trading volume was initially dominated by art/collectibles, recently, gaming-related NFTs have begun to see strong applications within the NFT community.

This may be one of the most interesting consumer applications emerging in the NFT ecosystem. Games like chain games (or "P2E" games) combine blockchain technology, allowing players to mint and trade in-game items as NFTs. You can then trade these NFTs on-chain within the game or even trade them on DEX or CEX through tokenization.

While most trading volume of art NFTs is related to a few high-priced and sought-after NFTs/NFT collectibles, so far, gaming NFTs have accounted for a significant share of trading volume, despite their lower average prices. It is precisely this mass appeal and accessibility of gaming NFTs that excites the entire market.

While early blockchain games like Gods Unchained (ImmutableX), Crypto Kitties (Dapper Labs), Decentraland, and The Sandbox achieved varying degrees of success in NFT/token sales, player engagement was generally low. However, chain games reached mainstream attention with the explosive growth of Axie Infinity, a Pokémon Go-style collectible game.

In June 2021, Axie Infinity reached a turning point, with a growing community of gamers from the Philippines gaining attention on streaming platforms like Twitch. Most importantly, the team decided to relaunch the game from Ethereum to their own sidechain called Ronin to reduce transaction fees and improve performance. Beyond Axie, companies like SoRare have already leveraged NFTs to create a new example in gaming, unlocking player rewards and earnings through the potential capital appreciation of collected NFTs.

Insights from LightSpeed India Partners

In the past few quarters of 2021, the entire NFT ecosystem has seen tremendous growth. We are excited about the changes brought about by the increased interest and liquidity from creators/artists, gamers, and crypto enthusiasts in this category.

To drive the development of the ecosystem, there is a need to enhance the one-click experience, enabling the next billion users to easily create, mint, and roam in the NFT world, whether through tools that generate NFT income or integrating interesting uses of NFTs in the real world, while protecting users from NFT fraud/phishing attacks, and building NFT SaaS tools that allow brands to build communities and connect with their audiences.

In the realm of NFT gaming, considering labor arbitrage, various "P2E" use cases are emerging, particularly important for the Indian and Southeast Asian markets. Platforms like Yield Guild are taking an early lead in establishing P2E movements. Just as the transition from Web 2.0 to Web 3 is happening, we believe there will be a shift from centralized gaming to decentralized gaming in the next decade, requiring a rethinking of various parts of the gaming stack. Starting from the game engine itself—games like Ember Sword have built their own game engines—down to various plugins for cryptocurrency economics, marketplaces, guilds, NFT integrations, and more.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles