IOSG Report: Rollup Empowers a New Financial System

The pace of DeFi innovation has slowed down, giving us the opportunity to reflect on the development of DeFi over the past five years and to discuss the theoretical framework for the future development of DeFi in the context of a multi-chain narrative.

The pace of DeFi innovation has slowed down, giving us the opportunity to reflect on the development of DeFi over the past five years and to discuss the theoretical framework for the future development of DeFi in the context of a multi-chain narrative.Author: Momir Amidzic, IOSG Ventures

TLDR

- After five years of rapid development, winners in various tracks are gradually emerging, and the DeFi market has made significant progress.

- Due to a lack of new narratives, most public chains are essentially just replicating Ethereum's DeFi landscape. Multi-chain DeFi can be considered a new narrative direction.

- Despite the claims of multi-chain and the saturation of Ethereum, activities on other chains are gradually increasing, but whales still have a strong preference for security. The TVL of the largest protocol on Ethereum, Curve.fi, is greater than the total TVL of all DeFi applications built on Avalanche and Solana.

- On the other hand, because these multi-chains can offer lower transaction fees, some users who cannot afford Ethereum's costs are gradually migrating to these chains. However, the contributions these users can provide are still not substantial enough.

- It is clear that currently no single blockchain can handle the throughput of all DeFi applications.

- In the long run, we expect that most applications will be built on Rollups, as this is the only solution that can sustainably support billions of users without sacrificing fundamental principles such as decentralization, censorship resistance, security, and trustlessness.

The slowdown in DeFi innovation gives us an opportunity to reflect on the development of DeFi over the past five years and to theorize the future development path of DeFi in the context of multi-chain narratives.

From Birth to Development

Over the past five years, the DeFi ecosystem on Ethereum has experienced explosive growth.

2017-18 can be called the first year of DeFi, with leading DeFi protocols in the market, such as Uniswap, Compound, AAVE, dYdX, emerging during that period. However, these protocols began to gain market attention in 2020 (dYdX started in 2021).

Source: IOSG Ventures

From today's perspective, the use cases of DeFi mainly include three types:

- Spot trading on decentralized exchanges

- Lending and borrowing

- Derivatives

Spot Market

Currently, the spot trading market on Ethereum is very saturated, with most trading activities concentrated in leading projects, making it very difficult for newly entering protocols. From the initial experiments, such as on-chain order book models, to later constant product market makers (CPMM), various new mechanisms have replaced them:

- Concentrated liquidity AMMs, led by Curve.fi for stablecoin trading, and later DODO, Uniswap v3, Curve v2 applying concentrated liquidity models to non-stablecoin assets. (Of course, each protocol has its design differences)

- AMMs supporting more than two assets, such as Balancer's constant mean market maker

- Automated market makers with impermanent loss protection, such as Bancor

- Constant product market makers, such as Uniswap v2 and Sushiswap

- DEXs that prevent MEV

- DEXs tailored for retail or whales, etc.

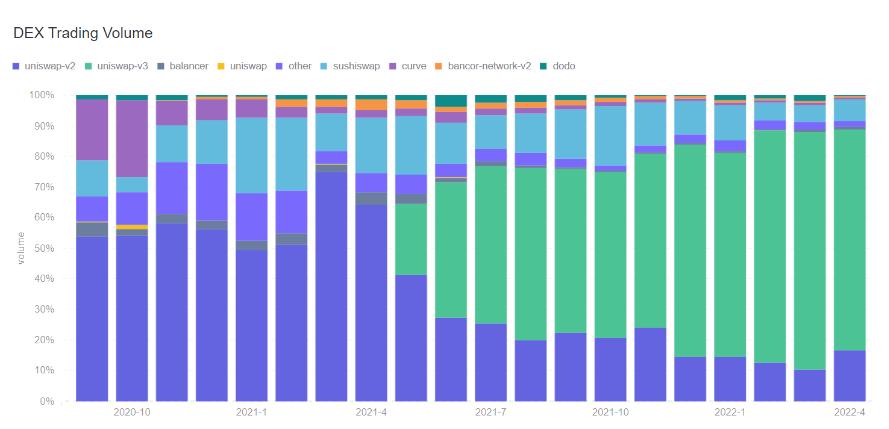

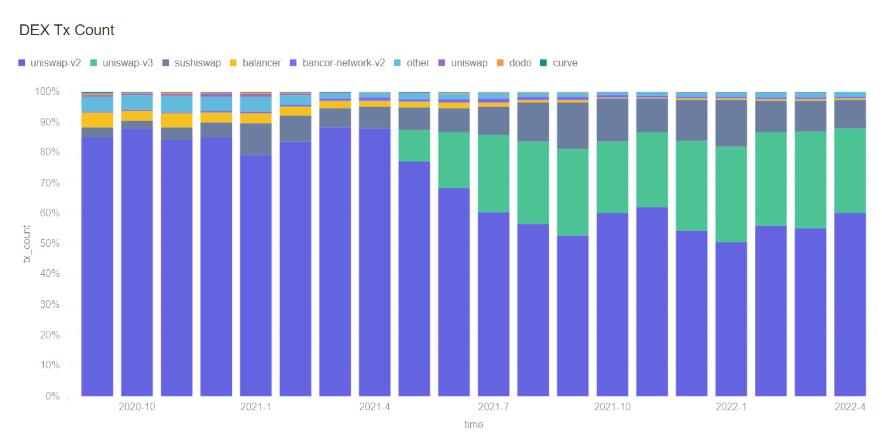

Looking back, until the end of 2020, investing in Ethereum's spot DEX was a great opportunity. Starting in 2021, several excellent teams began to enter this field. However, as more and more ideas materialized, innovation development seemed insufficient to capture a larger market share.

The launch of Uniswap v3 and Curve v2 further raised the entry barriers, "killing many projects that aimed to build DEXs from scratch in the cradle."

Source: IOSG Ventures, Footprint Analytics

(https://www.footprint.network/chart/DEX-Trading-Volume-fp-17021)

Source: IOSG Ventures, Footprint Analytics

(https://www.footprint.network/chart/DEX-Tx-Count-fp-17022)

Capital Market

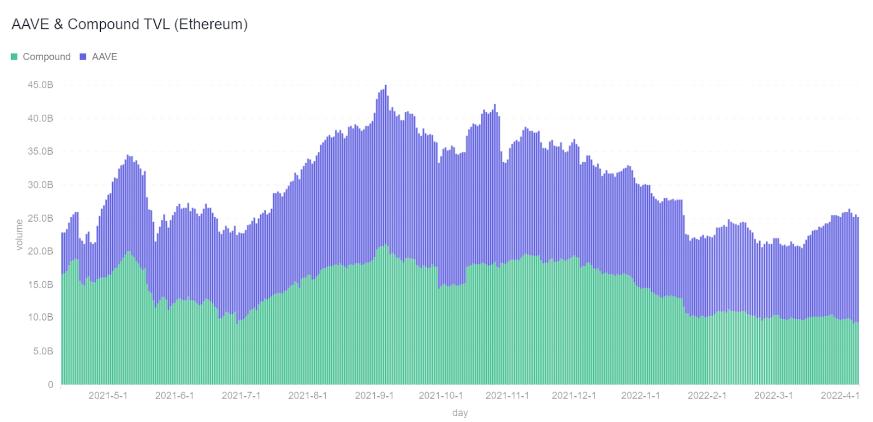

Because liquidity providers do not need to make directional judgments and can earn returns while protecting their principal, protocols in the capital market are very important for liquidity providers. In lending protocols, two projects stand out: Compound and AAVE, with a combined TVL on Ethereum exceeding $25 billion.

Source: IOSG Ventures, Footprint Analytics

(https://www.footprint.network/chart/AAVE-%26-Compound-TVL-(Ethereum)-fp-17026)

Compared to spot trading DEXs, the gameplay of lending protocols is still to be explored. New protocols can stand out by offering more customized terms through lower collateral ratios, combining DiD and credit scoring, dynamic parameter updates, and more diverse collateral (such as NFT collateral).

Recently, Euler and Beta Finance have made corresponding attempts to provide any borrowable assets in a permissionless manner. The practical effect of this measure will enable traders to short more altcoins.

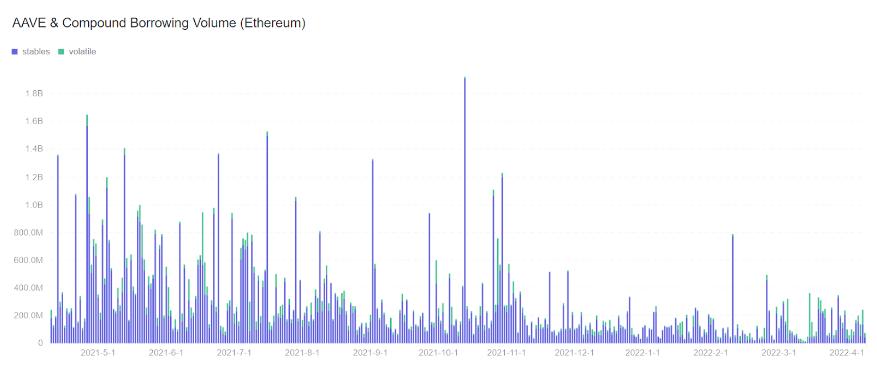

Nevertheless, the behavior of borrowers in the capital market indicates that users are mainly interested in borrowing stablecoins against their collateral, essentially leveraging lending protocols to trade altcoins. This means that rather than supporting more types of assets, DeFi projects should introduce more diverse collateral without increasing systemic risk. AAVE v3 and Silo Finance have already publicly announced plans for such developments in the future.

Source: IOSG Ventures, Footprint Analytics

(https://www.footprint.network/chart/AAVE-%26-Compound-Borrowing-Volume-(Ethereum)-fp-17025)

Synthetic Assets

Broadly speaking, synthetic assets encompass several important directions, such as financial derivatives, synthetic real-world assets, and stablecoins.

When it comes to derivatives, few other protocols can rival dYdX, even though these protocols have just launched their latest versions. Moreover, many of these protocols rely on scaling solutions, which themselves are not fully mature.

Similar to spot DEXs and lending protocols, they took two to three years to achieve broader market adoption. Derivatives exchanges established in the past 12 months may achieve similar accomplishments within the next 12-24 months, provided that the tech stack matures and the protocols find the right product-market fit.

Finding product-market fit for synthetic real-world assets (RWAs) is also challenging, despite the narrative being based on democratizing the U.S. stock market and commodity markets. Only when the timing is right, meaning when DeFi has a more diverse user base, can these decentralized futures protocols potentially realize on-chain RWAs.

Lastly, decentralized stablecoins remain a direction that continues to attract attention from top talent. The failures of many algorithmic stablecoins have not deterred new protocols from trying to establish more mature stablecoin systems.

Recently, some noteworthy (but not necessarily successful) attempts in the direction of synthetic assets include:

- dYdX Starknet exchange

- SQUEETH on Opyn

- Liquity's zero-interest synthetic stablecoin

- FEI's POL-based stablecoin

- Primitive's copy trading market maker

- Ribbon's options vault

- Perpetual Protocol v2

- SynFutures & MCDEX's permissionless futures AMM

- Deri's perpetual options

- Pods Finance's permissionless options AMM

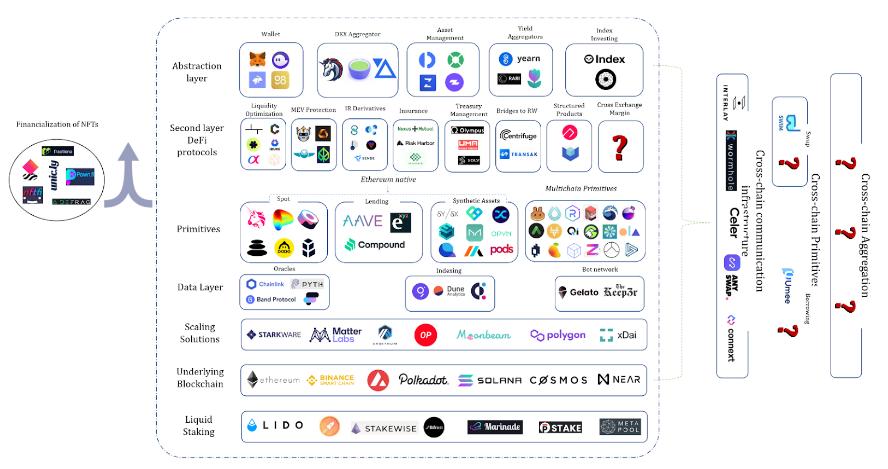

Layer 2 DeFi Protocols

In the Ethereum DeFi ecosystem, compared to other L1s or sidechains, L2 DeFi protocols have taken the stage in 2021. They are defined as L2 because they are based on composability, without which underlying DeFi projects cannot exist.

Some DeFi L1 projects, such as Uniswap, AAVE, Opyn, and Synthetix, have their ecosystems and attract a large number of protocols built within them.

For example, Uniswap v3 introduced the need for active liquidity management, leading to the development of a series of protocols aimed at optimizing liquidity supply while allowing end users to enjoy passive income. Some examples include Gelato's G-UNI, Charm's Alpha vaults, Visor Finance, Teahouse, etc. Similarly, Izumi Finance is also building tools to help protocols launch liquidity mining incentive mechanisms based on Uniswap v3 and achieve ideal liquidity distribution. These tools are not only important for launching new tokens but also have a profound impact on protocols like Perpetual Protocol v2 and Sense Finance that use Uniswap v3 as a base layer, aiming to provide incentives for liquidity providers to achieve efficient market making.

Other noteworthy protocols include Tokemak and Convex, which are built on the foundation of the spot market. The former is trying to position itself as a meta liquidity aggregator, while the latter is part of the Curve.fi ecosystem and one of the largest shareholders of the CRV token.

In Layer 2 protocols, we can also categorize interest rate derivatives built on lending protocols: insurance protocols that provide TVL guarantees for other applications, tools that help DAOs effectively manage funds, MEV tools, DEX aggregators, structured products, etc.

DeFi Map; Source: IOSG Ventures

Creating Sustainable Yields

Structured products made their first breakthrough in 2021, mainly due to Ribbon Finance. Ribbon built an options vault on Opyn, regularly underwriting options and providing passive income to its liquidity providers. Ribbon's success has inspired some teams to build in this direction; however, the vast majority are merely copying Ribbon's options vault. Therefore, structured products remain an undeveloped area with enormous potential. We expect the development of structured products to expand from merely underwriting options to encompassing various DeFi foundational use cases, such as lending markets, interest rate derivatives, perpetual futures, options, etc.

Ribbon Finance TVL; Source: defillama.com

For example, Vovo Finance aims to eliminate reliance on centralized market makers and build capital-protected products based on existing spot and derivatives exchanges. As mentioned, lending protocols have attracted billions of dollars in funding because they offer stable yields without threatening the principal of liquidity providers. Therefore, due to the protection of principal, Vovo has the potential to attract a large amount of TVL while allowing users to earn returns.

Finally, structured products have broader implications and significance for the entire DeFi economy, as the increasing capital supply in DeFi protocols lowers yields. For instance, at the time of writing this report (mid-April 2022), the APY of stablecoins on Compound and AAVE was generally below 3%. The APY of Curve.fi's 3pool was estimated to be around 0.5%, while including CRV mining rewards, it was 1.18%.

Since the above protocols represent the DeFi version of risk-free rates, it is no wonder that capital has been flooding into their smart contracts, driving yields down to levels comparable to those offered by TradFi banks.

With the current level of activity in DeFi, the opportunity to absorb more new capital inflows is relatively limited.

Federal Funds Effective Rate, Historical Data;

Source: https://fred.stlouisfed.org/series/FEDFUNDS

What happens when central banks begin to tighten monetary policy? Assuming that most of the new capital entering DeFi in 2021 in search of yields is institutional, the increase in interest rates will make the current TVL of DeFi unsustainable, leading to a significant outflow of capital to the off-chain economy.

To maintain its current TVL level, DeFi must find additional sources of yield.

Currently, DeFi yields mainly come from the following activities:

- Spot trading (earning yields by providing liquidity to spot DEXs)

- Demand for leveraged long positions (lending protocols, perpetual contracts).

- Short selling demand (lending protocols, perpetual contracts)

- Yield farming, such as borrowing a specific token required by yield farming protocol X while still maintaining exposure to the collateral.

- Others (establishing Ponzi economies to generate yields, supporting operations through collateralized loans, etc.).

Structured product protocols have the opportunity to explore new markets, such as the options market, foreign products, and potential new primitives, which can attract more trading demand to decentralized financial markets, thus having the ability to absorb more TVL (or at least maintain the current TVL level) even in a tightening monetary policy environment.

Multi-chain DeFi

Multi-chain expansion has been a highlight of 2021, with BSC, Polygon, Terra, Avalanche, and Solana dominating the discussion. While most of these chains position themselves as competitors to Ethereum, the leadership and community of Polygon chose to support the narrative of "backing Ethereum," even announcing an ambitious promotional roadmap and positioning itself as one of the leaders in the modular blockchain approach.

The main driver of multi-chain expansion is the slow progress of Ethereum's native scaling solutions, which has opened a window of opportunity for competitors/sidechains to capture some market share.

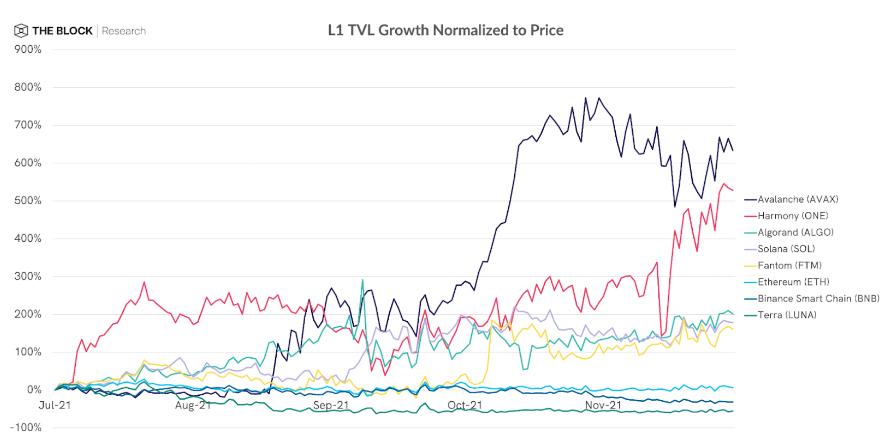

While TVL is most widely used to explain activities on a single chain, this metric also has certain flaws. Because TVL typically refers to the amount of native tokens locked on a specific L1, the appreciation of the token's price naturally leads to an increase in TVL, which further causes speculators to drive up token prices.

As The Block explains below, Avalanche has the highest influx of fresh capital.

Source: The Block

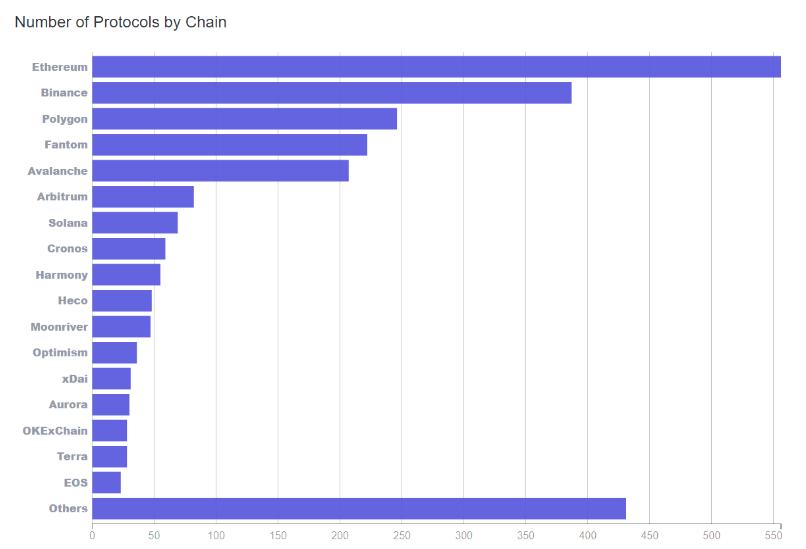

Despite increasing activities on other chains, Ethereum remains the dominant solution when it comes to absolute TVL and the number of dApps built on it. Intuitively, we can see that the total TVL of Curve (the largest Ethereum protocol) is greater than the combined TVL of all applications built on Avalanche and Solana.

Source: Footprint Analytics

(https://www.footprint.network/guest/chart/Number-of-Protocols-by-Chain-fp-66347dc7-530f-43c5-a9f5-80227f1ff432)

The development progress of other chains lags behind Ethereum by more than 12 months. To prove themselves safe enough to large capital providers, new chains will have to withstand the test of time. If we compare the stablecoin yields on Solana and Ethereum, the risk comparison becomes evident. For example, Solana's largest money market protocol, Solend, offers APYs on USDC and USDT that are 2-3 times greater than AAVE. This gap indicates that the implied risk premium of interacting with new protocols on a new chain is significant.

Any chain seeking to compete with Ethereum must rebuild the Ethereum DeFi map. Therefore, while the Ethereum DeFi ecosystem has been exploring new primitives and vertical construction, most other L1s have been replicating the Ethereum DeFi map.

If we observe the market capitalization of DeFi tokens, Ethereum DeFi's dominance is also very evident, with only 4 out of the top 20 token assets being non-Ethereum.

The identity of a pioneer in decentralized applications has helped Ethereum accumulate soft power. As a result, all alternative L1s have adopted EVM compatibility in various forms, such as Avalanche's C chain, Polkadot's Moonbeam, NEAR's Aurora, Solana's Neon, Fantom, Polygon, BSC, etc.

Multi-chain dApps

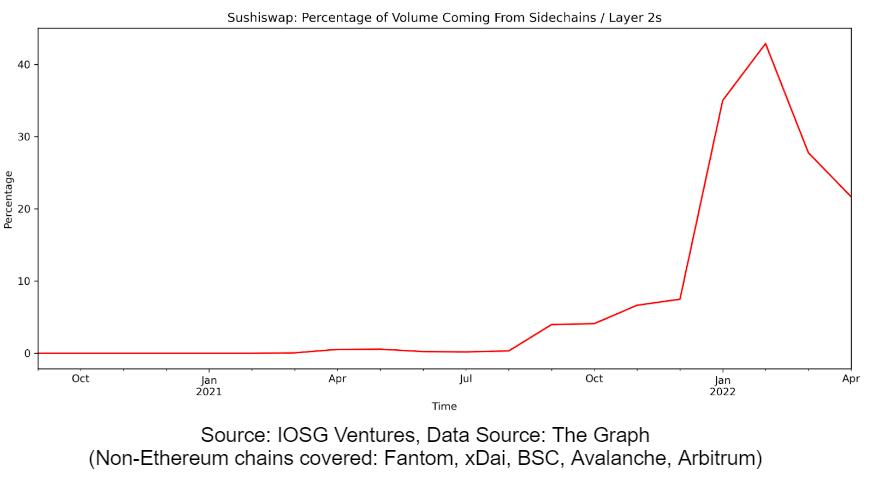

The emergence of capital-rich EVM-compatible chains has led to the expansion of Ethereum-native applications in multiple aspects. Sushiswap was the first protocol to advocate for aggressive expansion.

Sushiswap has appeared on more than 15 chains, yet it has struggled to become the dominant DEX in new ecosystems. Generally speaking, DEXs that focus solely on a specific chain tend to attract more interest. Therefore, Pancake Swap, Trader Joe, Quick Swap, and SpookySwap are positioned as the top DEXs on BSC, Avalanche, Polygon, and Fantom, respectively, while Sushi usually ranks second. This is because each of these protocols focuses only on a specific chain, allowing them to concentrate all resources, including new token rewards, to attract users and build communities on the new chains, while Sushiswap has diluted its attention across many venues.

Nevertheless, we can still say that the expansion strategy is the right choice for the Sushiswap community. Over 30% of Sushiswap's TVL is outside of Ethereum L1, and their flexible strategy has helped them become some of the largest DEXs on new chains, such as Moonriver and the leading protocol on Ethereum L2 solutions—Arbitrum. Ultimately, a significant portion of Sushiswap's trading volume comes from outside Ethereum L1; for instance, in February, about 50% of the trading volume was generated on other chains.

Source: IOSG Ventures, Data Source: The Graph

(Non-Ethereum chains covered: Fantom, xDai, BSC, Avalanche, Arbitrum)

Have scalability solutions delivered on their promises?

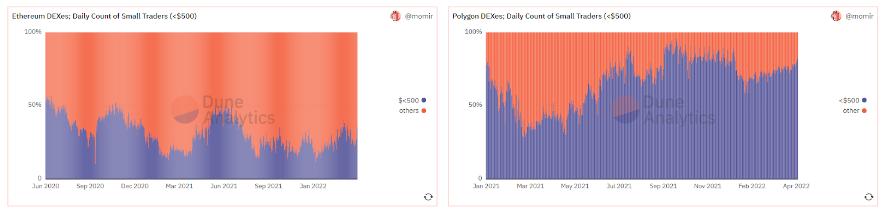

The main promise of scalability solutions is to make blockchains usable for everyone. To test the extent to which alternative chains have achieved this goal, we observed activities on Polygon.

We used $500 as the threshold to determine small traders and monitored how many traders fell into this category daily.

The chart below indicates that Polygon has indeed succeeded in attracting a new audience, with the majority of Polygon users (about 80% of traders) executing trades of less than $500 daily, while the representation of the same user group on Ethereum is much lower, typically below 30%.

Source: IOSG Ventures, Dune Analytics

(https://dune.xyz/momir/DEX-Users)

Based on the example of Polygon, we can confidently answer the above question: yes, alternative chains have delivered on their promises.

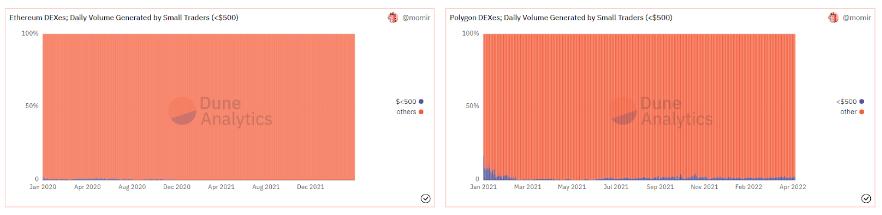

However, what is the true contribution of these small-scale traders? As shown in the chart below, the marginal value of these users is very low. Even on Polygon DEXes, these users contribute only about 1% of the trading volume daily, while on Ethereum, they account for at most 0.1% of the trading volume.

Source: IOSG Ventures, Dune Analytics

(https://dune.xyz/momir/DEX-Users)

One whale is worth ten thousand turtles: the 90-4 rule

On Ethereum, whales (addresses generating over $100,000 in trading volume daily) account for less than 4% of traders (about 3,000 addresses daily), yet they contribute nearly 90% of the total trading volume on Ethereum DEXes.

Similarly, whales account for about 1% of Polygon users, yet these accounts still generate most of the trading volume on Polygon DEXes, historically accounting for 74% of total trading volume.

Source: IOSG Ventures, Dune Analytics

(https://dune.xyz/momir/DEX-Users)

Despite some months where Polygon DEXs recorded more traders, the combined trading volume of Ethereum DEXs is still several times that of Polygon. The primary reason for Ethereum's dominance is not having the most users but being the preferred chain for large capital.

The conclusion is that the large capital represented by liquidity providers and traders still shows a strong preference for Ethereum, and although alternative solutions manage to offer upcoming scalability, changing public perceptions of security will be a long-term process.

Source: IOSG Ventures

Source: https://vitalik.ca/general/2021/04/07/sharding.html

Endgame

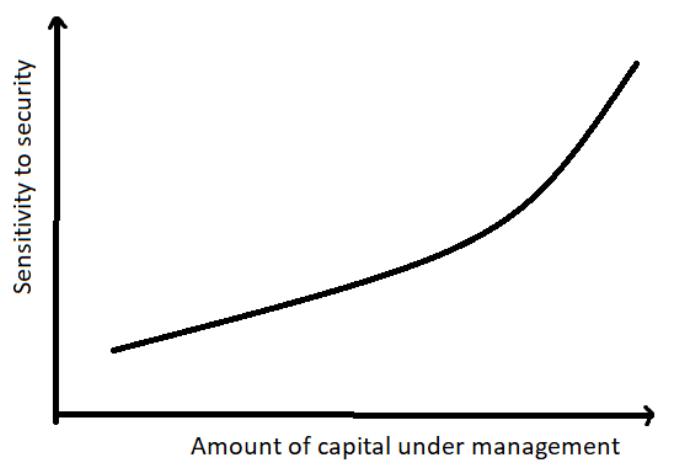

For financial applications and high-value transactions, security is paramount.

While some competing chains manage to create narratives of "cold-starting their DeFi ecosystems by finding niches in the blockchain trilemma," Ethereum remains focused on decentralization and security. Critics often have valid reasons to attack Ethereum's inflexibility, pointing out that with its current scale, Ethereum will not be able to serve as a global settlement layer.

This issue has led to a plethora of innovations, from sharded blockchains like Near and Zilliqa to application-specific chains like Polkadot and Cosmos, to single-chain highly scalable solutions like Solana and EOS.

However, despite each of these solutions bringing certain improvements in scalability, it is impossible to claim that any one chain is a viable solution for global/mass adoption. The following issues remain.

1) Economic sustainability - The vast difference between inflationary rewards and transaction fees raises doubts about the ability to maintain low fees in the long term.

2) Scaling - Supporting high throughput on a single chain inevitably increases the demands on node operators, which naturally excludes many who can keep up with hardware requirements, ultimately leaving only a small trusted subset.

The security provided by people for whales vs. the security provided by whales for people.

In 2022, ironically, highly decentralized blockchains like Ethereum are excluding ordinary users from participation due to their prices, while more centralized chains like BSC, Solana, or Polygon are open to the masses.

3) Composability friction - Related to specific application chains and sharding mechanisms, meaning there is a certain degree of friction between different shards/chains.

The Magic of ZK Technology

Traditionally, blockchains achieve zero trust by increasing redundancy and having a large number of computers perform the same computation. The more computers executing the computation, the more decentralized the network becomes; however, this places a burden on the network's scalability.

What if computations could be executed by just one computer while still maintaining the security assumptions of the most decentralized and robust blockchain?

"Any sufficiently advanced technology is indistinguishable from magic."

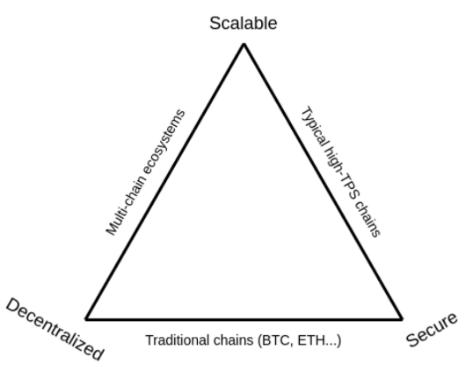

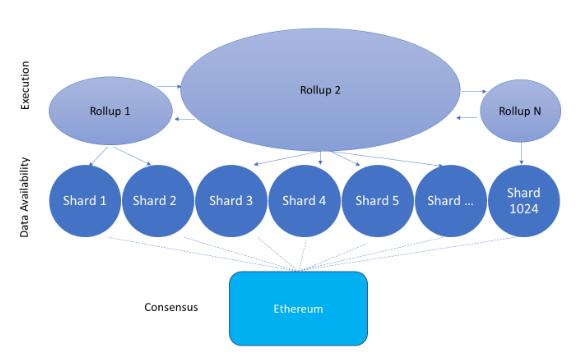

The theory of modular blockchains centered around Rollups is realizing the above goal. The impossible triangle of blockchains has become an outdated issue, as future applications will be able to fully leverage all three aspects: scalability, decentralization, and security.

Moreover, the theory of modular blockchains may represent the largest paradigm shift in the industry, capable of driving the mass adoption of blockchain technology without sacrificing its fundamental principles, the only viable solution.

Rollups can achieve scalability without worrying about economic sustainability, outward scalability, and composability friction.

That is to say, Rollups are only responsible for execution; they do not have to worry about consensus, decentralization, and security. Additionally, a Rollup can theoretically scale to millions of TPS without compromising composability, as it can scale across multiple shards.

Source: IOSG Ventures

Catalysts for DeFi Adoption on Rollup Solutions

If a new global financial system serving billions of people is to be fully built on blockchain, then Rollups seem to be the only reasonable choice that can support low-cost instant transactions without sacrificing security and decentralization assumptions.

However, realizing this vision will take at least 10 years. In the meantime, Rollups must compete for existing crypto audiences and applications. Additionally, some authors predict that the adoption of Rollups will face challenges in the short term, particularly due to sidechains offering extremely low fees, which help them attract low-income users who may be indifferent to decentralization and security issues.

However, for widespread adoption of a specific Rollup solution, fees may not be the key factor; the Rollup with the lowest fees may not dominate market share. From the perspective of Layer 2 network projects, network effects should take precedence over low fees.

Achieving network effects has several prerequisites:

- The long-term vision should align with Ethereum

- It should be easy for developers to deploy Ethereum mainnet code

- Proven technology will make large capital providers indifferent to participating in the mainnet or Rollup

- Token incentives can attract whale users who do not care about reduced gas fees

The Fat Application Theory

Regarding Rollups, the short to medium-term outlook is somewhat vague and uncertain, while the long-term outlook is clearer.

Single-chain networks have the following options:

- Adjust their roadmaps to incorporate modular and Rollup-centric approaches: while some blockchains, like Near Protocol, can serve well as data availability layers, others focused on execution can unleash tremendous potential by becoming Rollups themselves,

- Rely on meme theory to leverage stored value,

- Or risk being eliminated.

In some creative scenarios, we can even imagine centralized exchanges like FTX becoming decentralized, computing ZK proofs, and publishing them to data availability layers. The beauty of this technology is that it completely opens up the design space, no longer constrained by specific smart contract languages.

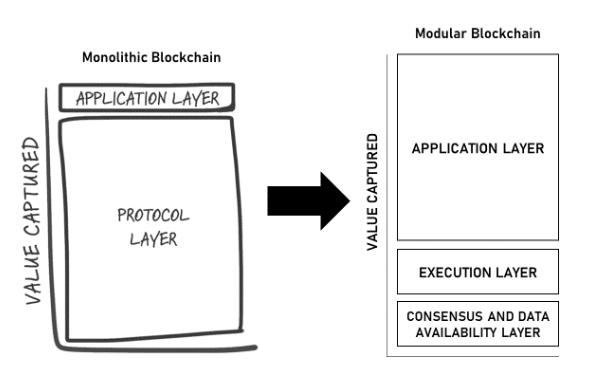

In the era of monolithic chains, when the market capitalization of a layer network often far exceeds the total market capitalization of the applications built on it, the fat protocol theory becomes even more effective.

Source: coingecko.com

Such situations arise not merely due to speculation but are fundamentally tied to monolithic blockchains. That is to say, if we price a layer network similarly to how we evaluate equity, the market capitalization should essentially equal the present value of expected future cash flows.

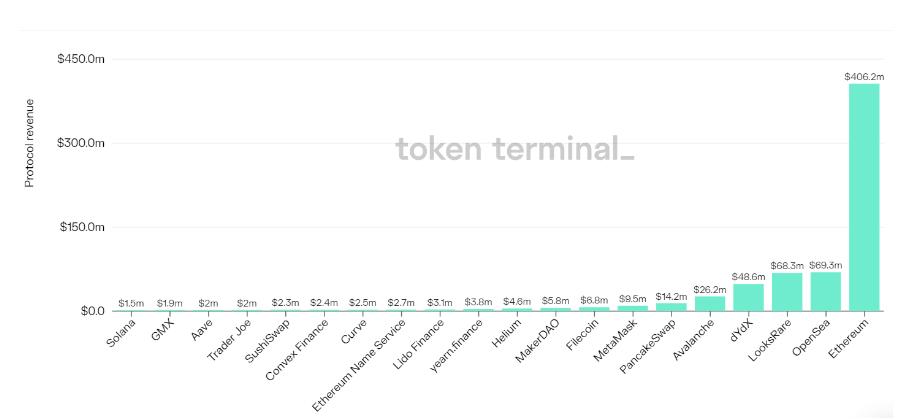

In simple terms, suppose there is a $5,000 transaction on Sushiswap. Sushiswap will charge a $15 transaction fee, of which only $2.5 is protocol revenue, while the rest is income for liquidity providers. Depending on network congestion, such a transaction could generate over $100 in fees for miners, which is nearly 50 times the protocol revenue.

In this case, the protocol is almost impossible to capture more cash flow than Ethereum miners (although theoretically, this could happen if the average transaction size is very large).

Source: https://tokenterminal.com/terminal/metrics/protocol_revenue

However, modular blockchains break this relationship:

- Due to advanced technology, we believe that ecosystems built on rollups, validium, etc., will become larger, and due to the economies of scale associated with ZK rollups, projects in prosperous ecosystems will pay very little to the security layer.

- By paying fixed fees to the base layer, the aggregate value of applications could be several times greater than the value of the base layer.

Finally, if we assert that blockchains will host companies worth trillions of dollars globally, we have reason to believe that the market capitalization of the base layer will ultimately not exceed the total value of the applications/companies built on top of it.

Source: IOSG Ventures; Illustration inspired by the original Fat Protocols thesis

Risk warning

Risk warning Risk warning

Risk warning