2022 Q2 Cryptocurrency Market Investment and Financing Report: GameFi Becomes the Investment Keyword

Affected by the secondary market, the financing activity in May and June sharply decreased.

Affected by the secondary market, the financing activity in May and June sharply decreased.Author: Shiwen, Odaily Planet Daily

Editor: Hao Fangzhou

The cryptocurrency market experienced significant volatility in the second quarter.

On a macro level, the Federal Reserve has confirmed an interest rate hike of 75 basis points to 1.75%, marking the largest single increase in nearly thirty years since 1994. Against the backdrop of rising interest rates, investor trading sentiment has been dampened, and they are likely to sell off risk assets before an economic slowdown, leading to bearish sentiment in the crypto market.

From the perspective of the crypto market itself, the collapse of Luna in May and the de-pegging of UST not only led the narrative of algorithmic stablecoins into a dead end but also triggered a series of chain reactions. With a significant drop in coin prices, a large amount of institutional collateral faced liquidation, the lending market shrank sharply, and institutions like Three Arrows, Celsius, Jump, Hashed, and Delphi suffered heavy losses, while some CeFi platforms also faced redemption pressure from users.

Numerically, the total DeFi TVL plummeted from over $240 billion to the current $72 billion, a loss of 70%. The NFT market also performed poorly, with its market cap dropping from $35 billion at the beginning of the year to $22.3 billion, a decrease of 36%. In the GameFi sector, the once P2E chain game king Axie Infinity saw its game token AXS drop by 92% from its peak.

It can be said that the second quarter of 2022 was chaotic for the crypto market.

However, despite the secondary market hitting new lows, investment trends and themes in the primary market are forming, with established institutions and new investors quickly entering the field to seek the best investment opportunities across various verticals. The primary market often anticipates hot areas ahead of the secondary market, indicating a "time lag" in the investment direction of the secondary market. Therefore, grasping the investment and financing situation in the primary market is equivalent to laying out a strategy for future investments in the secondary market.

Looking back at the Q2 primary market investment and financing activities, we can find:

- The number of financing events in Q2 was 511, with 28 transactions exceeding $100 million;

- Crypto financial service providers are closely linked with the traditional financial industry and continue to innovate in areas such as custody, settlement, and payment, thus attracting more capital attention;

- In terms of the number and amount of financing, GameFi is the preferred theme for major investment institutions;

- A total of 11 institutions participated in more than 10 investments in Q2;

- Animoca Brands participated in 41 investments, making it the institution with the most investment projects;

- Traditional institutions and enterprises are more inclined to invest in Web3, focusing on trading payments, the metaverse, and DAOs.

Note: Based on the business type, service targets, business models, and other dimensions of each project, all disclosed financing in Q2 (the actual close time is often earlier than the announcement) is categorized into five major tracks: infrastructure, applications, technology service providers, financial service providers, and other service providers. Each track is further divided into different sub-sectors, including GameFi, DeFi, NFT, payments, wallets, DAOs, Layer 1, cross-chain, and others.

The number of financing events in Q2 was 511, with a disclosed total amount of $12.713 billion

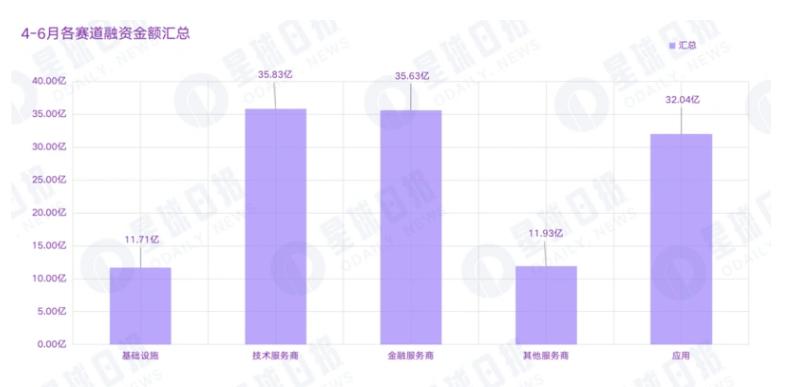

According to incomplete statistics from Odaily Planet Daily, from April to June 2022, there were a total of 511 investment and financing events in the global crypto market (excluding fund-raising and mergers and acquisitions), with a disclosed total amount of $12.71 billion, concentrated in the infrastructure, technology service providers, financial service providers, applications, and other service provider tracks, with the technology service provider track receiving the most financing, totaling $3.583 billion.

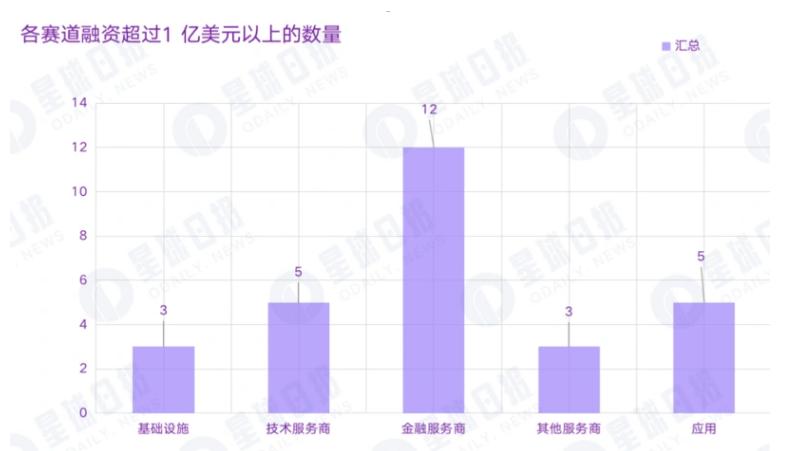

Among all financing events, the number of transactions exceeding $100 million reached 28. This includes 3 in the infrastructure track, 5 in the technology service provider track, 12 in the financial service provider track, 3 in the other service provider track, and 5 in the application track.

According to the blockchain report released by CB Insights for Q1 2022, the financing scale of the blockchain industry reached $9.2 billion in the first quarter, with a total of 461 blockchain investment and financing transactions, including 28 transactions exceeding $100 million.

In contrast, the investment activity in the Q2 primary market showed a certain increase. The financial service track is closely linked with the traditional financial industry and can continue to innovate in areas such as custody, settlement, and payment, providing support for the growth of the financial industry, thus attracting more attention.

Affected by the secondary market, financing activity sharply decreased in May and June

In May and June, the crypto market was significantly impacted by the collapse of Luna and news of various institutions being insolvent, leading to a prolonged low market sentiment and severe losses of funds in the market. This is reflected in the investment and financing data, showing a rapid decline in both the number and amount of financing in Q2, with low financing activity. In April, there were a total of 184 financing events, with a financing amount of approximately $7.05 billion; in May, there were 165 financing events, with a financing amount of approximately $3.54 billion; and in June, there were 162 financing events, with a financing amount of approximately $2.12 billion.

GameFi and NFT are more favored by capital

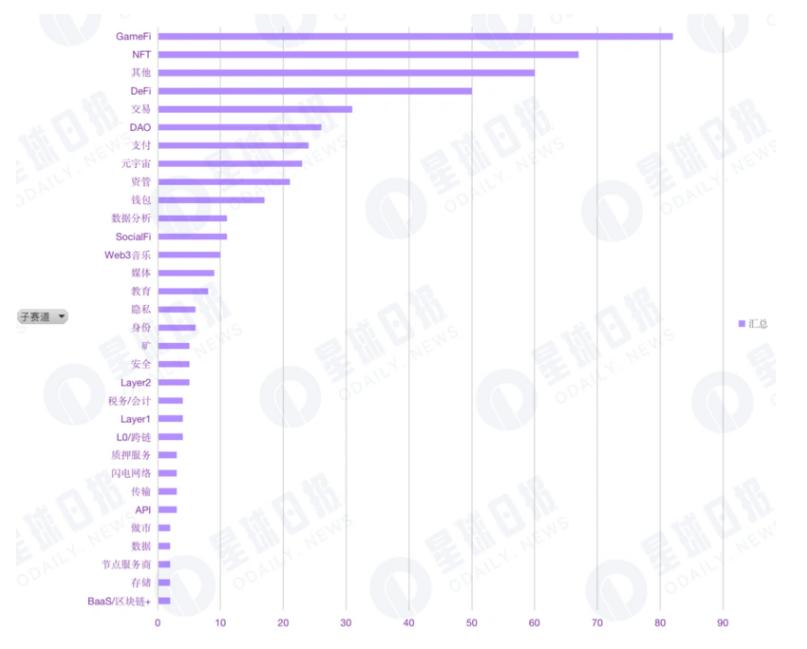

From the distribution of financing numbers in sub-tracks, GameFi-related application scenarios, infrastructure, and technical solutions have gained significant attention and layout from many large institutions, making it the most favored track by capital, with a total of 82 financing events, accounting for 16% of the total financing. Among these, there were 9 investments in GameFi technology services.

Although GameFi has seen a surge of funding projects after a brief boom, giving the impression of being "short-lived," the focus on investment in GameFi applications and infrastructure indicates that capital still holds high expectations for GameFi.

Similarly, the NFT track has also attracted capital attention, with a total of 67 financing events, ranking second. As the NFT market continues to expand, its ecosystem is also continuously improving. Especially when NFTs are combined with IP incubation and copyright commercialization, NFTs have become an important means for institutional brand marketing and external promotion. Moreover, since the explosion of digital collectibles, consumer acceptance of this new form of collection has been increasing, and NFTs are entering a period of accelerated development.

In addition, financing news from other sub-tracks has also been active, with a total of 60 events, ranking third. This large category includes areas such as incubation, consulting, marketing, technology development platforms, on-chain monitoring, carbon credits, and reward points. This also reveals a positive and clear characteristic: investment institutions are actively exploring new directions and continuously expanding the use cases of Web3 and opportunities for dialogue with end users.

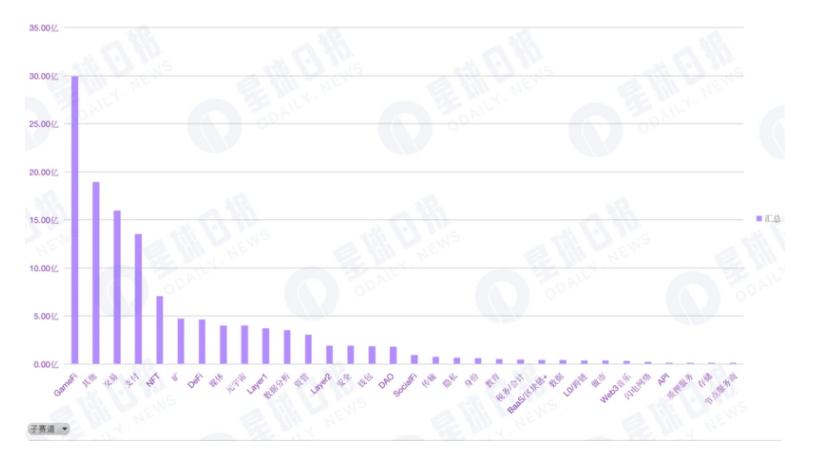

In terms of financing amounts in sub-tracks, GameFi leads significantly with a financing amount of $2.996 billion, accounting for 23.5% of the total industry financing. The trading and payment sectors also performed well, ranking third and fourth with $1.6 billion and $1.353 billion, respectively, while attention to technical services such as on-chain storage, data, and chain reform was relatively low.

Additionally, before the Ethereum upgrade, Layer 2 was considered the main way to achieve faster transaction speeds and greater transaction throughput without sacrificing decentralization and security. Therefore, the Layer 2 sector has always been highly anticipated. However, data shows that Layer 2's financing performance this quarter was not ideal, with only 5 projects receiving investment, totaling $190 million.

Compared to last year when various institutions launched special funds to invest in and incubate DeFi projects, investment institutions are now more cautious and rational in their investments in DeFi, having experienced issues such as security vulnerabilities, token supply mechanisms, and liquidations in a declining market.

The largest single investment amount was $2 billion (Epic Games)

As a large amount of capital flowed into the market, the valuations of leading projects were continuously driven up, and the industry record for the largest single financing was broken multiple times. According to specific track classifications, the largest single investment amounts in various vertical fields are as follows:

- In the infrastructure track, in the mining sector, the startup Crusoe Energy, focused on Bitcoin mining, completed a $350 million financing led by G2 Venture Partners.

- In the technology service provider track, in the GameFi sector, game developer Epic Games completed a $2 billion financing at a valuation of $31.5 billion to build the metaverse, which is currently the largest single financing in the crypto market. (Note from Odaily Planet Daily: Strictly speaking, Epic Games still belongs to the traditional game technology service track, and it is unclear whether blockchain and cryptocurrency (including NFTs) will play a role in its plans.)

- In the financial service provider track, USDC issuer Circle completed a $400 million financing, continuing its efforts to promote global economic transformation.

- In the other service provider track, football media startup OneFootball completed a $300 million Series D financing and established a new joint venture, OneFootball Labs, with Animoca Brands and Liberty City Ventures to explore the development of sports + NFTs.

- In the application track, three projects simultaneously received the largest financing amounts in this track, namely the NFT project Genies, the metaverse project Improbable, and the on-chain job-seeking project Naetion, each receiving $150 million.

11 institutions made more than 10 investments

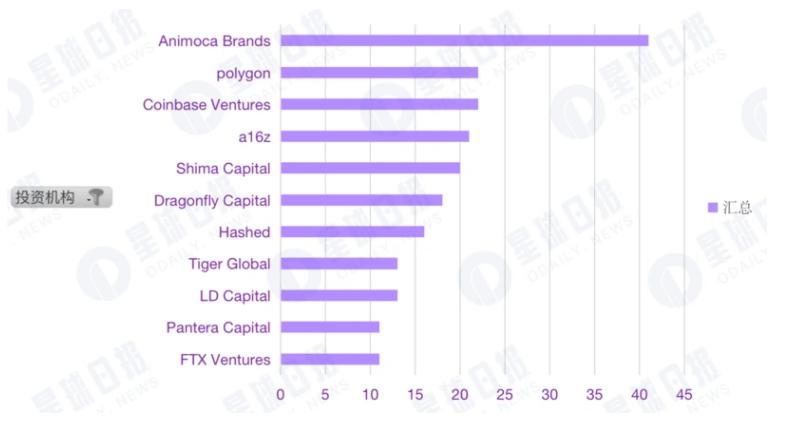

With the increase in the number of financing events, the landscape of investment institutions is also changing. In Q2, a total of 11 institutions made more than 10 investments, with Animoca Brands participating in 41 investments, ranking first, followed by other investment institutions including Polygon with 22, Coinbase Ventures with 22, a16z with 21, Shima Capital with 20, Dragonfly Capital with 18, Hashed with 16, Tiger Global with 13, LD Capital with 13, FTX Ventures with 11, and Pantera Capital with 11.

It is worth noting that Polygon, as a newly competitive ecosystem, has accelerated its investment layout in primary projects and is relatively optimistic about the payment, GameFi, and DAO tracks.

In addition, in Q2, many traditional institutions and enterprises participated in crypto market financing, including Tencent, SoftBank, Fidelity International, BlackRock, Goldman Sachs, and Sequoia Capital, with their investments mainly concentrated in trading payments, the metaverse, and DAOs, leaning towards areas with strong compliance.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles