Arthur Hayes Blog Post: My Highest Bid for Ethereum

Since the darkness of Three Arrows began, many outstanding crypto lending institutions and hedge funds have been forced to liquidate.

Since the darkness of Three Arrows began, many outstanding crypto lending institutions and hedge funds have been forced to liquidate.Author: Arthur Hayes

Compiled by: Wu Zhuocheng, Wu Says Blockchain

Since the end of last year, the market has been waiting for the Federal Reserve to shift its policy focus from curbing inflation to supporting economic growth. On July 27, the Federal Reserve stated that if economic growth falls short of expectations, they will shift their policy focus to support economic growth. This article argues for the necessity of restoring monetary expansion by showcasing the rapidly deteriorating U.S. economy.

If you believe my argument is correct, the next step is to consider which assets might perform best when the money supply expands again. The transition from monetary tightening to monetary easing is an excellent opportunity to significantly increase financial assets, and wasting such an opportunity is irresponsible, so we must carefully choose the right assets.

Should I invest in stocks, bonds, real estate, commodities, gold, or crypto assets? Obviously, you all know I advocate for crypto assets to take center stage in this scenario, so considering liquidity, which Token should we lean towards? Here is a premise: during the transition period of monetary policy, we should prefer concentration over diversification. As a concentrated bet, ETH will provide the best returns in the second half of this year.

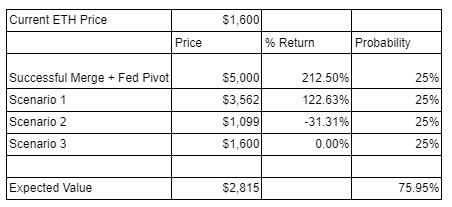

Expected Value

In the next 8 months or so, there are two potential events that could occur, and whether they unfold smoothly is crucial to my conclusion.

Will the Federal Reserve change its policy focus to restart the printing press for the economy?

Will the ETH merge be successful?

Investing is a time-sensitive endeavor, so I must set a time limit for the completion (or non-completion) of these events. This time limit is March 31, 2023.

Each event has two possible outcomes, resulting in a total of four scenarios.

Scenario 1: Federal Reserve shifts focus + ETH merge successful (this is the scenario I am most optimistic about).

Scenario 2: Federal Reserve does not shift focus + ETH merge successful

Scenario 3: Federal Reserve does not shift focus + ETH merge unsuccessful

Scenario 4: Federal Reserve shifts focus + ETH merge unsuccessful

For each scenario, I will provide a price target and assign a 25% probability. I will then calculate the average of all outcomes to derive the expected value of the ETH/USD price on March 31, 2023. If this expected return is positive, I will confidently increase my ETH long position. If it is negative, I will temporarily refrain from adding to my ETH position.

The following elaborates on this analytical structure.

Will the Federal Reserve's Policy Shift?

Over the past few decades, as financial services have matured, banks have begun to finance more residential real estate. Banks want to lend the excess reserves provided by the Federal Reserve to low-risk asset classes. The safest loans banks can offer are secured by hard assets, with houses being the most significant on that list. If you default on your mortgage, the bank can repossess your house and (hopefully) sell it for more than the remaining loan value. Over time, banks have started pouring more and more free capital into housing loans.

The widespread availability of housing financing and banks' willingness to accept additional risks have allowed more people to purchase homes through mortgages. At some point, the price of housing became less important. The only thing that mattered was whether borrowers could afford to pay their monthly mortgage with their disposable income. The result is that the housing market has become entirely dependent on financing costs, which are primarily determined by the central bank through the setting of short-term risk-free interest rates (more on how this works later).

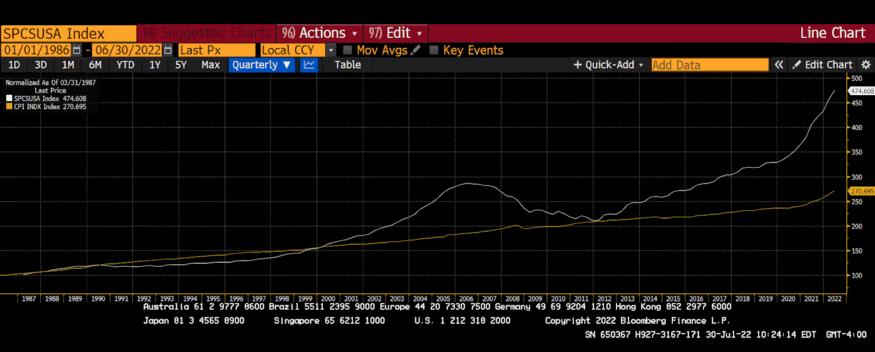

U.S. National Home Price Index (white) vs. U.S. CPI Index (yellow)

The chart above starts from 1985, with each data series indexed to 100. As you can see, over the past forty years, housing prices have risen 75% faster than the inflation measured by the government. If everyone were just buying homes with cash, prices would be much lower. But if you can afford your monthly mortgage, you have the ability to buy more expensive homes, and banks are willing to extend credit to homebuyers, which drives prices up.

70% of U.S. GDP is consumption. Since the 1970s, the U.S. has transitioned from a manufacturing powerhouse to a financialized service economy. Essentially, anything that can be used as collateral for a loan qualifies for financing. Most Americans live paycheck to paycheck, meaning their entire lifestyle relies on monthly loans.

"Research from PYMNTS found that in April 2022, 61% of American consumers lived paycheck to paycheck, up 9 percentage points from 52% in April 2021."

The return banks earn when they extend credit is known as the interest on excess reserves (IOER), which is set between the upper and lower bounds of the Federal Funds Rate (set by the Fed at its meetings). This is one of the tools the Fed uses to translate its policy rate into the actual rates observed in the market.

If a bank accepts your deposit and pays you 0%, it can turn around and immediately earn a risk-free return of 2.40% by borrowing from the Federal Reserve. Given that the market is competitive, if Bank A offers consumers a 0% deposit rate to earn a 2.40% spread, Bank B can offer a 1% deposit rate to steal business from Bank A and still earn a 1.40% spread. Therefore, banks will compete by offering increasingly higher deposit rates until they closely match the IOER provided by the Federal Reserve.

If banks must pay deposit rates close to the IOER, then when extending loans, they must charge rates above the IOER. The higher the Fed's risk-free rate, the higher your mortgage rate will be.

U.S. 30-Year Fixed Mortgage Rate (white) vs. Federal Funds Upper Limit (yellow)

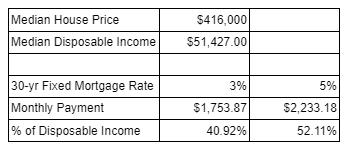

The above chart clearly shows that the higher the rate set by the Federal Reserve, the more Americans pay to finance their homes. This is extremely important for the health of American consumers, as monthly mortgage payments constitute a significant portion of median household disposable income.

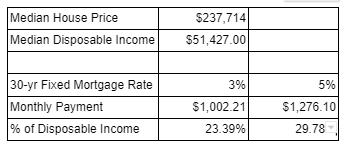

Mortgage rates were around 3% at the beginning of this year and are now slightly above 5%. Due to this change, the median household balance sheet has deteriorated by over 10%. The bigger issue is that the growth rate of loan amounts continues to outpace inflation. Looking back at the relationship between home prices and inflation in the chart above, imagine what would happen if the median home price were to drop to match the 75% inflation rate since 1985? Household balance sheets would look like this.

In this scenario, households would retain a larger proportion of their income for other necessities. The financial situation of the median household becomes increasingly strained due to the financing costs of mortgages, making them more likely to resort to other consumer finance tools to pay for other essentials, such as credit cards.

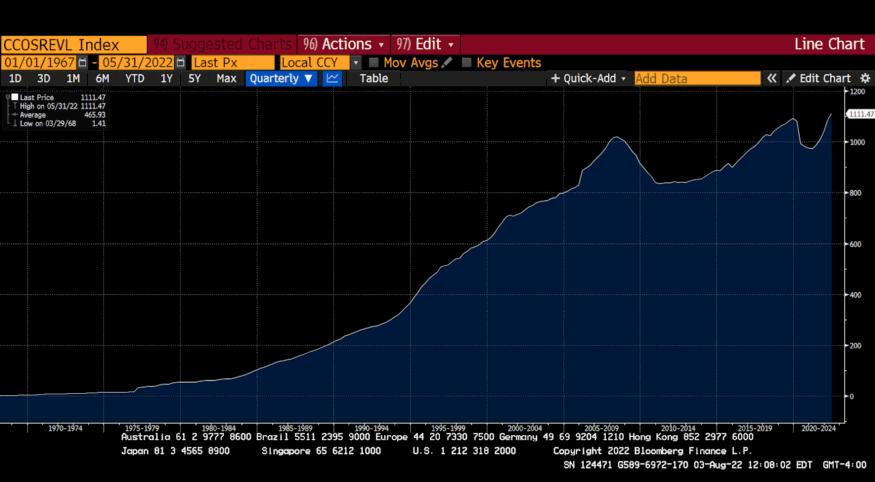

U.S. Household Debt as a Percentage of GDP

U.S. Outstanding Consumer Credit

The charts above clearly show that households are increasingly resorting to credit to fund their survival.

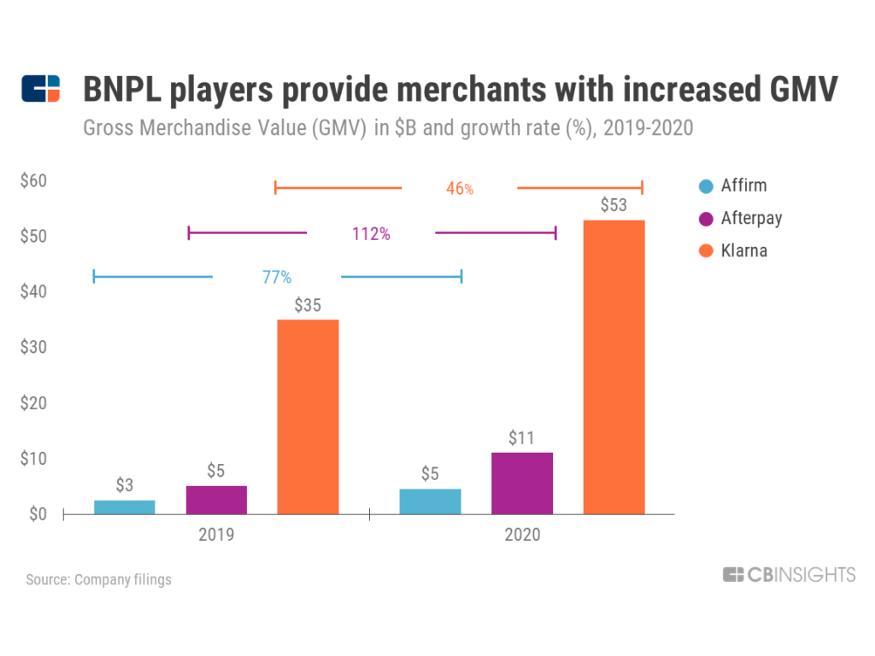

The total value of goods (GMV) in the chart above essentially represents the loan balances of top BNPL (Buy Now, Pay Later) fintech company clients. As you can see, nearly $70 billion in GMV was financed in this way in 2020. Older generations use credit cards, while younger generations use BNPL; different forms, same essence.

America is a car country, and for the average American earning a wage, owning a car is a necessity for commuting from home to work. Family vehicles are another asset that must be financed due to their high cost. According to Kelley Blue Book, the current average car price is $48,043, a record high. If you earn $50,000 a year and the average car price is $48,000, you need to finance that car!

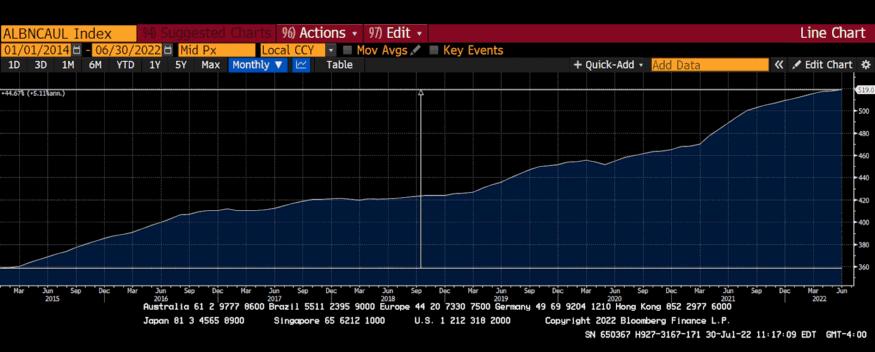

U.S. Commercial Bank Auto Loans

The data set from the Federal Reserve above dates back to 2015. Over the past seven years, outstanding auto loans have surged by 44%.

Housing and cars are two examples of key life assets that American households must finance. The interest rates that determine how much Americans must pay monthly for these necessities are directly influenced by the federal funds rate. Therefore, when the Federal Reserve makes money more expensive by raising rates, it directly makes the vast majority of American households poorer.

The Federal Reserve's impact on household balance sheets is directly related to the scale of loans these households hold. If the price of an average house or car suddenly drops by 50%, then a few percentage points increase in the Fed's rate won't have much impact on households because, while they may pay higher rates for their homes or cars, their monthly net payments may decrease. However, we are at the tail end of over 50 years of intense financialization in the U.S. economy, which has driven exponential increases in the prices of any assets that can be financed through loans.

If you can't afford the monthly payments, you can't buy a house, a car, or other durable goods. If buyers can only pay less, then sellers must sell at lower prices. Then, marginally, the entire stock of homes, cars, and other financed assets becomes less valuable. Given that these assets are financed by debt, this becomes a problem for banks that lend against this type of collateral because when their borrowers can't pay their loans, they will repossess assets that are worth less.

As asset prices decline, banks become more conservative about who and what they lend money to. At this point, asset prices must fall to a level that buyers can afford to make monthly payments at higher financing costs. While this is cautious, it effectively reduces the entire loan stock available to American households. This is a cyclical, reflexive process that leads to terrible debt-supported asset deflation.

As I have said many times, the central bank's goal is to ensure that assets do not experience deflation, as the commercial banking system cannot survive in an environment of asset deflation. Therefore, if the Federal Reserve or any other central bank believes deflation is imminent, it must act immediately, a lesson taught to anyone and everyone in economics courses. Most academic personnel at the Federal Reserve (or any other central bank) have written papers on and studied the Great Depression, believing that the Fed's mistake was not printing money, not supporting asset prices, and not resisting the deflation that plagued various developed economies in the 1930s.

The takeaway from this entire section is that the health of American consumers is directly related to the federal funds rate. If rates continue to rise, the economy will be affected. If rates fall, the economy will thrive.

Either/Or

This phrase is quite famous in China, where e-commerce giant Alibaba was accused of forcing merchants to choose between selling their goods on Alibaba or its competitors, not allowing coexistence with other platforms.

The Federal Reserve is facing a similar "either/or" dilemma. They can choose to combat inflation or support the financialized economy of the United States, but they cannot do both simultaneously. Fighting inflation requires raising the price of money and reducing its quantity, while the prescription for a "healthy" U.S. economy is entirely the opposite.

In March 2022, as inflation began to surge, the Federal Reserve decided to endure higher rates, raising the federal funds rate for the first time since 2018 by a quarter point. However, the chart below shows that the U.S. economy is in recession.

U.S. Real GDP Growth Percentage

Remember, the Fed's first rate hike occurred in March of this year, and the first negative GDP growth also occurred in the first quarter of this year—what a coincidence.

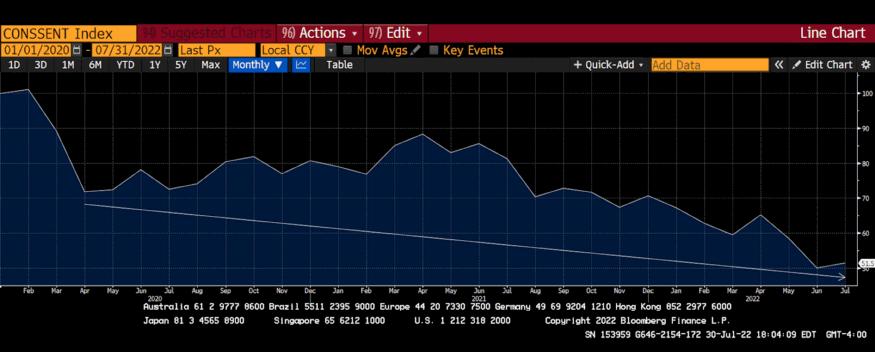

Americans today are more pessimistic about the economy than during the peak of COVID, when millions died from the virus, yet people are more desperate today.

University of Michigan Consumer Sentiment

However, even so, there are no signs that inflation is easing. By this standard, the Federal Reserve is failing.

Domestically, the Federal Reserve is causing the economy to collapse (it is in recession), but inflation continues to extract more and more purchasing power from the common people, who will head to the polls in a few months. What should be done? What variables should the Federal Reserve optimize?

If the Federal Reserve wants to continue reducing inflation, it must keep raising its policy rate. You could argue that the Fed needs to become more aggressive, as its policy rate ceiling of 2.5% is still 6.6% lower than the latest inflation reading of 9.1%.

If the Federal Reserve wants to grow the economy, it must buy bonds again, which will reduce the monthly payments for 90% of American households on housing, cars, and other durable goods.

Market Expectations for Policy

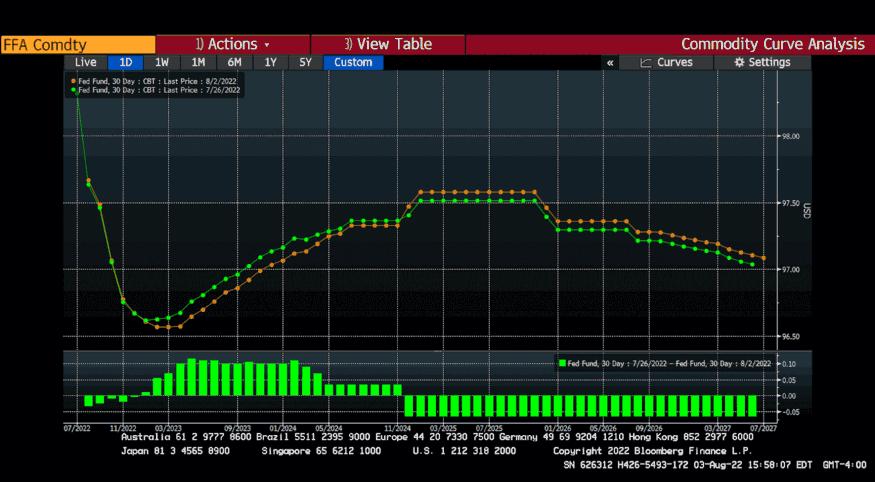

A significant rate hike is certainly expected at the September meeting. The market is currently pricing in a 50 basis point hike in September. What is currently at play is the subsequent pause for the November meeting. That is what the market cares about. By the end of September, short-term rates will be at 3%, which will be very difficult for the American public to bear.

In the June and July meetings, the Federal Reserve raised rates by 0.75%, while expectations for a rate hike at the September meeting have changed little. The federal funds futures contracts for September 30, 2022, were 97.53 on June 17 and 97.495 on July 27.

The expected rate is 100 minus the futures price; if the curve moves upward, it means the market expects rates to decrease, and vice versa. The market clearly still expects the Federal Reserve to raise rates over the next six months.

However, after the Fed meeting, all my macro risk asset indicators rebounded and maintained their upward momentum by Friday's close. Risk markets continue to hold gains after the Fed meeting, but forward-looking money market derivatives indicate no change. Who is right? I believe that as economic data continues to deteriorate and rising credit prices further restrict financial activity, the narrative of negative growth will outweigh the persistent high inflation. Powell stated that the Federal Reserve has reached neutrality, and now they need to observe the impact on the broader economy.

Market expectations for changes in policy rates at the September meeting have become deeply ingrained. However, from now until then, the Federal Reserve will have two additional CPI data points (July CPI, released August 10, and August CPI, released September 13). I am not a data detective, but the pace of price increases is likely to slow, which will provide Powell with the justification he needs to pivot back to easing monetary conditions.

Given the data, we can almost be certain that the Federal Reserve will raise rates by 0.5% to 0.75% at the September meeting. This makes the December meeting the decisive meeting for the remainder of 2022. I expect that the steadily rising federal funds rate will cause absolute harm to the average American.

Once the elections are over, the Federal Reserve will resume business—reducing the monthly payments for Americans through easing monetary policy. While the top 10% benefit disproportionately from rising financial asset prices, given that every aspect of American life is financed, the common people also need low rates to afford their lifestyles, and everyone is enamored with the cheap funds provided by the Federal Reserve.

We should now be prepared for the forward-looking expectations of Federal Reserve policy to point towards easing. Therefore, the risk asset market has likely bottomed out and will now trade.

Will the ETH Merge Be Successful?

Will the ETH network update to proof of stake (PoS) as planned? This is a question you must ask yourself. Before I provide a reason for my extremely optimistic view on the price of ETH post-merge, let me explain why I am more confident than ever that the merge will actually happen.

In 2018, I wrote an article titled "ETH, a Two-Digit Shitcoin," predicting that ETH's price would fall below $100. I was wrong!

I began to believe in 2020 when I saw a chart depicting how ETH's market cap was lower than the total market cap of all the dApps it supports. I firmly believe that DeFi provides a reliable alternative to the current financial system—and now, ETH is ready to power the world's financial computer.

Since 2015, Vitalik has been discussing the necessity of eventually transitioning to a PoS consensus mechanism. I do not possess the technical skills to assess whether ETH core developers can succeed, but there is a group of stakeholders in the ETH network that will absolutely hinder the chances of success. That is the current ETH miners.

Miners who have spent billions on GPU graphics cards and related capital expenditures can only earn income under a proof of work (PoW) system. Kraken wrote a great blog post explaining the differences between PoW and PoS systems. When the merge occurs and ETH transitions from PoW to PoS, miners' income will drop to zero, and their equipment and facilities will become nearly worthless unless they can find another valuable chain to provide the same marginal income as mining. I seriously doubt this possibility, as ETH is the second-largest cryptocurrency by market cap, and there is no other PoW blockchain with a market cap in the hundreds of billions that can be mined using GPUs. Therefore, when miners begin to voice their negative opinions about the merge, it can be fairly speculated that the merge is a real possibility.

Baoyi Ye is aligned with the Chinese ETH mining community. I have known him for many years, and I have no doubt about his determination to do so.

After reading this tweet, I reached out to some other contacts in the Chinese mining community. I asked them if there was real motivation behind a potential airdrop or hard fork to form a PoW-based ETH chain. One person said "absolutely" and added me to a WeChat group where serious people were discussing the best way to make this a reality. Another friend said it was absolutely a failure, and Baoyi Ye had reached out to him for help.

Similarly, after the merge, ETH miners' machines will become worthless overnight unless they can mine on another valuable chain. I seriously doubt the long-term viability of an ETH PoW chain, but for now, let's assume it will exist with a significantly non-zero market cap for a few months. More importantly, if miners do not believe the merge will occur as planned, they will not embark on this journey and spend valuable political capital within the community.

Therefore, if the merge is likely to happen sometime in the third quarter of this year, or at the latest in the fourth quarter, the question is—has the market already priced in the post-merge price?

Amber Group published a great article discussing everything about the merge. Here are the key points:

The market expects the merge to occur around September 19, 2022.

The issuance of ETH per block will decrease by 90% post-merge, making ETH a deflationary currency.

ETH staked on the beacon chain will be locked for an additional 6 to 12 months.

Amber believes the merge will be akin to a "triple halving":

In terms of supply, ETH is currently incentivizing miners (under PoW) and validators (under PoS). The minting tax pays miners 2 ETH per block to generate new blocks, and rewards are also distributed to validators on the beacon chain. After the merge, rewards for miners will stop, reducing ETH's issuance rate by about 90%. This is why the merge is colloquially referred to as a "triple halving"—a nod to Bitcoin's halving cycles.

Due to various factors, demand for ETH post-merge is also expected to increase. First, staking rewards for validators will immediately increase. Validators will receive transaction tips currently earned by PoW miners, potentially raising the APR by about 2-4%. Additionally, as they will be able to reorder transactions, they will also begin to earn MEV (maximum extractable value). Flashbots is a research organization studying MEV, and its researchers indicate that, assuming there are 8 million staked ETH, validators' yields could increase by an additional 60%. Therefore, if the merge were to happen today, validators are expected to earn about 8-12% APR due to all the aforementioned factors.

Most (if not all) of this information has not changed over many months; what has changed is the credit-driven cryptocurrency price crash. The market dislocation caused by Luna/TerraUSD and Three Arrows forced many to sell, impacting many hedge funds that had heavily entered DeFi.

Given all the forced selling that occurred during the market downturn and the poor financial condition of most crypto investors, the merge does not seem to have been reflected in the price—this gives us an excellent opportunity to increase our ETH positions at very attractive levels.

So, now that the dust has settled, the loyalists among us—whether holding ETH or fiat—must determine how significant we believe the merge's impact on price will be based on expected market conditions and/or other contributions.

Let me share a simple example to illustrate why I believe the merge will have an incredibly powerful impact on the price of ETH.

Many of you trade stocks and understand at a fundamental level that stocks are claims on a company's future profits. However, a company does not pay dividends in additional shares—it pays you in fiat currency. Moreover, to use a given company's services, you do not need to pay with the company's own stock but rather with fiat currency.

For ETH, the income earned by stakers is paid in ETH, and you must pay in ETH to use the service. Stakers must also stake their ETH to earn income, which requires them to lock up funds and effectively remove them from the market. The more ETH staked, the more income earned. Therefore, it is safe to assume that most stakers will take their earned ETH and lock it away. Coupled with the fact that users need to pay ETH fees to use ETH (which has been removed from circulation), and the fact that the issuance of ETH under the new PoS model will decrease by about 90% annually, we will quickly see a reduction in the supply of ETH. The more the network is used, the more of its own currency must be used to utilize it—thus, as the network becomes more popular (assuming it provides useful services), the amount of ETH exiting circulation will only increase. Of course, it is important to note that under the new PoS model, the transaction fees paid by users are expected to decrease, but even so, when you consider all these factors together, they should still drive the price of ETH to increase exponentially.

A good usage metric is the total value locked (TVL) in DeFi applications (i.e., the amount of funds users have deposited or "staked" on DeFi platforms from which they earn returns). I believe DeFi will provide a reliable alternative system to the financial rents we currently pay in the trillions of dollars annually. As you can see, TVL skyrocketed after 2020, with applications using this locked collateral paying ETH fees to the network. The larger DeFi grows, the more deflationary ETH becomes. This becomes an extreme issue, but we are not close to that situation yet.

Before proceeding, let’s revisit my assumptions.

I believe the merge will occur by the end of this year due to the increased noise from ETH miners, who may lose a significant portion of their income in a PoS world.

The recent market crash has broken the spirits of the bulls that had been shining brightly on ETH and DeFi, turning them into indiscriminate sellers.

There will be no "buy the rumor, sell the news" phenomenon post-merge. Given the significant price drop over the past month, anyone who might sell has likely already sold.

The merge means ETH becomes a deflationary currency, and as DeFi becomes more popular, usage is expected to continue to grow—this will accelerate the deflation.

While there are other L1 smart contract network competitors, many of them already have some version of a PoS consensus algorithm. ETH is currently the only major cryptocurrency transitioning from PoW to PoS.

Expected Value Calculation

This is the most important part of this article because even if my arguments are reasonable and you believe them, there is still a significant chance I could be wrong. With that in mind, let’s quickly review the price predictions for all potential outcome combinations.

Unless otherwise noted, the prices I reference in this section are sourced from Bloomberg.

Scenario 1: Federal Reserve shifts focus + ETH merge successful (i.e., what I speculate will happen, and the best case for ETH)

In November 2021, the Federal Reserve began printing money, altcoins surged, and attention began to shift towards the bullish narrative surrounding the upcoming ETH merge in 2022. Therefore, I will use $5,000 as my price target in this scenario. I believe this is a conservative estimate, as structural changes in supply and demand dynamics are never fully priced in a priori—just as Bitcoin halvings continue to generate positive returns, even when we are very clear about when they will occur in advance.

Scenario 2: Federal Reserve does not shift focus + ETH merge successful

Since the dark days of Three Arrows, many prominent crypto lending institutions and hedge funds have been forced to liquidate, and ETH has rebounded from a low of around $1,081 to $1,380—returning nearly 30% in just a few weeks. From the July 27 Federal Reserve meeting to the close on Friday, July 29, ETH's absolute value increased by 25%, compared to Bitcoin's 9% rise.

If the Federal Reserve does not restart the printing press, the baseline scenario is a return to the levels the market was considering before the Fed's pivot. To be conservative, let’s assume ETH's price returns to the market low of June 17 ($1,081), but also retains any price movement from the low of June 17 to July 26 (the day before the Fed's pivot was proposed), which we can strictly attribute to expectations of a successful merge. To isolate the price movement of ETH driven solely by merge expectations during that timeframe, let’s assume any recent performance of ETH relative to BTC was entirely driven by expectations of the merge's impact. This will allow me to separate the speculative impact of the merge's timing and outcome from the influence of dollar liquidity on the broader market.

From June 17 to July 26, ETH's value relative to BTC increased by 25.46%—therefore, if the Fed's pivot is canceled, we can assume the price will drop to $1,081 (the low on June 17) * 1.2546, resulting in $1,356.

Now, we need to add the expected price impact of a successful merge. As I mentioned earlier, since the merge will have structural impacts on the ETH network, it is expected to drive a "triple halving" event. To predict how this might affect ETH's price, we can look at Bitcoin's performance between halving dates. The table below shows the price appreciation that occurred between each Bitcoin halving date.

Bitcoin is decentralized money. ETH is decentralized computing power. If Bitcoin has continued to rise after halving, it is reasonable to assume ETH will also rise. Therefore, if we apply the minimum price increase of 163% post-halving to $1,356, we arrive at an expected value of $3,562.

Note: A 163% price performance post-merge is very conservative, as Bitcoin's total supply continues to increase with each halving, while ETH's supply post-merge, given current usage trends, should decrease.

Scenario 3: Federal Reserve does not shift focus + ETH merge unsuccessful

Let’s return to the dark days, which would be the recent low of $1,081—this is my price prediction for this scenario.

Scenario 4: Federal Reserve shifts focus + ETH merge unsuccessful

If the merge fails or is delayed, the ETH network will still function as it does today. Many may feel very disappointed, but ETH's value will not drop to zero. Solana is the 9th largest altcoin—with a market cap of $13.5 billion—having experienced multiple hours of downtime over the past 12 months, yet its value remains far above zero. Even if the merge does not go as planned, ETH will still do well.

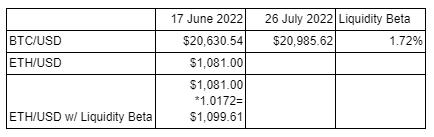

To calculate the impact of this scenario on ETH's price, let’s use the price performance of BTC/USD from June 17 to July 26 as liquidity Beta to determine what ETH's price would be before any potential positive price movements related to the merge occurred—while still including any price movements we believe are strictly driven by recent dollar liquidity conditions.

From June 17 to July 26, BTC/USD increased by 1.72%. Therefore, we can estimate that, without the excitement related to the merge, ETH's price would also increase by 1.72% during that timeframe—since we again assume the merge is the only factor driving ETH's outperformance relative to BTC. Thus, a failed or delayed merge would bring us back to $1,081 (the ETH low on July 17) * Liquidity Beta (1.0172), which equals $1,099. However, in this scenario, we could also experience more euphoric printing. DeFi will continue to make strides over TradFi. If history serves as any indicator, as the Federal Reserve expands the money supply again, ETH will suck fiat into its orbit. ETH has risen nearly tenfold from its low in March 2020, when the Federal Reserve expanded global dollar liquidity by 25% within a year. To be conservative, I predict ETH will only rebound to the current level of $1,600.

I assigned an equal probability to the four outcomes. (Clearly, you can use this basic model according to your own opinions, but this is a simple starting point). Then, I calculated the expected returns from current levels to the expected prices in each case, weighted these expected returns by probability, and averaged them together—resulting in the expected value.

Given that the expected future value is 76% higher than today, our forward price for ETH/USD on March 31 is $1,600 (current spot price) * 1.7595, which equals $2,815.

I believe my outcome for Scenario 3 is very cautious, so this is a very conservative estimate. Given that the expected return rate is far above 0%, I can confidently increase my ETH position.

Specific Actions

Let’s evaluate our options for participating in this opportunity.

Spot

This is the most straightforward option. ETH is currently trading at a price 76% lower than my model, and I am willing to buy ETH now. Moreover, I receive an additional bonus because I will obtain an equal amount of ETH from the PoW ETH fork. Once centralized spot exchanges list ETHPoW, I can sell these forked ETHPoW.

Futures

Today (August 4), the ETH/USD futures contract for March 31, 2023, is trading at $1,587. My model futures price is $2,815, so the futures market appears to be undervalued by 44%. Therefore, I will go long.

Call Options

Given that our model indicates the fair value for the March 31 futures contract is $2,815, I should purchase a call option with a strike price of $2,800.

On August 4, the price of the $2,800 strike ETH/USD call option for March 31 on Deribit was 0.141 ETH. Each contract is worth 1 ETH. Using their option pricing model, the important parameters are as follows:

Delta: 0.37. Implied Volatility: 98.3%.

I want to take on more risk regarding the timing of the merge and potential upside, so I purchased a December 2022 option contract with a strike price of $3,000. The shorter the expiration time, the less time value I pay, and considering the high level of implied volatility, this is expensive. My strike price is far from the current market price, which lowers the option's price, but on the other hand, since the term structure presents a smile curve, I will pay more for volatility.

As I formulate my trading strategy to respond to the merge, I will likely purchase more spot ETH and engage in other financing trades to maximize the opportunities presented by market mispricing. Such opportunities are abundant, just like during the Bitcoin fork in 2017.