How to design the token distribution cycle?

As business targets are achieved, shareholders should be allowed to proportionally reward themselves with some or all of the tokens. This also makes it easier for equity entities to be "acquired" by potential buyers.

As business targets are achieved, shareholders should be allowed to proportionally reward themselves with some or all of the tokens. This also makes it easier for equity entities to be "acquired" by potential buyers.Author: Vader Research

Compiled by: Block unicorn

Neither VCs nor founders should receive any tokens for a period of 7 years or more.

We would like to thank Charlie Sandor from CMT Digital for his contributions and feedback. This article would not have been possible without his insights.

Let’s imagine a scenario: a crypto startup raises funds from a venture capital firm for an equity entity and plans to raise more capital for that equity entity in the future. The startup also plans to launch a token in the future, and we assume that most of the overall value created by the protocol will accrue to the token entity rather than the equity entity.

We suggest that either a) tokens should not be allocated to equity investors and the team; or b) tokens should be allocated to equity investors and the team, but there should be a very long lock-up period.

The portion of tokens originally planned to be allocated to equity investors and the team should flow to the equity entity. The equity entity should not distribute tokens to shareholders until the underlying business reaches maturity as measured by certain business metrics.

If, for legal reasons, the above token allocation cannot be executed, then the tokens allocated to equity investors and the team should have a 10-year lock-up period, with the first tokens unlocking starting from the 7th year. That is to say, there should be predefined exceptions (e.g., KPI metrics, acquisitions) that allow them to unlock tokens earlier.

Next, we will discuss:

Proposal for a longer token unlocking schedule

Issues with existing token allocation plans

Traditional early-stage investment

VC model

Conclusion

Proposal

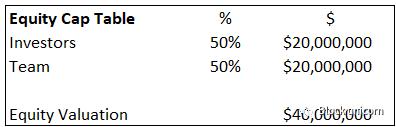

Let’s try to understand the above statements with an example. According to the startup's financing plan, the following equity capitalization table represents its situation before the token issuance.

The basic assumption should be that 100% of the protocol value accrues to the token entity—this is clearly not the case, but any cumulative token value below 100% would introduce uncontrollable additional complexity and undermine the proposal. Please refer to our article on the token capitalization table for a better understanding of the concept of cumulative value.

Assume this startup raised a total of $20 million in multiple funding rounds for this equity entity in exchange for 50% equity. Therefore, equity investors collectively own 50% of the equity entity. The valuation of the equity entity is $40 million, and the equity investors' stake in the equity entity is worth $20 million ($40 million * 50%).

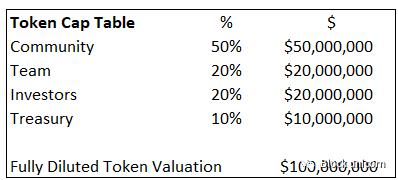

The startup also decided to allocate 50% of the token distribution to the community and 10% to the treasury. The remaining 40% will be allocated proportionally to investors and the team. Since the equity entity has a 50/50 ownership, the remaining 40% token allocation should also be distributed 50/50. Therefore, the ideal token distribution is 20% for equity investors and 20% for the team.

The fully diluted valuation of the protocol is $100 million; that is, the $40 million equity valuation divided by 40% (team + investor token allocation). The investors' stake in the token entity is worth $20 million (assuming the equity entity is nearly worthless).

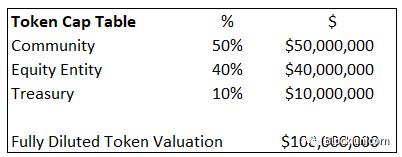

However, we suggest that the remaining 40% of the tokens should flow to the investors and the team, rather than the equity entity.

But why is that?

Issues

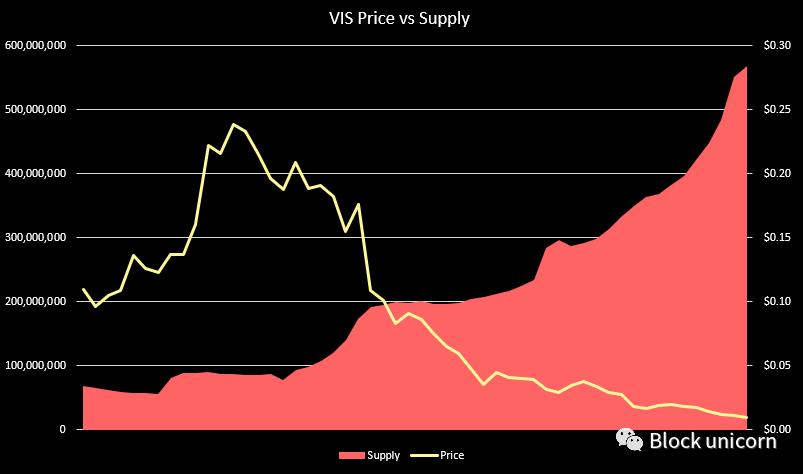

So far, the biggest issue with the token entity is that the speed and quantity of tokens issued from the treasury to circulation exceed the speed and quantity of market demand for the tokens!

Token release growth < Token demand growth | Token price?

Token release growth > Token demand growth | Token price?

VIS token price vs circulating supply

While there are many ways to try to address this issue, which is the subject of another article, a direct solution related to this article is to delay the unlocking of tokens for investors and the team as much as possible.

Tokens for investors and the team will be locked for a period of time. Once the tokens are unlocked, investors and the team typically cash out immediately—this undoubtedly puts further selling pressure on the token price as the supply of tokens in circulation increases.

Early protocols in crypto projects essentially use token incentives to drive user liquidity. By continuously distributing tokens to users to incentivize protocol activity. Therefore, the existing inflationary pressure to maintain and grow the ecosystem is inherently present. Selling their tokens before the platform is sufficiently mature will lead to further selling pressure.

Moreover, when founders cash out tokens before the product launch, they gradually lose the motivation and passion to develop the product. And incentivizing founders with a shorter lock-up period will lead them to focus on marketing the token by selling a product that will never be released to retail investors, rather than focusing on actually building the product and understanding customer pain points.

The same reasoning applies to investors; they support the company and pay a large amount of tokens before their lock-up period ends. Then, they sever their ties with the company and no longer support it—because they have little incentive to support the company's long-term success. As long as the price is high when their tokens unlock, they will be happy. This is where the incentives of private investors conflict with those of founders and the community.

We believe that investors and the team should not be able to sell their stakes until specific business metrics of the platform are met, regardless of whether it takes 5 years or 15 years for the business to reach those standards!

Let’s look at some examples of lock-up periods in existing projects:

AXS (Axie Infinity)

Source: AXS Whitepaper

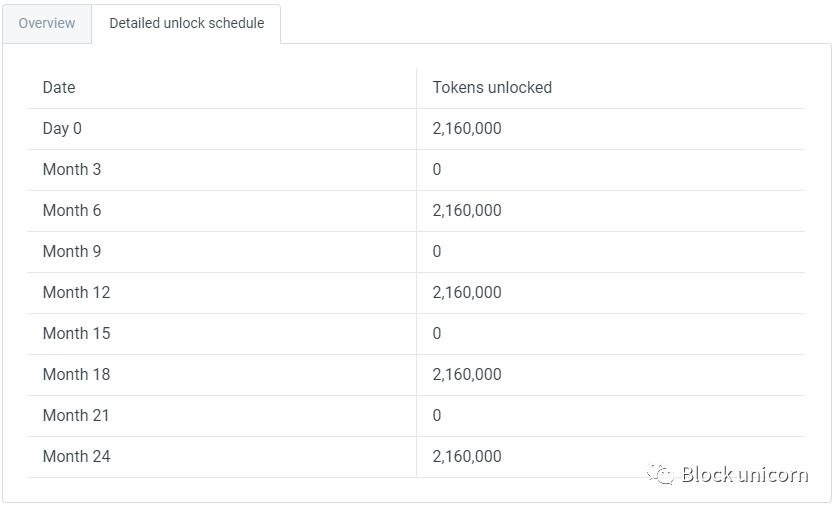

AXS private investors can unlock tokens every 3 months within two years from the date of launch. AXS allocated 4% of the tokens to private investors, which is a noticeably low figure compared to other projects, but the existing unlocking period is relatively short.

The above shows the detailed lock-up period for AXS private investors

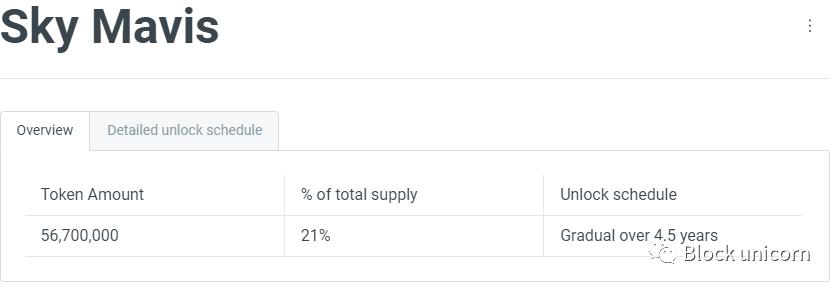

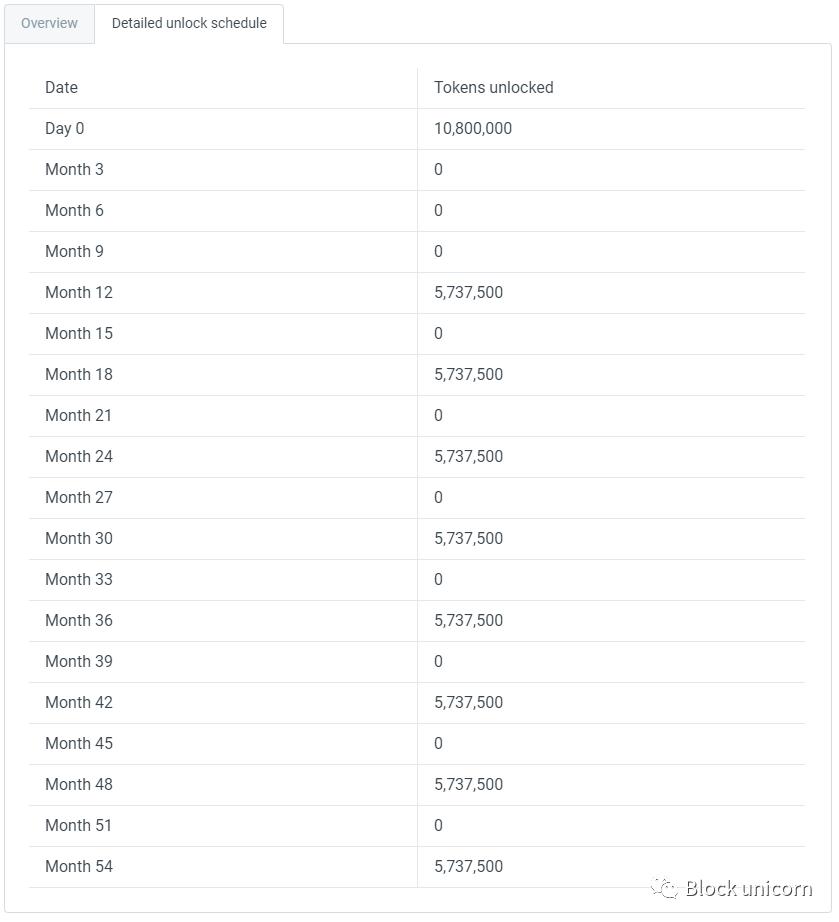

Tokens allocated to Sky Mavis (the equity entity) will unlock over 4.5 years—at first glance, this seems to be a relatively long lock-up period, but note the details.

19% of the tokens allocated to Sky Mavis were unlocked on the day of launch. Therefore, in reality, only 4% of the total token supply is held by the equity entity. While we do not know whether these tokens are held by Sky Mavis or distributed to team members or equity investors (who may have also cashed out).

YGG (Yield Guild Games)

Source: YGG Whitepaper

25% of YGG tokens are allocated to investors, with a total lock-up period of 5 years. However, about 30% of investors' tokens were unlocked at the time of the public sale of the tokens. This actually represents 7.5% of the total supply! About 80% of investors also unlocked their tokens two years after the token launch. This is certainly not a long-term lock-up period.

Traditional Early Investment

By selling "dreams" or "experiences" to retail investors, crypto enables founders and investors to exit early even without selling a product. Next, let’s see how exits for traditional early-stage investors work.

VCs invest in a startup and can only exit 1) when the company goes public (IPO) or 2) before the company is sold. According to Crunchbase, the exit path often takes 10 years.

Source: Acuris

There is actually a third option— a venture capital firm sells its illiquid private equity holdings to another venture capital firm through a secondary transaction. These transactions may require approval from the startup's board of directors based on the shareholder agreement. Additionally, there may not be enough buyer VCs willing to pay the price the selling VC wants to execute the transaction.

Since VCs must make long-term commitments, they typically spend a lot of time on due diligence to ensure they are betting on the right horse. Because once they actually make an investment, they have a strong incentive to create as much value as possible. The lack of short-term exit options also holds VCs accountable for their investment decisions—after all, the mindset of a VC investing for 10 years is very different from that of a trader betting for 1 year.

This also gives founders and employees the same options as VCs. Due to shareholder agreements and other legal reasons, it is even more difficult for them to sell illiquid, private equity. Therefore, they also have the motivation to ensure a successful exit in the future, as the company performs better, they can justify paying themselves higher salaries.

Thus, participants, investors, and founders in the traditional early investment industry are incentivized to build a long-term viable business without any early exit opportunities.

VC Model

Venture capital firms do not manage their own capital—they invest other people's money into startups. Venture capital firms are merely agents with a fiduciary responsibility to select the best investment opportunities for their clients, execute those opportunities, and return capital after 10 years.

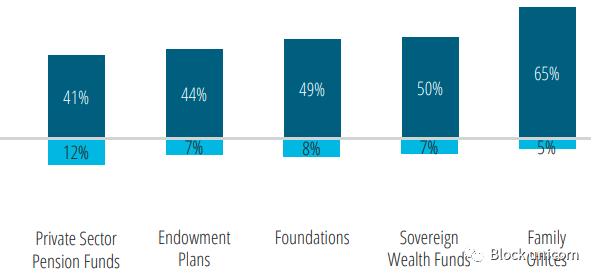

The "other people" are called limited partners—they are wealthy individuals, sovereign wealth funds (Saudi Arabia, Norway, etc.), pension funds (Yale University, BP), endowment funds/foundations (Gates Foundation), and other capital allocators. These institutions lack the talent and expertise to build internal teams to directly invest in these deals, so they ultimately invest in venture capital firms that specialize in specific areas and have a track record of successful investments.

Types of investors allocating capital to venture capital firms

The typical agreement between venture capital managers and limited partners is that the venture capital firm will not return funds for at least 10 years—in other words, the fund has a lifespan of 10 years. VCs invest in the first 3-4 years, and the remaining years are used to harvest returns.

The conclusion drawn from the VC model is that VCs are never in a hurry! Their job is to make long-term investments, so they do not need to exit an investment in the short term, at least not within 5-6 years.

Why have an equity entity? Why not just set a longer token lock-up period directly?

Allocating tokens to the equity entity not only grants shareholders more control and legal power but also allows for unilateral governance decisions related to the token protocol.

If the protocol has potential acquirers, they will find it easier to obtain 40% of the tokens and the legal interests of the equity entity, rather than having to acquire tokens from the public or negotiate bilaterally with each investor.

What are the potential issues with the equity entity holding a large number of tokens?

The SEC suggests establishing a regulatory framework for digital tokens based on the degree of decentralization of the token network. An equity entity holding 30%-40% of the token network may not meet the SEC's minimum decentralization requirements.

Another potential issue could be double taxation. Once the underlying business matures and decides to distribute tokens as dividends (in-kind payments) or is acquired by another company—its investors may need to pay taxes twice.

Conclusion

We recommend that tokens should not be allocated to equity investors, but rather that team tokens should be allocated to the equity entity. These tokens held by the equity entity should not be unlocked and distributed to shareholders until certain predefined business metrics are met. As business metrics are achieved, shareholders should be allowed to proportionally reward themselves with some or all of the tokens. This also makes it easier for the equity entity to be "acquired" by potential acquirers.

Alternatively, the token lock-up period should be extended to over 10 years, but with predefined business KPI targets or potential acquisition transactions as exceptions.

Risk warning

Risk warning Risk warning

Risk warning