AC's first post after leaving the circle discusses the crypto winter, macro environment, and lack of regulation

The recent decline in the cryptocurrency market has revealed systemic flaws, necessitating regulation to curb irresponsible behavior and protect consumers.

The recent decline in the cryptocurrency market has revealed systemic flaws, necessitating regulation to curb irresponsible behavior and protect consumers.Title: The Crypto Winter of 2022

Author: Andre Cronje, Founder of Yearn Finance

Compiled by: Anderson Li, Cointelegraph Chinese

1. Introduction

The cryptocurrency market experienced a massive shock in 2022, with the prices of various cryptocurrencies plummeting and the failures of networks and exchanges resulting in a total loss of $2 trillion.

So far, some of the biggest shocks to the market include the collapse of Terra LUNA/UST, Celsius Network filing for bankruptcy, Voyager Digital filing for bankruptcy, and the downfall of Three Arrows Capital. These shocks are not isolated events; they have had a significant impact on the entire market, leading to declines in the prices of Bitcoin and Ethereum. The most severe issue arising from this is that users' cryptocurrencies are locked in exchange accounts or their funds are in the hands of others, managed by others.

Investors who suffered losses during the "crypto winter" are unsure of what remedies they can pursue, and they do not know if they can seek compensation from the irresponsible parties within this system.

Remedies under the current regulatory framework are ineffective. Most investors have signed away their rights to cryptocurrencies in the vast terms and conditions of crypto exchanges, and if these exchanges are liquidated, many will (at most) become unsecured creditors.

Crypto exchanges and crypto investment service providers essentially operate like banks but without the safeguards and regulations that banks must follow. The reasons for the recent collapses are neither particularly unique nor novel; similar irresponsible practices can be found in the collapse of traditional financial markets in 2008.

These behaviors and their impact on the market are also not new, especially in a market that relies more on consumer expectations than any other. Many regulators have raised the question of how to protect consumers in the crypto market, and the answer is to adopt relative safeguards from traditional finance. That is: requiring exchanges to hold minimum reserves, mandating service providers to obtain licenses, regulating risk exposure, establishing transparency standards, and incorporating cryptocurrencies into the scope of financial products.

This brings us to the first, and perhaps most important, recent collapse of Terra USD and Luna. Terra was once praised for providing cutting-edge blockchain investments to global users, but is now blamed as a catalyst for the crypto winter of 2022. What went wrong and why are key questions the market has been grappling with—and they are questions that regulators are also considering.

2. Terra Luna/Terra USD (The Collapse of a Cryptocurrency)

2.1. The Collapse

Terra USD (UST) is a so-called stablecoin launched by Terraform Labs. The coin is algorithmically pegged to the US dollar, using another Terraform cryptocurrency, LUNA, to maintain its peg. The system operates through an arbitrage network, trading LUNA and UST back and forth—when there is profit, one is sold and the other is bought, increasing the demand for the cheaper coin and pushing its price back up. For a long time, this practice was effective, and UST maintained a near 1:1 exchange rate with the dollar. This mechanism also burned the coins being traded, which contributed to the collapse.

Part of Terra's ecosystem and stabilization mechanism is the Anchor Protocol, which is similar to a savings account where a large amount of UST is deposited to earn high long-term yields. At its peak, Anchor held nearly 75% of all circulating UST—UST's value was highly dependent on the operation of this pool.

Anchor Protocol borrowed UST from lenders and lent it to borrowers, achieving about a 20% yield for lenders—this function is very much like a bank. Starting in March of this year, this yield became unstable, fluctuating with the reserves held by Anchor Protocol (the capital retained by Terra to meet the yield). As more lenders were attracted by the high returns, the reserves began to dwindle. A temporary solution was to inject more UST into the Anchor Protocol to boost reserves. Clearly, this could not continue, as Anchor Protocol did not have enough appeal to users, and users would not continue to invest.

In May 2022, $2 billion worth of UST was withdrawn and liquidated from Anchor Protocol. This put immense pressure on LUNA, as arbitrageurs exploited the price differences, causing the spread between LUNA and UST to widen significantly, which should not have happened. The Luna Foundation attempted to inject more UST into the system to bridge this gap (remember, when LUNA is minted, UST is burned), seeking to regain control and balance the prices of the two cryptocurrencies.

As a large amount of LUNA entered the market, it could no longer maintain its value, leading to a subsequent crash. The Luna Foundation's efforts to stabilize UST/LUNA using its reserves of Bitcoin also failed, resulting in a massive influx of Bitcoin into the market—supply exceeded demand, leading to a drop in Bitcoin prices.

2.2. Where Did It Go Wrong?

A series of issues led to the collapse of Terra: insufficient reserves, flawed algorithms, and the Anchor Protocol not setting withdrawal limits.

If there had been restrictions to explain large withdrawals, perhaps UST would not have decoupled.

In May 2022, Jump Crypto reviewed the activities of UST/LUNA and found that only a few large transactions were responsible for the instability and collapse of the currency. These transactions traced back to a handful of wallets, the identities of all of which remain unknown. It is concerning that a few individuals could destabilize the entire cryptocurrency ecosystem without facing consequences or accountability. This will be further discussed below.

For a more comprehensive analysis of what went wrong with Terra, refer to Nansen's report at https://www.nansen.ai/research/on-chain-forensics-demystifying-terrausd-de-peg.

2.3. Withdrawal from Anchor Protocol

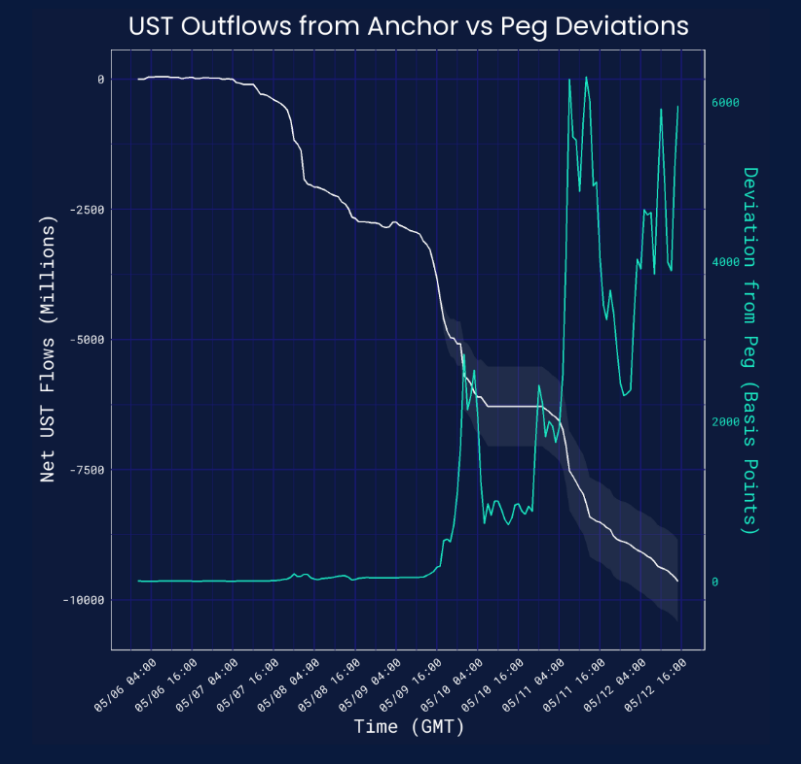

The $2 billion withdrawn from Anchor Protocol has been traced back to seven wallets, including Celsius Network.

The following image illustrates the increasing deviation of UST from its peg to the dollar as UST was withdrawn from Anchor.

During Nansen's analysis of UST's decoupling, seven wallets were identified as having a significant impact on the decoupling (see the image below). One of these wallets has been identified as belonging to Celsius, and its withdrawals from Anchor Protocol caused more harm than good. This will be further discussed in the next section.

The actions of several major UST holders were sufficient to destabilize the Terra ecosystem and cause losses for small wallet holders, who were unable to seek recourse.

Shockingly, as we will see, the collapse of Terra directly led to the collapse of many crypto hedge funds and networks. These funds and networks had "stablecoin" (an algorithmic stablecoin) positions that were too heavy, and this high-risk investment behavior resulted in losses for millions of users' funds.

Even so, the impact of the collapse of Terra cannot be entirely blamed on it; the large lenders and investors in the crypto market also lacked prudent practices and must bear their share of responsibility.

3. Celsius Network (The Collapse of a Cryptocurrency Exchange)

The renowned cryptocurrency exchange Celsius Network filed for bankruptcy in the United States. On June 12, Celsius froze investors' accounts, and after a month of uncertainty, Celsius announced its bankruptcy almost without warning, citing poor liquidity at the exchange.

The reasons for Celsius's inability to meet investor withdrawals remain unclear; they seem to involve excessive leverage (and insufficient reserves), poor decision-making by relevant parties, and possible misconduct by major crypto asset holders and Celsius executives.

3.1. ETH and stETH

To understand the recent collapse of Celsius and its associated token CEL, I will briefly explain Celsius's staking behavior.

Celsius heavily invested in stETH, a token representing ETH (the Ethereum network token) staked on the Ethereum 2.0 Beacon Chain, which is a "upgraded" Ethereum blockchain using different validation methods. The goal of stETH is to earn rewards during the "upgrade" of the ETH platform. The Ethereum merge transitions the current Ethereum network from a proof-of-work consensus mechanism (validation method) to proof-of-stake. stETH essentially locks ETH in decentralized smart contracts to earn rewards for long-term investors. To earn rewards, users stake their stETH in various network liquidity pools, which peg the price of stETH to the price of ETH. They can then earn rewards based on the future value of ETH on the new network.

Celsius users hand over the keys to their ETH tokens to Celsius, which then stakes these tokens as stETH in the form of smart contracts. When Celsius wants to withdraw ETH, it sells stETH in the Curve liquidity pool in exchange for ETH. Overtrading and withdrawing stETH for ETH led to instability in the 1:1 price peg—an increase in demand caused the price of ETH to rise. That is, as the Curve liquidity pool was depleted, Celsius no longer had enough ETH to meet customer withdrawals. The first decoupling of stETH was similar to the collapse of Terra, as users sought to return to the main network for trading due to concerns about instability. Nansen's report shows that a second event exacerbated the decoupling, as other major players attempted to sell their stETH positions.

This led to a bank run on Celsius, with users panic withdrawing their investments, resulting in Celsius freezing the network. The subsequent liquidity crisis led Celsius to file for liquidation on July 17, 2022.

3.2. Anchor Protocol

Celsius had a significant amount of user funds invested in Terra's Anchor Protocol. Although it withdrew most of its funds before the collapse of Terra, this also proved to be a double-edged sword. The withdrawal of funds put pressure on UST's decoupling, causing consumers to panic about the instability of the crypto market—leading to widespread withdrawals and price declines.

This also affected other currencies held by Celsius, particularly Bitcoin, which was directly impacted by Terra's attempts to stabilize UST (leading to a drop in Bitcoin prices).

3.3. Bad Loans

In its bankruptcy filing, Celsius classified 30% of user loans as bad debts—approximately $310 million. These are loans that borrowers (from Celsius) were unable to repay, essentially written off on Celsius's books.

Celsius further disclosed that Three Arrows Capital owed it nearly $40 million in debt—given Three Arrows Capital's bankruptcy, repayment is now unlikely.

Overall, the exchange reported a deficit of nearly $1.2 billion on its balance sheet—CEO Mashinsky attributed this to "bad investments."

3.4. Allegations of Misconduct and Lack of Regulation

Since freezing investor accounts in June 2022, multiple lawsuits have been filed against Celsius Network, some of which allege clear fraudulent behavior by the company.

Some actions taken before the freezing of investor accounts remain unexplained by Celsius, such as a payment of $320 million to the FTX exchange and the high-leverage positions held by Celsius. The payment to FTX was made shortly before customer accounts were frozen, allegedly to repay a loan. In ordinary liquidation procedures, this is preferential treatment for creditors in the event of impending bankruptcy. Typically, a court may order the reversal of payments so that creditors can be treated fairly based on the hierarchy of debts—even if creditors are not at fault in accepting preferential payments.

The statistics above are the last weekly statistics provided by Celsius before freezing customer accounts. The week of May 6—May 12 showed significant outflows of funds and negative position returns.

Celsius essentially behaved like a bank without the institutional framework supporting banking operations. Accepting customer assets (cryptocurrencies) looks very much like the absorption of deposits in traditional finance, which is a heavily regulated practice. Further lending out these deposits by staking them in liquidity pools also resembles how banks handle customer deposits, but without the insurance provided in traditional finance.

Before the collapse of Celsius, CEO Alex Mashinsky's tweets were misleading to the public. At the very least, they violated his fiduciary duty to Celsius. There are also claims that Mashinsky directly told the public that Celsius had minimal exposure to UST risk—this was not true, as it was one of the largest wallets affecting UST's decoupling.

In fact, until June 12, Celsius was actively attracting new customers, launching promotional products aimed at attracting liquidity, and offering rewards to customers who accepted a six-month lock-up period.

Mashinsky's tweet on June 12 was a response to user inquiries about withdrawals, reportedly indicating that the withdrawal function had been malfunctioning for several days before accounts were frozen.

Given that cryptocurrencies are not regulated like financial products or fiat currencies, it cannot be said that Celsius violated regulations. However, they can be deemed negligent for not implementing prudent practices and/or intentionally misleading consumers.

Regardless, Celsius has now filed for bankruptcy, and consumers cannot help but wonder what remedies they have left—the answer is very few.

3.5. Consumer Rights in Bankruptcy

In July 2022, Celsius filed for bankruptcy under Chapter 11. In the U.S., this allows companies to restructure their debts while keeping their business operations running.

Generally, Chapter 11 bankruptcy prioritizes the repayment of secured creditors first, followed by unsecured creditors, and finally equity holders. Most account holders at Celsius are unsecured creditors, who will only be compensated after secured creditors (who typically have the highest unpaid debts) are paid, and only in proportion to the remaining available assets in Celsius's accounts.

This is because when depositing fiat or cryptocurrencies into Celsius, those currencies become part of a pool of funds composed of deposits from other users ("commixtio"). Therefore, users do not have the right to demand the return of specific fiat or cryptocurrencies but can only request the return of the value they contributed, adhering to the agreement with Celsius, which is detailed in the terms and conditions. The protections and ownership rights related to deposits in ordinary banking law do not apply to crypto exchanges, and agreements with crypto exchanges can exempt them from full liability for deposit losses.

The risk of total loss of deposits held by users in Celsius is disclosed and exempted in Celsius's terms:

"By lending qualified digital assets to Celsius or otherwise using the services, you will not have any rights to any profits or income that Celsius may generate from any subsequent use (or otherwise) of any digital assets, nor will you face any losses that Celsius may incur as a result. However, you will face the possibility that Celsius may be unable to partially or fully repay its debts, in which case your digital assets may be at risk."

It is worth noting that depositing fiat currency here is no different from depositing digital assets. Typically, when assets are lent out, the owner retains ownership. The owner has the right to demand the return of their assets (to prove their ownership). This is not the case here, as depositors have relinquished ownership of their crypto assets and only have an unsecured claim to the value they contributed.

"Subject to applicable law, by choosing to use qualified digital assets in the Earn Service (if you are eligible to use it), thereby lending those qualified digital assets to us through your Celsius account, or during the period in which they are used as collateral in the Borrow Service (if you are eligible to use it), you grant Celsius all rights and interests in those qualified digital assets, including ownership, and the right to hold that digital asset in Celsius's own virtual wallet or elsewhere without further notice to you, as well as to pledge, re-pledge, hypothecate, multiple hypothecate, sell, lend, or otherwise transfer or use that digital asset, alone or with other property, and all attendant ownership rights, during any period of ownership."

When regulating the crypto industry, crypto exchanges will be the first stop for regulators. While we advocate for the decentralized nature of decentralized finance, these exchanges are, in fact, centralized—serving as access points to a centrally controlled crypto market. Investors entering crypto exchanges have no rights to their "deposits," while in traditional finance, deposits are specially protected by law. Traditional finance also provides a degree of transparency for depositors, whereas crypto exchanges do not. This practice of transferring control of cryptocurrencies from investors and the lack of transparency completely distorts the purpose of blockchain and decentralized finance, leaving investors questioning why they chose decentralization over traditional finance. Below, I will further discuss some potential regulations that, if properly implemented, could not only protect this industry but also promote its development.

4. Three Arrows Capital (A Cryptocurrency Hedge Fund)

In mid-2022, the collapse of Three Arrows Capital (3AC) surprised many within the industry. 3AC was a cryptocurrency hedge fund founded in 2012, investing in crypto assets since 2017. 3AC's strategy primarily involved crypto derivatives, but its portfolio also included investments in crypto companies developing crypto products and technologies. At its peak, 3AC's assets under management reached $10 billion.

3AC's downfall is related to its exposure to Terra. 3AC had purchased 10.9 million LUNA for $500 million and then locked these coins up for staking. With the collapse of Terra, the value of 3AC's holdings diminished, and the LUNA it held was now worth only $670.

3AC also held a significant amount of Grayscale Bitcoin Trust ("GBTC"), which has been trading at a discount since the rise of crypto ETFs. After the collapse of Terra, 3AC's main strategy was GBTC arbitrage, hoping that GBTC would be approved for conversion to an ETF, reversing the discount. This did not happen, as Bitcoin's price fell due to Terra selling its Bitcoin reserves, further depleting 3AC's other holdings' value. 3AC also used GBTC shares to purchase stablecoins, which brought it back to its purchases of Terra, all to repay Bitcoin loans. 3AC is no longer a holder of GBTC, having sold all its positions at an undisclosed time—presumably at a loss.

Like Celsius, 3AC was also affected by stETH—losing value as stETH depreciated. Additionally, reports indicate that 3AC was a massive borrower of crypto assets—especially Bitcoin—meaning that corresponding bad debts were likely to appear on the lenders' books. Voyager Digital was one of these lenders, having lent 3AC an unsecured loan of $660 million. Voyager Digital has now also filed for bankruptcy.

3AC is one of the best examples illustrating the interconnectedness of the cryptocurrency market, where relatively small shocks can have a larger impact on an over-leveraged, under-reserved ecosystem. After all, Terra is just one of many exchanges and one of many systems; it cannot be isolated from other exchanges. Critics point out that 3AC reached too many lenders, many of whom absorbed deposits from retail investors, increasing their debts to unsustainable levels. Thus, 3AC's investment decisions not only affected institutional clients but also retail investors, permeating through ordinary network users who provided bad loans to 3AC.

In addition to poor investment decisions, 3AC has also faced condemnation from Singaporean authorities for making misleading and false disclosures to lenders to obtain more loans—allegations of fraud.

As Decrypt noted: "In a sworn statement submitted on June 26, Blockchain.com's Chief Strategy Officer Charles McGarraugh revealed that 3AC co-founder Kyle Davies told him on June 13 that Davies wanted to borrow another 5,000 Bitcoin from Genesis, worth about $125 million at the time, 'to pay additional margin to another lender.' This behavior is common in Ponzi schemes, where money from later investors is used to pay earlier investors."

This highlights the lack of prudent oversight in crypto asset lending, as the industry has failed to check the risky behaviors of major players seeking quick returns.

5. Impact on the Underlying Market

Due to the current global economic downturn, the collapse of cryptocurrencies has become more severe. Interest rate hikes, wars, and shortages of energy and food have all fueled consumer expectations—affecting market behavior and even impacting crypto assets.

As the global financial outlook grows dimmer, consumers are looking to reduce risk and seek safer investments, including safer crypto investments and traditional investments. This includes investing in lower-risk crypto products, such as ETH instead of stETH.

If consumers' deposits in cryptocurrencies have no safety guarantees, it will fuel panic towards exchanges and staking pools—this is exactly the situation faced by Celsius and Anchor. Regulators are becoming increasingly aware of market manipulation, indicating the need for checks and balances in the major institutional roles within the crypto market. The uncertainty of regulation further exacerbates consumers' negative expectations, prompting the market to shift towards investments perceived as safer.

The crypto market is part of the global economy and will therefore experience fluctuations depending on the sentiments of ordinary consumers. However, the industry's cyclical fluctuations can be addressed through regulatory intervention, so that shocks to the system do not have catastrophic effects like those seen recently.

6. The Necessity of Regulatory Reform

Economists have conflicting views on why and when regulation should occur. These theories apply not only to banks but also to crypto exchanges and institutions providing bank-like services—absorbing deposits, generating interest, and lending. These theories often touch on monopoly, information asymmetry, and externalities.

Negative externalities refer to costs borne by third parties due to economic transactions. In banking, examples include: (i) bank runs on solvent banks; (ii) economic distress or collapse caused by bank failures; and (iii) rising costs of government-provided deposit insurance.

Monopolists in banking can lead to unfairness for consumers, as major players face no competitive challenges and can manipulate the market.

Information asymmetry involves the exploitation of consumers due to a lack of transparency, leading consumers to make unfavorable decisions. Consumers often do not have the same level of maturity in understanding investments and risks as banks do, and they need protection.

Recent shocks have clearly demonstrated all three of the above issues' impact on the crypto market. After the collapse of multiple crypto exchanges and investment funds, the market has evidently faced economic distress. The market is concentrated among a few major players, showing potential manipulation of the market both on-chain and through social media (think of the few wallets that destabilized the Anchor Protocol). The interconnectedness of the market also means that when one entity goes bankrupt, it cannot isolate other participants. These exchanges and investment funds lack transparency—consumers do not actually know where their funds are going or understand the information they receive—this is clearly an issue of information asymmetry.

All these issues provide good reasons for aligning the regulation of the industry with that of traditional finance, so that consumers are both protected and can enjoy remedies when they suffer losses.

6.1. Remedies in Traditional Finance

6.1.1. Central Bank Insurance

After the Great Depression, many central banks worldwide adopted mandatory insurance practices, forcing banks to purchase minimum amounts of insurance for deposits to ensure consumer protection in the event of bank failures.

This provides security for depositors and enhances confidence in banks during financial difficulties, reducing the phenomenon of bank runs. In countries without explicit deposit insurance schemes, central banks may also exercise discretion to compensate consumers who lose deposits in failed banks—this is assessed on a case-by-case basis.

The safety net of deposit insurance is a remedy that consumers can enjoy in traditional banking, whereas depositors in crypto exchanges (like Celsius) cannot enjoy this measure.

6.1.2. Prudent Regulation

In traditional finance, banks are subject to the authority and prudent regulation of central banks—essentially ensuring that banks operate legally and in compliance. If a central bank provides insurance to private banks engaging in high-risk activities and uses taxpayer money to compensate when those private banks encounter problems and are forced to close, that is irresponsible.

A strong regulatory framework that establishes rules for absorbing public deposits and supervises the use of those deposits can reduce bank failures and increase public confidence in the banking system.

Many central banks around the world regulate private banks based on these factors: capital, asset quality, soundness of management, profitability, liquidity, and sensitivity to risk (if risks are managed prudently). This can similarly apply to cryptocurrency investments and exchanges.

6.2. Remedies Available to Consumers

In traditional finance, most consumers can seek assistance from relevant regulatory bodies when harmed by imprudent (or illegal) banking practices.

Currently, in most jurisdictions, when exchanges or investment vehicles file for bankruptcy, consumers have rights as unsecured creditors. As mentioned above, they typically find themselves at the end of a long line of creditors, meaning their compensation is minimal.

Consumers also need to review their contracts with exchanges or investment companies to seek appropriate remedies. Unfortunately, many contracts (especially fine print) are vague and deny compensation for losses consumers may suffer. Currently, consumers should read all applicable investment terms and refrain from investing unless they are comfortable with the worst-case scenarios covered by those terms.

Of course, if there is fraud involved in any company's transactions that leads to consumer losses in investments, consumers can seek compensation in civil courts. However, this is a long and costly process that is not worth the time and expense for most consumers.

Like most industries, there are safety risks. Because crypto transactions are often jurisdictionless and anonymous, it is challenging to trace hackers. This is a consideration regulators need to take into account when implementing minimum regulations, which may hold exchanges accountable for losses to consumer wallets.

7. Pending Regulation

Most jurisdictions worldwide have plans to regulate cryptocurrencies. Some want to declare them as commodities, some as fiat currencies, and some as financial products.

In the European Union, anti-money laundering regulations require crypto asset service providers to hold licenses to provide services. This is different from the licenses required to provide financial services and does not come with the same reporting standards. The Markets in Crypto-Assets (MiCA) bill has been submitted to the European Parliament and is expected to pass in 2024—it aims to align crypto asset service providers more closely with the financial industry.

MiCA has the following objectives:

To provide legal certainty for crypto assets not covered by existing EU financial services laws, where there is currently a clear demand.

To establish a unified framework for crypto asset service providers and issuers across the EU.

To replace the current national frameworks applicable to crypto assets with EU financial services regulations; and

To establish specific rules for so-called "stablecoins," including electronic money.

Crypto assets defined as financial instruments or electronic money under the EU Markets in Financial Instruments Directive (MiFID) and the Electronic Money Directive (EMD) are not covered by MiCA. The purpose of MiCA is to coordinate regulation and "capture" crypto asset activities that fall outside existing regulations.

The bill specifically sets out licensing requirements for crypto asset service providers and establishes reserve requirements for stablecoins. While MiCA does not cover all aspects of the crypto world, it does address some significant issues in the market—particularly in regulating the services offered by crypto exchanges and establishing responsibilities for consumer protection.

Globally, the crypto industry will benefit from regulation of crypto assets, which imposes prudent standards on the industry (setting thresholds and reporting for safe operations) while providing consumers with a clear avenue to enforce their rights and a designated regulatory body for protection. These regulations can prevent excessive pursuit of risky assets and boost market confidence in the industry.

8. Conclusion

The recent decline in the cryptocurrency market reveals systemic flaws that require regulation to curb irresponsible behavior and protect consumers.

The collapse of Terra is not an isolated incident; it marks a turning point for over-leveraged crypto hedge funds and exchanges. Celsius is one of them, not only over-invested in Terra but also a major participant in driving the run on Anchor Protocol. The exposure to stETH, another tool that decoupled, exacerbated Celsius's losses.

3AC may be one of the best examples illustrating the ripple effects produced across the entire industry. As a significant borrower facing bad debts on exchanges, 3AC's over-leveraged positions led to liquidation. Behind all the turmoil are the irresponsible actions of executives at these funds and exchanges, gambling with other people's money while facing no severe consequences themselves.

Participants in the crypto market may be private enterprises, such as hedge funds, but they still impact the overall market as they hold a large proportion of market resources. As we have recently seen, implementing regulation on all those who could disrupt market stability can provide consumers with much-needed protection and assist in achieving long-term market stability.

Risk warning

Risk warning Risk warning

Risk warning