How will the market landscape of stablecoins be reshaped?

The competition in the stablecoin market has never ceased, with participants continuously emerging, promoting new concepts such as decentralization and algorithmic support.

The competition in the stablecoin market has never ceased, with participants continuously emerging, promoting new concepts such as decentralization and algorithmic support.Written by: Azuma, Odaily Planet Daily

"The Second Great Stablecoin War has officially begun."

This was the comment made a few days ago by FTX founder Sam Bankman-Fried (SBF) regarding the recent competition and market share changes in the stablecoin market.

Rewind to around 2018, when several over-collateralized stablecoins backed by fiat currencies engaged in a fierce battle. Ultimately, the first-mover advantage of USDT and the compliance endorsement and excellent liquidity scenarios of USDC defeated competitors like TUSD, GUSD, USDP, and HUSD, winning the "First Stablecoin War."

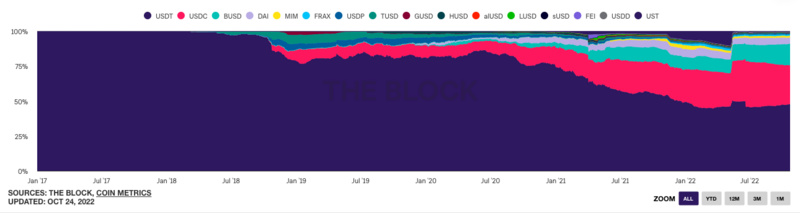

Since then, competition in the stablecoin market has never ceased, with new entrants touting concepts like decentralization and algorithmic backing emerging continuously. However, the dominant positions of USDT and USDC have remained unshaken (one of the rare "surprises" during this period was UST, but its previously strong momentum has been proven unsustainable by reality). In the king-level competition, the rivalry between USDT and USDC has generally been mild; although USDC has taken a significant share from USDT thanks to the DeFi boom, the comparison of their market shares has not changed much since entering 2022 as DeFi cooled down.

The Block's stablecoin market share change chart, with the purple section representing USDT and the red section representing USDC.

If the story continued to develop at this pace, USDT and USDC seemed poised to maintain their thrones, and the overall landscape of the sector might gradually solidify… but changes always come unexpectedly.

Main Battlefield: BUSD vs USDC

The change began in September this year, initiated by the aforementioned "surprise" BUSD and its backing ecosystem from Binance.

BUSD is a stablecoin issued in cooperation between Binance and Paxos, approved by the New York State Department of Financial Services (NYDFS) and backed 1:1 by the US dollar. Similar to USDC, BUSD also follows a compliance route and is backed by one of the top exchanges in the market, but due to its later inception, its market presence has always been weaker than the former. However, over time, while USDC and USDT compete directly in the open market, BUSD has gradually accumulated an issuance scale of over a hundred billion dollars, leveraging Binance's traffic advantage and the support of the BNB Chain ecosystem, slowly expanding its market share to over 10%, initially qualifying to compete with the two major leaders.

On September 5, an announcement from Binance ignited the flames of war. In the announcement, Binance stated that on September 29, it would automatically convert the existing USDC, USDP, and TUSD stablecoin balances and new deposits of platform users into BUSD at a 1:1 ratio, and would delist several trading pairs involving the above three stablecoins. Subsequently, other exchanges under Binance, such as WazirX, also followed suit.

In short, Binance is intervening in the usage scenarios within its sphere of influence to affect the supply and demand situation between BUSD and other stablecoins like USDC. Although the deposits and withdrawals of stablecoins like USDC are not affected, since these stablecoins will automatically convert to BUSD within Binance, over time, user habits will gradually form—except for some relatively low-frequency necessary scenarios (such as needing to withdraw USDC to mine a certain token), in more frequent scenarios (mainly trading and platform financial management), users only need to hold BUSD.

It has been proven that Binance's move has yielded excellent results. According to CoinGecko data, from September 5 to October 27, the issuance scale of BUSD has grown from approximately $19.427 billion to $21.42 billion, while the issuance scale of USDC has dropped from $51.903 billion to $43.904 billion.

Of course, the significant drop in USDC's issuance scale is not solely due to Binance's actions but is the result of multiple factors.

First, the overall downturn in the crypto market has suppressed trading demand for stablecoins, and the reduction in market activity has led to a continuous decline in the yields of stablecoin deposits. On the DeFi side, USDC, as the most widely adopted stablecoin in DeFi, has been most affected; on the CeFi side, due to Circle's yield capabilities being inferior to Binance's, it cannot provide USDC with sustained financial returns like Binance does with BUSD, which is awkwardly reflected in Circle Yield's current 0% long-term financial yield.

Another key factor is the tightening of regional regulations, especially after the U.S. Treasury sanctioned Tornado Cash, leaving Circle, based in the U.S., under greater regulatory and public pressure regardless of its actions.

Under such pressure, USDC naturally will not "sit idly by." Its recent actions include three noteworthy points. First, Coinbase, one of USDC's strongholds, has waived fees for purchasing USDC with fiat; second, Circle will launch a new cross-chain transfer protocol to enhance USDC's interoperability; third, Circle has reached a payment infrastructure cooperation agreement with major brokerage and trading platform Robinhood, which has also listed USDC.

These three initiatives, the first is to leverage USDC's influence within its sphere, similar to how Binance strongly supports BUSD, which is a "defensive" operation; the second is to consolidate advantages in a public domain where it has already ventured but cannot control, while the third attempts to explore entirely new areas, all of which are "offensive" operations.

Overall, the current battle between BUSD and USDC is still in its early stages, so it is too early to discuss victory or defeat. However, considering that both sides have essentially cleared each other's influence within their spheres (Binance and Coinbase platforms), whoever can capture more market share outside their spheres of influence will become the key factor determining the direction of the battle.

The external scope here includes other major players like FTX, which currently holds a neutral stance (SBF stated today that FTX has not yet determined details regarding stablecoin development but does not rule out future actions), as well as potential traditional financial platforms like Robinhood, and the completely open and free DeFi market (which may also be why CZ mentioned a few days ago that he would heavily invest in DeFi).

In summary, regardless of who ultimately prevails in the upcoming competition, this direct confrontation between BUSD and USDC will undoubtedly shake the entire stablecoin market and reshape the landscape of the entire sector.

It is also worth mentioning USDT. As the biggest winner of the "First Stablecoin War," USDT can still enjoy the fruits of its victory for now. However, in my personal view, USDT is like a "giant clad in armor but standing on a narrow bridge." Its first-mover liquidity advantage is an unmatched moat for USDT, but the lack of transparency in its reserve information remains a hidden landmine—if nothing happens, all is well, but once an issue arises, the consequences could be unimaginable. This is also the biggest variable in the entire stablecoin sector.

Local Battlefield: DAI vs Challengers

In addition to centralized stablecoins like USDT, USDC, and BUSD, decentralized stablecoins operating through smart contracts are also an undeniable force in the sector.

After the U.S. Treasury announced sanctions against Tornado Cash in August this year, Circle quickly froze USDC assets in related addresses, raising concerns in the market about the "arbitrary actions" of centralized stablecoins. In contrast, decentralized stablecoins, due to their permissionless and non-single-point-controlled characteristics, have become the long-term development direction of the stablecoin sector in the minds of many.

Looking at the current landscape of the decentralized stablecoin market, DAI still holds a dominant position. Apart from the collapsed UST, there is currently no challenger that can threaten its status. The partially algorithmic stablecoin FRAX looks decent but still lags behind DAI by a factor of four or five in market size. However, variables that may disrupt this local battlefield are gradually approaching.

In mid-October, Aave announced the development progress of its decentralized over-collateralized stablecoin GHO and stated plans to begin deploying GHO on the testnet in the coming weeks. Earlier, Curve developers had also uploaded the code for their native stablecoin crvUSD to GitHub.

The entry of major players like Aave and Curve means that DAI and MakerDAO are encountering competitors of comparable strength in the decentralized stablecoin market for the first time, especially Curve, which, as the largest stablecoin DEX by transaction volume, has previously been the battleground for various stablecoins. Now that it is entering the fray itself, it may change the competitive landscape of decentralized stablecoins.

Given that GHO and crvUSD have not yet been deployed on the mainnet, this local battlefield has not yet reached "full-scale combat," but the smell of gunpowder is indeed becoming stronger.

Marginal Battlefield: The "Sovereignty" Struggle of Small Ecosystem Stablecoins

In some smaller ecosystems with weaker market attention, there has also been competitive activity surrounding stablecoins. The two sides of the battle are generally one side consisting of native stablecoins supported by ecosystems, such as Kava's USDX and WAVES's USDN, while the other side includes leading stablecoins like USDT and USDC.

However, apart from the former UST, which could dominate its own Terra chain (mentioned for the nth time, as the data back then was indeed impressive), these small ecosystem stablecoins have not yet demonstrated sufficient competitiveness and may even struggle to maintain their peg due to design flaws or past bad debts.

Some small ecosystem stablecoins have reached the end of the road. On October 25, the NEAR Foundation officially recommended gradually shutting down USN, and to fill the bad debt gap of USN, the NEAR Foundation allocated $40 million to ensure sufficient redemptions. Although this is just an extreme case, it reflects the difficult situation of small ecosystem stablecoins to some extent.

The only exception may be USDD, which, under Sun's "bold moves," has not only accumulated over $700 million in issuance but has also become one of the legal tender currencies of the Caribbean nation of Dominica, embarking on an "unforeseen" path.

As the "Second Great Stablecoin War" begins

As the most commonly used medium of exchange in the cryptocurrency world, stablecoins carry massive trading and transfer demands. Supported by astronomical business volumes, the "issuance, circulation, and redemption" of this simple business model has become one of the most "guaranteed" businesses in the market. Whether for commercial entities like Circle or DeFi protocols like MakerDAO, the strong value capture ability of stablecoin businesses cannot be overlooked, which is also the main reason this sector has become a "battleground."

Standing at the onset of the "Second Great Stablecoin War," we can predict that this will inevitably be a long and variable competition. In addition to the dominant leaders sitting on their thrones and the new challengers wielding swords, more new entrants will gradually join the fray, and their respective positions and roles may change unexpectedly. The grand show is about to begin, and we are all witnesses.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles