Understanding Hong Kong's Virtual Asset Regulatory Framework at a Glance

The master's and doctoral team in law provides professional interpretation of the legal regulations and policies regarding virtual assets in Hong Kong.

The master's and doctoral team in law provides professional interpretation of the legal regulations and policies regarding virtual assets in Hong Kong.Original Title: 《Pure Dry Goods | A Comprehensive Understanding of Hong Kong's Virtual Asset Regulatory Norms》

Author: Xiao Za Legal Team

Yesterday, the Financial Secretary of Hong Kong officially released the "Policy Declaration on the Development of Virtual Assets in Hong Kong," which has drawn significant attention from the blockchain community, from mainland China to Singapore, Canada, and Australia. Indeed, this is a major positive development, but we should not merely skim the surface; we must seriously study the real issues. This article will summarize the legal norms and policies regarding virtual asset regulation in Hong Kong, providing insights for our friends in the industry.

We also look forward to everyone choosing the Xiao Za team and the Dentons Hong Kong office for legal services and think tank consulting services.

1. Will Hong Kong's Policies on Virtual Assets Affect the Mainland?

I saw in my social circle that some industry insiders believe that Hong Kong's financialization of virtual assets is just the beginning, and that the mainland will also open up to the financialization of virtual assets in the future. I do not agree with this viewpoint. I believe that Hong Kong and the mainland have a complementary relationship in the development of virtual assets. At the same time, Hong Kong's open attitude towards the financialization of virtual assets will alleviate some concerns from mainland law enforcement agencies regarding advocates of virtual assets and sporadic transactions.

On one hand, the winds are changing in Hong Kong, indicating that our country is quietly laying out a strategic plan regarding the legal stance on virtual assets. The financial innovation of virtual assets, their entry into Web 3.0, and the metaverse represent significant opportunities for the future. As an international financial center, Hong Kong will undoubtedly position itself as a bridge for the financialization and innovation of virtual assets between the mainland and overseas. This will attract more projects, personnel, and assets to Hong Kong for innovative attempts. There is no doubt that this news is a major positive development. Friends currently in Singapore are still observing, but we believe that in the future, the gradual relaxation of virtual asset licenses in Hong Kong, particularly the increase in Type 1 and Type 9 licenses, will stimulate more of the "evangelists" from back in the day to return from abroad and "nest" in Hong Kong to develop virtual asset businesses.

On the other hand, the mainland will still approach the legal nature of virtual assets with caution. Firstly, we can confirm that the mainland will not classify mainstream virtual currencies like Bitcoin as "prohibited items." Holding mainstream virtual currencies like Bitcoin will still be protected under Article 127 of the Civil Code. Secondly, the use of consortium and private blockchains based on distributed ledger technology will continue to deepen in areas such as shipping, supply chain finance, power transmission transactions, and bank reconciliation, gradually iterating and upgrading. Thirdly, ICO activities based on public chains will still be classified as "illegal financing," with compliance points being that there are no domestic jurisdictional connections (specific details can be found in many previous articles on Xiao Za's public account). Finally, the compliance of NFTs and Web 3.0 is relatively high in both the mainland and Hong Kong, with particular attention needed on anti-money laundering risks and financialization issues.

As for the "digital Hong Kong dollar," we also welcome it. Similarly, the digital renminbi is gradually being accepted by consumers in online shopping. This year's Double Eleven shopping festival saw large e-commerce platforms launching interesting activities to promote the application scenarios of digital renminbi and encourage its use.

The "green bond tokens" allow the Hong Kong government to tokenize green bond issuances for institutional investors to subscribe. The logic behind this attempt is profound, and we look forward to more institutional investors recognizing the value of green bond tokens, contributing to Hong Kong's development and also benefiting the economic development of the mainland.

2. Overview of Hong Kong's Blockchain Industry Regulatory Framework

Currently, there are three main regulatory bodies for virtual assets in Hong Kong: (1) the Securities and Futures Commission (SFC); (2) the Financial Services and the Treasury Bureau (FSTB); and (3) the Hong Kong Monetary Authority (HKMA). Among them, the SFC is the main regulatory body, dividing virtual assets into regulated "securities financialization assets" and unregulated "non-securities financialization assets," while the FSTB and HKMA assist in regulation from different perspectives (with the FSTB as the second regulatory body primarily focused on combating money laundering and terrorist financing activities related to virtual assets). Under the planning of these three regulatory bodies, the licensed regulatory system for virtual assets in Hong Kong is gradually becoming clear. Of course, referring to the U.S. "Responsible Financial Innovation Act" classification of NFTs and other virtual digital artworks, it is not ruled out that in the future, Hong Kong's market supervision and management agencies may join the regulatory ranks and introduce specific regulatory norms for "non-financial securitized" virtual assets (pure digital artworks).

The regulation of virtual assets in Hong Kong can be roughly divided into two phases:

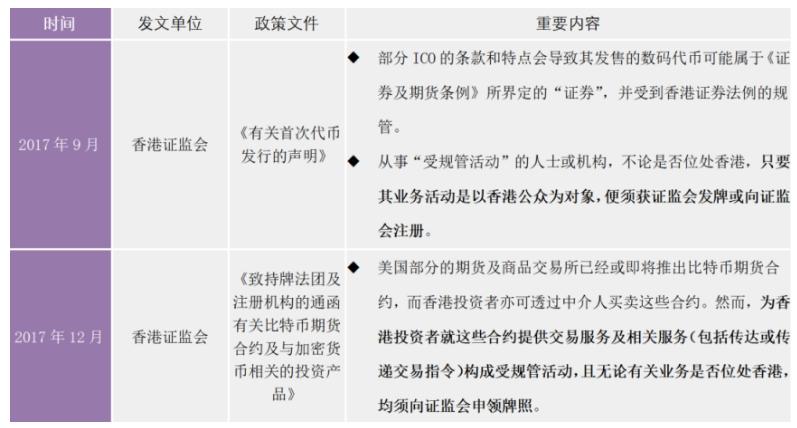

Phase One: 2017 - 2018, centered on regulating ICO activities. The regulatory approach during this period was to regulate virtual asset activities with financial attributes by comparing them to traditional securities financial products, primarily led by the SFC to standardize ICO activities.

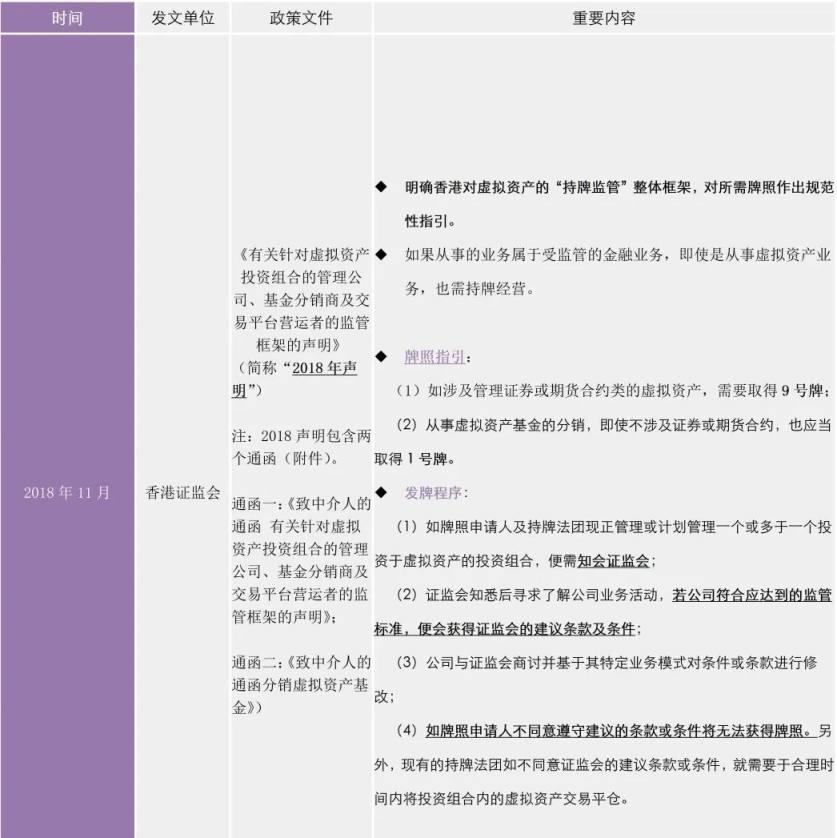

Phase Two: From the end of 2018 to the present. This period is marked by the SFC's "2018 Statement" issued in November 2018, which signifies a shift in Hong Kong's regulatory approach towards virtual assets, expanding the focus from ICOs to the regulation of all virtual asset activities, gradually establishing a "sandbox-style licensing regulatory" framework, which is still being refined through various normative documents. Below, we will detail Hong Kong's virtual asset regulatory system and implementation details through charts.

Phase One

During this period, in March 2018, a significant ICO event occurred when a group conducted a public ICO issuance activity in Hong Kong, which was deemed by the SFC as an "unrecognized promotional activity and unlicensed regulated activity." The ICO was ultimately halted by the SFC, which ordered the group to return its tokens to Hong Kong investors and canceled subsequent related ICO transactions.

Phase Two

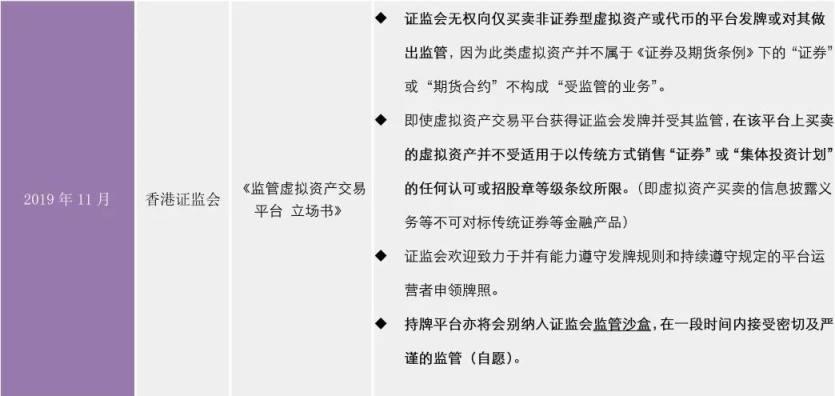

Currently, the licensing regulatory practice in Hong Kong is relatively cautious, with only two virtual asset trading platforms successfully obtaining trading licenses: one was issued in 2020 to a member company of a certain technology group, OSL (Digital Securities Limited, OSL DS); the other obtained a license in the first half of this year, Hashkey Group. Publicly available information shows that OSL holds a Type 1 license (securities trading) and a Type 7 license (automated sales).

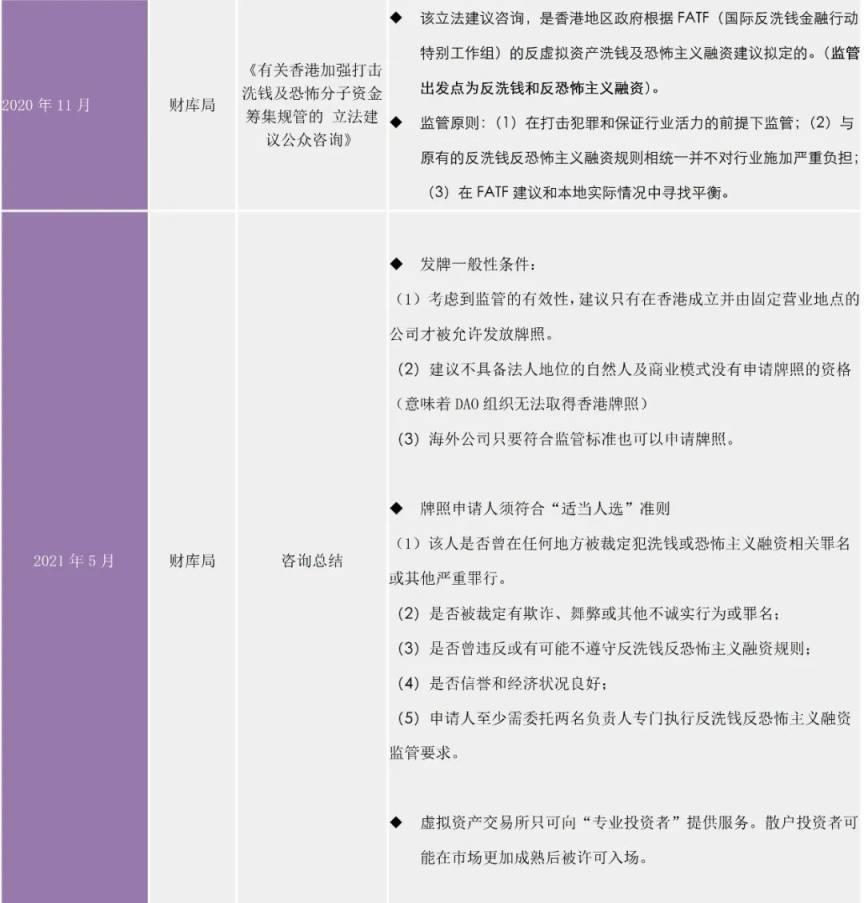

It is important to note that according to the FSTB's "Consultation Summary," although both platforms have obtained licenses, the investors allowed to trade can only be professional investors in Hong Kong. The requirements for professional investors in Hong Kong are: (1) individual investors must have financial assets (cash, stocks, etc.) reaching HKD 8 million or USD 1 million; (2) institutional investors must reach HKD 40 million or USD 5 million. Additionally, exchanges must fulfill KYC obligations and conduct investor risk assessments to ensure clients have sufficient net assets to bear risks and trading losses.

The Xiao Za team believes that depending on the specific types of business of the platforms, virtual asset trading platforms may need to consider obtaining a Type 4 license (providing advice on securities) and the Type 9 license mentioned in the SFC's 2018 statement (managing virtual assets related to securities or futures contracts) for compliant operations. This is merely one opinion for reference. Furthermore, it is a general trend for all virtual asset trading platforms to operate under a regulatory framework and licensing system in Hong Kong. According to the FSTB's normative documents and relevant securities laws in Hong Kong, any person engaging in regulated virtual asset activities without a license may be suspected of committing a criminal offense, with a maximum penalty of 7 years imprisonment and a fine of HKD 5 million.

3. Complementarity of Blockchain Industry Segments Between Hong Kong and the Mainland

Regarding the regulation of virtual currencies, the mainland issued the "Announcement on Preventing Risks of Token Issuance Financing" in 2017, which is known as the announcement by the three associations. This announcement clearly defined token issuance financing as an unauthorized illegal public financing activity, linking it to illegal issuance of token vouchers, illegal issuance of securities, illegal fundraising, financial fraud, and pyramid schemes, and explicitly prohibited any organization or individual from engaging in illegal token issuance financing activities, effectively cutting off the path for token financing in the mainland.

In this regard, Hong Kong's attitude is to allow ICOs (with Hong Kong categorizing securities token issuance as STO), but they must be subject to rigorous licensed regulation, as these virtual assets inherently possess financial attributes that constitute "regulated financial products." In 2017, the Hong Kong SFC issued the "Statement on Initial Coin Offerings," which stated that the following three scenarios would be recognized as securitized ICOs and require special regulation: if the tokens being offered represent equity or ownership interests in a company, if the tokens are used to establish or confirm debts or obligations borrowed by the issuer, or if the proceeds from the token sale are collectively managed and invested in different projects by the ICO program operator, allowing token holders to share in the returns provided by those projects.

As for NFTs, the mainland's regulation is still relatively broad, primarily warning investors and consumers about potential fraud and gambling risks associated with NFTs. In April 2022, the mainland released the "Initiative on Preventing Financial Risks Related to NFTs" by the China Internet Finance Association, the China Banking Association, and the China Securities Association. From this initiative, it can be seen that the mainland is cutting off NFTs from financial activities, clearly stating the need to curb the financialization and securitization tendencies of NFTs and prevent their financialization. The policy tone regarding NFTs is to affirm their significance in promoting digital cultural creativity in the real economy and to firmly distance them from financialization.

In this regard, Hong Kong's regulation has made more detailed distinctions, recognizing the existence of financialized NFTs and actively dividing them into collectible NFTs and financial asset NFTs. For collectible NFTs, their activities are completely outside the regulatory scope of the SFC. However, for financial NFTs, their promotion and distribution must be regulated by the SFC, and they can only be conducted after obtaining a license. Readers may wonder where the boundary lies between the two. The Hong Kong SFC points out that if an NFT constitutes a security or has a structure similar to collective investment rights, it is defined as a financialized NFT that requires licensed issuance.

According to the Hong Kong Securities and Futures Ordinance, the definition of a security is "any shares, stock, debentures, bonds, funds, or notes issued by any body (whether or not incorporated) or by any government or municipal authority." This definition sounds somewhat broad, and collective investment rights are also included under securities. Under this definition, collective investment schemes are defined as containing four elements: "they must involve arrangements concerning property; participants have no day-to-day control over the management of the property involved; the property as a whole is managed by the person operating the arrangements or by someone on their behalf, or the contributions of participants and the profits or returns paid to them are pooled; and the purpose or function of the arrangements is to enable participants to share or receive profits, returns, or other benefits derived from the property." Those meeting the above conditions will be defined as financialized NFTs subject to licensing regulation.

Overall, if it is merely about NFT art collectibles, both the mainland and Hong Kong can accommodate this, but the mainland has a larger potential market and richer IP resources. However, if one aims for NFT financialization, there are significant legal risks in the mainland, and it may be worth considering obtaining a license in Hong Kong.

At the underlying technology level of blockchain, we know that China and the United States have chosen completely different directions in this field. China has opted for the metaverse and hardware empowerment, while the United States has chosen web 3.0 and software creation. This divergence in direction also determines policy; the mainland's development policies for the underlying technology of blockchain are relatively friendly. In 2020, the Ministry of Education issued the "Action Plan for Blockchain Technology Innovation in Higher Education Institutions," aiming to establish a number of blockchain technology innovation bases in universities by 2025 and cultivate teams focused on blockchain technology.

Following this document, notifications were issued regarding various specific directions for blockchain applications, including the "Guiding Opinions on Accelerating the Application and Industrial Development of Blockchain Technology" by the Ministry of Industry and Information Technology and the Central Cyberspace Affairs Commission, and the "Guidelines for the Construction of an Import Container Electronic Release Platform Based on Blockchain" by the Ministry of Transport. Even in May 2022, the Supreme People's Court issued "Opinions on Strengthening the Judicial Application of Blockchain," affirming the application prospects of blockchain evidence technology in the judicial field. In this regard, Hong Kong has not provided many encouraging regulations.

From a policy perspective, the mainland encourages the development of virtual technologies that are more closely linked to the real economy, including empowering the real economy through NFTs and promoting the underlying blockchain technology for real development; conversely, Hong Kong has more lenient conditions in terms of the financialization of virtual assets.

Final Thoughts

The differing policies between Hong Kong and the mainland lead to different future development directions and completely different roles. The mainland will continue to provide financial tools, digital art IP, technical tools, etc., to support Hong Kong in becoming a world-leading core area for the virtual asset economy. Meanwhile, Hong Kong will bear the significant responsibility for the development of China's virtual economy, concentrating resources to build a regulated, rapidly developing, competitively healthy, and open virtual economic center. The Xiao Za team will continue to monitor the virtual asset regulatory policies in Hong Kong and provide timely professional regulatory interpretations for everyone.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles