Data Analysis: What is the Impact of the FTX Collapse on the Cryptocurrency Market?

Rebuilding lost trust will be the most difficult challenge for the cryptocurrency industry at present.

Rebuilding lost trust will be the most difficult challenge for the cryptocurrency industry at present.Written by: Clara Medalie, Riyad Carey, and the Kaiko research team

Compiled by: Block unicorn

First came the collapse of Terra, then the bankruptcy of centralized crypto lending institutions, and now, one of the world's largest cryptocurrency exchanges, FTX, has (almost certainly) gone bankrupt.

The collapse of FTX has shaken the confidence of the entire industry, partly because its business model is fundamentally different from that of cryptocurrency lending institutions like Celsius. FTX is a cryptocurrency exchange that facilitates trading for traders: they earn trading fees on every transaction they execute for customers. FTX is neither a trading firm nor a lender, so theoretically, they should have access to 100% of customer assets at all times.

But we now know that this is not the case due to the dangerous interconnections with FTX's sister company, Alameda Research, and the improper use of FTX's native cryptocurrency, FTT.

After a massive outflow of funds, FTX halted withdrawals, and shortly thereafter, SBF (the founder and CEO of FTX) announced a "strategic transaction" with competitor Binance to ensure that "customers are protected." Binance then stated that it would not proceed with the transaction (some reports indicated that FTX US had to be included for Binance to consider the deal) and said, "These issues are beyond our control or ability to help." Reports indicated that SBF informed investors on Wednesday that FTX would need to file for bankruptcy, with a shortfall of up to $8 billion.

Ironically, FTX had extended over $750 million in credit to struggling crypto companies, which ultimately went bankrupt due to the misappropriation of customer funds. While we still do not know the extent of the balance sheet holes or whether a buyout will materialize, the cryptocurrency industry has just undergone a historic restructuring.

FTT: A Cursed Hybrid

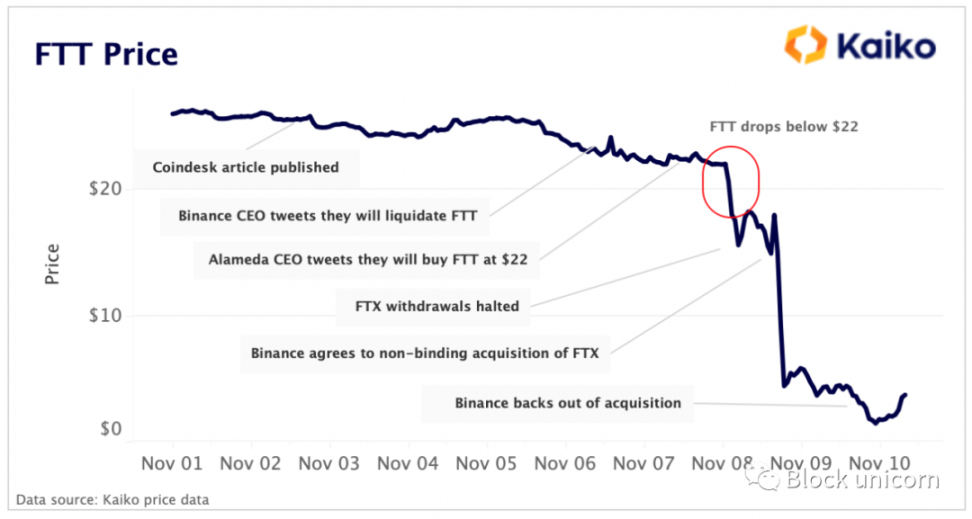

The rapid bankruptcy of one of the world's largest exchanges began with a CoinDesk investigative report, which stated that a significant portion of Alameda's balance sheet was in FTT, a cryptocurrency created by FTX. This immediately raised questions about the purpose of financial trading laws: what is the actual purpose of financial trading laws?

Cryptocurrency exchanges have long issued their own tokens, which typically offer little benefit beyond providing holders with trading fee discounts, and have rarely been scrutinized. As stated in FTX's FAQ section, here are the utilities of FTT:

What does FTT do? FTT will be a pillar of the growing FTX ecosystem:

FTT tokens will be listed on FTX.

FTX will use one-third of trading fees to continuously buy back FTT tokens and burn them.

FTT will be usable as collateral on FTX.

FTT will receive socialized profits from FTX's supportive liquidity fund.

Burning mechanism: Continuously buy back FTT tokens to burn until half of the total supply of FTT tokens is destroyed.

The more we learn about FTT, the more we feel that this packaged cryptocurrency supports a significant portion of the FTX/Alameda empire. The utility of this token is extremely limited, but it is widely used as collateral: in DeFi, within FTX, and on Alameda's books.

CoinDesk's investigation revealed that Alameda not only had a large amount of FTT on its balance sheet but had also been using FTT as collateral for loans. This alone should have raised alarms, but the bigger question is: who accepted billions of dollars worth of FTT as collateral? New reports indicate that the problematic lender was none other than FTX, which we can infer through some on-chain investigative work.

Alameda and most other cryptocurrency hedge funds suffered massive losses during the market crash in May, and FTX attempted to use its own funds to acquire FTT as collateral to cover these losses. Most likely, some of this capital belonged to their customers.

The information on Alameda's balance sheet was enough for Binance CEO Changpeng Zhao ("CZ") to announce that Binance would liquidate all of its FTT holdings (which were acquired as part of exiting its stake in FTX), which were then valued at around $500 million. From that point on, things began to unravel.

Illiquid Tokens

FTT is a relatively illiquid token, actively traded on only 10 exchanges with a total of 23 spot markets. In comparison, BTC has ~370 spot trading markets, SOL has ~80 spot trading markets, and DOGE (the meme token) has over 130 spot trading markets (for more information on FTT's liquidity issues, you can check previous articles from Block unicorn by clicking here).

Following CZ's tweet, Alameda CEO Caroline Ellison tweeted that her company would buy all FTT from Binance at $22. If the solvency of the Alameda/FTX empire depended on FTT, maintaining its price might be the top priority.

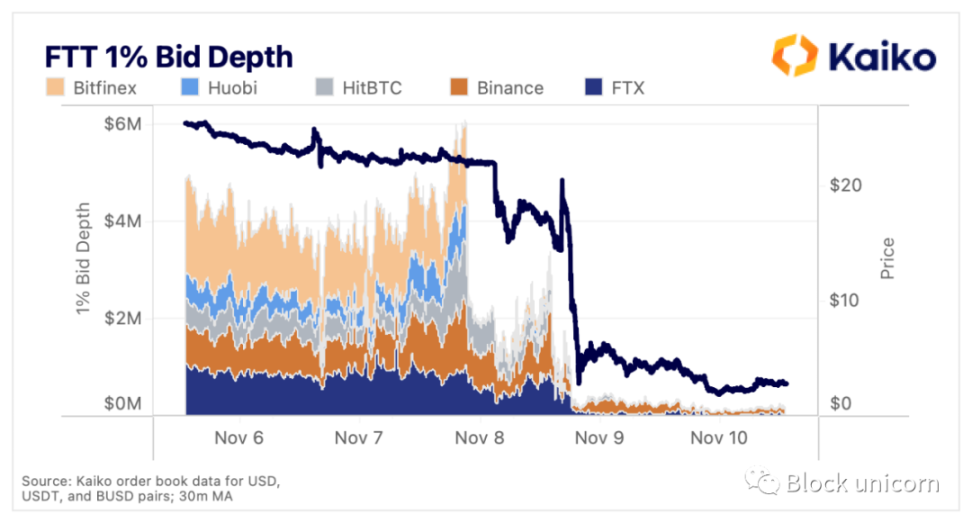

It is unclear whether these off-market discussions made any progress, but at 9:15 PM UTC on November 7, FTT's liquidity quickly withdrew from the order book. Bitfinex's 1% bid depth dropped from nearly $2 million to below $250, while Huobi's bid depth fell from $1.5 million to below $3,000 within minutes. The depth on Binance and FTX remained unchanged during the same time period, suggesting that a non-Alameda market maker decided to exit the Bitfinex and Huobi markets, perhaps after hearing news of a breakdown in over-the-counter negotiations between Binance and FTX.

Alameda likely accounted for the vast majority of FTT market-making activity, which explains why FTT's price only plummeted days later after selling pressure had already begun. At this point, before the collapse, market depth had sharply increased, indicating the presence of buy orders (if the market loses confidence in a particular asset, buy orders can plummet). However, the sudden collapse of liquidity did raise a question: if the company's future depended on maintaining its price, why didn't Alameda take more measures to support the bid for FTT?

Five hours after the liquidity collapse, FTT's price fell below $22. As FTT rebounded in the $15-$17 range, liquidity seemed to improve, but it disappeared again before the announcement of FTX's acquisition by Binance. Upon the news, FTT's price surged, but quickly fell below $3. Since then, FTT's 1% buy-side depth across all markets has hovered around $200,000, and it remains unclear who is still making markets.

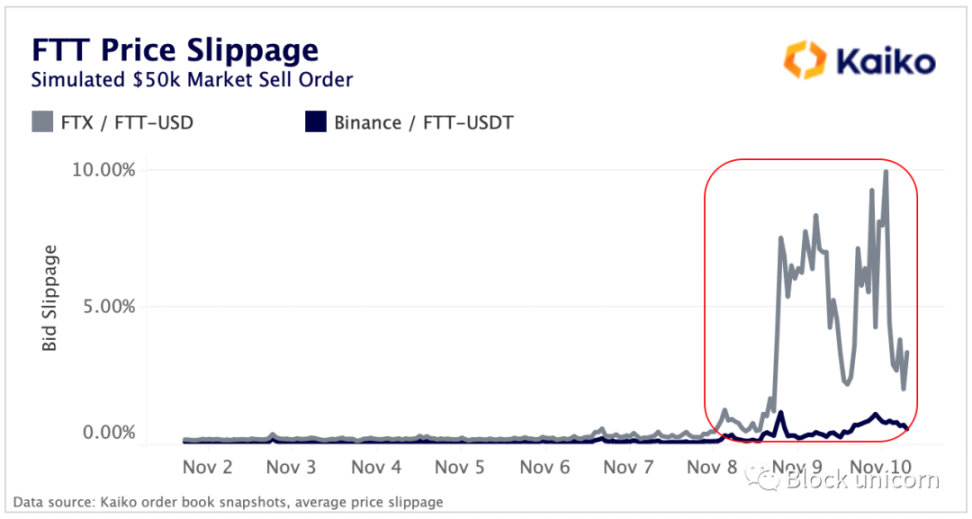

By observing the price decline, we can see how quickly FTT's liquidity collapsed. By simulating a $50,000 market sell order, the declines in the two most liquid FTT pairs listed on Binance and FTX sharply increased. By Wednesday, a $50,000 sell order on FTX would lead to a significant 8% drop in FTT's price (here's a reminder to investors that market cap does not equate to liquidity; in illiquid conditions, a market cap of $10 billion is merely a mirage).

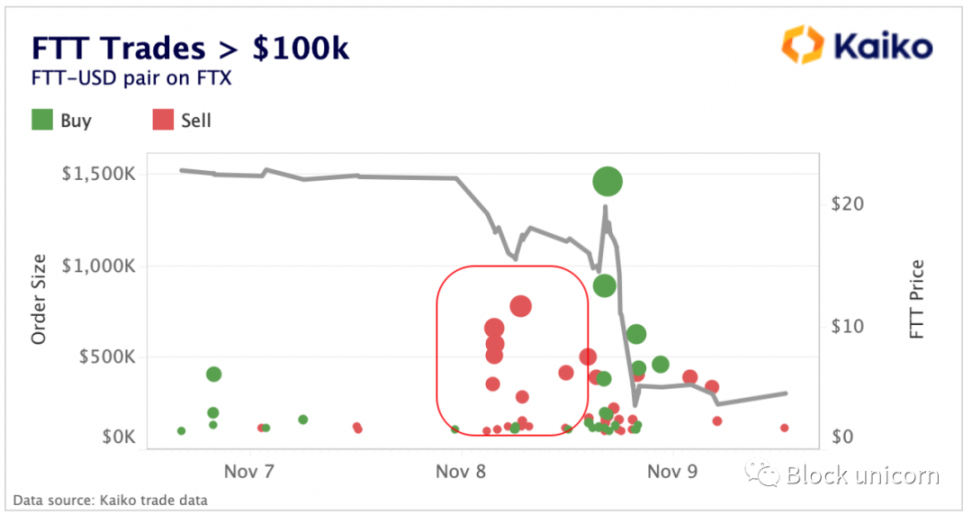

As prices fell, a large number of market sell orders flooded in. Further disclosures regarding Multicoin Capital's exposure to FTT indicated that as FTT dropped below $22, industry participants were rapidly closing their FTT positions. Typically, traders would split their orders into smaller parts to avoid slippage, but in desperate times, firms will accept any price they can get, with many orders exceeding $100,000.

As news of Binance's potential acquisition spread, FTT experienced a brief surge, with several very large market buy orders, possibly from Alameda attempting to push up the price, but the market quickly repriced the seriousness of this move.

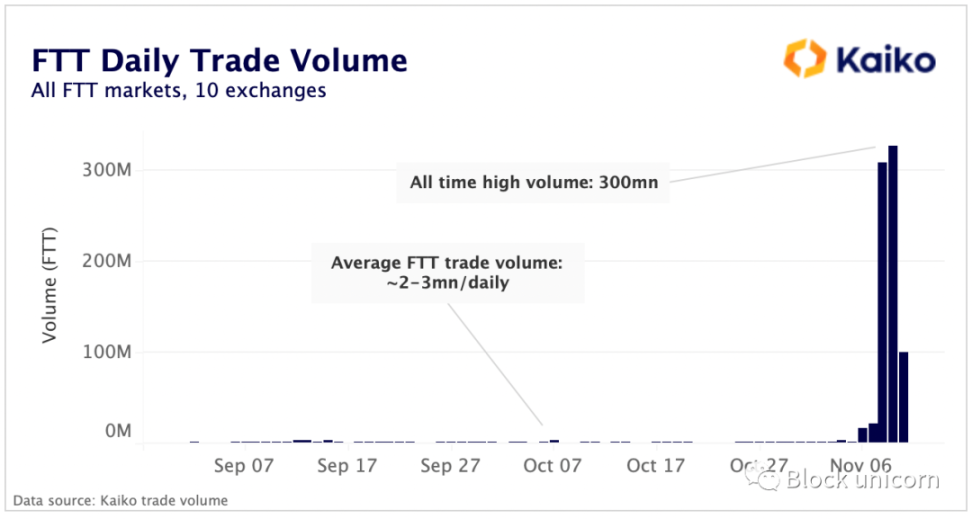

By the end of Tuesday, FTT's trading volume had surged to an all-time high, with daily trading volume reaching 300 million FTT. On Wednesday, Binance warned all traders to stop buying and selling FTT due to extreme risks, after which trading volume stabilized.

FTT is now virtually worthless; it is the token of an exchange with a balance sheet hole of billions of dollars. The token has dropped nearly 90% in the past week and is currently trading below $3, with a fully diluted valuation just above $1 billion.

Unfortunately, due to the importance of FTX and the intricate investment network supported by Alameda Research using the FTT token, the damage from this market collapse has spread very widely.

The ripple effects of FTX/Alameda will take months to fully manifest, and the sheer number of them cannot be fully covered in a single article. But let's start with FTX itself and then expand to Alameda and the broader impacts.

Purgatory for FTX

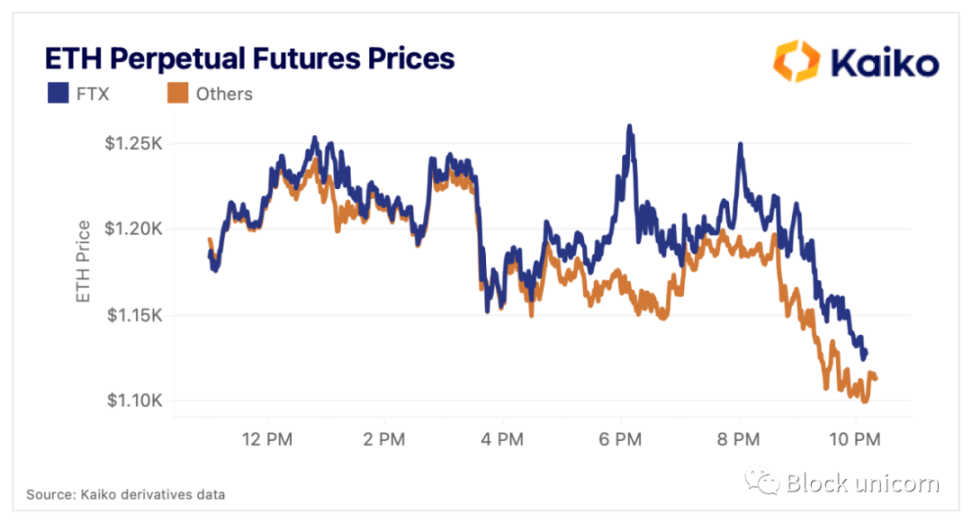

FTX is now in purgatory, with all funds on the exchange effectively turned into Monopoly money or legitimate claims, depending on your time frame. Market makers and investing users are trapped on the exchange, isolated from other markets, and can only develop their own biosphere, as evidenced by the price of ETH perpetual contracts on FTX, which began to diverge from ETH prices on other exchanges on November 9.

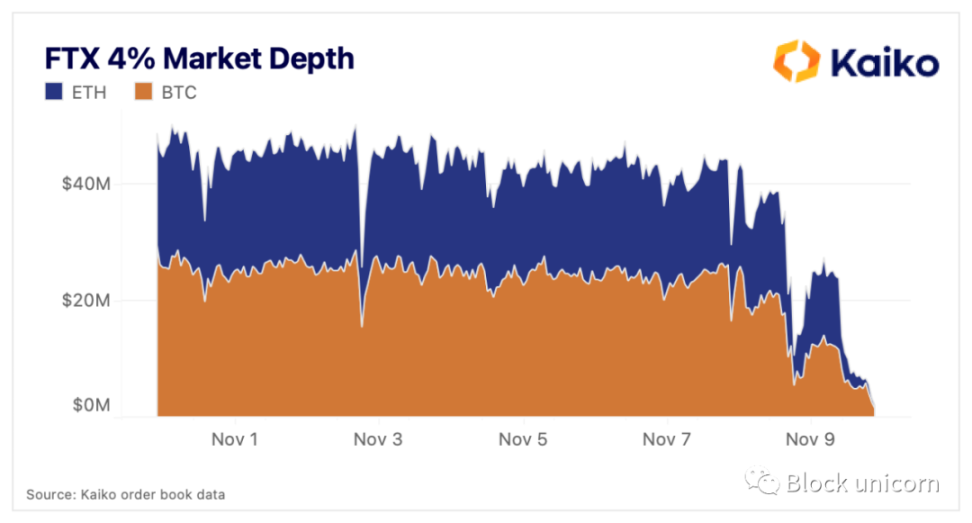

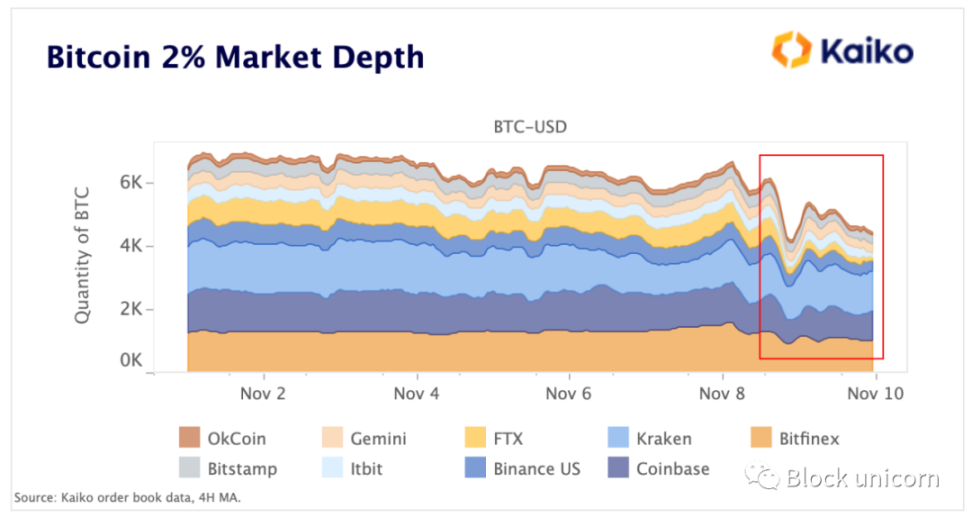

The liquidity of the exchange has evaporated, which is understandable. The market depth for BTC dropped from $25 million to below $2 million; ETH fell from $17 million to below $750,000.

We have reason to expect that the FTX market will continue to become more alien, and the longer users are trapped, the less connection they will have to reality.

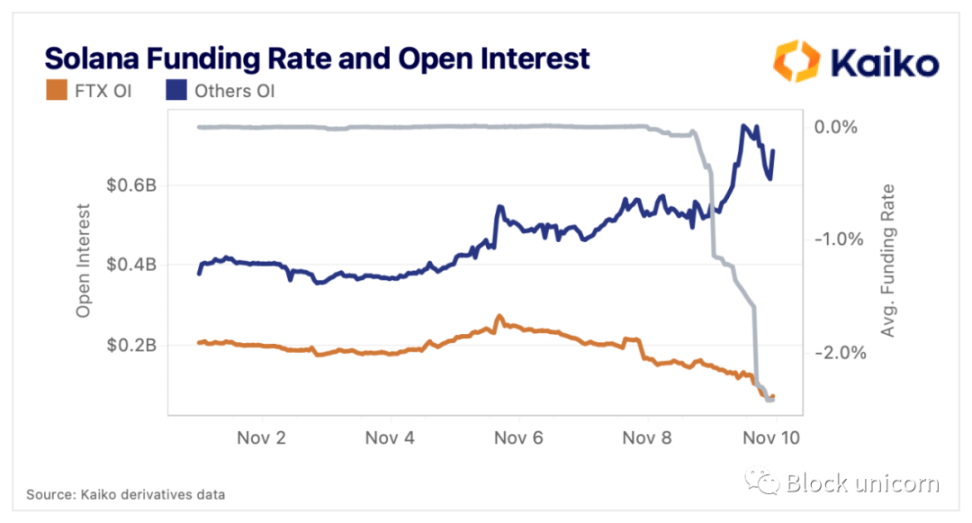

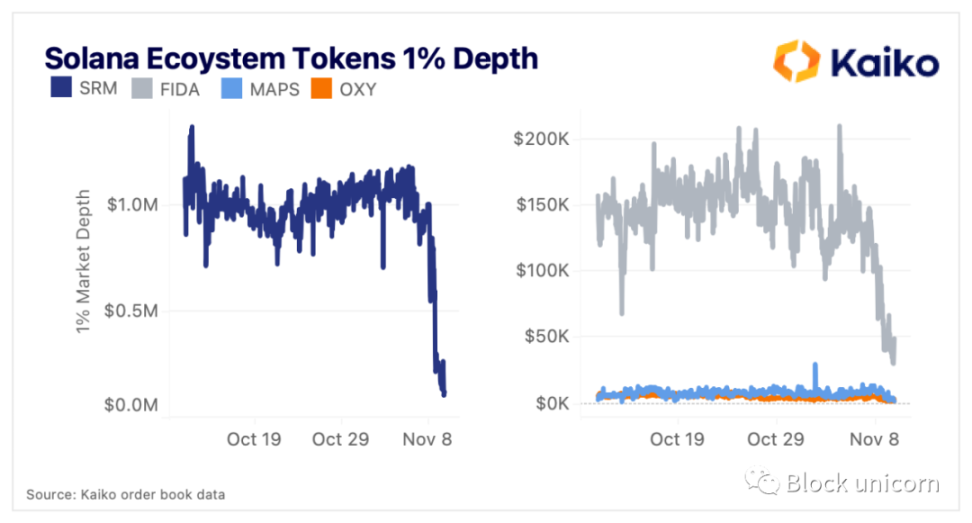

Next, let's talk about Alameda, which holds a large amount of SOL and Solana ecosystem tokens. FTX was also an early supporter of this project, and SBF often praised the network. The price of SOL plummeted during the collapse, and the open contracts on FTX tended toward zero. Open contracts on other exchanges surged, coupled with a sharp decline in financing rates, indicating a significant amount of short selling.

Alameda has long been involved in the Solana ecosystem and has built a reputation for investing in projects with large fully diluted valuations and small market caps, allowing them to profit when early retail investors were crushed. Many of these tokens have dropped over 90% from their historical highs (for OXY, the token's market cap peaked immediately after the token was issued). However, Alameda still holds these tokens, even though their liquidity later became very poor, and the company was unable to sell all the tokens before they went to zero.

While this is a dark moment for Solana and its ecosystem, the network will face a test as one of its most important (and predatory) supporters has now declined (FTX or SBF). Ethereum and Bitcoin have gone through similar—possibly even more difficult—trials and emerged stronger. If SOL can survive this calamity, it may develop better in the future.

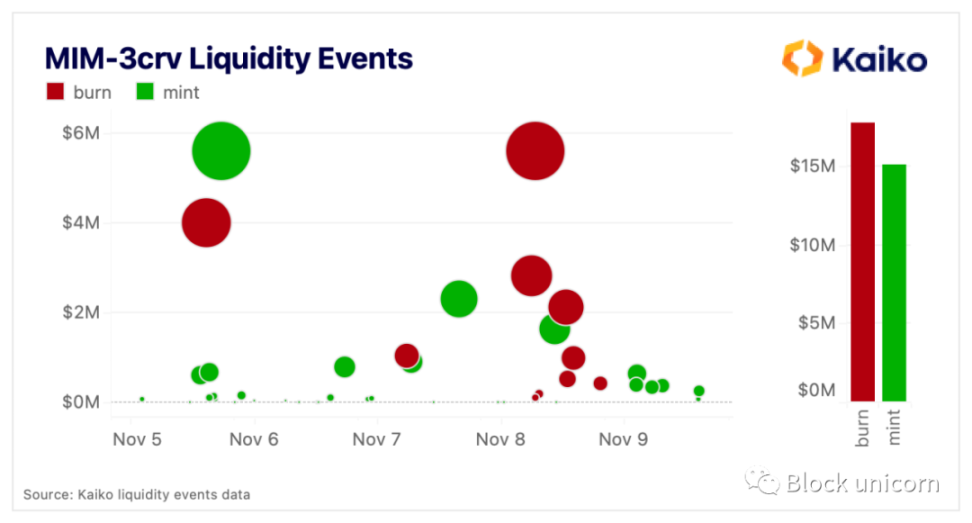

This impact has also spread to Ethereum. People quickly realized that FTT was a major support for the collateralized stablecoin MIM. On-chain investigations showed that most of this was Alameda's position, and when FTT reached $6, it would be liquidated. Upon this news, MIM's peg began to wobble, although the team quickly announced that it was working with Alameda to reduce their loan size. Subsequently, MIM returned to a stable peg and did not see significant capital outflows from its CRV pool, with the amount of MIM burned in the past few days only slightly exceeding the amount minted.

On the other hand, the Lido Staked Ether (stETH) CRV pool experienced massive outflows in the past three days, with over $600 million in net outflows. The stETH discount has also reappeared, currently around 2%. While some speculate that Alameda holds a significant stETH position that needs to be liquidated, the exact reasons for this liquidity elimination and the reappearance of the discount are still not entirely clear.

This is just one example of the countless ways this collapse has shaken the market, including centralized and decentralized exchanges, and the full consequences of SBF's arrogance will not be fully understood for months.

Giants Get Bigger

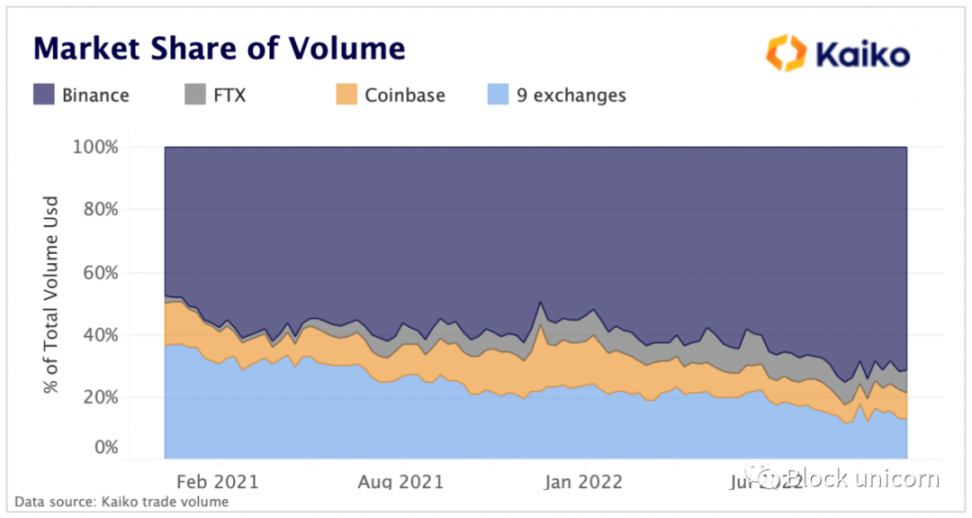

While the acquisition seems to have completely fallen through, what would a Binance+FTX behemoth look like? Since 2021, Binance's market trading volume share has climbed from 47% to 71% relative to the 11 most liquid exchanges, with its total trading volume larger than the sum of all other exchanges.

While FTX's trading volume was only a small portion of Binance's, the exchange experienced significant growth at the expense of other exchanges. During the same period, FTX's market share rose from 2.5% to 7.5%, making it Binance's second strongest competitor after Coinbase.

(The other 9 exchanges include FTX.US--0.8%-- and Binance.US--1.7%--, so if these U.S. entities are considered, the total market share is even larger.)

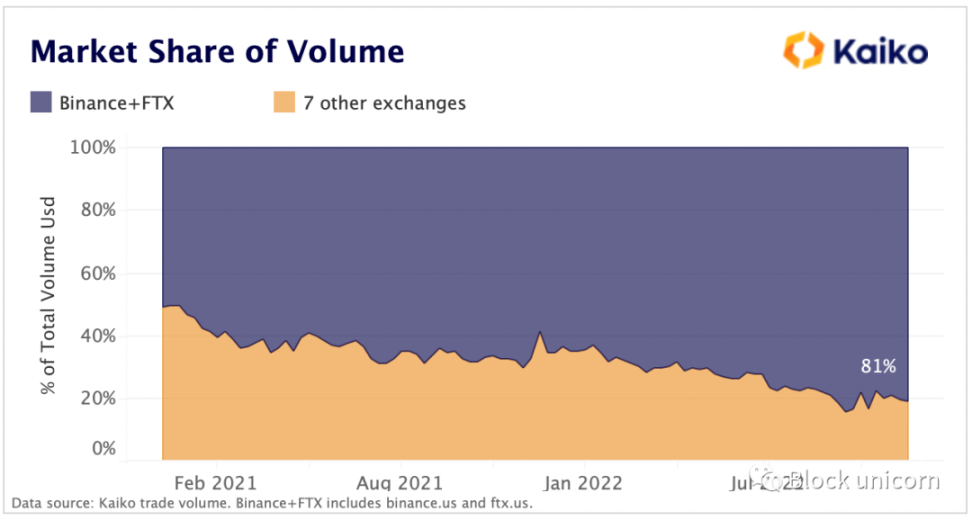

Now let's look at the market share post-acquisition, or more likely post-bankruptcy. Assuming Binance claims any former traders using FTX.US, then these traders' market share would increase.

Combining Binance.US and FTX US into a new Binance behemoth, the exchange would claim over 80% of the total market share. In either case—acquisition or bankruptcy—Binance's market share will almost certainly surge.

Loss of Alameda's Liquidity

Alameda is one of the largest market makers in the cryptocurrency industry, with others including Wintermute, B2C2, Genesis, and Cumberland. While it is impossible to know how much they contribute to overall market liquidity, their balance sheets clearly indicate that the company is a systemically important market maker.

Alameda's bankruptcy may have already impacted liquidity, as the number of bitcoins on BTC-USD orders across all markets has dropped from about 6,000 to 4,000 in the past two days.

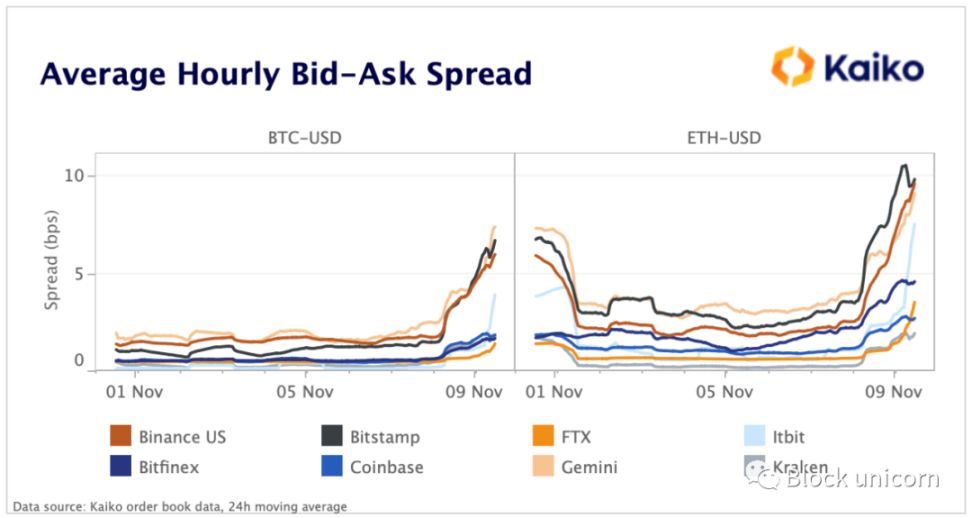

The price spreads for BTC and ETH on every exchange are at annual highs, indicating that all market makers are extremely sensitive to price during extreme volatility.

What to Do Now?

Earlier this month, SBF faced fierce criticism for proposing regulation of DeFi protocol front ends. Regulators should focus directly on centralized entities that engage in severe mismanagement of risk at the expense of customer interests, rather than on DeFi.

A three-pronged approach to regulating centralized entities in cryptocurrency should include the following:

Proof of reserves for exchanges and centralized lenders to demonstrate they can at least match deposits 1:1.

Separation between a company's trading/startup department and their exchange business.

Disclosure of significant positions held by these trading departments that could lead to contagion across the market, similar to Alameda's disclosures regarding FTT.

But even if all three are implemented, there are still two major issues: (1) proof of reserves does not show liabilities; and (2) regulatory arbitrage. There is no way to guarantee that institutions will act honestly, even if they broadcast their assets on the blockchain. There will always be some jurisdictions that allow companies to play fast and loose; this is why SBF was able to simultaneously deliver bad news to investors in the Bahamas. (Although people in the cryptocurrency space painfully acknowledge that U.S. regulations did indeed protect customers in this case, as FTX.US could continue processing withdrawals).

These two issues are very difficult to solve, but what does not face these two issues? DeFi can operate without facing these two difficult problems. This collapse, caused by a complex and opaque network filled with deception and greed, is the greatest advertisement for DeFi in history.

Now the question naturally turns to Binance: how much risk does Binance have with BNB, and what would happen if it dropped to $0? Did Binance misappropriate customer assets for investment, and could they match withdrawals 1:1 in the event of a similar bank run? Hopefully, Binance will do everything it can to establish transparent and solid financial conditions to avoid this type of bank run.

The collapse of FTX is a brutal blow to the industry, and we empathize with all the injured consumer investors. FTX's 7% market share will be replaced, but rebuilding lost trust will be the industry's most challenging task at present. However, we believe that the industry will recover. Ultimately, cryptocurrency has repeatedly proven its resilience, thanks to countless builders and innovators dedicated to creating a decentralized and transparent financial future.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles