Former Spartan Group Partner Writes Long Article: The Truth About Everything Related to FTX

"SBF has a strong gambling nature, and every major decision he makes is related to using more leverage."

"SBF has a strong gambling nature, and every major decision he makes is related to using more leverage."Source: Twitter, Original Author: Jason Choi

Compiled by: Moni, Odaily Planet Daily

In response to a "whitewashing article" about SBF published by The New York Times today, former Spartan Group partner and veteran crypto practitioner Jason Choi shared everything he knows as a firsthand witness through dozens of tweets on social media. He expressed his inability to accept The New York Times' distorted reporting, stating that he knew SBF before the birth of FTX and witnessed the rise and fall of FTX, thus hoping to tell everyone what really happened.

This article is translated and organized by Odaily Planet Daily:

In short, the story of Alameda and FTX can be summed up in one sentence: SBF has a strong gambling nature. In fact, every major decision they made was related to using more leverage—deceptive fundraising, financial engineering, and ultimately outright fraud.

From November 2018 to January 2019, the then-small hedge fund Alameda Research began raising funds from investors, promising "risk-free high returns." It is speculated (to my knowledge) that they had $5 million in equity but attempted to borrow $200 million at a 15% annual interest rate to engage in future market making.

July 2019 was the planned launch time for FTX, and they announced the completion of an $8 million seed round in August 2019, with several funds participating. (Editor’s note: This round was participated by Proof of Capital, Consensus Lab, FBG, Galois Capital, etc.) In an investor memo, "Alameda & FTX" was marked as risky because SBF had to manage both companies simultaneously. Sources told me that FTX was launched because Alameda was having difficulty raising funds at that time, so FTX might have just been a "by-product" to facilitate Alameda's fundraising.

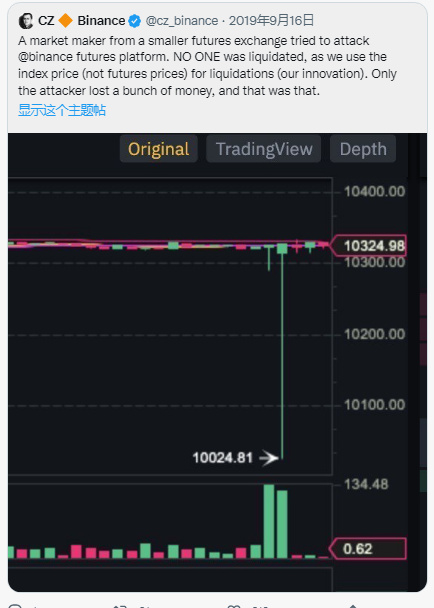

In the early days, Alameda had a dedicated API key for FTX, allowing them to access trades faster than other users, which was almost an "open secret." Around September 2019, Alameda allegedly attempted to attack the Binance futures platform but suffered a setback, which may have marked the beginning of the discord between Binance and FTX.

As FTX continued to grow, their appetite for capital became larger. During the "DeFi boom," they created a decentralized trading platform called Serum on the Solana chain. Subsequently, FTX began participating in multiple Serum/Solana ecosystem projects, such as FIDA, MAPS, Oxygen Protocol, etc., all of which launched tokens in a short period.

According to sources, the operations of Serum were actually run by FTX employees. Some Serum ecosystem projects, although publicly promoted as third-party projects, were in fact internally incubated/operated.

Why did FTX do this? In fact, at that time (winter 2020), some changes were happening internally at Alameda/FTX. Alameda abandoned its delta-neutral strategy because their advantages were eroded and had to start expanding risk exposure under significant leverage. Token assets like Serum were likely used as collateral to achieve the aforementioned leverage, and the trading volume and prices could easily be manipulated by Alameda and FTX to fill their balance sheets.

For example—suppose Alameda funds a semi-incubated project with $2 million at a "fully diluted valuation" of $10 million (token price * total number of tokens to be issued). FTX then lists the token on its exchange but only puts 1% of the total tokens on the market. Alameda could support the price with a few million dollars to create a "fake" fully diluted valuation, such as $1 billion. Suddenly, $2 million becomes $200 million on paper.

By doing this, Alameda created the illusion of a large and diversified balance sheet, which they could then borrow against to fund their "targeted bets." In fact, some people had already noticed this issue at the time but were bullied and threatened, and SBF himself remained silent about it.

In summary, as shown by the leaked FTX balance sheet, Alameda quickly created hundreds of millions of dollars in false liquidity and equity value, but even so, it was dwarfed by FTT.

Serum and FTT were possibly the only two tokens that could be used as collateral on FTX, which likely caused Alameda/FTX to create a multi-billion dollar hole: Alameda promised to borrow money using illiquid collateral to finance, and as the market fell this year, those deposits were called back, leading to FTX user funds being stolen (or used to put out fires).

This meant that FTX's liquid reserves might be lower than user deposits. Of course, if given enough time, this hole might have been controllable, but CZ revealed this fact, which triggered a run on FTX.

As all this brewed behind the scenes, SBF was actively pushing for mainstream legitimacy and building a regulatory moat… ensuring that FTX and FTT equity value could be treated differently. In the process, SBF had to ramp up promotional efforts, which is why we saw FTX announcing a $135 million naming rights deal for the NBA Miami Heat arena, SBF becoming the second-largest donor to President Biden, and even trying to get involved in Elon Musk's acquisition of Twitter.

By January 2022, several rounds of financing pushed FTX's valuation to $32 billion, attracting investments from Sequoia Capital, Temasek, Paradigm, among others. Against this backdrop, SBF was also trying to push for policy changes; let’s not forget that SBF's parents are both Stanford Law School professors and have close ties to the Democratic Party.

In October 2022, FTX proposed a regulatory draft called "Digital Asset Industry Standards," which would greatly benefit FTX if passed. (It is worth noting that Alameda co-CEO Sam Trabucco suddenly left in August 2022, which did not receive much attention, but there were deep waters behind it.)

A month later, FTX bid for Voyager. Why did they do this? It was likely to rescue a large number of FTT holders to prevent them from selling FTT.

At that time, SBF was still very aggressive, even mocking that he could come and go freely in Washington while Zhao Changpeng could not, but he later deleted the related tweets.

Soon, Coindesk published an article about Alameda's balance sheet, pointing out that a large portion of its $14.6 billion in assets was issued by the FTX team itself—sharks smelled blood.

On November 6, 2022, Zhao Changpeng announced the liquidation of all FTT assets held by Binance, worth up to $584 million at the time. Ironically, another co-CEO of Alameda, Caroline, announced that she would buy FTT from Zhao at $22, which backfired and sparked speculation that the actual liquidation price of FTT was below $22. The market reacted in panic. By November 7, 2022, according to Nansen data, stablecoins worth about $450 million left FTX within 7 days—a run began.

Shortly after, SBF publicly claimed that FTX did not invest customer assets and had enough funds to meet all withdrawals, but he later deleted this tweet. However, although withdrawals were frozen, Alameda was still able to withdraw funds from the exchange. When asked why, Caroline evasively said it was FTX US, which backfired and made people realize that the parent company FTX must have liquidity issues.

On November 8, 2022, FTX froze withdrawals. On November 9, FTX announced it might be acquired by Binance. On November 10, Binance announced it would abandon the acquisition.

Soon after, FTX seemed to resume withdrawals (Editor’s note: at that time, its wallet was detected to have a small amount of assets flowing out), but there were speculations that insiders were cashing out and mixing their withdrawals with those of other Bahamian users. On November 11, 2022, Sun Yuchen announced a cooperative arrangement allowing some FTX users to withdraw funds on Tron through assets related to that project.

So far, FTX officials and SBF have never answered questions about Bahamian withdrawals and whether insiders cashed out.

After declaring bankruptcy, withdrawals were finally suspended, but hundreds of millions of dollars had already flowed out of FTX.

On November 14, 2022, after a brief silence, SBF began posting "letter tweets" (What Happened) to mock the public. Crypto investor @ercwl revealed that SBF was likely using these tweets to fool bots designed to detect deleted tweets, but this has not been confirmed and is unlikely.

According to internal sources from FTX, only 4-5 senior executives knew the true situation of FTX, namely: SBF, Caroline Ellison, Gary Wang, Ramnik Arora, Constance Wang, Nishad Singh, while ordinary employees were almost completely unaware.

There are many interesting facts—such as SBF's so-called "addiction to stimulants," "office parties"—but they are irrelevant to those trying to uncover the truth, though perhaps The New York Times would love these gossip details.

Risk warning

Risk warning Risk warning

Risk warning