The Block Researcher: It's time to reflect on the chaotic capital allocation in the cryptocurrency industry

We are working to create an open system, but many founders within this system do not disclose information that is crucial for ordinary users and investors.

We are working to create an open system, but many founders within this system do not disclose information that is crucial for ordinary users and investors.Author: @dantwany, The Block researcher

Compiled by: Peng SUN

1/ The events in the crypto industry last week made me start to reflect on myself. For the past four years, I have been tracking and analyzing the capital allocation in this industry. Now, with the regulatory hammer about to fall, there has never been a better time to state my views on all the known issues.

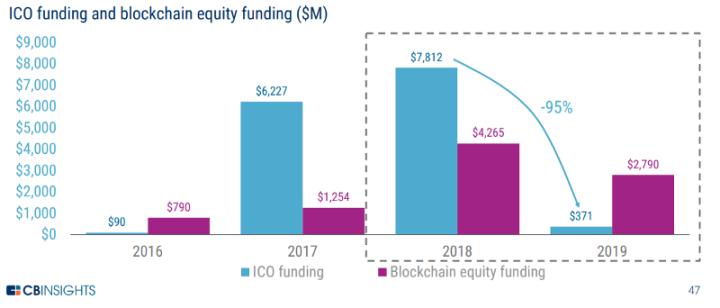

2/ In 2017/18, ICOs were the main driver of capital allocation compared to VCs. ICOs were rife with scams and bad ideas, but the public ICO model was more democratic than it is today. Of course, VCs were also investing, but they might have had the same participation conditions as ordinary people.

3/ Most of the most fascinating trends are also democratic and have not been captured by VCs for value, which is not a coincidence: anyone could participate in ICOs, anyone could participate in YFI's liquidity mining (DeFi), and anyone could mint a CryptoPunk or BoredApe (NFTs).

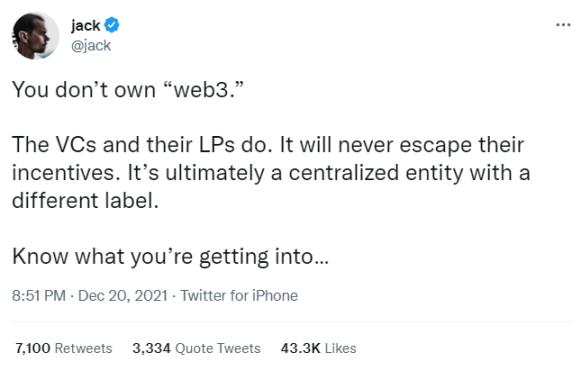

4/ We should ask ourselves, "How did we get here? Why is our system in 2022 clearly higher in barriers than it was in 2017?" @jack said, "Web3 is not yours, it's VCs and their LPs." This statement angered many people. Was he wrong?

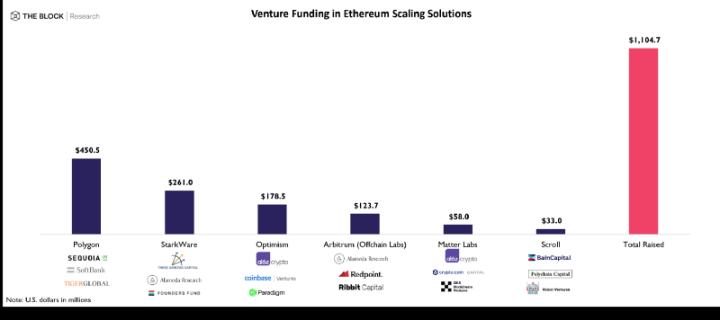

5/ Many pointed out the unfairness of an ecosystem (high FDV Solana ecosystem projects), but overlooked that the upward potential in that ecosystem has also been noted. Anyone can buy Ethereum. As for its future (L2s)? That is left to venture capital firms like SoftBank, Sequoia, and Tiger Global.

6/ I believe many projects wish their token allocations were more democratic. That’s why we see a large number of airdrops to users. The lack of regulatory transparency and concerns about fundraising from retail are the main reasons we have developed to this point.

7/ It may be that public sales are mostly a thing of the past, and due to regulatory issues, the venture capital model is the only way out. In any case, it is time to demand transparency regarding these token raises. For an industry that advocates transparency, there is a complete lack of it here.

8/ Projects want to behave like a typical startup (selling equity + token warrants), but at the appropriate time, they are a decentralized protocol. Just as we require exchanges to provide proof of reserves, we should demand complete transparency for all tokens they issue.

9/ We have created a system where there are publicly issued tokens that any retail investor can buy, but the founders do not have to disclose how much they raised, how many times they raised, when they raised, who bought, and at what price they bought.

10/ Ironically, we are striving to create an open system, while many founders within this system do not disclose information that is crucial for ordinary users and investors.

11/ Angel investing: In my view, the current financing environment has not received the attention it deserves, as many have advanced to become angel investors. Many have forgotten their original intentions. Why say things that are beneficial to themselves?

12/ Angel investing II: The openness of basic finance still exists, but only if you have advanced to that angel level. Unlike any other industry I have seen, the equity structure in the crypto industry sometimes looks like a novel with a large number of characters.

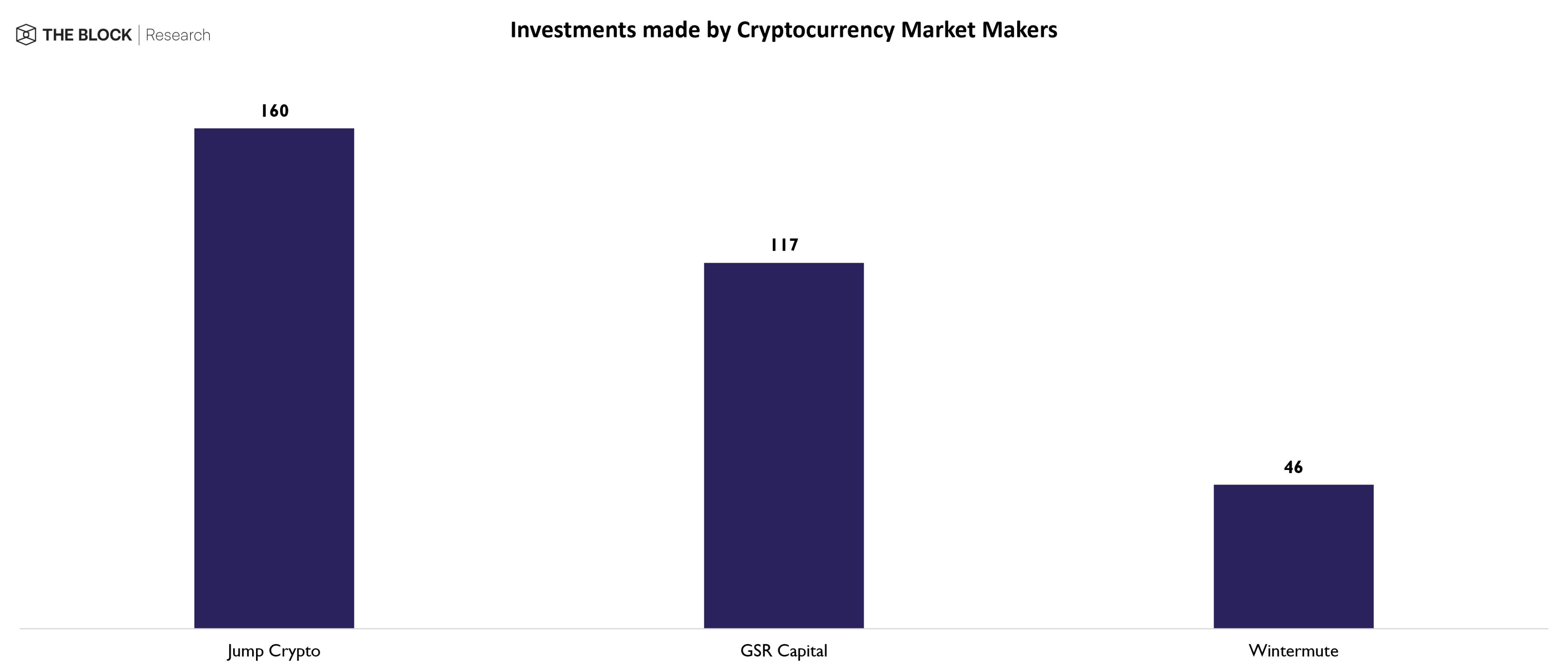

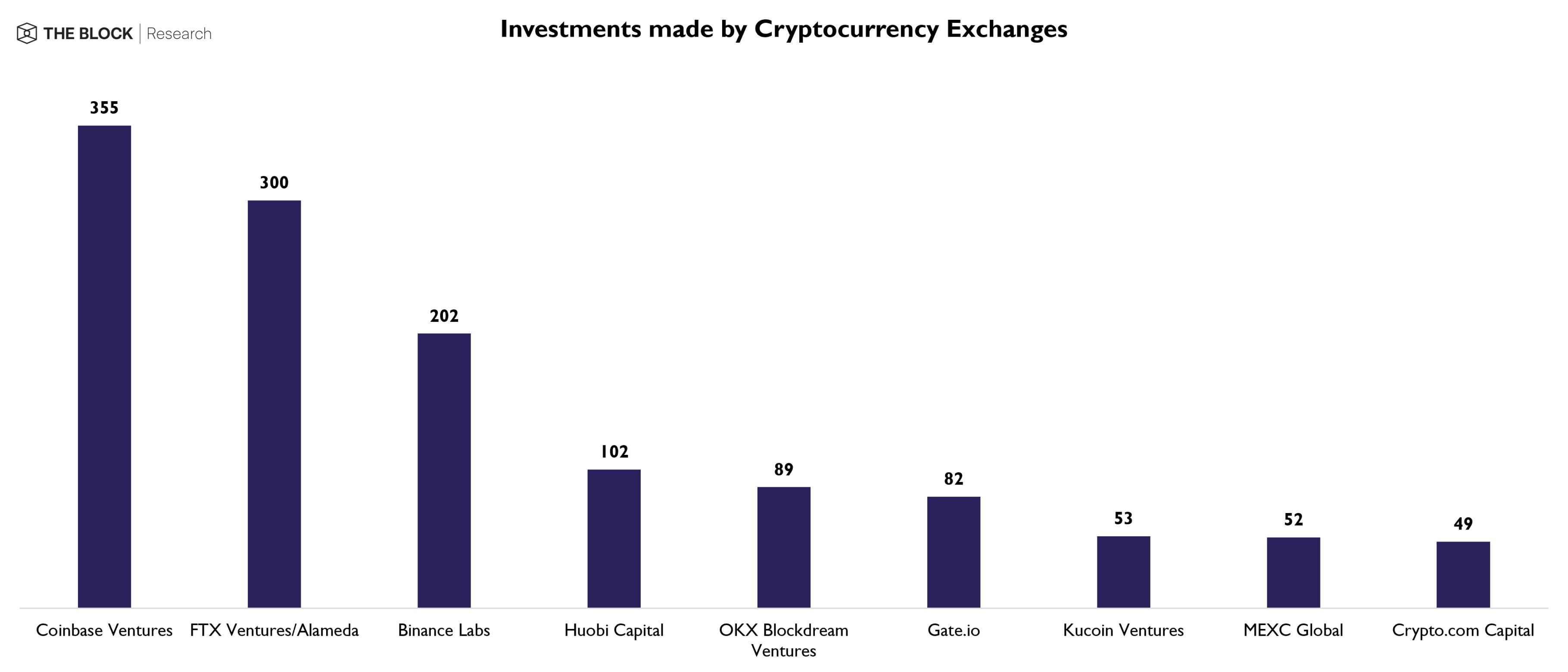

13/ Potential conflicts of interest: Outside of the most well-known venture capital firms in the field, who can get the most shares? Cryptocurrency exchanges and market makers. Simply put, project parties like to see themselves on their equity structure tables in hopes of getting listed and market-making.

14/ I have no doubt that for exchanges like Coinbase and Kraken, their venture capital departments are completely separate from their exchange businesses. However, can we trust this for many exchanges operating in the shadows? The downfall of Alameda/FTX exemplifies this concern.

15/ Should exchanges directly help tokens that are listed on their platforms? This is a question we should ask.

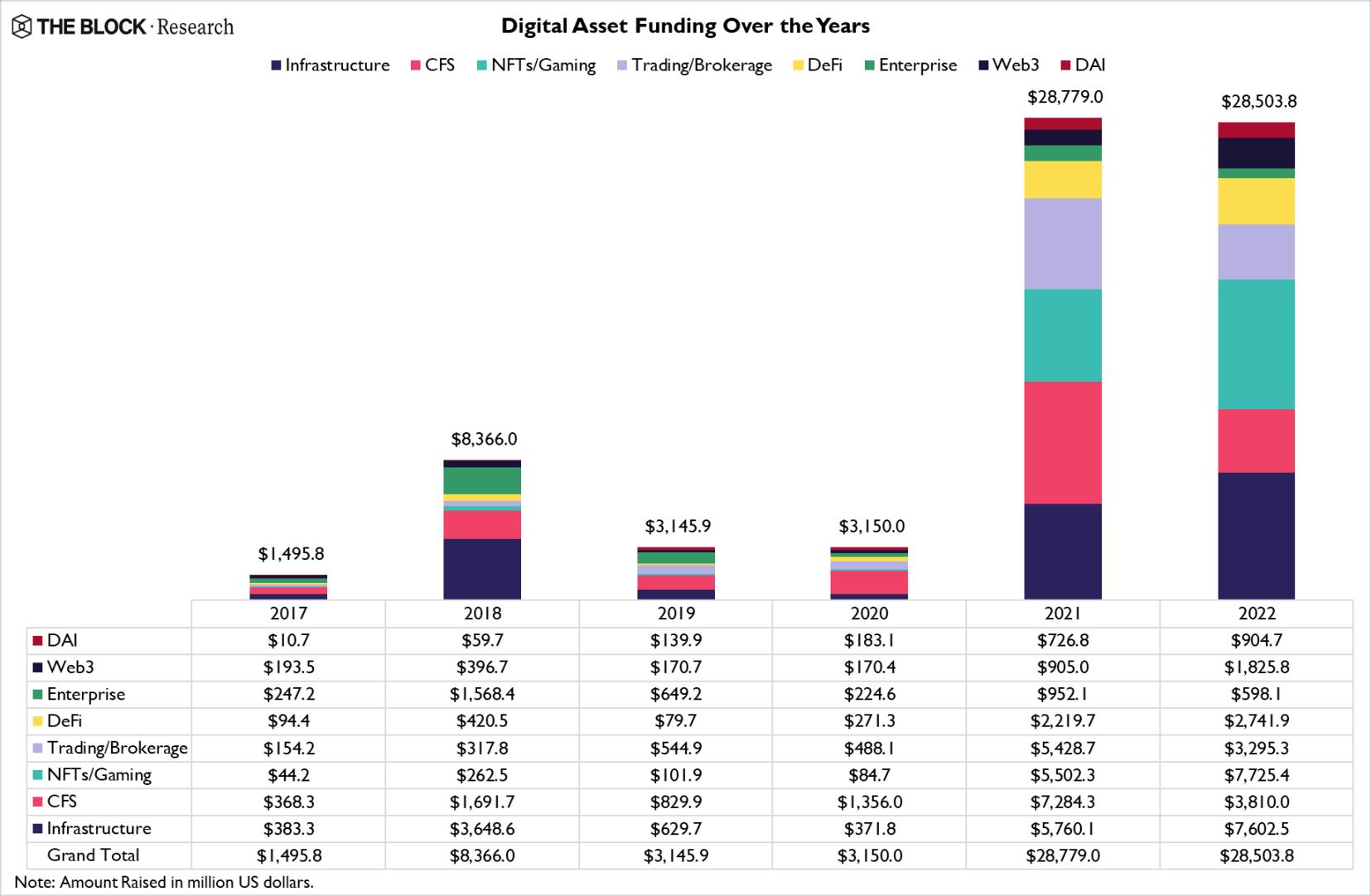

16/ Imagine a world where the most active investors in traditional finance are Nasdaq and the NYSE, and the financial information of these listed securities is opaque. This is the reality we face in the crypto space, and this is what we have created.

17/ What will happen in the future? Just this year, venture capital firms related to cryptocurrencies have raised billions of dollars. What is concerning is that many of these funds raised so much money because they are rolling funds. After recent events, there is no doubt that many LPs will seek to cut risks and pull back their capital.

18/ This does not include many who announced the establishment of new funds but are based on pre-committed funds. For example, Fund X raised $75 million for a new crypto venture capital firm, but it is said that only $25 million of that is actual commitments. Much of the announced funding is just soft commitments that will not be fulfilled.

19/ What about all the capital that has already been allocated? So far, nearly $30 billion has been allocated to crypto companies. Theoretically, these companies should be able to operate for years with such ample capital. But what if much of this money has already been spent?

20/ The coming months will reveal which companies are prepared for the long winter and which companies are idly dreaming of a "only up" environment like crypto degen traders. October has already been the lowest funding month since February 21, which is a fact before all the recent turmoil in the industry.

21/ What lessons should be learned from this? It is time to say less nonsense, to show sincerity, to improve, to self-reflect and adjust, to be transparent, and to let those projects that are fundraising tear off the decentralized veil.

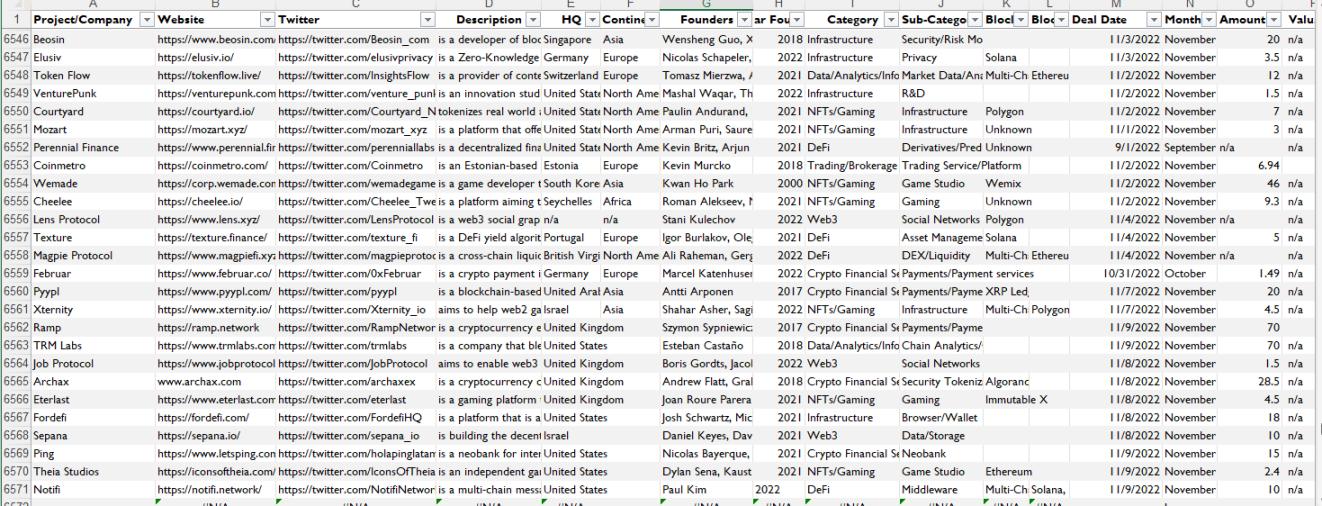

22/ Perhaps nothing will change. What I know is that my team and I have manually recorded nearly 6,600 crypto-related financing transactions and over 770 M&A transactions, and @TheBlockRes will do its best to make these markets as transparent as possible.

Risk warning

Risk warning Risk warning

Risk warning