Maverick's Internal Letter to Investors (Excerpt): Unscathed in the FTX Bankruptcy, Reflecting on the Investment System and Looking Ahead to Future Crypto Investment Opportunities

At Maverick, our top priority is always to ensure the safety of our own and our clients' assets and risk control. Managing risks before pursuing excess returns.

At Maverick, our top priority is always to ensure the safety of our own and our clients' assets and risk control. Managing risks before pursuing excess returns.Original Title: 《Maverick Investor Update on FTX Blow-up》

Written by: Simiao Li, Maverick Crypto

Compiled by: Biscuit, ChainCatcher

The impact of FTX's bankruptcy is still spreading, and there remains uncertainty about the subsequent developments. However, we now have enough time and information to 1) summarize the impact of this event on the Maverick portfolio, 2) retrospectively analyze our investment framework/process in light of this market stress test, and 3) look ahead to our views on the future of the cryptocurrency market and industry.

This article will avoid grand discussions about the background and moral implications of the FTX bankruptcy event. Handling this information is the responsibility of the courts and newspapers. As investors in the crypto market, our primary principle should be to pragmatically and objectively view the market, grasp market laws, and play the role of "market mechanics" rather than crypto moralists (although the moral conclusions surrounding the FTX incident should be quite evident).

Facts

Maverick was completely unaffected by the FTX bankruptcy.

1. No trading risk exposure: Maverick had no trading risk exposure on FTX, and we typically do not keep our large assets on a single centralized platform for the long term.

2. No portfolio risk exposure:

- We maintained 100% cash before and throughout the event. This was due to Maverick's self-developed indicators 1) being strongly bearish on current macro-level liquidity, and 2) assessing that the short-term trading style of the crypto market did not align with our investment system, leading us to maintain a very cautious position recently (details below).

- Maverick chose not to actively short during the entire event and its aftermath, as this type of highly unique event and news-driven shorting opportunities are not our system's strengths. Our investment horizon is medium to long-term, and the factors we best understand are the fundamentals of crypto assets, macro conditions, and structural changes in liquidity. We calmly observed the legendary "short-term event-driven news traders" in this "big short."

- Regarding FTX/Alameda-related assets:

a. We researched FTT while investigating CEX tokens and identified several warning signs. Overall, we found FTT less attractive compared to BNB and other CEX assets (more details below).

b. In the first half of 2022, we had two opportunities to invest in a small amount of FTX equity (secondary share transfers) at a slight discount to previous venture capital rounds, but we deemed FTX's valuation too high and declined to invest.

c. We maintain a long-term constructive view on Solana, but our position in it was zero before the event and remains so at this time. In the future, we may accumulate positions related to Solana, provided we can continue to see new developer activity (details below).

d. We have no exposure to any other ecosystem assets related to FTX/Alameda.

Whenever such a collapse occurs, what is more important than discussing specific investment outcomes is to deeply reflect on and optimize our investment and risk management systems ("investment machine"). The history of the crypto asset market is not long, and there are not many long-tail case samples, so the FTX bankruptcy event serves as a rare stress test for our investment framework and risk management processes that can be compounded and improved.

Detailed Explanation of Investment System Process

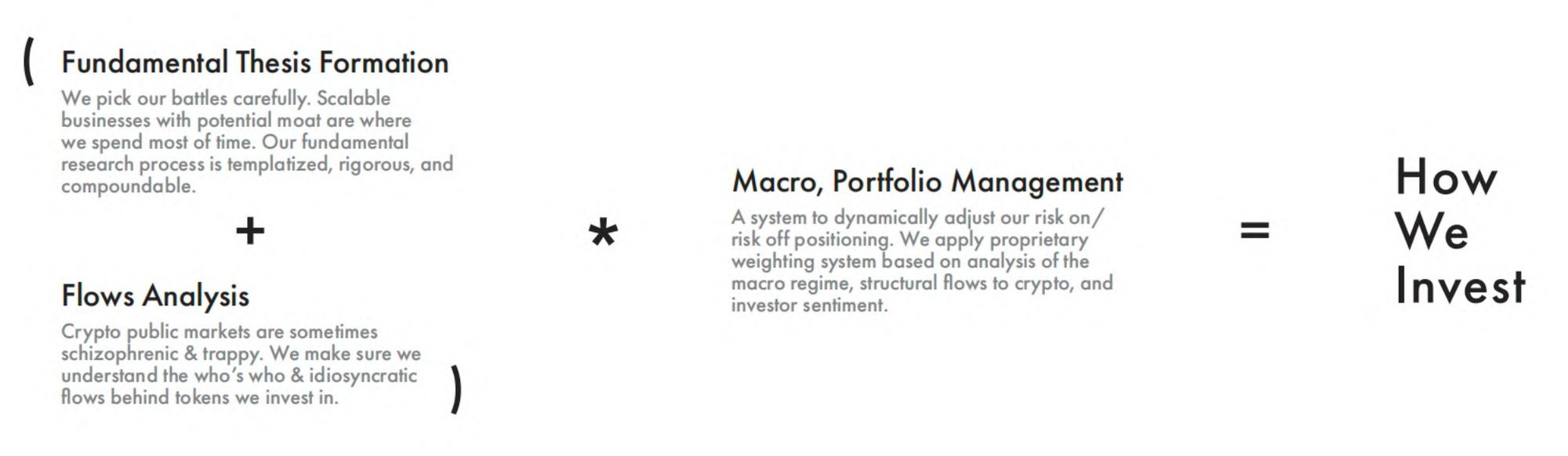

Maverick's investment framework has three key pillars:

- Fundamental analysis

- Liquidity analysis

- Macro environment and portfolio risk management

We only amplify overall risk exposure when the asset targets and market conditions meet all the criteria in the above framework.

Top-down risk exposure management

We combine 1) macro indicators, 2) liquidity-based market indicators, and 3) tracking investor sentiment to understand the market environment and style we are in. This ensures that we have top-down control over the total risk exposure of our portfolio at any given time.

Before the FTX bankruptcy event, the market had been rising continuously, but we maintained cash because:

- We were strongly bearish on a macro level, especially after the hawkish FOMC meeting. We have repeatedly stated that given high inflation and a persistently hot labor market, the Fed's framework is akin to Volcker's hardcore hawkish stance, and the macro turning point has not yet arrived. The Fed is data-driven, and data is always lagging; the current attitude of the Fed clearly leans towards ensuring a significant drop in inflation, even at the cost of economic recession and further declines in the stock market. Therefore, as secondary market investors, attempting to predict the Fed's pivot in advance is counterproductive.

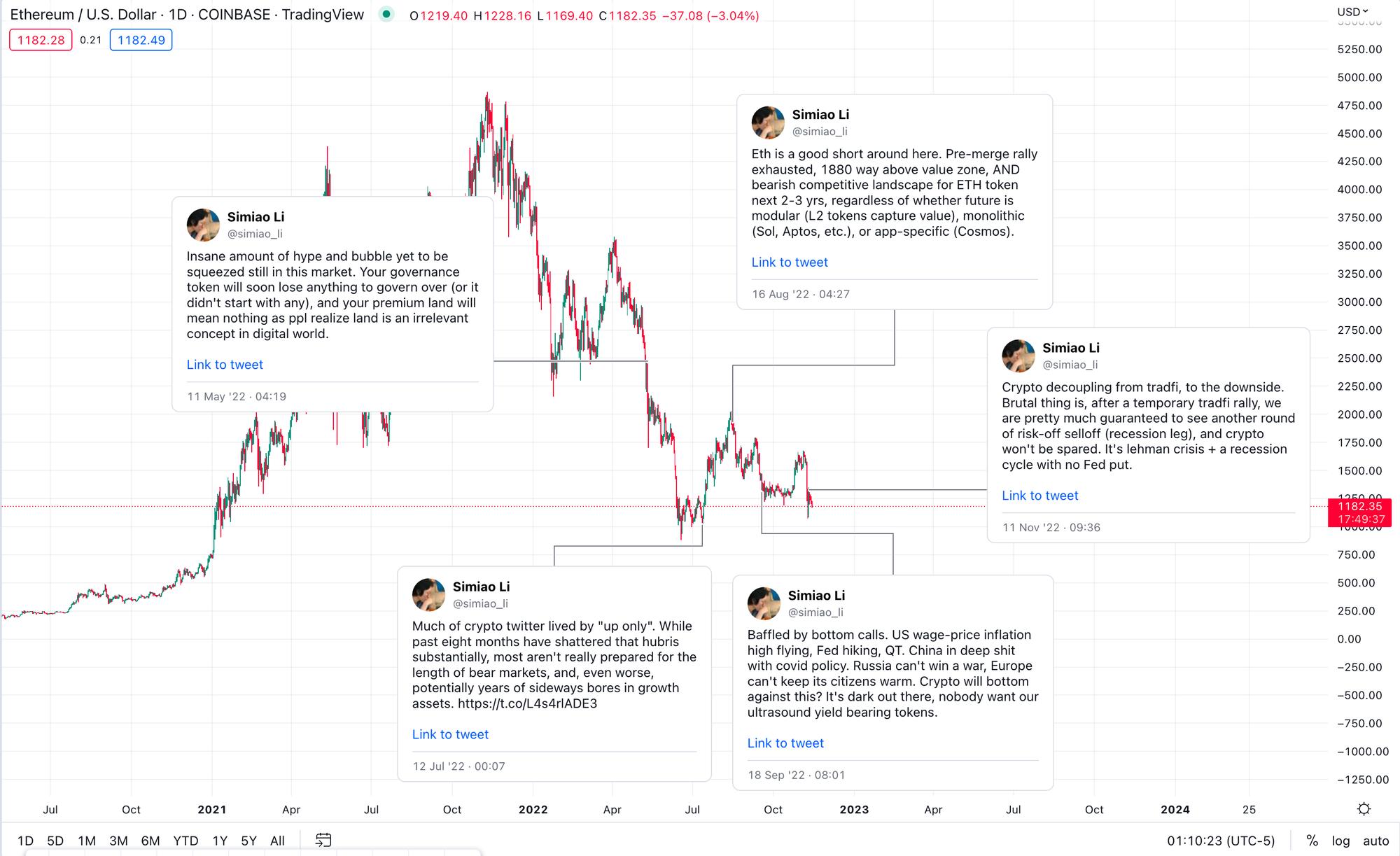

Note: Our tweet list regarding the overall market direction.

The market dashboard developed by Maverick based on liquidity shows that the crypto market is currently in a very unfavorable short-term PvP "meta-game," leading us to choose to hold 100% cash positions.

"There is little new capital flowing into the crypto market. While stablecoins have the firepower, there are no major catalysts to drive deployment. Additionally, a large number of tokens will be unlocked in the next 6-12 months."

"This is clearly a PvP market. There is no clear trend, fluctuations within a small range, and increasingly difficult theme rotations to chase. Uptrends do not last beyond brief news cycles, such as the surge caused by Instagram supporting NFTs or the Twitter acquisition event."

"The current market conditions are not suitable for our investment time frame and style."

Considerations on (Not) Shorting

Our investment system will not hesitate to hedge and deploy capped net short positions when necessary, but during this round of declines, we chose to maintain zero net exposure. For various reasons, shorting in this environment is exceptionally dangerous, as all volatility is driven by unpredictable news:

1. Highly unique news-driven events:

Before the event: There was no insider information, and it was difficult for anyone to predict how such a singular event would unfold. Frankly, we previously thought the likelihood of FTX going bankrupt in this manner was relatively low.

During the event: As events unfolded and new information emerged, the likelihood of bankruptcy increased, but the progression was very rapid (from FTX's run on the bank, Binance's suspected acquisition, to FTX announcing bankruptcy in less than 48 hours). Throughout this process, shorting FTT, Sol, or related assets was high-risk because many short-term price changes were influenced by negotiations involving various participants (Binance, Justin Sun), and we had little advantage in judging these developments.

In the later stages of the event: As trading volume stabilized and prices ended the first wave of declines, the risk-reward ratio for shorting significantly decreased. We believe the bankruptcy event will continue to unfold, and dominoes will fall, but these events are inherently difficult to capture in real-time, as those unable to pay have strong incentives to pretend to be solvent until they can no longer do so.

2. Extraordinary counterparty risk:

- Additionally, in extreme cases, all centralized exchanges carry additional counterparty risk, and it is likely that the profit potential of short positions will not compensate for the loss of principal.

There are many experienced news event traders in the market, and we prefer to wait and watch them counter each other. This is not our time to act; even if we profit from shorts, it would be due to luck rather than skill.

Due Diligence on FTT

We have previously conducted in-depth research on exchange tokens (and equity) and ultimately preferred other opportunities (such as BNB, Coinbase equity) over FTT for various reasons:

Opaque value capture: FTT has neither significant native demand (unlike BNB) nor a transparent and long-term guaranteed cash flow accumulation mechanism (unlike Coinbase stock), but rather an opaque "burn" conducted by the FTX exchange.

Conflict of interest with FTX equity: FTT contributes nothing to the FTX exchange, yet it is a net non-cash expense of one-third of the exchange's revenue. There is a strong conflict of interest between FTX equity holders and FTT.

FTX's commitment to FTT is questionable: Given that FTX attracted a large amount of venture capital and appears to aim to become a publicly traded company, retaining FTT would not align with their interests if/when this occurs.

Why would FTX continue to operate a token that has no significant positive contribution to the FTX exchange and would continually drag down their revenue? Why would shareholders allow them to maintain this status? We are puzzled by this. We saw enough warning signs with FTT to avoid participating. Here are our original internal notes: [CEX Token Economics Research]

It turns out, of course, that the developments were much worse than we anticipated. FTT now appears more like a token purely for manipulating prices, increasing collateral value, and keeping the FTX Ponzi machine running. In hindsight, we may have found the answer to why FTX continued to operate what seemed like a strange token.

Due Diligence on Other Related Tokens

Solana (SOL)

We currently have no risk exposure to Solana and its ecosystem assets. However, our long-term fundamental view on the Solana ecosystem is worth mentioning separately. In the later sections of this article, you can see our forward-looking comments on Solana.

SRM and other FTX/Alameda-related projects

We have never engaged with these assets and do not intend to spend much time focusing on them in the future. The low circulation/FDV has always been a turn-off for us. Generally, we do not pay particular attention to popular venture capital targets, as the average quality of hot assets in the primary market is questionable, and ironically, the level of enthusiasm in early-stage projects often inversely correlates with expected returns in the public market.

However, we remain very interested in order book-based decentralized exchanges (CLOB) built on high-performance blockchains (whether Solana or other networks), as we have always believed this is the next step in DEX development.

Forward-Looking Views

Macro Level: Resisting the Temptation to Catch Falling Knives

This is the Lehman moment for cryptocurrencies and the trigger for the "ultimate bomb" that we have been waiting for internally over the past year. The domino effect has not yet fully revealed itself, so now is not the time to play the hero; do not attempt to catch the falling knife.

We will publish a longer article to provide more reference points based on historical cases (both crypto and Tradfi), but for now, we can present a simple argument.

We do not know more publicly available information regarding the impact of FTX's bankruptcy, but the liquidity gap of billions of dollars will not be easily absorbed by the young crypto financial system. Especially in a situation where liquidity has already dried up due to the bear market, market makers and proprietary trading firms are likely to pause restructuring after suffering heavy losses. Liquidity crises will be ubiquitous, and credit both inside and outside of crypto will become increasingly tight.

There is no Federal Reserve to save us all in the cryptocurrency space. While some hope that Changpeng Zhao (CZ) and Binance will take on this role, it contradicts CZ's philosophy ("let the market do what it should, and price does not matter in the short term"). Even if CZ wanted to play the savior, there are no prior cases or "deep market memories" to solidify the market consensus of "CZ the crypto Powell," allowing "CZ" to boost the crypto market in the same way as the Fed.

Our view is that the crypto market will experience some consolidation within a narrow price range, followed by one or two more collapses, likely accompanied by the spillover effects of the FTX incident and the last drop in the traditional financial market as recession expectations set in. After that, the market will undergo several months of range-bound fluctuations characterized by low volatility and random movements, which we internally refer to as "the nothingness stage," until some catalyst triggers the next uptrend (possibly related to a pivot in Fed policy).

In any case, the risk-reward ratio for prematurely going long in the current environment is very poor. Even if we are wrong in our view and this is indeed the bottom of the market, we will not see a V-shaped reversal because:

1) Macro environment and liquidity conditions (bearish);

2) Structural liquidity pressure in cryptocurrencies (bearish);

3) Lack of transformative innovative catalysts that excite institutional or retail participation;

4) The likelihood of negative regulatory catalysts emerging in the next six months.

Solana

Frankly, it seems very difficult to remain optimistic about Solana right now, but typically, when things swing to the extremes of the pendulum, genuine independent insights can shine and yield substantial returns. If we see sustained developer activity in the Solana ecosystem over the next 12 months, we believe the risk/reward of holding SOL will again become attractive. At present, we will not provide a 90% confidence interval judgment on anything within the Solana ecosystem; we will continue to monitor developments. However, at this juncture, cautiously waiting for positive changes with an open mind is far more rewarding than maintaining a bearish stance.

This is a long-overdue cleansing of the Solana ecosystem, ridding it of opportunists who have hijacked the Solana narrative. In the short term, this ecosystem will be intertwined with pain—we expect prices to decline further, liquidity to dry up, and some projects within the ecosystem to migrate to another blockchain.

However, the Solana technology itself is differentiated and promising. The founding team of Solana emerged during the last bear market cycle; they are not crypto tourists but a group of committed, capable engineers. Now is the time for the Solana native developer community to rise and shape their ecosystem.

Contrary to intuition, the collapse of FTX and their allies may actually be beneficial for Solana. Because the narrative of "VC/giant-backed L1" has been thoroughly shattered, the impact on Solana's direct competitors (other high-performance single chains like Aptos and Sui) is equally profound, yet the latter lacks a truly spontaneous community that has experienced peaks and troughs together to endure the upcoming bear market. In the world of cryptocurrencies, path dependence is crucial; the trajectory of projects and assets (especially L1) often ultimately hinges on the people/community behind them and whether they have the motivation to become "diamond hands." Among human nature, what unites people more than fleeting glory is the suffering that follows glory and the rebirth after suffering. The path Ethereum has walked may be one that Solana will retrace.

In summary, we remain attentive to see how things unfold. This could either be a top-tier buying opportunity or a dismal exit for a fragile ecosystem. Before reaching an epic conclusion, there are almost no more viewpoints to showcase.

Beneficiaries of the FTX Bankruptcy

Not all hope is lost. Some crypto assets will clearly benefit from the FTX bankruptcy, and starting to deploy some pair trades from here could be very interesting.

Binance Chain (BNB):

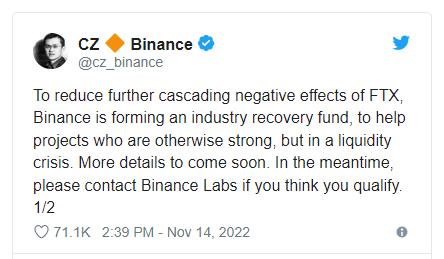

Binance has solidified its leading brand and market share. Some projects that were previously built on and/or funded by FTX/Alameda will migrate to Binance, under the protection of the BNB chain and Binance Labs (we have already seen the savvy CZ make moves after taking down FTX).

Source: https://twitter.com/cz_binance/status/1592044496174612482

Overall, we have always believed that the BNB ecosystem is underestimated by crypto-native investors. It is the Ethereum of the East, backed by a benevolent dictator, with strong execution and support from grassroots crypto players. We have always been long-term bullish on BNB, and this event is merely a catalyst for that direction.

Source: https://twitter.com/simiao_li/status/1568176304780091392

Polygon (MATIC)

Currently, Polygon hardly needs anyone else's help, as they have been leading other public chains in execution and business development for a long time. The collapse of FTX and its allies is undoubtedly another strong impetus for Polygon in the context of the bear market. After the dust settles, pair trading (long MATIC, short SOL) will be interesting for the medium term.

Native Infrastructure

Code must replace trust. This is the only way cryptocurrencies can break the monopoly of intermediaries and thwart anti-social actors. This is also the consensus among mainstream funds after the FTX collapse. Rebuilding a better, scalable on-chain financial system requires robust high-performance infrastructure. We will seek to invest in key decentralized infrastructure crypto assets, provided that: 1) the team remains committed and possesses resilient capabilities; 2) the project can become a core part of the next round of crypto technology stack; 3) it adjusts to attractive valuations during the bear market.

We will update and publish our internal in-depth research on key infrastructure at the appropriate time.

Next-Generation Non-Custodial Wallets with Improved UI/UX

If you don't own the private keys, you don't own the cryptocurrency! But don't expect ordinary people to have the patience to become seasoned users of crypto wallets through a 20-step process. We must cater to the needs of ordinary users. This requires a balance between security and user experience. As token investors, we do not expect to directly capture this trend, but we have noticed some emerging next-generation wallets, such as OneKey, that offer promising solutions.

DEX (especially derivatives)

There is no doubt that FTX was the exchange focused on crypto derivatives, and its collapse is favorable for DEX, especially derivatives. The market has already reacted, with GMX and Dydx performing well. We believe this is more of a key long-term investment argument. Uniswap has more than ten times the upside potential in the next cycle. We had already conducted research here before the FTX saga. We expect to release a paper on derivative DEX in the coming months.

NFT Exchanges

This may not be obvious, but we believe NFT exchanges will benefit significantly from this situation. Regulation will continue to crack down on token trading and DeFi, making NFTs (which are not directly related to finance and have always been non-custodial) gain the attention of users and speculators in a relatively better environment. We will conduct in-depth research on the NFT market, but currently, we are interested in 1) mobile-first; 2) game-related NFT exchanges, especially if these projects are built in less competitive regions of the Eastern Hemisphere.

Image Source: https://twitter.com/simiao_li/status/1591998055234273280

In Conclusion

From time to time, a catastrophic event occurs in the crypto market, ringing alarm bells for the industry and all involved parties. The FTX bankruptcy is one of them.

At Maverick, our top priority is always to ensure the safety of our and our clients' assets and risk control. Managing risk before pursuing excess returns. In the long run, we will continue to refine our investment system, using such events as valuable stress tests and case studies.

Cryptocurrencies will continue to exist, but as an industry, we all have some overdue "clean-up" work to do. Let us overcome these challenges and move forward.

Yours Sincerely,

Simiao Li

Founder & CIO, Maverick

Risk warning

Risk warning Risk warning

Risk warning

Popular articles