After the collapse of leading market makers like Alameda and Genesis, how does DODO meet the market-making demand?

No need for permission, efficient and transparent, self-created market, everyone can enjoy the benefits of liquidity creation. The market-making vision depicted by DEX sounds too perfect.

No need for permission, efficient and transparent, self-created market, everyone can enjoy the benefits of liquidity creation. The market-making vision depicted by DEX sounds too perfect.Original Title: 《Demonetizing Market Makers》

Author: Yaoyao, DODO Research

FTX's explosion, the collapse of the empire, a series of leading platforms suffered heavy losses, market makers and lending became the hardest-hit areas: Alameda, as one of the largest market makers in the cryptocurrency industry, perished in this farce and officially ended trading on November 10; DCG's market maker and lending company Genesis also faced the dilemma of insufficient repayment ability.

The collapse of leading market makers, the destruction of large amounts of capital, and the sharp one-sided market conditions… this has caused unprecedented panic among industry market makers. In the aftershocks, market makers tend to come to a standstill, communities and projects face enormous pressure tests, and market liquidity in the cryptocurrency industry has encountered a significant decline.

Whether in traditional markets or cryptocurrency markets, for the general public investors, talking about market makers always feels like playing a game of blind men touching an elephant.

Now, let’s start from the beginning.

Table of Contents

1. Market Makers in the Cryptocurrency Field

- What is a market maker, how do they operate, and how do they profit

- Market makers in the cryptocurrency market

- What is the use of market makers

- Market making strategies

- Opportunities, risks, and the Wild West

2. Yes or No: Everyone is a Market Maker

- Market makers vs. automated market makers

- AMM: Everyone is a market maker

- Why LPs lose money

3. The Collapse of Leading Market Makers: After the Market Loses Liquidity

- Market makers in the domino effect

- When the market loses liquidity

- How DODO meets market making demands

Market Makers in the Cryptocurrency Field

What is a market maker, how do they operate, and how do they profit

According to Wikipedia, a market maker is referred to as a "specialist" on the New York Stock Exchange, called a "dealer" in the Hong Kong securities market, and known as a "market creator" in Taiwan.

As the name suggests, a market maker is someone who creates a "market."

In traditional financial markets, a market maker is a commercial organization, usually a brokerage firm, large bank, or other institution, whose main job is to create liquidity in the market by buying and selling securities;

Market making is an established and mature financial practice in which market makers provide liquidity and depth to the market, allowing both buyers and sellers to transact without waiting for a counterparty to appear, as long as a market maker is willing to take on the counterparty's side of the trade, they can complete the transaction, and the market maker profits from the bid-ask spread.

The difference between the buying price and the selling price in the market is called the bid-ask spread, which is the primary way for market makers to profit (they can also earn through trading platform rebates, as trading platforms pay some market makers to increase trading volume and enhance profits).

In a liquid market with many buyers, sellers, and market makers, the spread is small, and market makers need to conduct a large number of trades to profit. They use highly advanced quantitative algorithms to establish very short-term positions—ranging from a few hours to a few seconds. The greater the market volatility, the more trades market makers can execute, and the more profits they earn.

Buying this asset requires 103, selling this asset yields 97, the spread earned by the market maker is 6

In simple terms, market making is about providing two-sided quotes to any given market, offering market size for both buying and selling; without market makers, the market would be relatively illiquid, hindering the convenience of trading.

Market Makers in the Cryptocurrency Market

Whether in traditional markets or cryptocurrency markets, liquidity is the lifeline of all trading markets, and market makers are the helmsmen.

In the cryptocurrency market, market makers are also referred to as liquidity providers (LPs), which perhaps directly points out: Like traditional markets, the cryptocurrency market needs market makers to help guide the market's "invisible hand" to solve liquidity traps.

This liquidity trap mainly manifests in a vicious cycle:

Cryptocurrency projects need people (cryptocurrency exchanges and cryptocurrency investors) to contribute to token liquidity; at the same time, these people will only participate when the tokens have market liquidity.

And this is where Market Makers come in.

In simple terms, market makers nurture liquidity with liquidity, a project usually needs to leverage the support of market makers to provide liquidity, confidence, and upward price momentum for their token market until the trading volume is sufficient for them to maintain their own trading ecosystem.

How professional cryptocurrency market makers solve market liquidity issues for projects

source: Wintermute

What is the Use of Market Makers

Taking cryptocurrency as an example. One of the core points, of course, is the liquidity that has been repeatedly mentioned. Because liquidity is the foundation of any effective market.

- Strong pricing function: Market makers can track price changes over the long term, make judgments on the fair price of the market, and provide the most referenceable quotes. For example, platforms like 1inch not only guide funds to different liquidity pools but also invite some market makers (such as Wintermute) to quote.

- Enhanced market liquidity: Investors can trade directly with market makers without waiting or searching for counterparties. Market making is about providing two-sided quotes to any given market, which is the core of providing liquidity.

- Improved overall market efficiency: Market makers quote through various trading platforms, eliminating chaos between markets through arbitrage, helping to improve overall market efficiency. For example, Kairon Labs currently connects to over 120 exchange APIs, assisting in reducing the impact of price fluctuations.

- Facilitating new token promotions, lowering issuance costs: Market makers will drive trading volume to continuously rise and see a large number of new tokens appear on multiple cryptocurrency exchanges.

- Increasing trading volume and market expectations: Attracting investor attention, enhancing market confidence, thereby driving token prices up.

- Facilitating large transactions: Market makers themselves are suitable for becoming counterparties for institutional investors to conduct large transactions.

Market Making Strategies

Market making strategies refer to a method of establishing limit buy and sell orders separately, utilizing fluctuations in the underlying price to trigger limit orders, and obtaining trading profits through the difference between buy and sell orders. This belongs to the risk-neutral arbitrage strategy within high-frequency trading strategies. In simple terms, it is the middleman earning the spread mentioned earlier.

Twitter user 0xUnicorn detailed common market maker trading strategies categorized by spot and futures in a tweet, and will not elaborate further here. Of course, strategies can also be more specifically divided into: delta-neutral market making (self-hedging inventory risk), high-frequency "instant" market making, grid trading, etc.

In essence, the focus of market making strategies is on the number of limit orders and the setting of the distance between buy and sell quotes and the midpoint price, thus in various classic market making strategies, the main research is on estimating the midpoint price, and then setting buy and sell orders at appropriate positions on either side of the midpoint price. Therefore, market makers are most afraid of sudden one-sided market conditions, as this means that buy and sell orders will experience one-sided transactions, accumulating a large amount of risk positions.

Risks, Opportunities, and the Wild West

As mentioned above, risks mainly come from inventory risk.

When a large amount of inventory accumulates, it also means that the market maker has a greater chance of being unable to find buyers for their inventory, leading to a risk: holding more assets at the wrong time (usually during depreciation). Another situation is that market makers may have to start selling their inventory at a loss when asset prices rise to maintain operations.

In DeFi, the handling of market making risks may be more cautious. For example, perpetual contracts. Market makers often utilize the funding rates of perpetual contracts (the core mechanism is to anchor the contract price to the spot price) to conduct arbitrage between spot and leveraged positions. In summary, this arbitrage method involves creating positions of equal value in the spot/leverage and perpetual contract markets, with opposite position directions. Therefore, under abnormal price fluctuations, market makers will face significant liquidation risks because the positions they hold due to arbitraging different funding rates may be large.

Opportunities arise from high returns behind high risks. Even a $0.01 spread, when such trading orders are executed a million times in a day, can yield profits of $10,000.

Market makers also provide leverage to traders, and once clients are liquidated, market makers can liquidate the traders' collateral. According to coinglass data, the daily liquidation amount in cryptocurrency ranges from $100 million to $1 billion. This will enable market makers to achieve substantial profits.

It is undeniable that the cryptocurrency market is still in its early stages, and compared to the very mature market making operations in traditional financial markets, there is still a crazy side running here.

If we zoom in on some details of cryptocurrency trading: asset liquidity is relatively low; significant slippage risk; when large orders appear or when a large number of sell orders cancel the best buy quotes in the order book, the possibility of a flash crash is very high. These characteristics often bring some hidden corners or profits to crypto market making.

Overall, due to technological and regulatory factors, for market makers, the cryptocurrency market and users still feel a chaotic sense of blind men touching an elephant.

Welcome to the Wild West. When a market maker promises a specific trading volume level to a token issuer, the next step will be a more ambitious commitment: the token price will rise to a specific level. How to achieve this?

- Wash Trading: A beginner trader will place a large sell order and then place a buy order for themselves within a few seconds. An advanced trader will use smaller orders and place them for a longer time; at the same time, to avoid detection by exchanges, they will operate from multiple accounts rather than a single account.

- Pump-and-dump: Among all price manipulation strategies, the pump-and-dump practice is particularly common. Social networks are the best front line; once the FOMO sentiment is strong enough, they can profit by selling a large number of tokens purchased in advance.

- Ramping: Ramping refers to creating an impression of a large buyer. Market makers can adopt this strategy to create a "big buyer" that conducts large transactions within a fixed time frame; here, FOMO sentiment comes into play again, as other traders rush to get ahead of the "big buyer" (but ultimately become losers)—when the market notices such behavior, prices naturally rise. Of course, once the market maker's activities end, the phantom buyers will mysteriously disappear, and the token price is likely to plummet.

- Cornering: When a token has multiple market makers simultaneously, a certain market maker can attempt to buy a large portion of the available tokens to profit, forcing other market makers to raise prices because they must maintain the spread at the same level. Due to the complete lack of regulation, these speculative operations indeed appear in the execution strategies of market makers, ultimately disrupting the market, erasing confidence in trading assets, losing trust from exchanges, affecting the reputation of projects, and leading to long-term losses.

Yes or No: Everyone is a Market Maker

Market Makers vs. Automated Market Makers

Although market makers (MM) and automated market makers (AMM) sound similar, they are completely different entities.

As mentioned earlier, in traditional finance, a market maker is an institution or platform that offers various securities trading to multiple exchanges, providing liquidity to the market and profiting from the bid-ask spread.

AMM, on the other hand, is a decentralized exchange (DEX) protocol that, unlike traditional exchanges that use order books, prices assets based on specific pricing algorithms, with the pricing formulas varying by protocol.

For example, Uniswap uses the following mathematical curve to determine trading prices: x * y = k

Where x and y are the quantities of two assets in the liquidity pool, y is the quantity of another asset, and k is a fixed constant, meaning the total liquidity of the pool must remain constant.

The working principle of AMM is similar to that of traditional order book trading platforms, both of which set trading pairs (e.g., ETH/DAI). However, the former does not require trading with specific counterparties. In the AMM mechanism, traders interact with smart contracts to "create" a market for themselves. The liquidity in the smart contract is provided by liquidity providers (LPs), who earn fees from trades conducted in the trading pool as a reward for providing liquidity to the protocol.

AMM: Everyone is a Market Maker

In traditional financial terms, AMM refers to a method that simulates human market maker behavior through algorithms, and in the DeFi space, it has gradually evolved into a violent engine:

It uses automated algorithms to balance the supply and demand of tokens in the trading pool, avoiding situations where a certain token could be bought out (with no buy/sell orders in the market) under a one-sided market condition that could occur in order book models;

Unlike other market makers, for example, CEX market makers profit from the bid-ask spread, adjusting their positions to control inventory based on their strategies. DEX market makers provide liquidity differently from CEX market makers, and they also earn trading fees;

When these trading fees are given to liquidity providers, it incentivizes them to inject idle assets into the trading pool to provide liquidity, which to some extent also solves the problem of insufficient trading depth in order book models.

AMM-based DEXs have proven to be one of the most influential DeFi innovations, breaking the limitations of order books and matching, helping DEXs break the monopoly of CEXs in the cryptocurrency trading market, making open and free on-chain trading a reality. It is also AMM that allows ordinary users to participate in market making in a permissionless way, enabling every DEX to proudly declare: Everyone is a Market Maker.

No permission needed, highly efficient and transparent, self-created markets, everyone can enjoy the benefits of liquidity creation. The vision of market making depicted by DEX sounds too perfect.

Why LPs Lose Money

Now let’s clarify the vision and reality.

The first question is, will users become LPs and definitely profit from market making on DEX? (A voice: Did you forget about impermanent loss?)

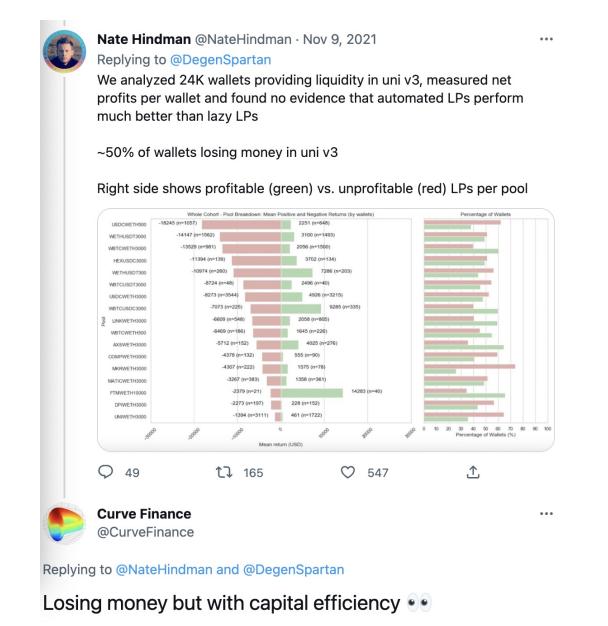

In a widely cited study on Uniswap v3 LP losses, rekt brutally points out: compared to providing liquidity on Uniswap v3, they (users) would be better off choosing to HODL.

As indicated in the article, during the period from May 5 to September 20 when V3 was launched, 17 asset pools with TVL > $10 million (accounting for 43% of TVL) generated over $100 billion in trading volume, earning LPs about $200 million in fees. However, during the same period, losses due to impermanent loss exceeded $260 million, resulting in a net loss of over $60 million. In other words, about 50% of V3's LPs were losing money.

Although Uni V3 popularized the concept of leveraged liquidity provision—where the range of liquidity provided is narrowed, achieving a higher degree of capital efficiency by eliminating unused collateral. This leverage increases the fees earned but also increases the risks taken, as high-leverage liquidity will face higher impermanent losses.

The reason goes back to the design goal of Uni V3: customized market making.

For users, higher proactivity means that market making operations become more complex. LP earnings depend on LPs' ability to judge the market, increasing the decision-making costs for LPs, leading to uneven LP earnings. This design has also given rise to the phenomenon of JIT (Just In Time) attacks (utilizing V3's concentrated liquidity to set LP positions for adding and withdrawing within the same block, thus strictly defining the range of positions to match trades, amplifying the transaction fees).

Enhancing capital efficiency while simultaneously losing earnings—this is not what LPs want to see.

https://twitter.com/NateHindman/status/1457744185235288066?s=20\&t=jb-YsLK25pE8GuHZaMAudg

This raises the next question: will users lose money when they become LPs on DEX?

Let’s simply answer this question: Whether DEX market makers profit or not, aside from subjective ability, it mainly depends on what model the trading pool they provide is.

In traditional AMM model pools—there is no difference in the profit logic of ordinary users providing liquidity and professional market makers, as the capital and external quotes of market makers are limited by the AMM function. Essentially, it is a competition of TVL, which determines who can earn higher trading fees.

In pools where prices can be customized—such as Uni V3, Balancer V2, Curve V2, DODO V2. These pools allow market makers to actively intervene in the pricing of the pool, enabling them to utilize these tools to profit from the price differences and lags between CEX and DEX markets (and now there are many DEX aggregators, better quotes mean that the pool is more likely to be captured by aggregators).

One of the reasons LPs lose money is that they choose a scheme that is not suitable for them.

So why do leading DEXs offer pools that allow for price customization? Not just Uni V3, when liquidity is evenly distributed along the curve, they will face issues of excessive slippage and dispersed liquidity. Therefore, traditional AMMs all want to enhance capital efficiency, and the aforementioned Uni V3, Balancer V2, Curve V2, DODO V2 are all moving towards concentrated liquidity optimization.

In comparison, the advantage of proactive market making is that users can concentrate liquidity in a certain range by adjusting prices, improving capital efficiency, thus reducing slippage and increasing depth; but the disadvantage is that it raises the threshold for ordinary users to participate in market making to some extent, making it more suitable for professional market makers. While the potential for profit may increase, we must acknowledge that the risk of losing money also increases, as ordinary users cannot compete with professional market makers in terms of expertise and market sensitivity.

Everyone is a market maker; we need to reinterpret this slogan: anyone can become a market maker, but not everyone can be a good market maker.

The Collapse of Leading Market Makers: After the Market Loses Liquidity

Market Makers in the Domino Effect

The collapse of the FTX empire has severely impacted a series of leading platforms, with market makers and lending becoming the hardest-hit areas: Alameda, as one of the largest market makers in the cryptocurrency industry, perished in this farce and officially ended trading on November 10; DCG's market maker and lending company Genesis, due to the FTX explosion, suspended redemptions and new loan issuance in its lending department due to insufficient repayment ability, while seeking $1 billion in emergency loans from investors.

As a key link in the domino effect, what impacts do market makers bring:

1. Significant Decline in Market Liquidity

The FTX explosion event—collapse of market makers—liquidity shortage. With the disappearance of leading market makers, it is expected that market liquidity will decline significantly. Other market makers will also suffer more losses due to FTX's collapse, further expanding this shortage. A harsh reality corresponding to this is that cryptocurrency liquidity is dominated by only a few trading firms, including Wintermute, Amber Group, B2C2, Genesis, Cumberland, and Alameda. And it has only been half a year since the Three Arrows Capital crisis in May and June. When the market is once again shrouded in shadow, market making becomes extremely difficult.

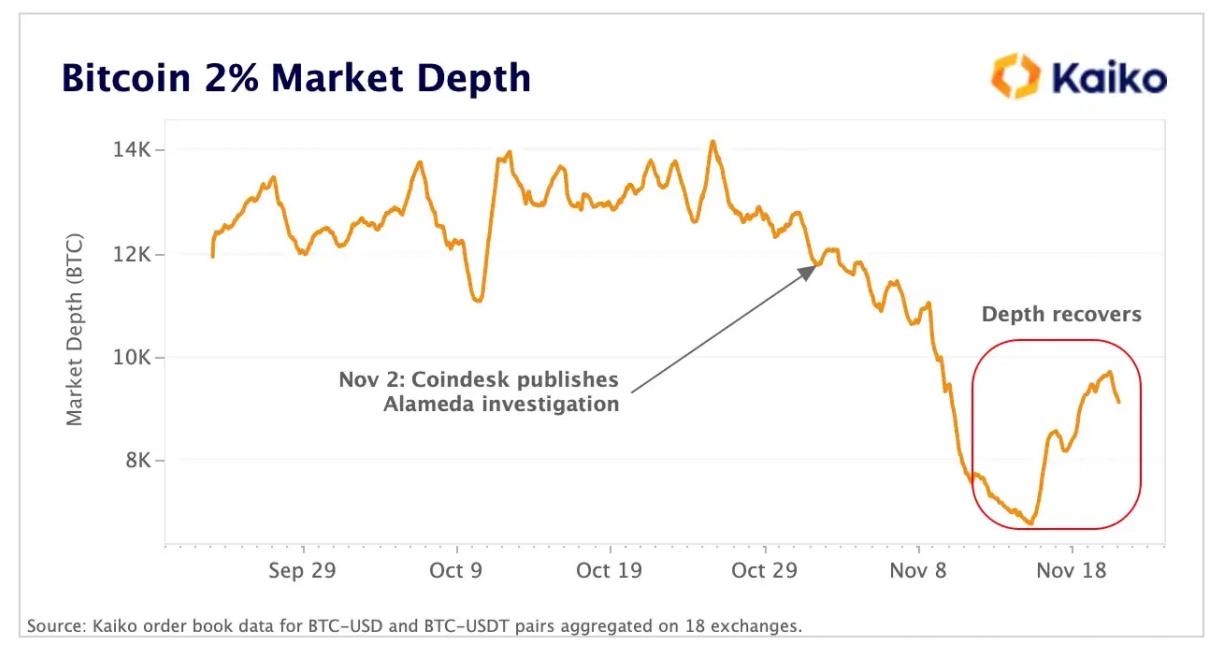

According to Kaiko's data, since CoinDesk published its investigation into Alameda's asset situation, the liquidity of BTC within a 2% midpoint has dropped from 11.8k BTC to 7k, the lowest level since early June. In this article, there are many data points indicating that the overall market liquidity has been significantly impacted by Alameda's collapse and the losses suffered by other market makers.

Fortunately, liquidity has slightly rebounded over the past week, indicating that market makers are redeploying capital. But it is evident that this pace is very slow.

The total amount of BTC within a 2% midpoint has increased from 6.8k to 9.1k. In dollar terms, market depth has increased from $112 million to $150 million

Source: Kaiko

2. Token Liquidity and Pressure Testing for Projects

Alameda invested in dozens of projects, holding low liquidity tokens worth millions of dollars (since Alameda is also a market maker, they are also the main liquidity providers for these tokens). Although it is currently unclear about all the details of the tokens held by Alameda and FTX, according to the detailed FTX balance sheet provided by the Financial Times, "this is a market maker of systemic importance." Especially for token liquidity outside of BTC and ETH, the extreme market conditions brought about by the collapse undoubtedly serve as a massive pressure test for these projects.

For example, one of the heavily invested tokens by Alameda is SOL (Solana). According to a CoinDesk report, Alameda held approximately $1.2 billion worth of SOL tokens on June 30. SOL was one of the best-performing tokens in the 2021 bull market, but it has now dropped 95% from its historical peak.

A collapse of this scale: first, it brings liquidity tightening and poses risks to the DeFi ecosystem through large-scale liquidations, which could lead to bad debts for lending protocols; second, it causes a collapse of confidence, leading to a large outflow of staked tokens, increasing the likelihood of interruptions that bring stability and security risks, and lowering the cost of network-level attacks.

Within a few weeks after the implosion of FTX and Alameda, SOL plummeted from around $35 to about $11, a decline of 68.5%

Source: TradingView

3. The Dual Collapse of Confidence and Trust

More importantly, the dual collapse of confidence and trust.

Confidence: The "black swan" event has shaken the industry's confidence in so-called high-performance public chains, and to some extent destroyed users' and supporters' confidence in a series of ecological projects under FTX. Confidence is worth more than gold, and fear is more terrifying than hell. The cryptocurrency market has experienced two Lehman moments within six months, the Luna/Terra and Three Arrows Capital events, teaching users what uncertainty is and bringing a panic sentiment to the cryptocurrency market that spreads faster than a virus.

Trust: In the collapse of Alameda, we can see how this industry's top market maker operated frantically, for example, their entire trading business was improperly mixed with customer funds by FTX. However, investors and project parties had no way of knowing this. Of course, this is the trust that CeFi has been asking the public to relinquish from the beginning, but when a once reputable, well-backed, and large-scale market maker reveals its naked ugliness, you still feel the disillusionment of trust in the crypto world. Despite our repeated statements: FTX / Alameda ≠ Blockchain.

When the Market Loses Liquidity

As mentioned earlier, liquidity is the driving force behind any market.

When the overall market trend declines, the withdrawal of leading market makers undoubtedly exacerbates the situation, meaning that more projects and investments tend to slow down, thus creating a vicious cycle (until the fundamentals recover):

Market slows down---liquidity drops, or a major crisis occurs---sharp one-sided market conditions---market making activities decline---trading volume and investment activities decrease---liquidity drops---market slows down

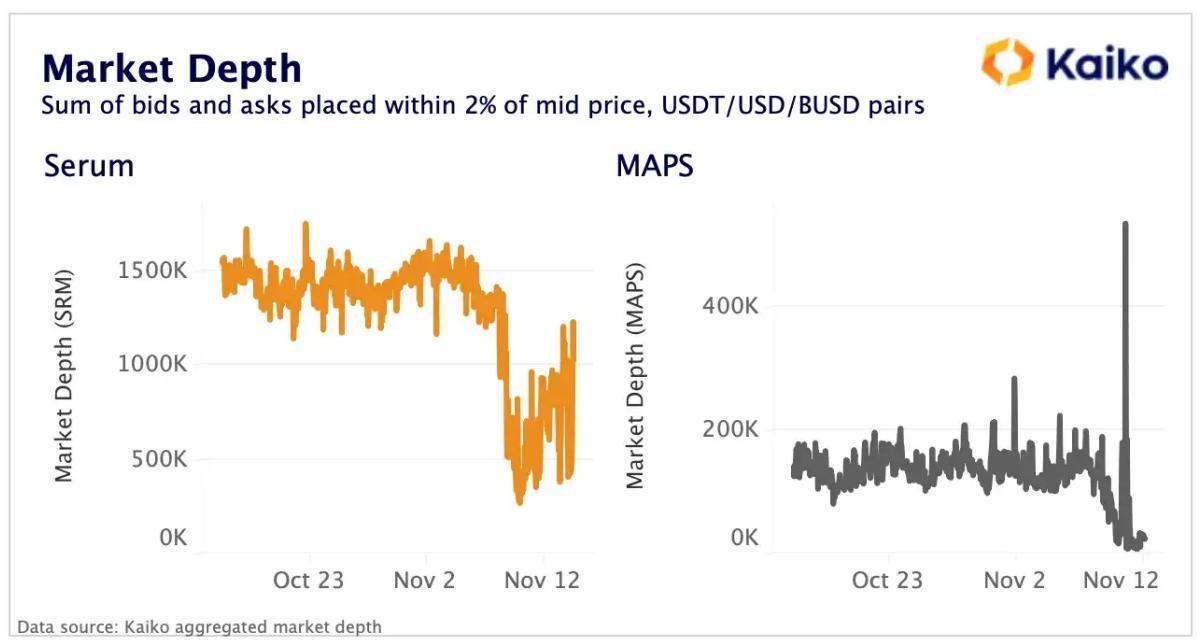

The depth of SRM and MAPS has also seen a significant decline, with market making activities affected by Alameda

Source: Kaiko

To maintain liquidity in the cryptocurrency market, many market makers provide liquidity to blockchain exchanges and financial protocols. Therefore, in the absence of market making or a sharp reduction in market making activities, there may be situations of low trading volume and reduced investment. Here we need to distinguish: liquidity may normally decrease during volatility because market makers are withdrawing sell/buy tasks from the order book to manage risks and avoid bad liquidity; but a sharp decline caused by major crisis events and the withdrawal of market makers will pose severe challenges to market liquidity for a period of time.

It can be seen that the current liquidity decline is more severe than in any previous market downturn, and the market's recovery during the bear market is also extremely slow, indicating that this liquidity shortage may persist in the short term.

So what should be done?

How DODO Meets Market Making Demands

As mentioned earlier, we have primarily raised two questions:

When AMMs are optimizing towards concentrated liquidity, and becoming an LP for market making may turn into a challenging or even losing endeavor, how can market makers earn profits?

When the FTX explosion leads to the collapse of leading market makers and a decline in market liquidity, how can trust be rebuilt, truly utilizing the decentralized nature of the crypto world to bring much-needed liquidity to projects? How can market makers achieve true permissionless and highly efficient transparency?

Regarding the second question, the answer is already self-evident: Use DEX, Use Blockchain. Let’s return to the chain, return to the code, return to "don't trust, verify."

Regarding the first question, there are already many protocols or platforms in the market providing corresponding liquidity management tools to help LPs manage risks and stabilize earnings. Here we might provide a solution from DODO: bringing professional market makers on-chain.

In an interview with DODO market makers, how to improve market making efficiency using DODO, market maker Shadow Labs mentioned that after deducting gas and other fees, they can achieve a net profit of 30-40% from publicly available on-chain earnings. For example, in the DODO WETH and USDC market maker pool, after deducting various fees, the year-to-date net earnings for market makers reached $500,000, with a net profit margin of approximately 36.2%.

How is this achieved?

It is well known that AMMs are often referred to as "lazy liquidity" because the price points provided to traders cannot be controlled, unlike traditional market makers who have more understanding and flexibility. This is precisely where DODO intervenes, pioneering the PMM (Proactive Market Making) algorithm. The PMM algorithm adjusts the pricing curve using price predictions, with simple yet flexible parameters, effectively improving capital utilization, reducing trading slippage and impermanent loss. For more information on how different algorithms enhance the efficiency of concentrated liquidity, you can refer to this article.

Beyond these familiar aspects, we want to discuss DODO's V2 version launched in March this year, which introduced DODO Private Pools (DPP), also known as private pools, specifically designed for professional market makers.

Private pools, as the name suggests, allow market makers to independently market with their own capital and flexibly modify the private pool configuration during the market making process, including transaction fee rates, current external reference prices, curve slippage coefficients, and also support adjustments to the pool's capital scale. All modifications are triggered by relevant accounts calling smart contracts (including two methods: invoking the DODO DPPProxy contract and directly calling the underlying private pool for market making modifications; specific operational steps can be referenced in the DODO V2 Private Pool Operation Instructions). Therefore, this pool mainly meets the market making needs of professional market makers.

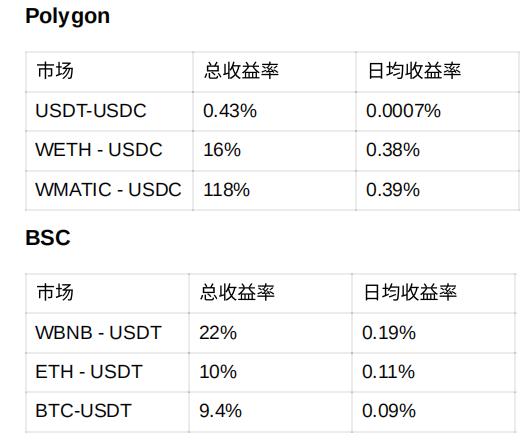

In terms of yield performance, according to DODO's data statistics, the total yield for market makers in the WETH-USDC pool on Polygon is 16%, and the total yield for market maker pools on BSC (launched at the end of July) has reached 10% to even 22% over the past four months, which is quite considerable.

*Currently, there are no DPP pools on Ethereum, and most market makers choose to build pools on Polygon and BSC chains where gas fees are lower.

Additionally, an article analyzing the comparison of Uniswap V3, Curve V2, and DODO market making algorithms has demonstrated the improvement in capital efficiency brought by concentrated liquidity through liquidity distribution data.

By selecting the WETH/USDC market maker pool as a sample, the article shows the average liquidity ratio within price ranges of 2%, 6%, and 10%. The liquidity ratio of DODO V2's market maker pool within the 2% range reaches 83.1%.

Bringing professional market makers on-chain, because decentralized exchanges are inherently trustless, non-custodial, and permissionless, is the direction for future trading and market making. However, due to cost and efficiency issues, solutions based on the AMM framework have made slow progress in this regard.

DODO's PMM algorithm and DPP private pools provide professional market maker teams with highly flexible market making curves, reducing market making costs, improving capital efficiency, and delivering an efficient market making experience; in a market environment with declining liquidity, it also offers projects a better collaboration choice.

Reference

https://foresightnews.pro/article/detail/5995

https://twitter.com/0xUnicorn/status/1592007930328776706?

refsrc=twsrc\^tfw|twcamp\^tweetembed\&refurl=https%3A%2F%2Fwww.notion.so%2Fbe02a02105b5470e83fff8f06425e298

https://twitter.com/NateHindman/status/1457744185235288066?s=20\&t=jb-YsLK25pE8GuHZaMAudg

https://medium.com/wintermute-trading/the-good-the-bad-and-the-ugly-of-crypto-market-making-hacker-noon-c0c4fd55263a

https://www.chaincatcher.com/article/2062401

https://www.notion.so/dodotopia/Uni-V3-CurveV2-DODO-4bb203cb20654a058482e59ce2fddb62

https://dodotopia.notion.site/DODO-DODO-97a9cbbaa925431d88f110754446cdf9

https://rekt.news/uniswap-v3-lp-rekt/

https://www.coindesk.com/business/2022/11/09/who-still-has-exposure-to-ftx/

https://blog.kaiko.com/crypto-liquidity-in-a-post-alameda-world-5fb2c190f0b

https://newsletter.banklesshq.com/p/is-solana-dead

Risk warning

Risk warning Risk warning

Risk warning

Popular articles