Mint Ventures: A Review of the Development of the NFT Sector in 2022

After the frenzy and bubble of NFTs gradually fade, people will pay more attention to the real significance brought by their non-fungibility. Utility and surrounding ecosystems will become the strategic focus of project teams, with NFTs serving as the core carrier.

After the frenzy and bubble of NFTs gradually fade, people will pay more attention to the real significance brought by their non-fungibility. Utility and surrounding ecosystems will become the strategic focus of project teams, with NFTs serving as the core carrier.Author: Jessica Shen, Mint Ventures

## I. The NFT Market in 2022

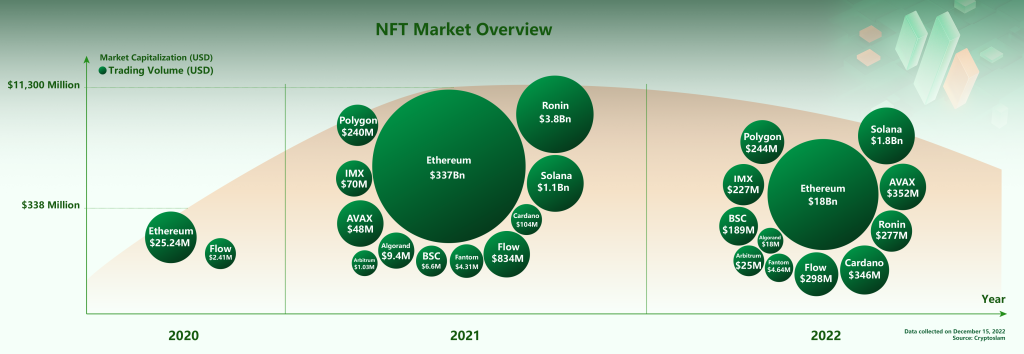

NFT Trading Volume and Market Value from 2020 to 2022

From 2020 to 2022, the NFT industry underwent many changes in just two years. In the eyes of many, NFTs in 2020 were merely a conceptual idea, but by 2022, the asset and financial attributes of NFTs had become deeply ingrained. From the perspective of trading volume, we have the following observations about NFTs:

The overall market value of NFTs grew rapidly in 2021, but trading volume plummeted during the bear market in 2022

The explosive popularity of PFPs on Ethereum in 2021 marked the beginning of the NFT era, but this year, NFT trading volume on Ethereum has decreased by more than tenfold.

NFT assets on various public chains gradually exhibit distinct characteristics

NFTs began with NBA Top Shot on Flow in 2020 and Axie Infinity on Ethereum at that time. By 2021, NFT assets flourished across various public chains, with a strong focus on Ethereum, where PFP assets with significant cultural and artistic attributes led the trading and opened up industry imaginations for the future of NFTs. In 2022, affected by the bear market, the NFT market cooled down, with trading volume on Ethereum dropping nearly 95%. However, PFP trading on Ethereum remained the main theme of the industry, while NFT trading on public chains like IMX, BSC, Solana, and Polygon, which host many GameFi and SocialFi ecosystems, remained relatively active.

From the perspective of public chains

- Ethereum and Solana continue to lead NFT trading. Ethereum and Solana maintain their lead in NFT trading volume, with both being active in PFP trading. However, frequent outages on Solana have limited the development of its ecosystem, and the loss of user confidence has impacted its on-chain NFT trading.

- The limitations of the NFT OG public chain Flow are becoming apparent. The established NFT public chain Flow, which used NBA Top Shot to educate the industry about NFTs, saw its trading volume drop to less than $300 million by 2022, with its NFT ecosystem still revolving around sports cards.

- Polygon is undoubtedly becoming the most promising NFT public chain. With its lower costs, relatively stable performance, and EVM compatibility, Polygon has become the preferred public chain for many brands and influential figures, including Starbucks Odyssey, Donald Trump Digital Trading Card, and Reddit Avatar. The highly anticipated social protocol Lens Protocol's NFT is also based on Polygon.

The explosion of the NFT industry mainly relies on content; art and creation are the soul elements of NFTs at this stage. The market has recognized the cultural attributes carried by NFTs and the expectations for future ecological development through real transactions, granting many PFPs high valuations. After the issuance of NFTs, the model of building ecosystems around them has gradually formed a mainstream approach in the industry. A few projects that established ecosystems before issuing NFTs have a stronger user base, while NFTs without ecosystems have also garnered significant user attention in a short time. As the frenzy and bubble around NFTs gradually fade, people will pay more attention to the real significance brought by their Non-Fungibility, and utility and surrounding ecosystems will become strategic priorities for project parties, with NFTs serving as the core carrier. Compared to PFPs with strong consumption attributes, NFTs with practical value have better liquidity and a stronger ecological foundation, which is why these types of NFT assets can grow against the trend during the bear market.

## II. The NFT-Fi Market in 2022

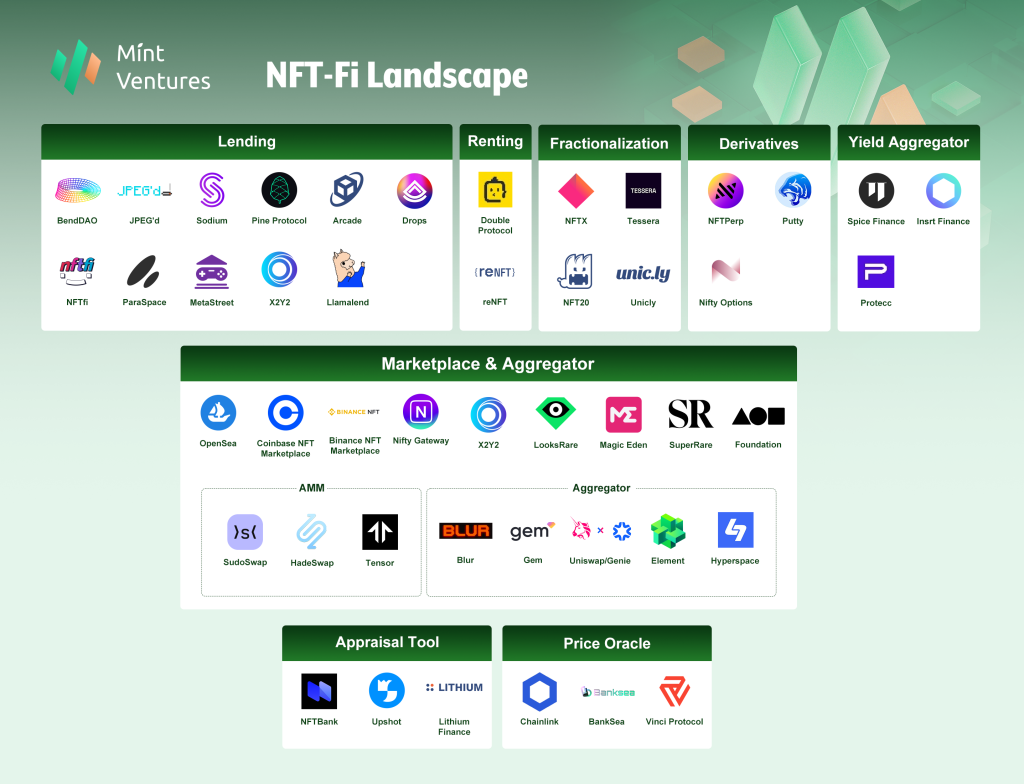

NFT-Fi Track Landscape

NFT-Fi Track Landscape

Compared to the NFT industry landscape in 2021, the NFT market landscape in 2022 underwent subtle changes. Some promising tracks did not see much progress, while others unexpectedly saw many new players entering the competition. Here are several trends we observed in 2022:

Competition in trading markets is fierce and increasingly user-centric

From trading fees, various token reward subsidies, discussions about royalty rules, to innovations in AMM mechanisms, the refresh frequency of aggregators, and multi-chain deployments by various trading markets, we continuously see NFT trading markets and aggregators making ongoing attempts and explorations to better serve users. Although some have succeeded and others have failed, OpenSea remains the platform with the largest user base and highest trading volume, but we also see the emergence of Blur, which has received positive reviews and welcome from professional NFT traders. This new entrant seems to have the opportunity to disrupt the existing landscape.

The aggregator business is challenging

In 2022, multiple NFT trading aggregator platforms emerged in the industry, but in terms of trading volume, the two early entrants, Gem and Genie, did not achieve impressive results. As trading platforms engage in fierce competition, the market demand and profit model for aggregators have faced some skepticism.

NFT lending is flourishing

A wave of BAYC and MAYC purchases triggered by Yuga Labs' airdrop in the first half of 2022 made NFT lending protocols a leverage tool for some players. Subsequently, when the Ape Staking feature was launched at the end of December, several lending protocols introduced pairing functions and staking yield pools, attracting many users to participate. In 2022, NFT lending emerged as the area with the most new competitors in the NFT-Fi sub-track, compared to the more fragmented, futures, and options products that are relatively mature.

Fragmentation protocols remain lukewarm

Although everyone understands that making non-fungible tokens fungible is a way to improve liquidity, fragmentation protocols in the NFT-Fi track have not successfully injected liquidity into the industry as hoped. Early participants in fragmentation, such as Niftex, have ceased operations, and Fractional.art has rebranded to Tessara this year to reorganize its business. Other fragmentation protocols are also lukewarm and have not become the liquidity valves for NFTs as anticipated.

NFT-Fi liquidity pools are gearing up

The development of first-layer NFT-Fi protocols such as lending, fragmentation, and derivatives has yet to form a clear pattern, but the liquidity pool business based on these yield-generating protocols is preparing for a sprint. Projects like Spice Finance, Insrt Finance, and Protecc are all targeting this untapped territory, waiting for the NFT-Fi explosion to provide more convenient and user-friendly products for end users. However, the liquidity pool business heavily relies on first-layer NFT-Fi/DeFi protocols and requires the ability to quickly capture market opportunities, adjust strategies in a timely manner, and update products. Additionally, considering that the overall market for liquidity pools in the DeFi space accounts for less than 5% of DeFi protocols, we must ponder how the NFT-Fi liquidity pool market can achieve breakthroughs.

Risk warning

Risk warning Risk warning

Risk warning