What new strategies do the four major established DeFi protocols have, and what synergistic effects will they bring?

These early DeFi protocols seem to operate independently, yet they create synergies that further advance the field.

These early DeFi protocols seem to operate independently, yet they create synergies that further advance the field.Author: Chinchilla

Compiled by: The Way of DeFi

Some projects have brought the spark of DeFi to us.

Now, for various reasons, they have begun to innovate within this ecosystem.

What kind of changes will these innovations bring to the field?

The article will mention:

・Aave GHO

・Synthetix V3

・Curve CrvUSD

・MakerDAO Stark Protocol

These early DeFi protocols seem to operate independently, yet they create synergies that push the field forward once again. They have all successfully captured their market share. While they are all launching new features, they can benefit from each other.

According to data from DefiLlama.com, the total value locked (TVL) in DeFi is approximately $50 billion.

The above protocols account for a significant portion of this:

・MakerDao $7.23 billion;

・Curve $4.94 billion;

・Aave $4.81 billion;

・Synthetix $444 million.

Although Synthetix's locked amount is much smaller, together they account for about 35% of DeFi TVL.

Aave

After the V3 upgrade on the mainnet, Aave has just launched the long-awaited stablecoin $GHO on the testnet.

This is an over-collateralized stablecoin backed by multiple crypto assets. It is minted through a basket of volatile or stable assets via its Facilitators.

Its interest rates are not influenced by supply and demand but are determined by the Facilitators and the DAO.

$AAVE stakers receive borrowing discounts, which may still lead to buying pressure.

But my aim is to highlight the improvements in capital efficiency with V3.

This is thanks to "E-mode," which allows users to have higher collateralization (higher LTV - loan-to-value ratio) when borrowing tokens related to their collateral.

This means users can borrow more funds by reducing their collateral.

Indeed, this mechanism can only be implemented for related token pairs. For example, stablecoins have their own volatility/correlation.

But that is not the whole story.

Additionally, as shown in the image below, Aave can enhance the overall system's liquidity alongside well-known projects.

Synthetix

This protocol has the smallest TVL/market cap ratio among the several DeFi projects mentioned in the article.

But we should not forget that it was one of the first protocols to discuss decentralized derivatives. Its contributions are significant, though it has not met initial expectations.

However, market catalysts and new versions may drive it to regain market share and re-establish its position from three years ago.

For instance, let's not forget that its stablecoin $sUSD is used in some mainstream protocols.

But the most interesting aspect of Synthetix is the recently released V3.

This is the team's attempt to build a seamless permissionless derivatives platform.

With this major upgrade, the protocol will now introduce:

・The possibility of creating existing financial derivatives - whether they are based on crypto or TradFi. This includes commodities, stocks, etc.;

・Enhancing market liquidity by allowing other protocols to source and route market liquidity from the Synthetix platform;

・Simplifying staking by implementing new mechanisms regarding debt pools and collateral types.

As the Synthetix team states, the purpose of these changes is to achieve permissionless asset creation, "liquidity as a service," and better control over staker credit.

Curve

This industry giant has always been a leader in providing deep liquidity and efficient swaps while maintaining low fees and slippage.

Now, it aims to solidify its position by launching the stablecoin $crvUSD.

This over-collateralized stablecoin comes with some impressive innovations, such as:

・LLAMA, which will provide a continuous liquidation mechanism for debt positions to prevent losses from market volatility.

・$ETH and LP collateral (possibly tricrypto2 and 3 pool).

Additionally, recent news suggests that there may be a higher LTV for collateral (debt positions).

This would mean users can maximize capital from their collateral while reducing concerns about liquidation.

The system's liquidity would also be stronger.

MakerDAO

In terms of TVL, this is the second DeFi protocol after Lido.

Although the tokenomics of $MKR and the collateral of $DAI may spark intense debate, MakerDAO has spawned one of the most widely used ecosystems in cryptocurrency.

Now it is expanding.

Maker's "growth-focused branch" Spark Protocol will launch in April.

Interestingly, it is built on top of Aave V3.

Thanks to Maker's credit line, users will be able to borrow $DAI at a very low interest rate (currently 1%).

Moreover, Spark Protocol will collaborate with fixed-rate protocols to provide this important tool.

In TradFi, the TVL of such markets is about $450 trillion, while cryptocurrency still lags behind due to its nascent lending mechanisms and volatility.

Additionally, Maker will launch its own synthetic asset $ETH, called $EtherDAI.

Spark Protocol will help create more demand by offering its liquid staking derivative $sEtherDAI.

In summarizing the innovations of these veteran DeFi projects, I want to emphasize that these projects all aim to grow their businesses by sharing liquidity and infrastructure with other protocols.

・Aave governance is discussing locking all their $CRV to directly release into the $GHO pool;

・Spark will return 10% of the $DAI market profits to AaveDAO.

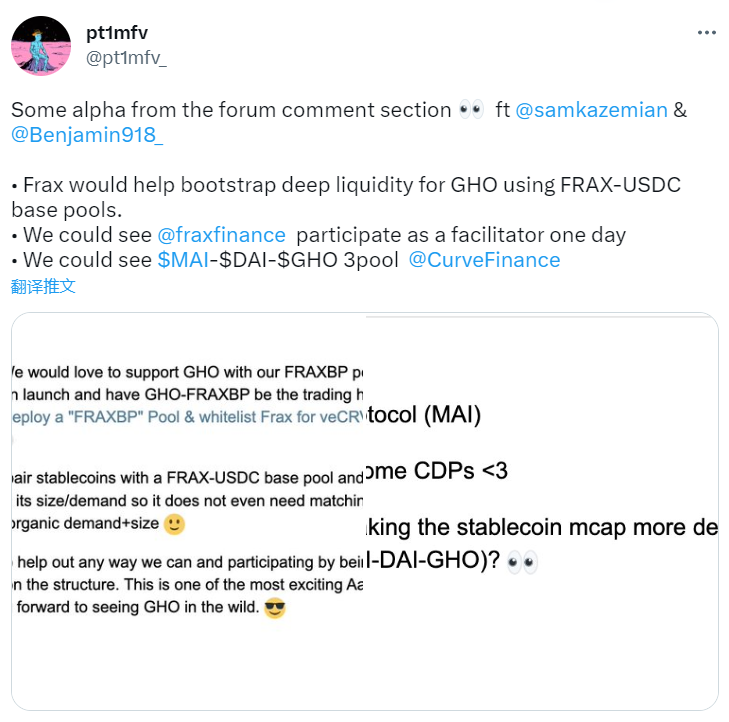

・Additionally, as I mentioned earlier, Frax Finance has announced it will help guide deep liquidity for $GHO.

・Synthetix aims to become a liquidity hub for derivatives.

Clearly, all these actions are not driven by empathy but by development.

Nevertheless, collaboration and mutual assistance can still yield overall + EV (positive expected value).

This has been the spirit that has consistently driven DeFi forward.

But why are they building different stablecoins?

At this point, I agree with @DefiIgnas. In fact, I believe these projects have different goals. Their stablecoins also serve different purposes.

For example, $crvUSD can help Curve improve capital efficiency while also increasing the liquidity of other stablecoins.

Meanwhile, $GHO may primarily serve as a tool to increase Aave's liquidity.

While Spark could become a tool to increase the adoption rate of $DAI in DeFi.

Thus, while I do not favor capital fragmentation, I am very curious about how these projects will develop synergistically.

Risk warning

Risk warning Risk warning

Risk warning