Silicon Valley Bank's stock price plummeted by 60%. What happened behind this?

The progress of this event depends on many factors, such as whether SVB will face a more severe run on the bank or even go bankrupt.

The progress of this event depends on many factors, such as whether SVB will face a more severe run on the bank or even go bankrupt.Original author: @Degg_GlobalMacroFin

1. Unprecedented Tech Bull Market

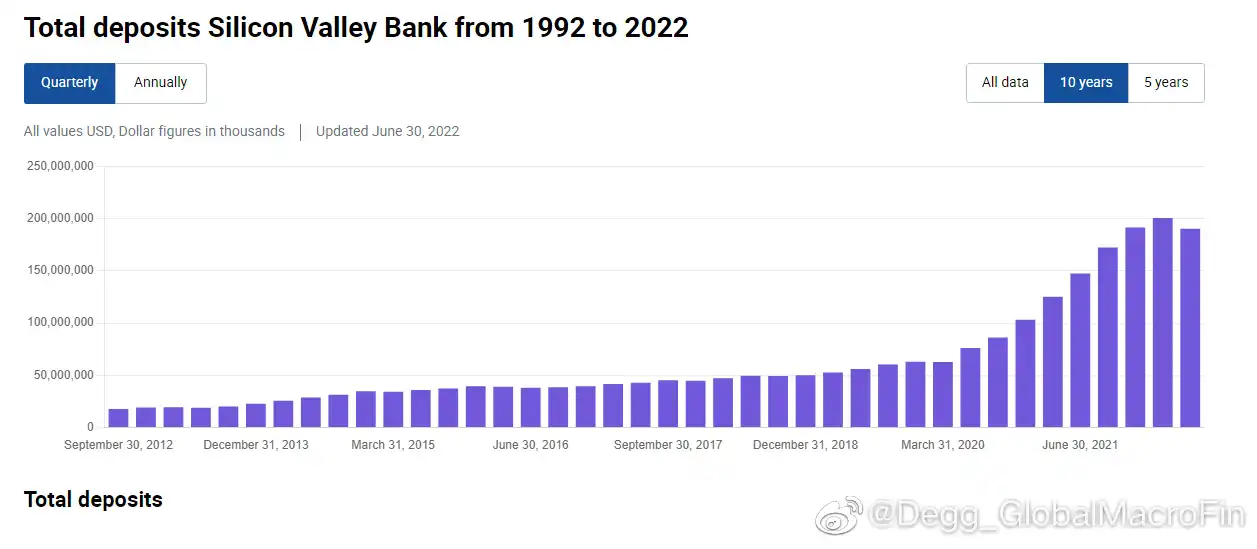

After the concerns about the pandemic faded in the second half of 2020, and with the Federal Reserve still committed to maintaining a 0% interest rate for a long time, quantitative easing continued, and inflation was nowhere in sight, the world welcomed a financing boom for tech companies. The rapid growth of loans and venture capital for startups led to a significant accumulation of cash and deposits in tech startups, much of which flowed into Silicon Valley Bank (hereinafter referred to as SVB), the most important bank in Silicon Valley and one of the top 20 banks in the U.S. From June 2020 to December 2021, SVB's deposits rose from $76 billion to over $190 billion, nearly doubling (Figure 1).

2. "Buying with Eyes Closed"

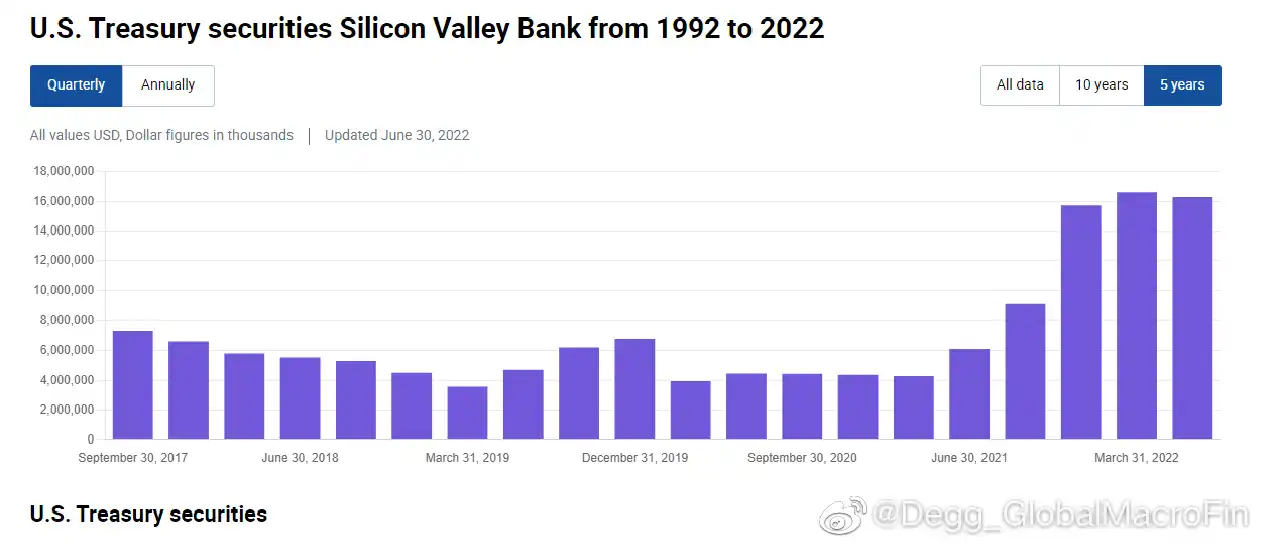

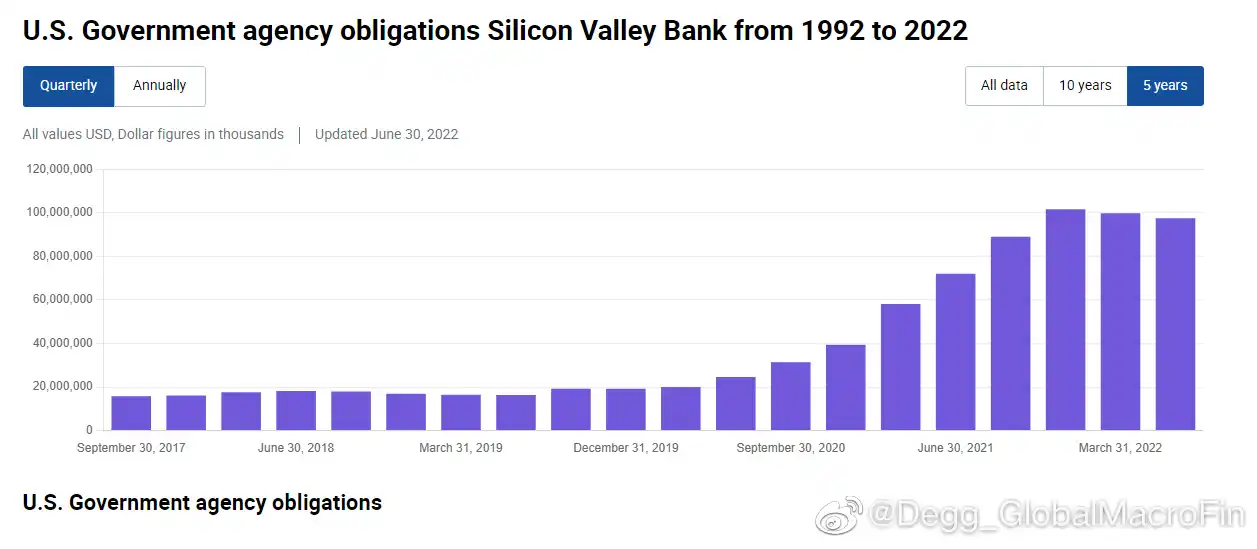

Faced with a massive influx of funds on the liability side, SVB's investable funds on the asset side also rose rapidly. Between 2020 and 2021, the Federal Reserve had not yet started raising interest rates, and keeping money in the Fed's reserve account yielded a meager annual interest of only 0.1%. SVB's choice was to buy a large amount of U.S. Treasuries and MBS. According to its 10-Q, from mid-2020 to the end of 2021, SVB increased its holdings of U.S. Treasuries by $12 billion, growing from $4 billion to $16 billion (Figure 2). More importantly, SVB increased its MBS holdings by about $80 billion, growing from over $20 billion to $100 billion (Figure 3). What does this mean? SVB's total assets were about $200 billion, which means it allocated half of its assets to MBS, or it considered that 70% of the over $110 billion in new deposits from 2020 to 2021 was allocated to MBS. This is almost unbelievable for a commercial bank primarily engaged in lending, even absurd.

3. "Cash is Trash"

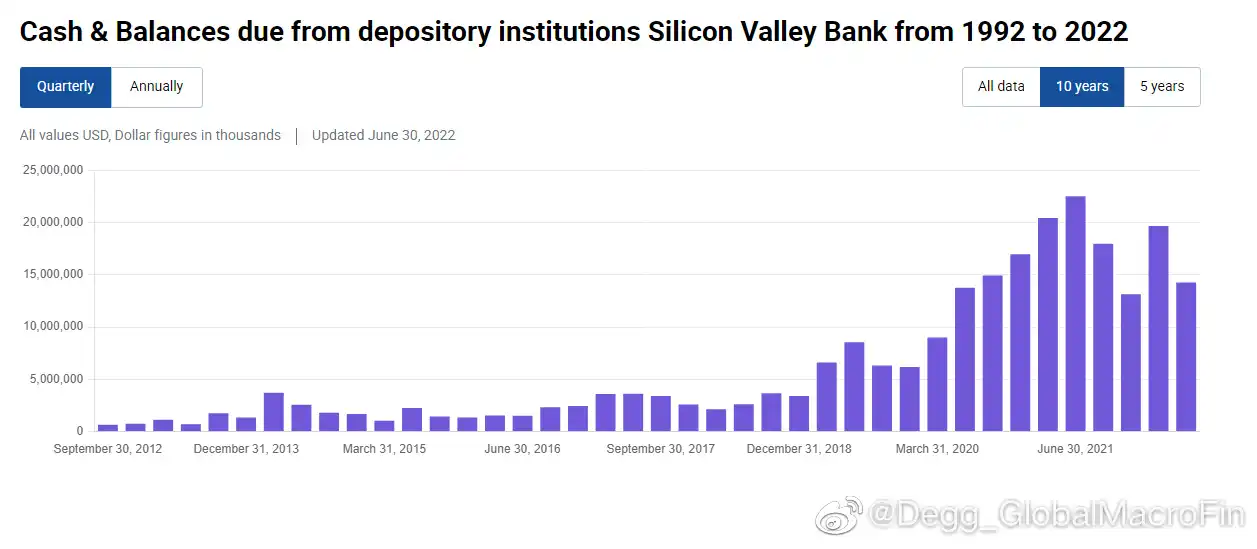

In contrast to the frenzied accumulation of MBS, the growth of cash and cash equivalents (including reserves, repos, and short-term debt) at SVB was not significant, rising from $14 billion to $22 billion from mid-2020 to mid-2021, and by the end of 2021, it even dropped to $13 billion, which was lower than the level in mid-2020 (Figure 4). This reflects that while SVB aggressively allocated long-duration assets, it did not reserve a proportionate amount of sufficient cash to cope with deposit outflows.

4. "Prudent" Accounting Treatment

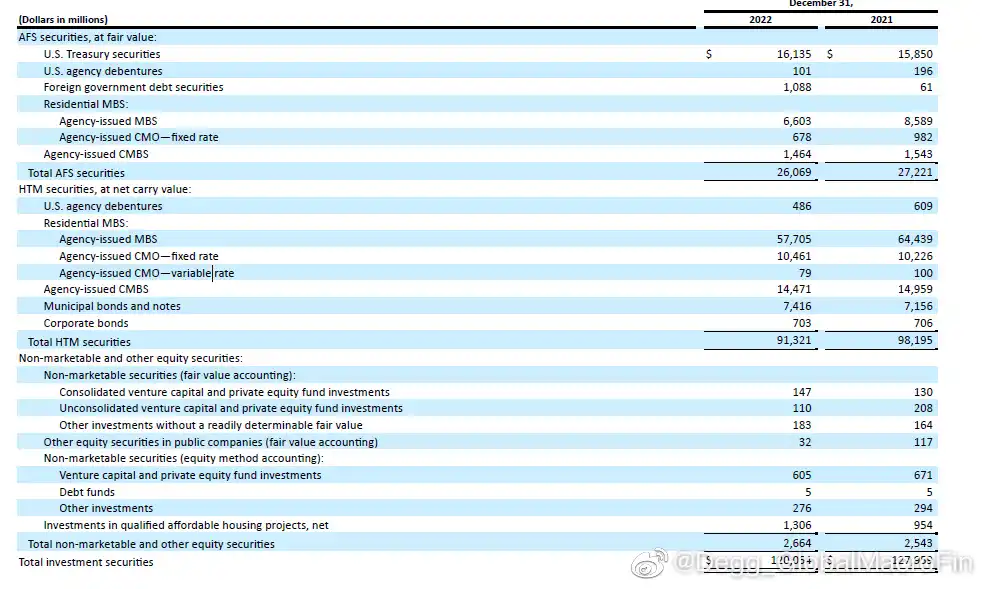

We know that commercial banks mostly account for fixed-income products as available-for-sale (AFS) and held-to-maturity (HTM). SVB is no exception. Its $16 billion in U.S. Treasuries is entirely measured as AFS, while the $100 billion in MBS is primarily measured as HTM (Figure 5). The advantage of AFS and HTM is that the market value (mtm) fluctuations of assets do not directly reflect in profit and loss, at most affecting the unrealized gains and losses under other comprehensive income (OCI), and can be reversed. However, the downside is that once AFS and HTM are forced to be sold, a profit or loss must be recognized in the current period.

5. Federal Reserve's Rate Hikes and Unrealized Losses

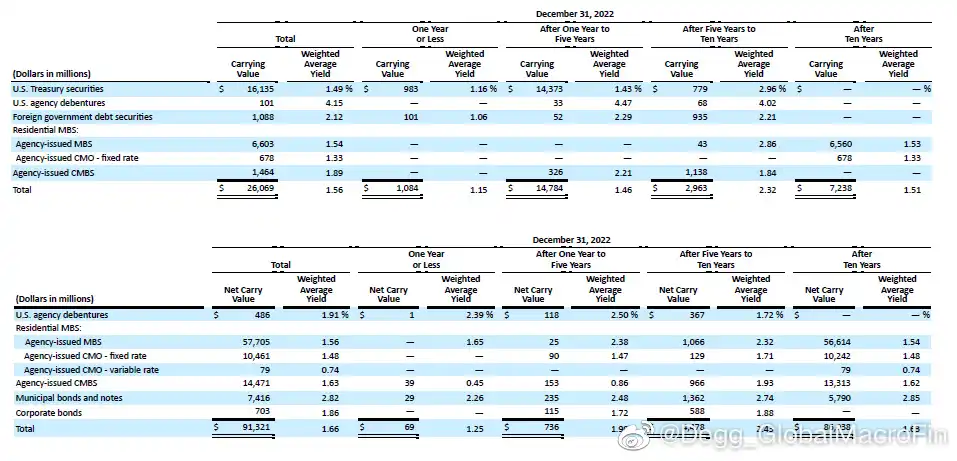

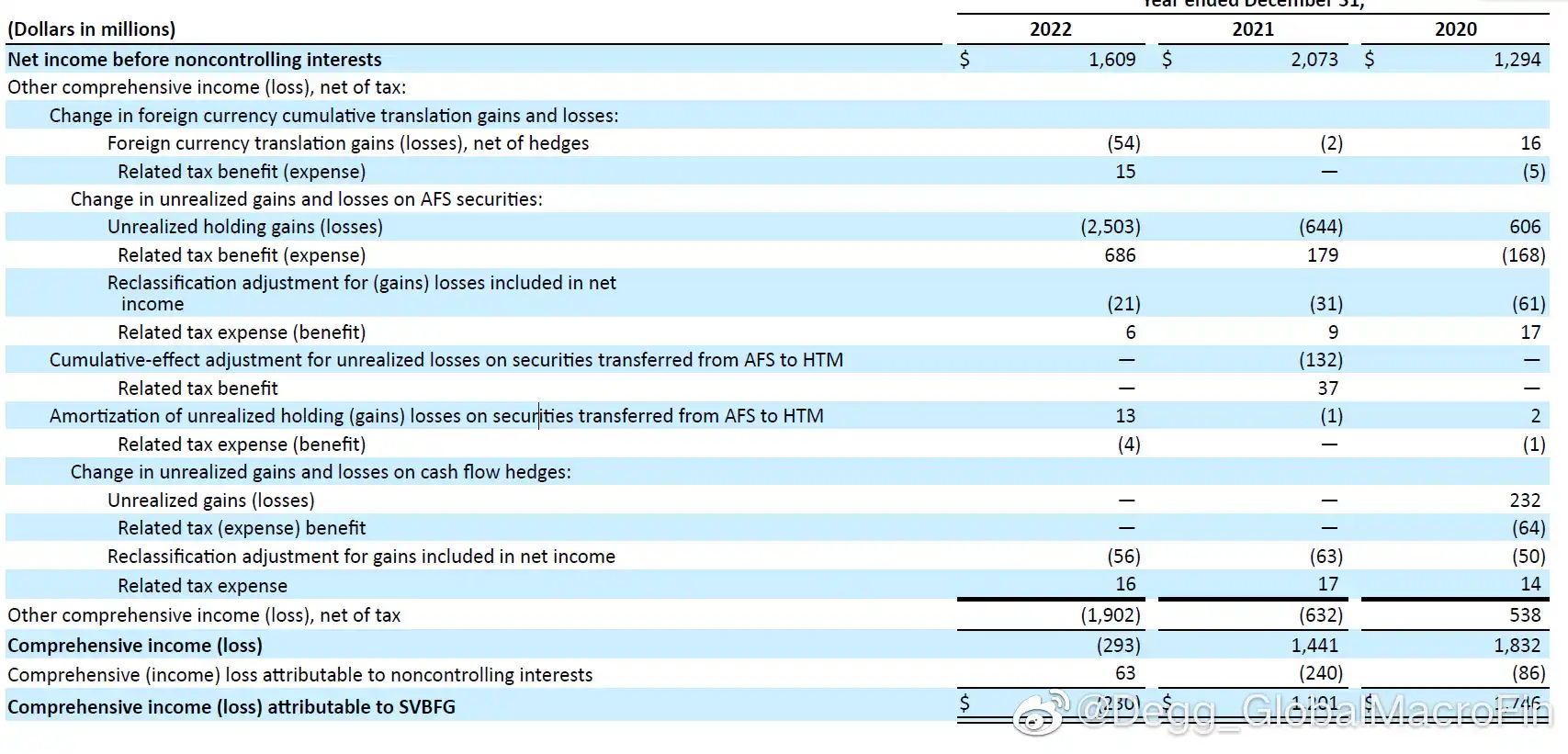

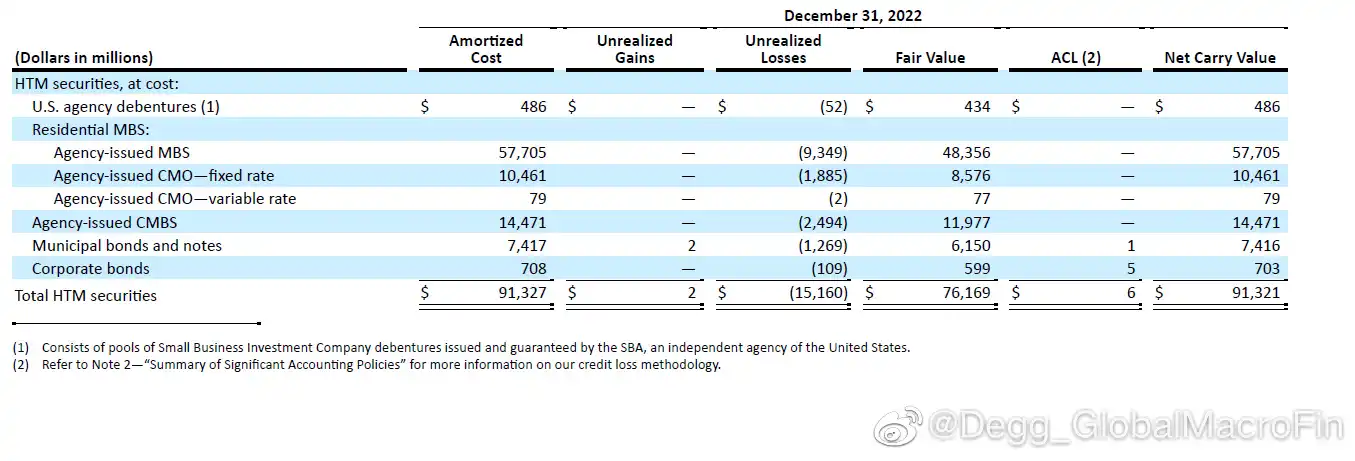

Since SVB's asset purchases were concentrated during the low-interest period of 2020-2021, the average yield of AFS and HTM assets was very low. According to the 10-K, the average yield of its AFS was only 1.49%, and the average yield of HTM was only 1.91% (Figure 6). With the Federal Reserve's rapid rate hikes in 2022, these low-interest AFS assets led to over $2.5 billion in unrealized losses for SVB in 2022 (Figure 7), and when considering the unrealized losses of the $100 billion in MBS measured as HTM, the total unrealized losses reached as high as $17.5 billion (with HTM unrealized losses of about $15 billion, Figure 8).

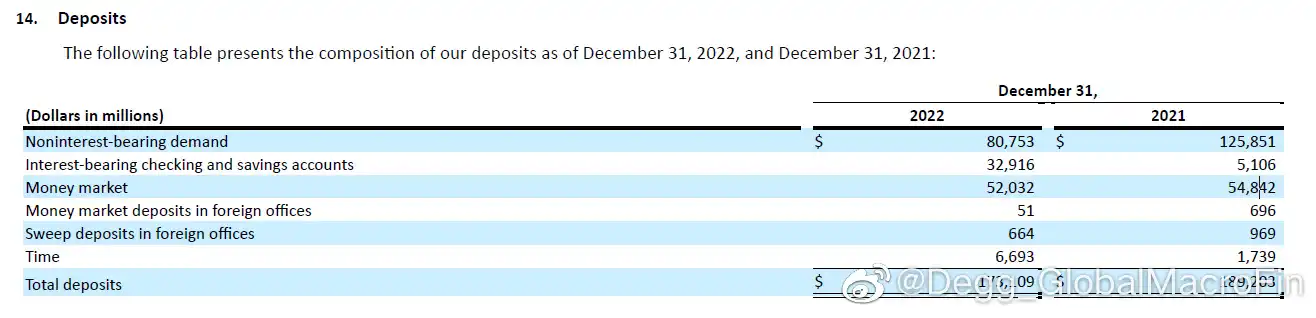

6. Deposit Outflows

These unrealized losses do not become actual losses as long as you do not sell, and are often viewed as "paper losses are not losses." The problem is that the rapid rate hikes by the Federal Reserve in 2022 made it difficult for global tech startups, which struggled to secure financing and saw their stock prices continuously decline, to continue their R&D, forcing them to deplete their deposits at SVB. Coupled with the Fed's balance sheet reduction and other factors, SVB's deposits have been flowing out since peaking in March 2022. The total deposits decreased by $16 billion throughout 2022, accounting for about 10% of total deposits, especially the non-interest-bearing demand deposits plummeting from $126 billion to $81 billion, significantly increasing the interest expense pressure on the liability side (Figure 9).

7. Negative Convexity of MBS

Specifically, when interest rates rise, homeowners are more willing to gradually refinance rather than prepay their loans, which extends the duration of MBS. This leads to the duration of the large amount of HTM MBS held by SVB becoming longer and increasingly difficult to cope with the continuous outflow of funds on the liability side. Therefore, since the end of last year, SVB has faced a situation where the asset side MBS has significant unrealized losses that cannot mature in the short term, while cash reserves are also not very ample; on the liability side, deposits have been continuously flowing out, and the cost of liabilities keeps rising.

8. Cutting Off the Arm?

SVB's management actually had some other options, such as borrowing in the repo market, seeking advances from FHLBs, or issuing bonds to meet the pressure of deposit outflows. But there are two problems. First, the current yield curve is severely inverted, with the cost of borrowing on the short end far exceeding that on the long end. Maintaining the HTM on the long end by borrowing on the short end would incur greater losses than directly cutting positions. Second, once startup deposits flow out, they are unlikely to return, so rather than using short-term borrowing as a stopgap, it is better to cut positions to reduce leverage—though this would lead to a sharp drop in stock prices in the short term, it would be the safest action in the long term. In this environment, a "cutting off the arm" approach may have already become the optimal choice.

9. Panic

When SVB announced it had sold $21 billion in AFS assets, resulting in an $1.8 billion loss, market panic manifested in several ways. First, would the $100 billion in HTM assets that had not yet been sold, corresponding to a $15 billion unrealized loss, turn into actual losses? It is worth noting that SVB's total market capitalization is only about $20 billion. Second, issuing a large number of shares would dilute the equity of existing shareholders, which is inherently negative. Third, most of SVB's clients are tech companies, which are not covered by deposit insurance, making it easy for a bank run to occur. Many tech executives expressed their intention to withdraw all funds from SVB within just 12 hours. Fourth, the market was unclear whether other banks with significant exposure to tech companies would face bank runs and whether this crisis would spread.

10. Outlook

The progress of this event depends on many factors, such as whether SVB will face a more severe bank run or even bankruptcy. In the coming days, at least two aspects can be observed to monitor the evolution of the crisis: one is whether the interbank market and repo market will worry about the overall financial condition of small and medium-sized banks? Will there be localized liquidity tensions? Observing whether the EFFR and SOFR 99% levels will rise significantly in the coming days. The other is to observe how the market views the risks associated with loans/assets related to tech companies, such as whether banks with significant exposure to tech companies will face serious bank runs? 99% of the panic regarding banks is FUD (fear, uncertainty, and doubt), but the remaining 1% of real panic can often evolve into a highly destructive financial crisis. Let the bullets fly a little longer.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles