2023 Q1 Cryptocurrency Investment and Financing Report: Market Overview, Popular Trends, and Performance of Investment Institutions | RootData

The number and amount of cryptocurrency financing this quarter have both hit a new low since 2021, but industry hotspots continue to emerge one after another.

The number and amount of cryptocurrency financing this quarter have both hit a new low since 2021, but industry hotspots continue to emerge one after another.Author: Xi Xiangxiang, Gu Yu, RootData

The first quarter of 2023 has just passed, and the feelings of those in the cryptocurrency industry are mixed. On one hand, several banks in the United States faced a crisis of bank runs, and regulatory agencies continued to crack down on centralized exchanges, impacting market confidence; on the other hand, cryptocurrency assets represented by BTC and ETH performed quite well in the secondary market. Besides price factors, we also believe that several signals within the cryptocurrency field are showing strong signs of recovery and growth.

So, how did the cryptocurrency investment and financing market perform in the first quarter of 2023? What are the hottest trends in the current market? What are the investment institutions' frequency and preferences? Rootdata conducted a comprehensive analysis based on platform statistical data. This report consists of three parts: Overview of the cryptocurrency investment and financing market in 2023Q1, analysis of investment and financing market trends, and performance of investment institutions.

1. Overview of the Cryptocurrency Investment and Financing Market in 2023Q1

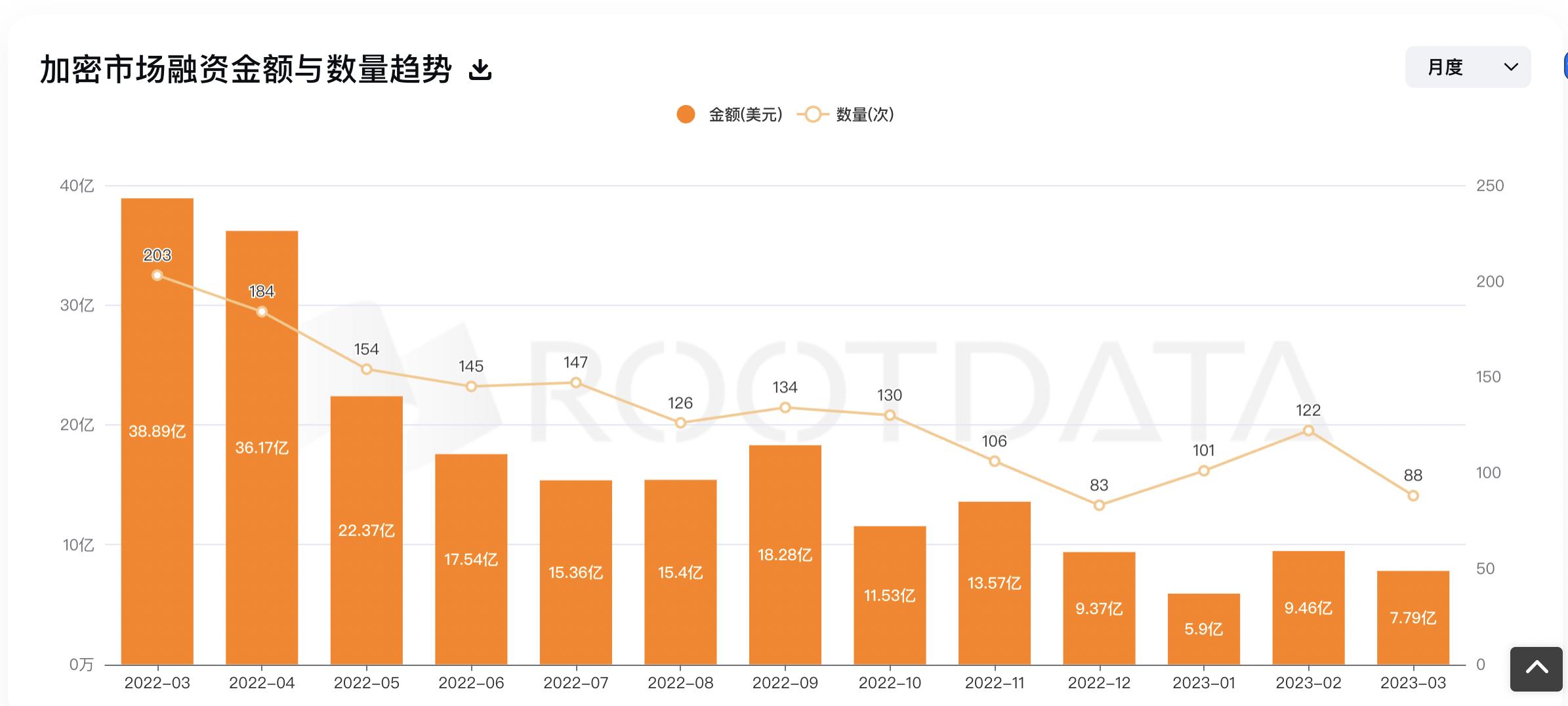

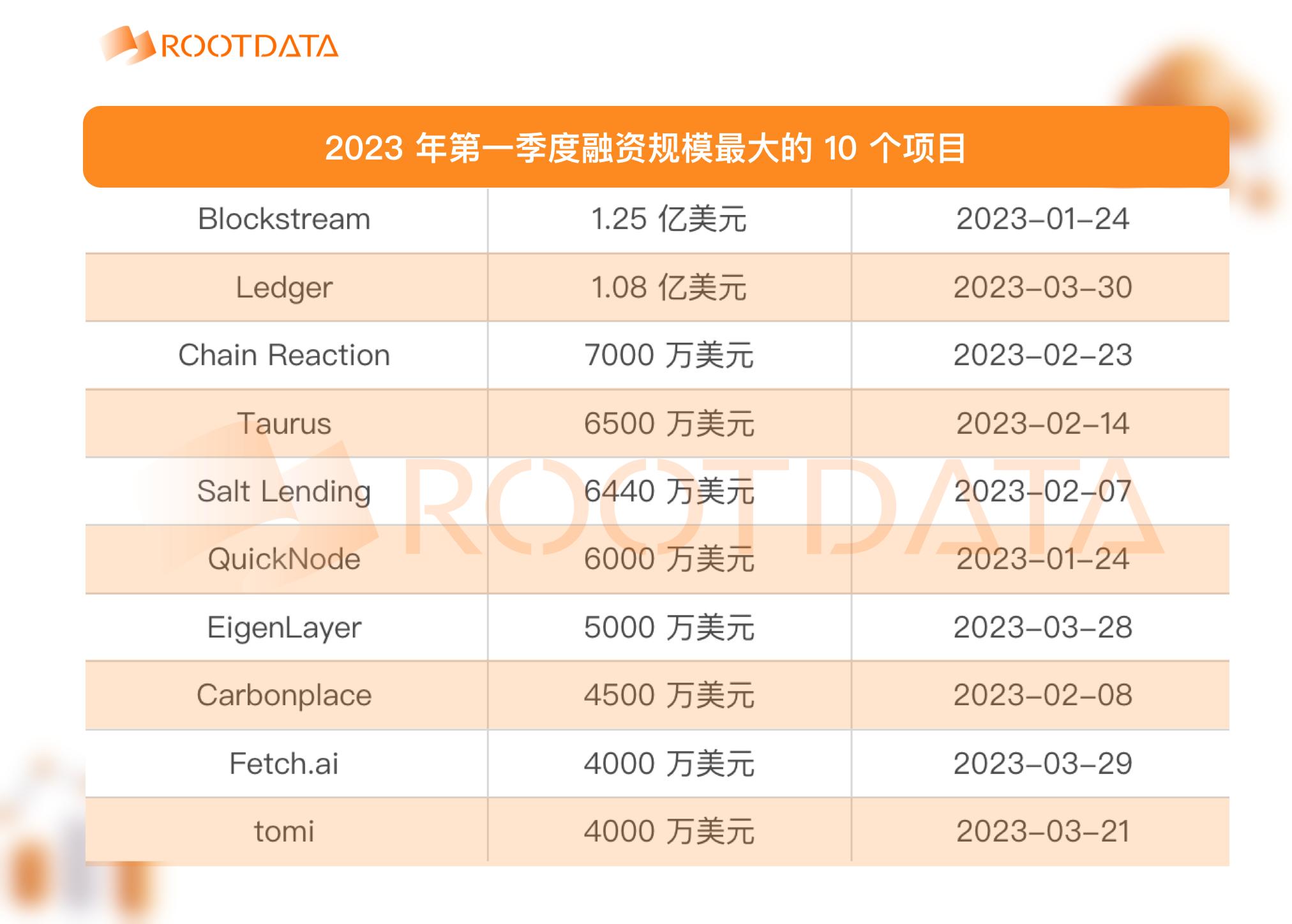

RootData data shows that from January to March 2023, the cryptocurrency industry disclosed a total of 309 project financing events, with a total financing amount reaching $2.317 billion, far lower than the $12.48 billion in the first quarter of 2022, a year-on-year decrease of about 81%. Compared to the $3.463 billion in the fourth quarter of 2022, there was also a significant decline, with a quarter-on-quarter decrease of 33%. In summary, both the number of financing events and the amount of financing in this quarter hit a new low since 2021.

It can be seen that after entering a bear market cycle, the financing rhythm in the primary market of the cryptocurrency industry has experienced a cliff-like drop, and investment institutions have been relatively cautious and have not actively engaged. On the other hand, many projects have seen valuation inversions between the primary and secondary markets, making the secondary market more favored by investors.

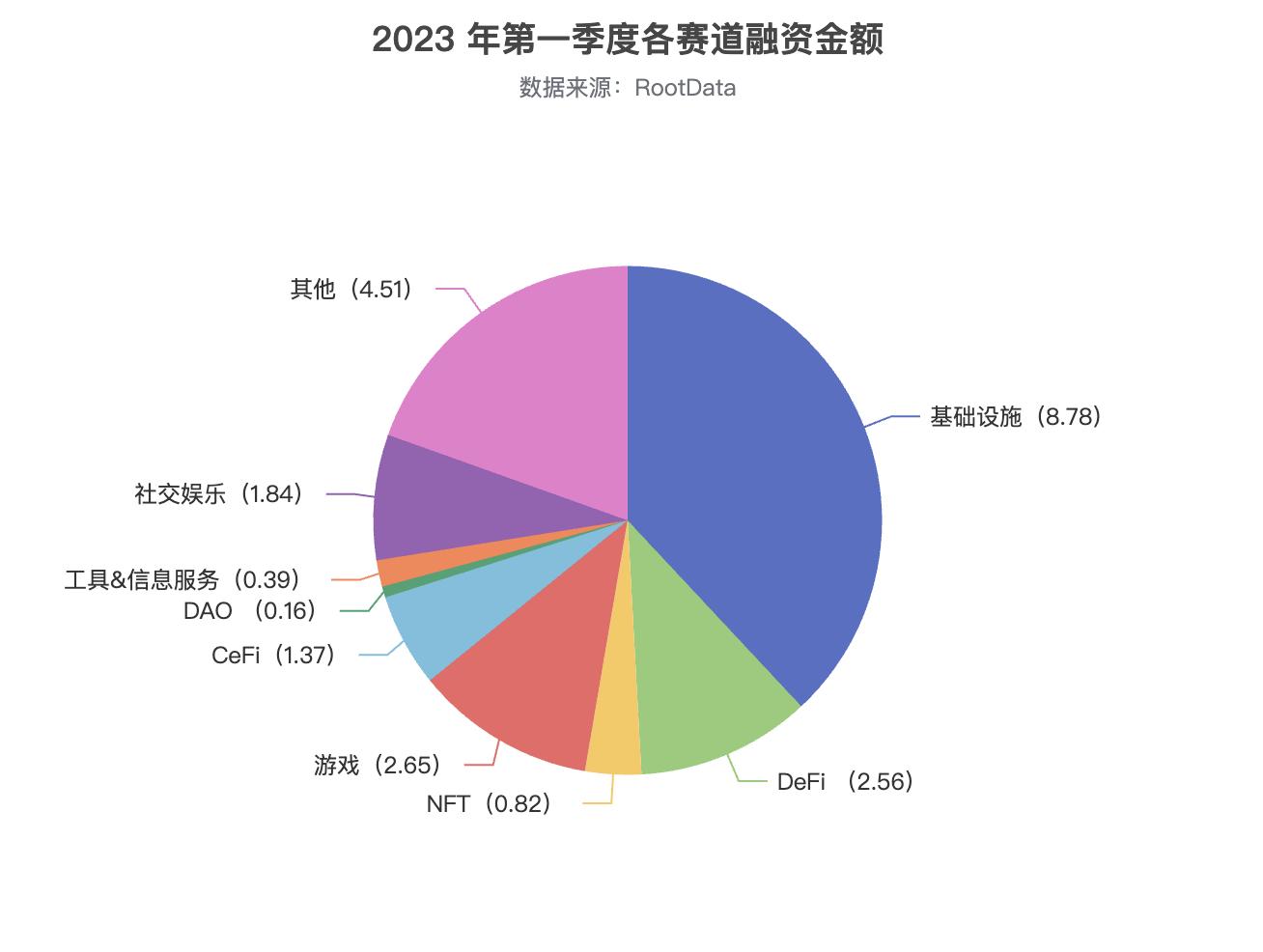

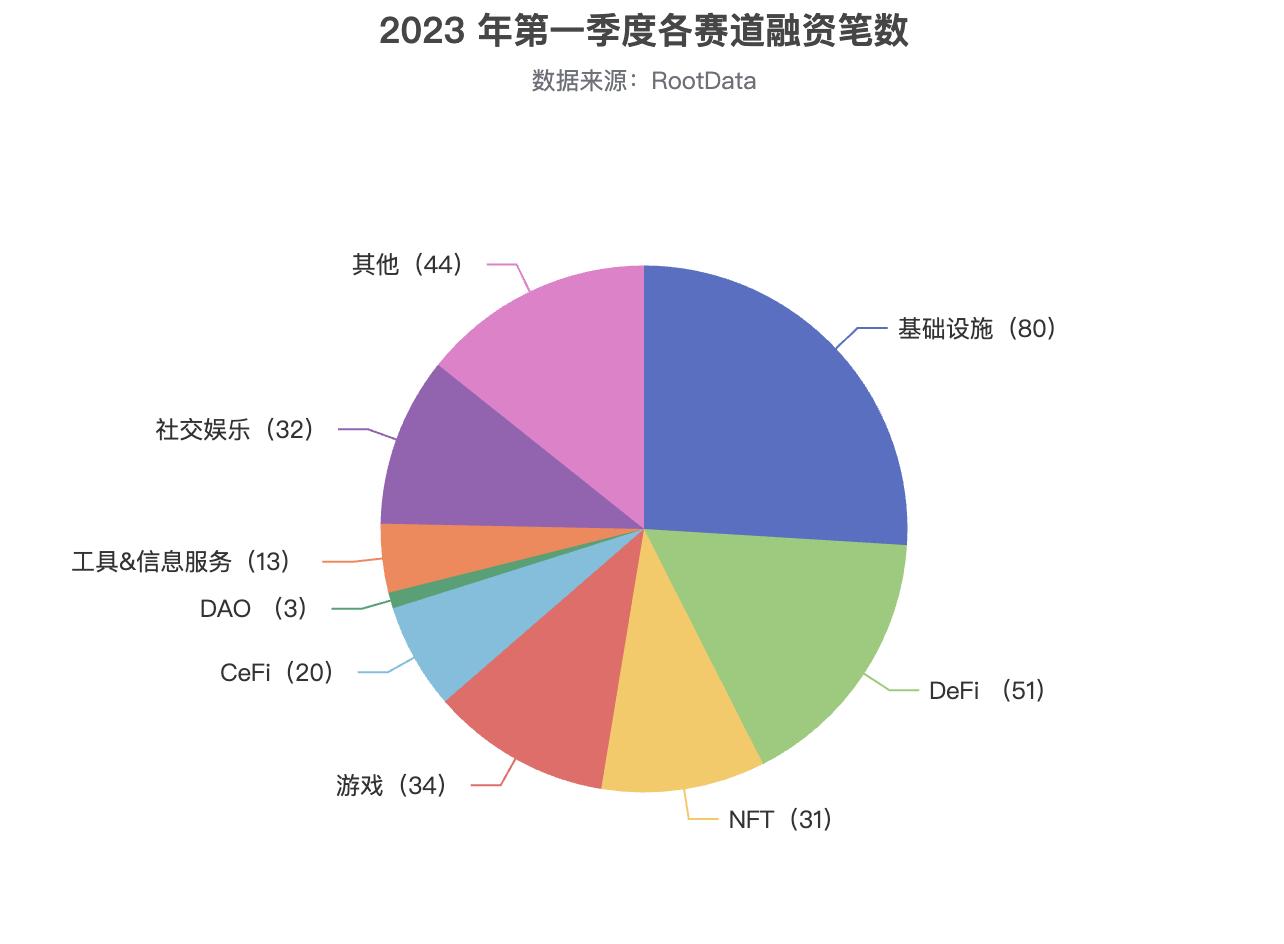

From the distribution of financing across various sectors, the following chart shows the number of financing events and financing amounts (in hundreds of millions of dollars) for each sector from January to March 2023:

Among them, the infrastructure sector had the highest number and amount of financing among the nine major sectors, with an average single financing amount exceeding $10 million. Popular financing projects in this sector include modular blockchains, zk concepts, etc.;

The DeFi sector ranked second in terms of the number of financing events and fourth in financing amount, with popular subfields being DEX, derivatives, etc.;

The gaming and social entertainment sectors ranked third and fourth in terms of financing events, with subfields such as gaming platforms and creator economy being favored by capital in the first quarter of 2023.

2. Analysis of Cryptocurrency Investment and Financing Market Trends in 2023Q1

1) Ethereum Staking Protocols and Services

Ethereum liquid staking allows users to lock ETH in the blockchain network to earn rewards while maintaining the liquidity of the locked funds. According to DefiLlama data, as of the end of March 2023, the total value of crypto assets deposited in liquid staking protocols approached $15 billion. The upcoming Ethereum Shanghai upgrade will unlock staking, which is expected to bring higher staking participation and intensify competition among liquid staking protocols.

For users, liquid staking is attractive in several aspects: first, it is user-friendly, allowing participation in network validation and benefits without needing 32 ETH, making it a relatively stable and secure fixed-income product; second, staking tokens can be withdrawn at any time, with no thresholds; third, it releases liquidity, thus improving capital utilization efficiency; fourth, users can not only receive validation rewards but also participate in governance of the rewards.

In addition, liquid staking is expected to grow further, as the ETH staking ratio is significantly lower than that of other L1 tokens. Currently, only 14% of ETH is staked, while the average for L1 staking is 58%. The current market consensus is that once the Shanghai upgrade is successful, the liquidity risk and uncertainty of the lock-up period will disappear, leading to more funds flowing into staking protocols.

Current liquid staking protocols in the market are facing fierce competition, and newly emerging similar products are focusing on three main directions: first, collaborating with other Dapps to provide more application scenarios for generated derivative tokens; second, striving to deploy on more L1 chains to maximize TVL; third, focusing on improving the security level of the protocols.

During 2023Q1, staking protocols and services such as Unamano, Rocket Pool, Obol Network, Diva, and Ether.Fi received financing successively. Additionally, institutional cryptocurrency custody and staking solution Finoa and MoodMiner, which has a low asset threshold of 1 euro and supports staking for over 100 digital assets, also received funding.

It can be said that the future of liquid staking protocols depends on the overall long-term development of public chains, with security being a top priority. Additionally, factors such as value capture capability and on-chain DeFi ecosystem construction also significantly impact the protocols.

2) AI

Over the past decade, artificial intelligence has steadily entered the commercial field and gradually improved the user experience of internet products, but this has not attracted much interest from outsiders. ChatGPT changed that. Suddenly, everyone is talking about how AI will disrupt their work, learning, and lives.

How AI will transform the cryptocurrency field has become one of the most focused topics in the cryptocurrency industry this year. Many believe that the maturity of AI concepts will bring significant benefits to the Web3 world, with typical use cases including DeFi, GameFi, NFT, DAO, smart contracts, etc.

During 2023Q1, blockchain platforms based on artificial intelligence and machine learning received significant financing, such as Fetch.ai, decentralized collaboration platform FedML, identity system-focused Aspecta, social direction-focused PLAI Labs, digital asset research platform Kaito, and AI creation platform Botto. We can expect to see further integration of artificial intelligence and blockchain, leading to safer, more transparent, and efficient systems.

3) DeFi Derivatives

Just as the traditional financial derivatives market is supported by the hedging needs of physical industries, DeFi derivatives are also evolving from a single trading demand to more diverse fields such as risk hedging.

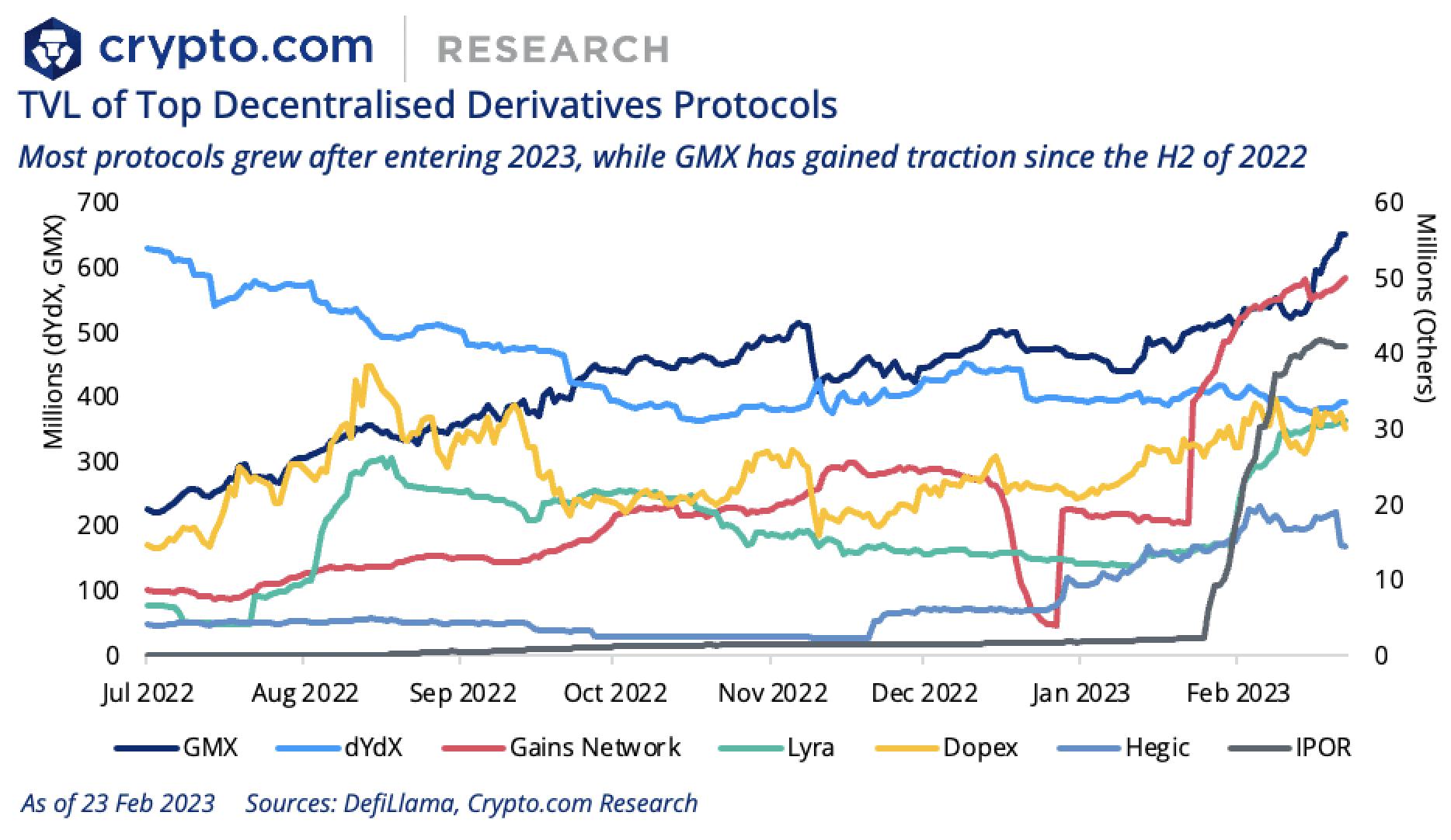

On the other hand, although CEX leads in derivatives trading volume, decentralized derivatives protocols like GMX and Gains Network have also shown significant growth during the bear market of 2022 due to higher transparency and innovative system design.

Currently, emerging decentralized derivatives protocols centered around traders, liquidity providers, and token holders are continuously appearing. Fundamentally, they focus on solving the following problems: first, attracting liquidity and improving asset utilization; second, building composability and cross-margining, such as using various forms of crypto collateral to secure leveraged positions; third, providing a user-friendly experience for traders and liquidity providers.

According to Rootdata statistics, in the last quarter, projects in the DeFi derivatives direction that received financing include the perpetual contract trading platform Narwhal Finance, the decentralized perpetual contract exchange in the Arbitrum ecosystem Vest Exchange, the options trading platform Optix Protocol that supports 10x leverage, and the alternative derivatives protocol Cega that builds exotic options structured products for retail investors, as well as the strategy aggregation protocol Blueberry Protocol that aggregates various leverage strategies into one account.

4) NFTFi

The NFT sector is undergoing significant changes. This emerging asset class is expected to establish a dedicated financial ecosystem.

With the widespread adoption of NFTs, various DeFi protocols and technologies are expected to be applied to NFTs, which is NFTFi, functioning like "LEGO blocks" that can enhance capital efficiency by inserting different protocols.

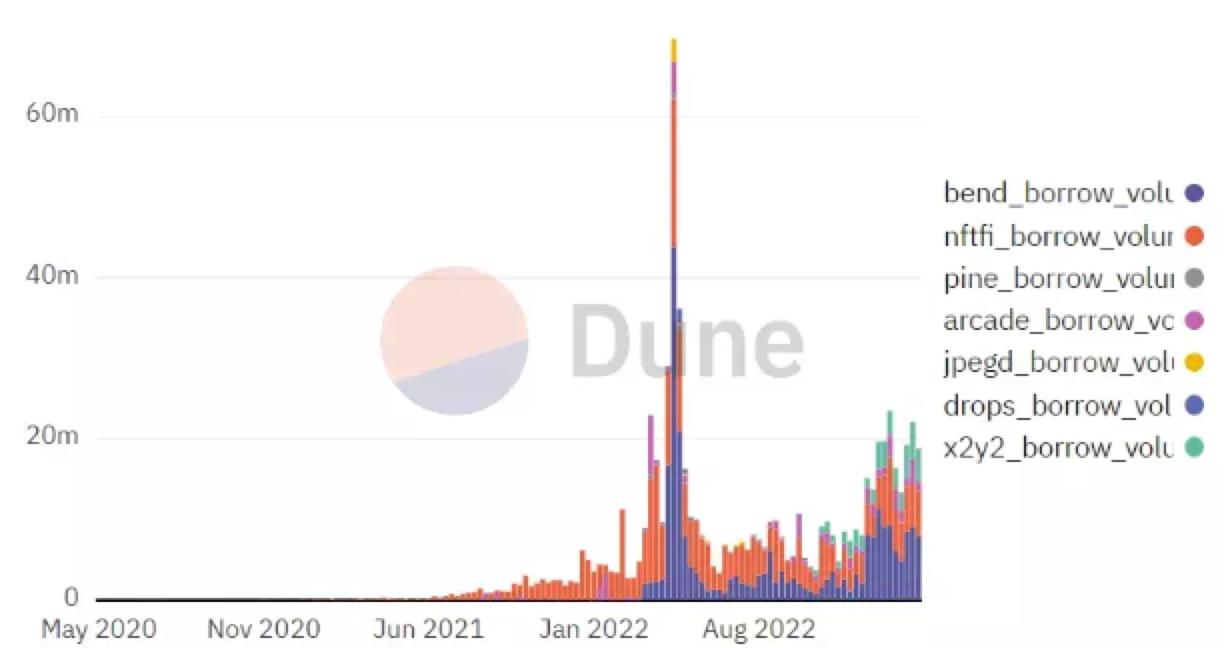

DeFi platforms like Aave and Compound have been around for several years, and now similar products in the NFTFi field such as BendDAO, ParaSpace, JPEG'd, and NFTfi have also emerged. User data and transaction volume data from platforms like Bend, NFTfi, Pine, Arcade, JPEG'd, Drops, and x2y2 indicate that this market is steadily expanding.

(Transaction scale data of NFT lending platforms)

Similar to the DeFi summer of 2020, the NFTFi summer is expected to emerge at some point. This may attract DeFi players who may not have direct interest in NFTs but are likely to be drawn by potential returns.

Over the past two years, NFTs have experienced a turbulent cycle without leveraged participation in trading, and with the launch of NFT derivatives, more people are expected to engage in larger-scale trading. The emergence of NFTFi is expected to bring greater liquidity and higher market efficiency to the entire ecosystem.

During 2023Q1, NFT automatic market maker protocol Midaswap based on Liquidity Book, NFT yield generation protocol insrt finance, NFT lending protocol paprMEME supported by Uniswap V3, NFT derivatives exchange NFEX providing leveraged trading, and community-centered NFT exchange EZswap all received financing.

5) Data Analysis Products

Most companies in Web3 are striving to make data-driven decisions to drive growth. The cryptocurrency field needs more data analysis products to provide users with more comprehensive, diverse, and in-depth insights. On the other hand, pioneering crypto data tools will also effectively enhance the scientific nature of investor decision-making while making the flow of data in the cryptocurrency industry more transparent.

Currently, important issues that many gaming companies, NFT companies, and even asset management platforms are focusing on include how to integrate off-chain, on-chain, and social media data, how to leverage data to drive new user acquisition and activity retention, and how to analyze user behavior through data to guide business.

During 2023Q1, such products that announced financing news include the data analysis platform Helika for game studios and NFTs, multi-chain insights focused on NFTs and digital assets bitsCrunch, data intelligence platform focused on Web3 EdgeIn, and Web3 security infrastructure Trusta Labs providing witch attack prevention analysis.

6) Creator Economy

Although the creator economy in the Web3 industry is still in its infancy, with a small audience and a lack of content production, on the other hand, there are few strong competitors in the industry, making it a very blue ocean with great potential.

Token incentives, as an important innovative tool in the creator economy, allow creators to attract fans using new monetization and value capture mechanisms and co-create new content with them. Its larger-scale application is expected to help strengthen and energize the creator ecosystem.

During 2023Q1, many projects in various subfields of the creator sector received financing. In music, Web3 interactive music platform Muverse and music collectibles platform VAULT; in content, Web3 content creation platform RepubliK and novel reading platform Read2N; in brands, fashion, and artists, cultural brand ManesLAB, artist platform Wild, Web3 fashion platform Syky; and also the platform GigaStar that builds a better mutually beneficial mechanism for YouTube creators and fans all received financing.

7) Modular Blockchain

Modular blockchain refers to a blockchain that completely outsources at least one of the four components: "execution layer, settlement layer, consensus layer, data availability layer" to external chains. Due to the complexity of providing services to millions or more users on a single chain and limited resolution capabilities, shard and Layer 2 solutions were proposed, which gradually evolved into modular blockchains. The initial solution for modular implementation was rollups, a concept that was later expanded into modular blockchains.

The main advantages of modular blockchains currently are twofold: first, they possess sovereignty; although they use other layers, new modular blockchains can have sovereignty like L1. This allows blockchains to respond to hacker attacks and push upgrades without any underlying permission; second, they effectively improve scalability, achieving expansion without sacrificing security or decentralization.

During 2023Q1, projects focusing on building high-performance, customizable second-layer blockchains Caldera, modular settlement layers dYmension, and ecosystems of interoperable and scalable rollups Sovereign all received significant new rounds of financing.

8) zk Concepts

The zk ecosystem is becoming increasingly prosperous. Zk-Rollup uses validity proofs to verify and package all transactions off-chain, and when the verified transactions are submitted to the main chain, they are accompanied by zero-knowledge proofs to prove the validity of the transactions. In the words of StarkWare CEO Uri, "It provides trustless computational integrity, ensuring that the computation is executed correctly even without supervision." This sounds very similar to the early ideals of Bitcoin.

In comparison, Optimistic Rollup can be compatible with EVM, has a mature and early technical solution, and has lower migration costs for developers, with representative projects Arbitrum and Optimism currently holding the highest market share among rollups. However, zk-Rollups, due to their incompatibility with EVM and higher technical difficulty, have slower development progress and are currently not as widely applicable as OP series rollups that can target smart contracts.

However, zk-Rollups have many advantages compared to Optimistic Rollups: first, better scalability, as zk-Rollups require uploading less data to the mainnet than Optimistic Rollups. In practical applications, zk-Rollups can enhance performance approximately ten times that of Optimistic Rollups; second, shorter transaction finality times; third, higher security.

Vitalik once said in 2021, "In the short term, Optimistic rollups will win due to their EVM compatibility. But in the medium to long term, as zk-SNARK technology improves, zk-rollups will win all use cases."

During 2023Q1, zk concept projects that announced completed financing include the trust layer based on zero-knowledge proofs Proven, Ethereum native zkEVM second-layer solution Scroll, zk-rollup protocol Polybase, Web3 interoperability infrastructure PolyHedra, zk dark pool protocol Renegade, ZK hardware acceleration project Cysic, ecosystem of interoperable and scalable rollups Sovereign, ultimate Web3 middleware based on ZKP Hyper Oracle, and zero-knowledge proof market =nil;.

9) Security Solutions

Web3 security technology is rapidly developing, but the transparency and openness of blockchain code still lead to frequent hacking incidents. Since 2021, losses in Web3 due to security issues have exceeded $10 billion. Therefore, how to provide asset protection-related products for enterprises, infrastructure providers, and ordinary users to avoid losses from hacking or human errors has always been an important theme in the cryptocurrency industry.

How to analyze smart contracts to prevent vulnerabilities? How to monitor malicious activities on-chain? How to establish a better and more mature digital asset ecosystem? These are also the problems that companies in this sector are trying to solve.

During 2023Q1, relevant projects can be divided into two categories based on the type of clients served: one targeting B-end clients, such as the cryptocurrency security service provider Ironblocks that automatically conducts threat detection and helps teams take preventive measures quickly, the cryptocurrency security company Hypernative that uses proprietary machine learning models to monitor on-chain and off-chain data sources, and MetaTrust that automates the generation of security scanning solutions using a security scanning engine; the other targeting C-end users, such as the cryptocurrency security company Staging Labs that actively scans transactions around the clock and can timely transfer risk assets, and the cryptocurrency security solution Coincover that can identify unauthorized access to suspicious transactions.

3. Performance of Cryptocurrency Investment Institutions

After experiencing a series of upheavals such as the FTX incident, the cryptocurrency investment institution market is also undergoing a reshuffle, with many venture capital firms falling silent while several institutions are still accelerating their investment frequency.

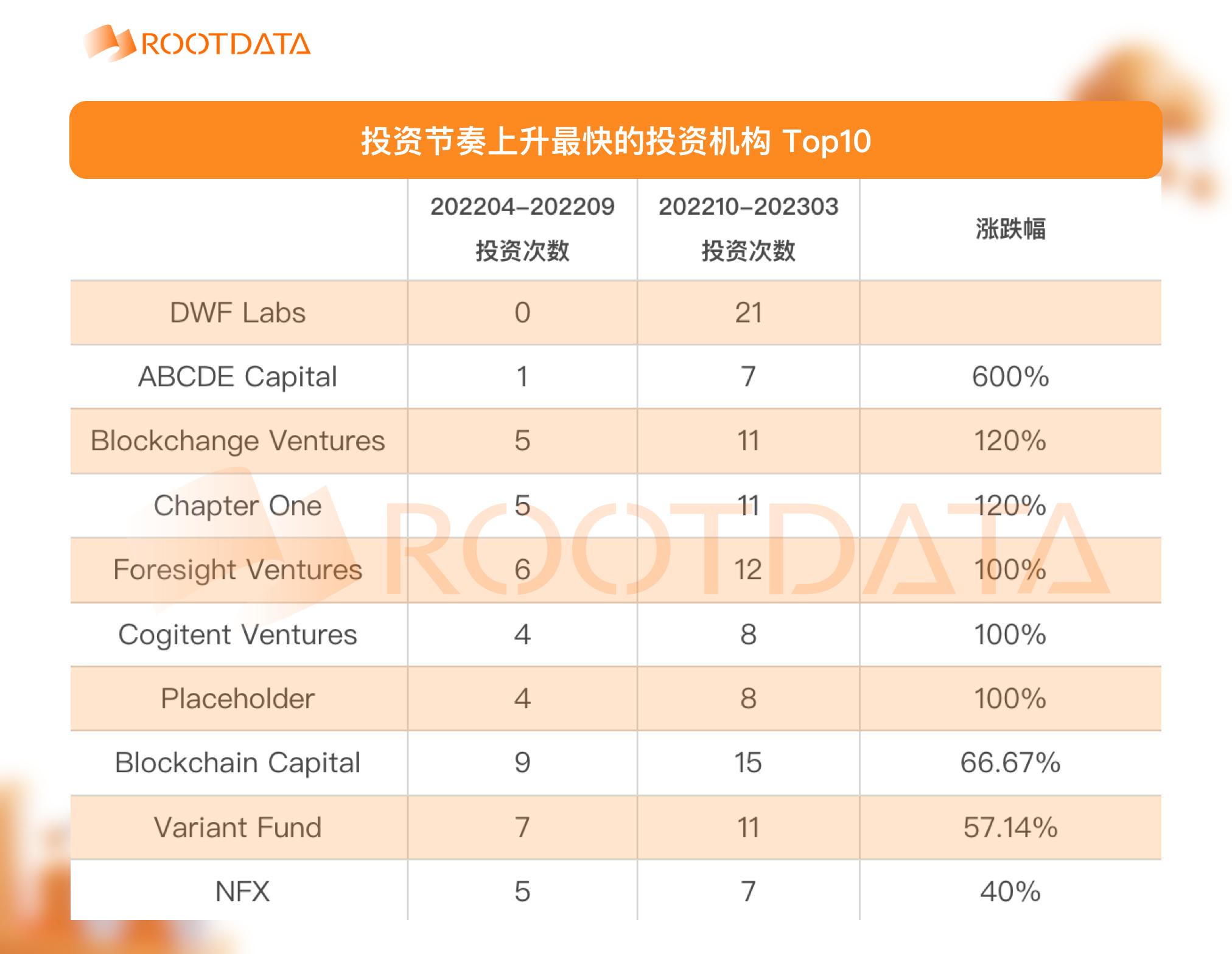

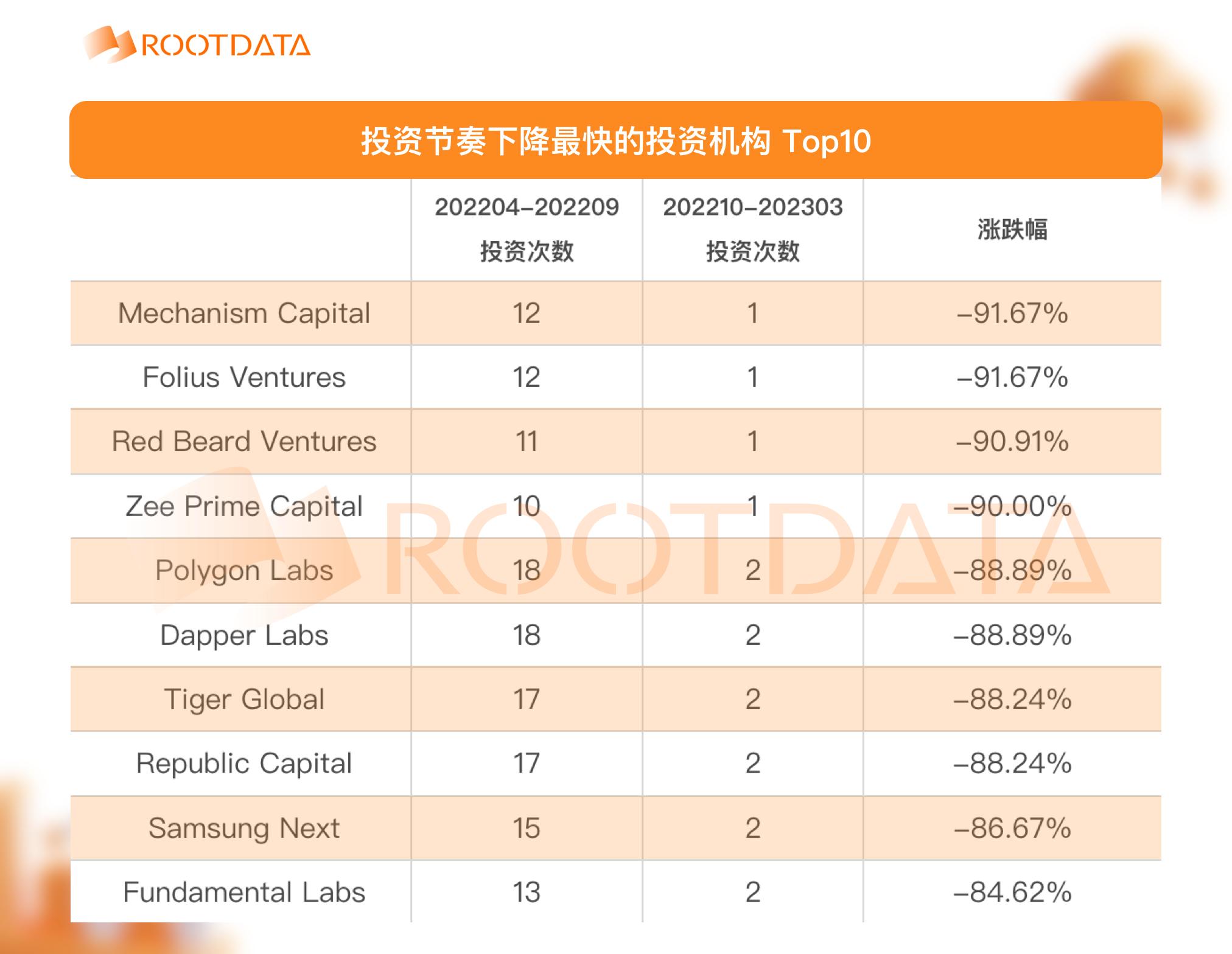

Considering the representativeness of the data interval (the data volume in the first quarter is insufficient), Rootdata counted the number of times cryptocurrency investment institutions made moves in the past six months (from October 2022 to March 2023) and compared it with the data from the previous six months (from April to September 2022), filtering out the 10 investment firms with the highest increase and decrease in investment frequency based on a minimum investment of 8 times.

In terms of the fastest growth, DWF Labs is a well-known dark horse in the industry, with at least 21 publicly disclosed investments in the past six months, while this institution had no previous records of making moves. Additionally, ABCDE Capital, Blockchange Ventures, Chapter One, Foresight Ventures, Cogitent Ventures, and Placeholder all publicly disclosed investment counts that increased by more than double.

In terms of the largest declines, well-known institutions such as Mechanism Capital, Folius Ventures, Zee Prime Capital, Polygon Labs, Dapper Labs, Tiger Global, and Republic Capital all experienced declines exceeding 85%, with publicly disclosed investment counts not exceeding 2 times.

Furthermore, in terms of overall investment counts, the top ten investors in the past six months are Coinbase Ventures, Shima Capital, Big Brain Holdings, Polygon Ventures, DWF Labs, Polychain, Circle Ventures, HashKey Capital, Solana Ventures, and a16z.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles