The Choice Between Centralization and Decentralization: Analyzing the Pragmatic Principles of the New Stablecoin HOPE

Overall, we have a positive attitude towards project innovation in the stablecoin sector. An additional competitor also means a greater possibility of changes in the landscape.

Overall, we have a positive attitude towards project innovation in the stablecoin sector. An additional competitor also means a greater possibility of changes in the landscape.Author: CryptoDada, Deep Tide CryptoFLow

What exactly are we talking about when we discuss stablecoins?

Setting aside the similarities and differences in the design principles of various stablecoins, the emergence of such products actually reflects the development of the crypto world: cryptocurrencies have grown from a small-scale geek experiment to a larger-scale entity that can compete with real financial assets.

As the industry grows, the functions of stablecoins are also changing in tandem: from a safe haven to avoid significant crypto volatility, to the first stop for attracting traditional investors, and possibly to a vehicle for cross-regional settlements… It is undeniable that stablecoins have developed a close connection with the real world. Today's stablecoins need to fulfill the dual functions of "bringing in" and "going out"—attracting traditional investors into areas like DeFi, while also serving as a settlement medium that permeates traditional economic activities.

However, the reality is that stablecoins are not stable. In the past two years, the collapse of stablecoins has been evident, with negative events affecting fiat-backed stablecoins due to banking influences, which has undermined the confidence of both on-chain and off-chain users in the use of stablecoins.

So, do we still need new stablecoins?

The answer is yes. We need a free, practical, and secure asset that serves as a bridge between the real world and the crypto world, one that is unaffected by traditional finance, yet allows users to quickly recognize and use it, thereby better achieving the aforementioned "bringing in and going out" functions.

In keeping an eye on the daily developments in the industry, the recently launched stablecoin HOPE has garnered considerable attention: backed by native crypto assets, its value can fluctuate, and it features distributed custody of funds… Various keywords seem to differ from the traditional concept of stablecoins. Could it be a project that understands industry pain points and is innovating? And for most ordinary users, could this represent a new investment opportunity?

With questions and interest, Deep Tide will interpret HOPE from aspects such as its design intentions, product principles, actual experiences, and economic models, hoping to provide more references for practitioners and users.

1. Stability, Independent of the Storm

Before studying HOPE, let's first take a look at the current external environment associated with stablecoins.

In the previously popular show "The Storm," there was a line, "The bigger the storm, the more valuable the fish," which seems to add too much rationality to risk-taking. But in the crypto world, the greater the external storm, the easier it is for people to be overwhelmed.

We can outline some potential sources of storms that may affect the crypto world.

- Collapse of the CeFi Ecosystem: The collapse of Three Arrows Capital and FTX has led to the downfall of assets associated with these centralized institutions, reminding people not to let their guard down regarding assets held by centralized entities.

- Stablecoins Are Not Smooth Sailing: The previous collapse of the UST algorithmic stablecoin, followed by the bankruptcies of Silvergate and Silicon Valley Bank during the interest rate hike cycle, has caused panic over the USDC, which is backed by fiat currency, being unable to be redeemed; and the over-collateralized DAI, which also has a significant portion of its reserves in USDC, is unlikely to escape unscathed when external storms arise.

- Regional Confrontation and Globalization: The increasingly tense geopolitical situation in some regions and the transaction costs in global cross-border payments and financial activities have made people realize that there may be a need for a decentralized stablecoin solution.

If we summarize the above points, it becomes clear that the crypto world may need a stablecoin that is not supported by fiat currency or algorithmic mechanisms, and that can become a more widely recognized reserve asset to isolate the significant risks posed by traditional financial systems, centralized institutions, and unreliable algorithms.

So, is it feasible to use Bitcoin or Ethereum as collateral to create a stablecoin?

This is also what HOPE is currently attempting to do—starting with crypto assets as collateral, independent of the aforementioned storms, to create a stablecoin.

BTC and ETH, after years of development, have relatively solid consensus and stable prices (compared to Altcoins), and their influence can extend further. Using these two as collateral to generate HOPE seems to align with the concept of "crypto-native stablecoins" to the greatest extent; moreover, Deep Tide has learned in preliminary research that HOPE initially does not adopt a complete pegging design; its price will fluctuate with the prices of BTC and ETH, which is quite different from most stablecoins seen previously.

If it cannot even achieve pegging, does that mean HOPE is not suitable for being a stablecoin?

However, if we temporarily set this question aside, under the design of being crypto-native, we can feel some obvious advantages:

- First, BTC and ETH may isolate the risks of single-point failures in CeFi and systemic impacts from fiat currency;

- Second, the upcoming Bitcoin halving cycle and the potential cessation of interest rate hikes provide expectations for the rise of BTC and ETH, which also means the possibility of expanding market capitalization.

In the current competitive landscape of stablecoins, we believe that a stablecoin backed by BTC and ETH is a worthy exploration. Returning to the key question—how is HOPE's price fluctuating with the two? This design involves the specific product mechanism of HOPE.

In the following sections, we will introduce HOPE's generation, custody, circulation, and use cases one by one.

2. Budding, Born from Fluctuation

In the official definition, HOPE is a "pricing token supported by reserves of BTC and ETH, evolving from a multi-stage growth plan into a distributed stablecoin." In the above description, "pricing" and "distributed" correspond to HOPE's generation and custody phases, which are also the focus of our research.

First, let's look at the pricing based on BTC and ETH, i.e., how HOPE is generated.

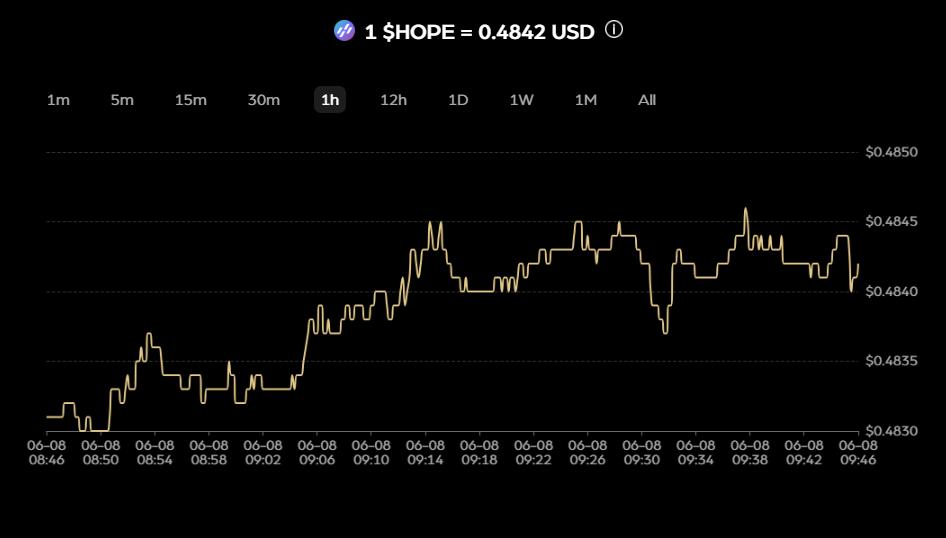

Anchor Asset: Pegged to BTC/ETH, initially issued at 50% of face value ($0.5); as BTC and ETH appreciate, its market value is expected to gradually reach 100% ($1). The price now fluctuates with the prices of BTC and ETH while maintaining the established ratio.

From the official data currently available, HOPE's price is around $0.48. It can be seen that HOPE is not directly pegged to a value of $1 but is pegged to the value of Bitcoin and Ethereum; subsequently, if the prices of the two appreciate, HOPE's price may grow to $1 along with the expansion of the market capitalization of crypto assets.

Before that, HOPE is not strictly a "stablecoin," but more like a collateralized crypto asset isolated from fiat currency. If considering exchanges with other Altcoins, it is closer to a mainstream currency-based purchasing power.

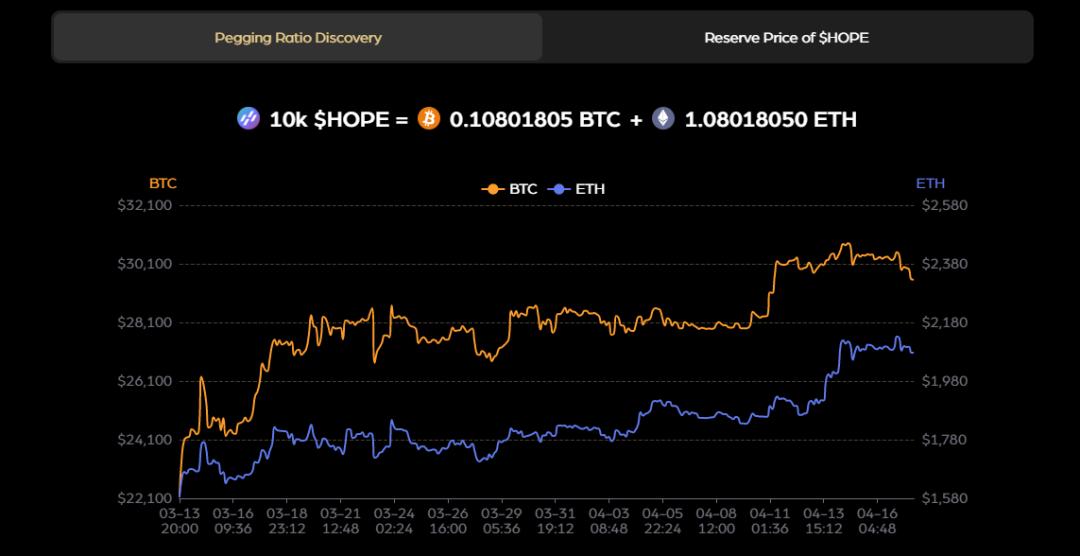

Minting/Pricing Principle: After establishing the initial pegging ratio of BTC and ETH for HOPE, the price observation process is completed to determine the pegging ratio with BTC/ETH. From the diagram below, we can see that currently, to generate 1 HOPE, a certain amount of BTC and ETH needs to be reserved;

This approach is somewhat similar to the mechanics of LSD, where ETH is collateralized to generate stETH and other derivatives. However, in LSD, the derivatives maintain a 1:1 constant with the collateral, while HOPE weights BTC and ETH according to a certain calculation formula. The current ratio is shown in the data from the official website below.

As of now, HOPE has completed the price discovery process, and the calculation formula for the discovery mechanism is:

In practice, to ensure fair price discovery, the project team collects OHLC data (open, high, low, close) for Bitcoin and Ethereum from three exchanges (Binance, OKX, and Coinbase) every minute and forms an average; from the formula above, it is also easy to see that the current BTC/ETH ratio is 1:10, which should be able to change with market fluctuations and voting mechanisms.

If we follow the above mathematical calculations, a HOPE valued at $0.5 corresponds to $0.5 of the weighted BTC and ETH. Therefore, if the prices of BTC and ETH rise to a critical point, it means that the value of HOPE will exceed $1.

At that point, it will truly be a stablecoin pegged in the real sense. Once the value of HOPE exceeds $1, its price will remain at $1 and not rise further, while the underlying BTC and ETH as collateral will have a value exceeding $1, essentially meaning that HOPE has become an over-collateralized stablecoin; in the official design, the ideal over-collateralization rate is 110%.

The reason for designing this ratio is that a 110% slight over-collateralization can maintain the price stability of HOPE while allowing room to adjust the issuance of HOPE according to market demand. Changes in reserves and adjustments in issuance will be decided through community proposals and voting.

Next is about the custody of HOPE. As mentioned above, for every $1 of HOPE, there is an equivalent amount of BTC and ETH behind it, so the question arises: where are they stored? How can we ensure their credibility?

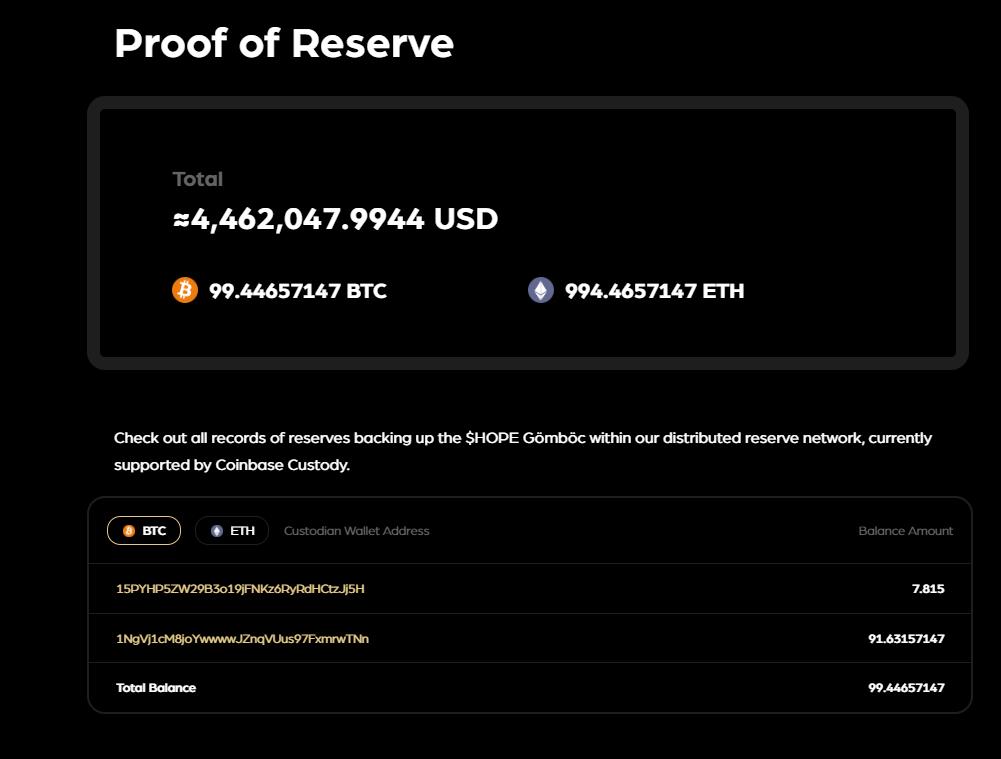

HOPE Gömböc: Distributed Reserve Design

HOPE Gömböc is a set of distributed reserve pools that spread crypto assets across trusted third-party custodians to ensure security; the name Gömböc is derived from a geometrical shape that is stable.

In the early stages of the project, HOPE chose Coinbase for custody, and will later select other custodians or decentralized custody protocols on-chain. Additionally, the BTC and ETH in the reserve pool will gradually be converted into distributed, stable-value, and liquid assets to avoid being affected by price fluctuations.

Regarding the wallet addresses of custodians, custody amounts, and fund movements, HOPE has made them fully public, and the status of funds at these addresses can be viewed through BTC and ETH explorers.

It is worth noting that the public nature of the custody addresses somewhat proves the existence of equivalent asset collateral; however, HOPE has not provided specific indications regarding the ownership of these addresses, the entities behind them, or whether there are connections between the addresses, which requires further observation and research.

In the above distributed reserve design, we instinctively raise a question—choosing multiple third-party custodians to hold assets, while it diversifies risk, does it not resemble a choice that trusts centralized institutions?

With this question in mind, Deep Tide also consulted HOPE's design team, which stated that this is a more pragmatic design:

Choosing a distributed route between centralization and decentralization aims to take the strengths of both while avoiding their weaknesses to achieve optimal feasibility. Traditional DeFi is self-custodied and appears completely decentralized. However, many traditional investors want to participate in HOPE and have put forward a very important condition—being able to undergo audits.

Currently, regulatory-approved audits can only be supported by large custodians like Coinbase. Therefore, from the perspective of attracting traditional investors, HOPE will collaborate with major global institutions, including Coinbase, to provide secure distributed custody for user assets.

From the perspective of the stablecoin's function of "bringing in," attracting traditional investors is crucial. Thus, pursuing complete decentralization means sacrificing stability and capital efficiency, which is not the optimal choice in the current market cycle. For HOPE to become a bridge for real-world payments, it cannot completely detach from the operational rules of capital in the real world to attract traditional funds and project participation.

After understanding the generation and custody design of HOPE, another important point lies in the circulation aspect.

Phased Guidance for Circulation:

The development of $HOPE can be roughly divided into two phases: the growth phase (price between $0.5-$1) and the maturity phase (price stabilizing at $1).

In the growth phase, its design mechanism only accepts BTC/ETH as reserve assets to mint $HOPE, and market makers can arbitrage based on market prices and deviations from the value of $HOPE;

In the maturity phase, it will accept other stable assets such as USDC/USDT as reserve assets to mint $HOPE; at the same time, the project will open on-chain automated mint/burn protocols at appropriate times, allowing more market participants to directly mint/burn $HOPE.

Finally, when the value of BTC and ETH rises, the total value of the collateral corresponding to a single HOPE will exceed $1, at which point it will enter a state of over-collateralized stablecoin, with the DAO deciding on the use of the excess reserve funds. In summary, HOPE does not pursue immediate stability but aims to gradually grow towards stability, representing a relatively novel design in the current market, which still requires time for validation.

3. Product Functions: Prioritizing HOPE Liquidity Expansion

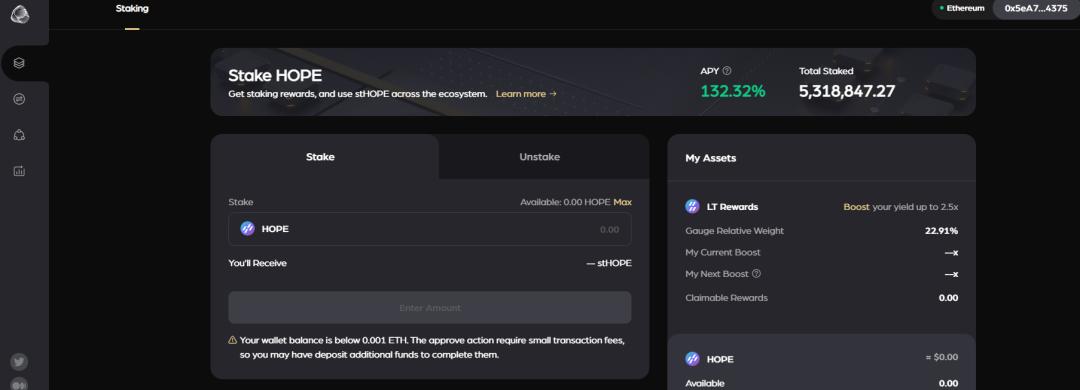

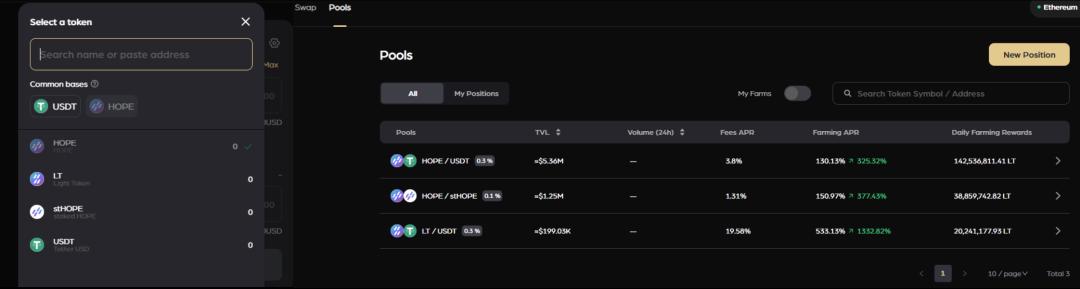

Currently, the HOPE mainnet has been launched, and the website offers two basic products: HOPE staking and HopeSwap.

Among them, the staking function is similar to common DeFi projects, allowing users to stake HOPE to receive liquidity tokens stHOPE. stHOPE can be used in the current Swap and later launched lending products like HopeLend, and users can also earn rewards in the project's governance token $LT.

We will introduce the specific details of the LT token in the economic model section later. The simple logic to understand here is: staking HOPE generates stHOPE, and holding the latter can earn LT; at the same time, the more stHOPE one holds, or the longer the earned LT is locked, the more LT will be generated.

In HopeSwap, users can exchange between tokens, currently supporting project-related tokens and USDT; at the same time, on the liquidity pool side, users can also inject liquidity into the pool to earn LP rewards.

In addition to the existing staking and Swap products, HOPE will also launch the following products:

In addition to the existing staking and Swap products, HOPE will also launch the following products:

- HopeLend: A non-custodial lending protocol with multiple liquidity pools. Lenders can deposit liquidity to earn interest, while borrowers can withdraw tokens after providing collateral.

- HopeConnect: A decentralized custody and clearing settlement platform that allows various applications to be built on its foundation. The overall product is divided into three phases, with the first phase allowing users to obtain payment and transaction credit by staking assets within HopeConnect, without bearing the risks of centralized custody. Ultimately, it will become a standard protocol connecting DeFi, CeFi, and TradFi.

- HopeEcho: Synthetic assets that track the prices of real-world assets (RWA), democratizing access to traditional finance, including but not limited to stock indices, fixed-income instruments, commodities, foreign exchange, etc.

Overall, we believe that HOPE's product strategy is relatively clear—first attract users and expand HOPE's liquidity through functions like Swap and staking, addressing the foundational issues, gaining recognition in DeFi, and then layering on higher-level financial plays, gradually penetrating into CeFi and TradFi.

4. Economic Model: Hope and Light ($HOPE $LT)

The product experience section has already touched on the LT token, and here we can conduct a more detailed examination. In fact, the project has two types of tokens, HOPE and LIGHT. The former serves as collateral (growing into an over-collateralized stablecoin later), while the latter is a governance token. The names of the two tokens symbolize "hope" and "light," respectively.

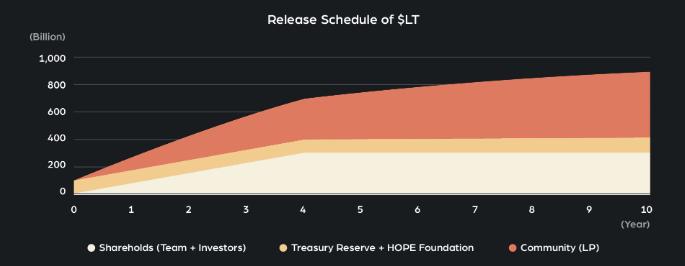

The total supply of LT is designed to be 1 trillion, with an initial supply of 400 billion tokens, accounting for 40% of the total supply; the remaining 60% of LT follows a segmented linear inflation model, with all released tokens allocated to liquidity providers in the HOPE ecosystem.

In the initial circulation, 50 billion LT will be allocated to the project treasury as reserves, and another 50 billion will be allocated to the HOPE Foundation.

According to official statistics, in the first year of the project, approximately 260 million LT will flow into the supply daily. Further examining the role of LT, we can summarize two main directions: locking and governance.

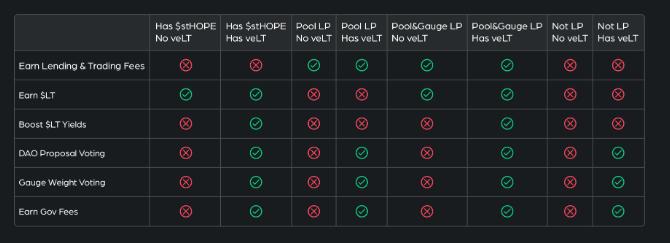

Locking: After holding or obtaining LT, users can choose to lock LT to obtain veLT. Similar to the ve model of most DeFi projects, the duration and quantity of the lock are proportional to the LT rewards that can be obtained, encouraging users to lock while also exerting a certain degree of suppression on token emission inflation;

From the table below, it can be seen that when other conditions are the same, there is a difference in the rewards that can be obtained between holding veLT and not holding it.

Governance: LT holders can participate in several aspects of governance, including the monetary policy of $HOPE, such as maintaining the peg and managing reserves. For example, if 10 billion $HOPE are initially issued, the total reserve value will be approximately $5 billion; as the value of assets like Bitcoin increases, the reserve value may grow to $50 billion, resulting in $40 billion of excess reserves. The community will decide how to handle the excess portion through proposals.

One possible proposal is to convert the reserves into stable assets like Hong Kong bonds and Singapore bonds to increase the application potential of $HOPE. Having $50 billion in stable reserves effectively means that more $HOPE can be issued, distributing more excess value to $LT holders.

Additionally, 50% of the fee income generated by various protocols within the HOPE ecosystem will be allocated to liquidity providers, while the other 50% will be distributed to community members holding $LT tokens.

From the design of the above economic model, it can be seen that the project's economic incentives balance short-term and long-term considerations. If HOPE can peg to $1, the value generated by excess assets will actually benefit LT holders, and theoretically, after reserving real assets, the project's imagination will be greater.

By synthesizing the above surface information, we can deduce the subsequent value manifestation of LT:

1. LT is essentially a perpetual call option on BTC/ETH:

Since the target price of $HOPE is $1, it means that when the prices of BTC and ETH reach double their current values, the price of $HOPE itself will no longer continue to rise (from $0.5 to $1);

In the next bull market, when BTC/ETH exceeds the above prices, the reserve value of $HOPE will continue to grow, and this portion of value will be fully reflected in the price of $LT. As long as one is optimistic about the long-term market trend, LT effectively becomes a call option.

Assuming that BTC reaches $100,000 and ETH reaches $10,000, the value of the $HOPE reserve pool will be five times what it is now. However, as a stablecoin, without additional issuance, the market capitalization of $HOPE can at most double. Other values will be reflected in the overall ecological value of $LT and HOPE, as $LT holders can decide how to use these excess reserves, determining decisions on issuance increases, reserve changes, etc.

2. veLT holders may become the biggest beneficiaries of the HOPE ecosystem:

veLT holders can receive mining reward bonuses, and 50% of the platform's fee income will be distributed to veLT holders; in addition, veLT holders decide the mining reward ratios for each pool and the monetary policy of $HOPE, the use of the Treasury, and other matters;

3. Positive Flywheel Effect Created by Ecological Effects:

It can be imagined that the development of the HOPE ecosystem will bring more use cases for $HOPE, further expanding the ecosystem, which means an increase in the demand and reserve scale of $HOPE; at the same time, the rising prices of BTC/ETH will also lead to an increase in the reserve scale of $HOPE.

As the reserve scale of $HOPE increases, the overflow value will be borne by $LT, which to some extent will also lead to an increase in the underlying value contained in $LT, while forming a complete value chain:

Development of the HOPE ecosystem and increase in the reserve scale of $HOPE -> Increased demand for governance (veLT) -> Increased demand for $LT.

However, it should be noted that currently, the absolute daily emission of LT is relatively high, and whether the ve model can sustainably lock liquidity to prevent selling pressure remains to be seen; additionally, the initial liquidity of 50 billion LT allocated to the project foundation, the purposes and usage of this portion, whether they will be made public for verification later, will also affect market confidence in LT.

5. Future, Connecting Crypto and the Real World

Overall, we hold a positive attitude towards project innovations in the stablecoin space. More competitors mean more possibilities for changes in the landscape.

However, whether the landscape can truly change depends on how well the project plans and executes its strategies.

Currently, HOPE has not yet achieved the $1 peg, and there is still a considerable distance to go. The project is also regularly holding AMAs, along with various rewards and promotional activities, attempting to create buzz in the early stages of development to increase user awareness of HOPE. To venture into the traditional financial sector, it still needs to actively showcase itself in more traditional financial conferences and events to establish deeper resources and connections, addressing channel and regulatory issues.

In terms of specific planning paths, HOPE has also designed a three-step plan:

- 2023-2025: Create application scenarios to establish a robust liquidity market and interest rate market for $HOPE, with the primary task in the early stages being to develop $HOPE into a reliable collateral choice in the DeFi space;

- 2026-2029: With the narrative of halving and the easing of the expected interest rate environment, HOPE will have the opportunity to transition from native asset reserves to an over-collateralized stablecoin. The goal during this phase is to make $HOPE a payment tool, providing financial services to everyone, including the unbanked population;

- Long-term: Enable all users, including those without crypto and DeFi experience, to use various financial services through $HOPE and the HOPE ecosystem without barriers, openly and transparently.

This long-term goal returns to the characteristics of inclusive finance in DeFi, which is also the direction the industry is collectively striving for—Web3 is currently not doing well enough in bringing in, and going out seems to be a challenging task.

From the small-scale collateral in DeFi to an international clearing and settlement currency, we hope that more similar projects can undertake the functions of "bringing in and going out."

Though the journey is long and arduous, it is worth climbing.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles