The Stablecoin Landscape After MakerDAO EDSR: Transformation, Response, and Opportunities

In the case where MakerDAO allocates a 5% annual yield for DAI holders, stablecoin holders have increased demand for earning returns, leading to many stablecoins being drained. Let's take a look at the performance and responses of USDC, FRAX, LUSD, and eUSD.

In the case where MakerDAO allocates a 5% annual yield for DAI holders, stablecoin holders have increased demand for earning returns, leading to many stablecoins being drained. Let's take a look at the performance and responses of USDC, FRAX, LUSD, and eUSD.Written by: Jiang Haibo, PANews

With the emergence of disruptors like Liquid Staking Derivatives Finance (LSDFi) and MakerDAO's Enhanced DAI Savings Rate (EDSR), stablecoin holders have increased demand for yield. Since MakerDAO's EDSR allocates a 5% annual yield to DAI holders, other stablecoins may be exchanged for DAI to earn yield, leading to "bloodsucking," which reduces issuance or turns premiums from positive to negative. In response to this dilemma, some stablecoin issuers are actively updating their strategies.

USDC: Hold in Coinbase to Earn 5% Annual Yield

Maker's Peg Stability Module (PSM) allows for 1:1 minting of DAI using centralized stablecoins like USDC or redeeming DAI for centralized stablecoins. After this feature was launched, the proportion of USDC in DAI's collateral gradually increased to over 50%. This has led to criticism that DAI has lost its decentralized characteristics; although the issuance of DAI has increased, this portion of DAI does not generate stable fees for Maker and instead bears the counterparty risk of USDC, which was evident during USDC's depegging incident this year.

The situation began to change as Maker gradually invested the funds in the PSM into Real World Assets (RWA). In this process, USDC in the PSM would be redeemed for USD and used to purchase US Treasury ETFs. The pressure then shifted to USDC's issuer, Circle. Since there are no fees for minting or redeeming USDC, Circle transitioned from being a beneficiary of DAI to a compliant channel helping Maker attract funds to purchase US Treasuries.

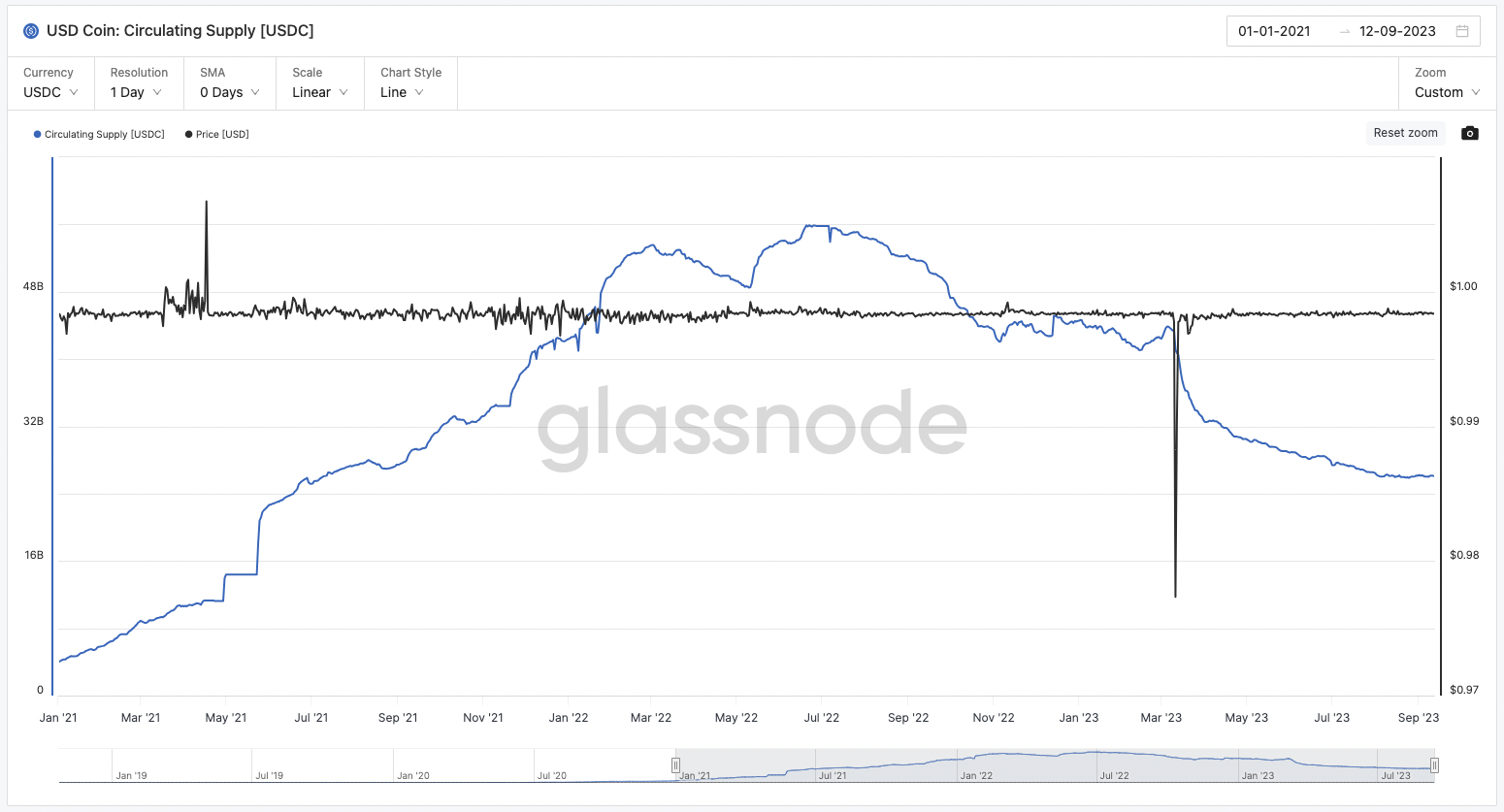

According to Glassnode data, the issuance of USDC has decreased from 55.9 billion in June 2022 to 26.08 billion as of September 12, 2023. Maker's redemption of USDC to purchase US Treasuries has played a certain role in this decline.

In September 2022, Coinbase proposed in the Maker forum to deposit part of the USDC in the PSM into Coinbase Prime to participate in Coinbase's institutional rewards program, which could earn a 1.5% annual yield.

However, Maker did not stop redeeming USDC to purchase government bonds. In July of this year, when only over 300 million USDC remained to ensure necessary liquidity in the PSM, Maker co-founder Rune proposed to implement EDSR and raise the DSR to 8% to attract incremental funds. Subsequently, the EDSR was lowered to 5%.

In this context, Coinbase chose to follow suit, allowing users to earn a 5% annual yield simply by holding USDC on the Coinbase exchange.

Recently, the issuance of USDC seems to have escaped the downward trend, but due to Coinbase's concessions, the earnings for USDC issuers will decrease. Similarly, new competitors like PYUSD and FDUSD have emerged in the centralized stablecoin space.

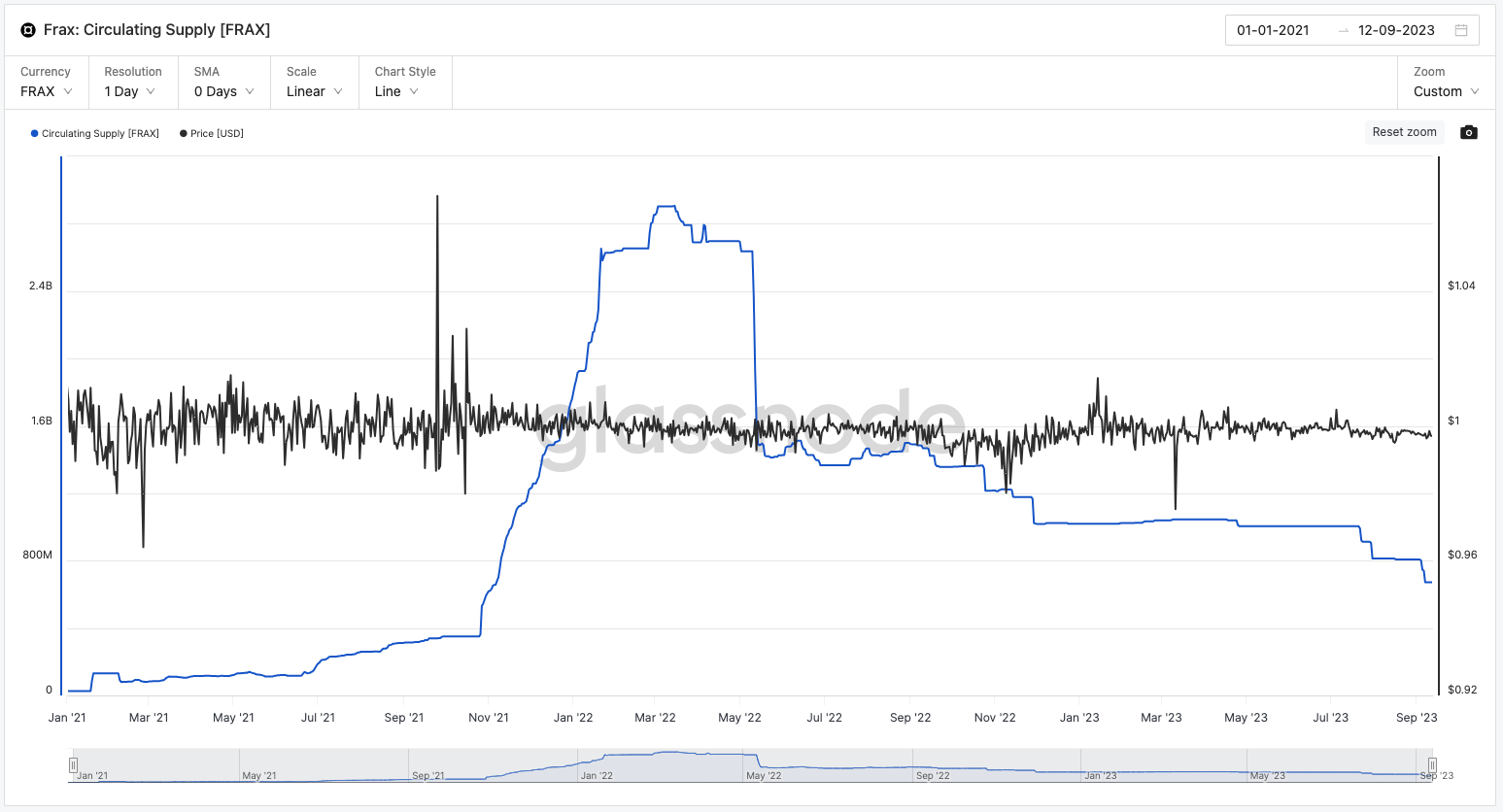

Frax: Significant Decline in Issuance

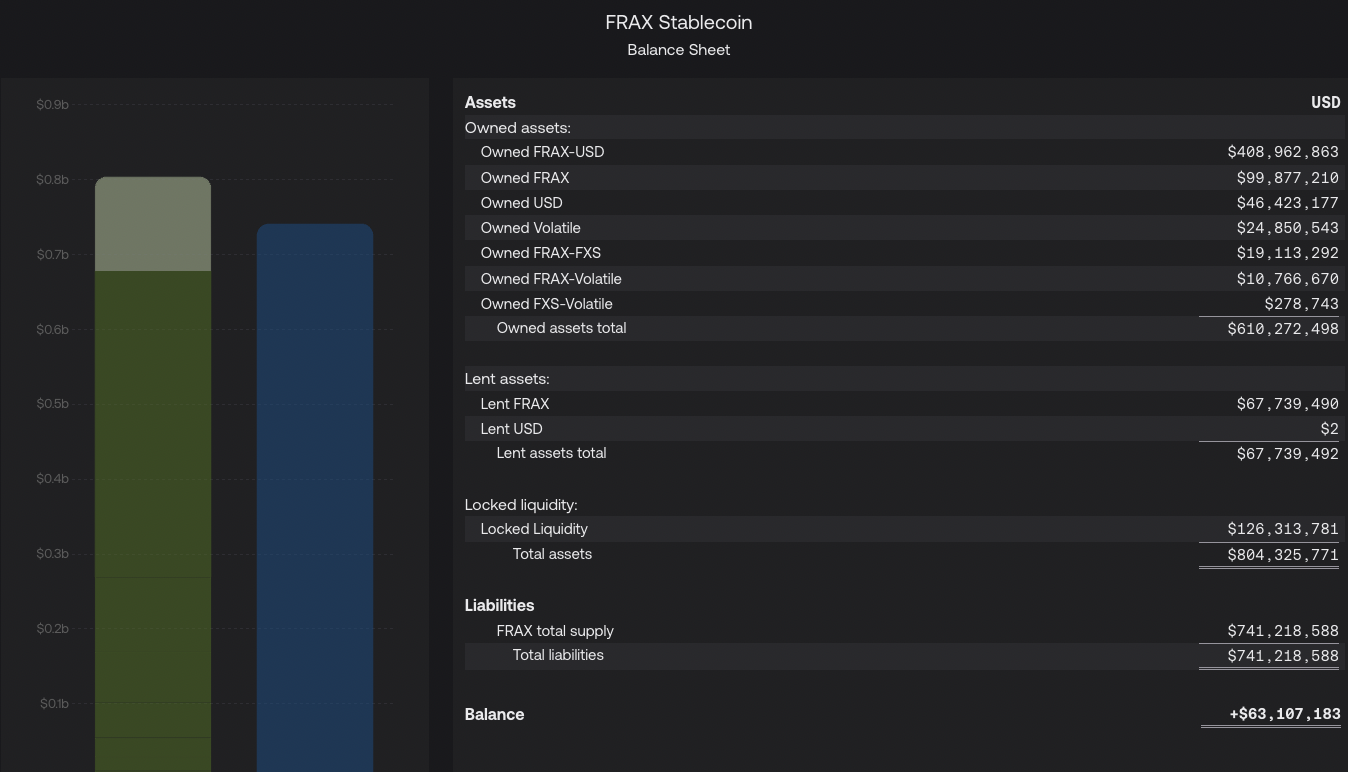

From the beginning, the majority of the reserves of the stablecoins issued by Frax Finance have been USDC. As shown in the figure below, since most of Frax Finance's reserves are the protocol-held FRAX-USD, which is the liquidity of FRAX with USDC and USDP on Curve. This means that a portion of the circulating Frax is held by the protocol, and USDC accounts for a considerable proportion of the remaining reserves. With DAI offering higher yields and being relatively safer, the issuance of the FRAX stablecoin can be easily affected.

According to Glassnode data, the issuance of Frax has decreased from 2.9 billion in March 2022 to 670 million currently, representing a 17.3% decline compared to the 810 million when Maker's EDSR took effect.

At the time of Maker's EDSR implementation, Frax founder Sam Kazemian proposed to collaborate with the American company FinresPBC to redeem USDC and USDP for USD to earn interest through the FRAX v3 RWA asset strategy. After deducting costs, the remaining profits generated for Frax by FinresPBC would be directly returned to the protocol.

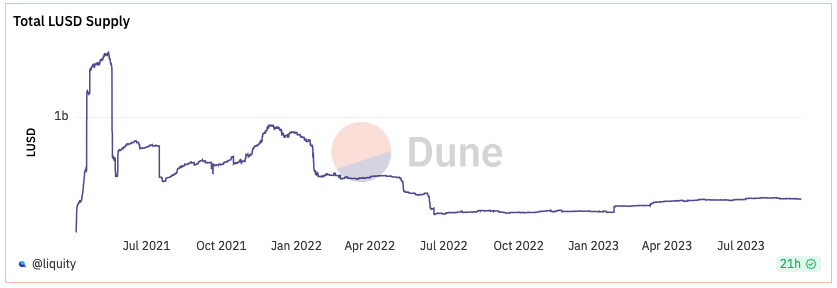

Liquity: LUSD Premium Turns Negative

As Maker gradually shifts towards RWA, Liquity's LUSD has become a representative project in the fully decentralized stablecoin space, supporting only ETH as collateral for minting LUSD.

Because Liquity currently only supports ETH as collateral, it must consider adding new features in the face of competition from forked products like Gravita and Lybra.

During the Stable Summit held in July, Liquity founder Robert Lauko announced the Liquidity V2 plan, which aims to balance decentralization, stability, and scalability. Liquidity V2 is expected to be publicly released in 2024 and will introduce leveraged and lending products, supporting staked ETH as collateral.

According to official data, the issuance of LUSD has decreased from 1.56 billion in May 2021 to 287 million currently. Compared to the 297 million when Maker's EDSR took effect, the decline is relatively small.

However, the impact on LUSD's price seems more significant. According to CoinMarketCap data, LUSD has remained in a negative premium phase for over a month, marking the first occurrence of this situation in the past year.

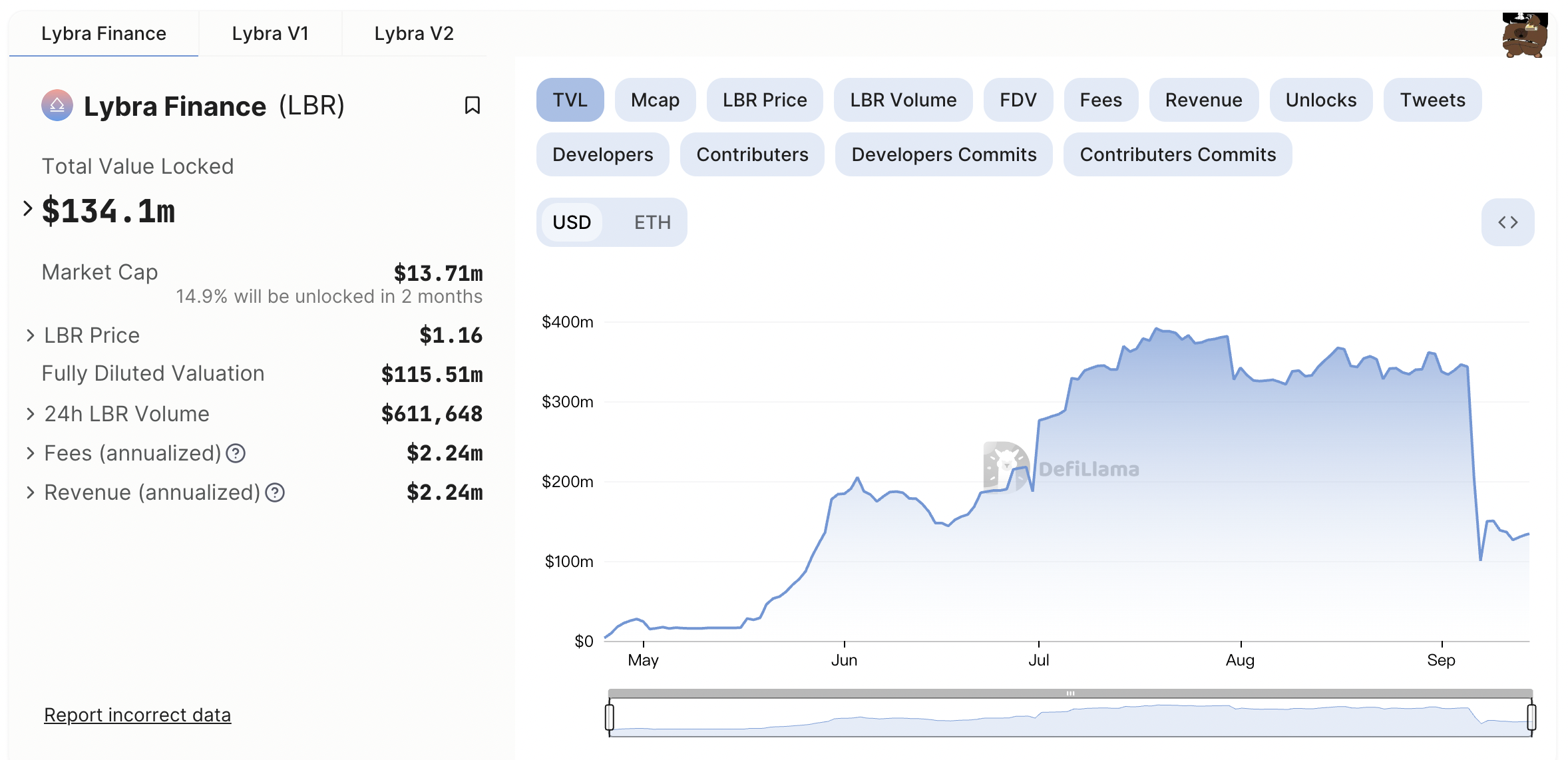

Lybra Finance: Over Half of Funds Withdrawn After Lybra V2 Upgrade

As for which is the better solution in the yield-bearing stablecoin space, US Treasuries or LSDFi? Currently, US Treasury projects seem to have the upper hand.

Lybra is a leading LSDFi project that supports minting eUSD using ETH staking derivatives as collateral. eUSD holders can earn higher yields than Maker's EDSR, but due to a significant recent decline in data, it is worth mentioning here. According to DeFiLlama data, the total value locked (TVL) of Lybra's V1 and V2 versions has dropped from $343 million on September 5 to $129 million currently. Lybra V2 was recently launched, which is the full-chain version of Lybra, supporting more collateral and allowing stablecoins to expand to other chains without sacrificing interest.

Similarly, according to CoinGecko data, the price of eUSD (OLD) was $1.04 on September 5, with a market cap of $184 million. However, as of September 13, according to Etherscan data, the issuance of eUSD (OLD) and eUSD was only 29.3 million and 36.02 million, respectively, with the combined total decreasing by more than half compared to before.

This indicates that during the migration from Lybra V1 to V2, most previous funds chose to leave directly. While it cannot be determined if this is due to Maker's EDSR, the primary income for users in Lybra still comes from liquidity mining subsidies provided by the project, and the appeal may have diminished as the governance token price has fallen.

Conclusion

With the development of LSDFi and the launch of Maker's EDSR, stablecoin holders may be more inclined to share yields from the stablecoins they hold, while other stablecoins that do not generate yields may be "bloodsucked" in the process, leading to reduced issuance or negative premiums.

Among the stablecoins observed by PANews, FRAX has seen a significant decline in circulation, LUSD's premium has turned negative, USDC has followed suit by allocating a 5% annual yield to holders in Coinbase, and the issuance of Lybra's eUSD has decreased by more than half during the migration from V1 to V2.

Risk warning Risk warning

Risk warning Risk warning