How do Ripple, Stellar, and Chainlink solve cross-border payment issues?

The future of payments is moving towards a hybrid model, and combining existing payment systems with digital currencies is the next step towards achieving comprehensive financial decentralization.

The future of payments is moving towards a hybrid model, and combining existing payment systems with digital currencies is the next step towards achieving comprehensive financial decentralization.Original Title: 《How Can Ripple, Stellar, And Chainlink Solve Cross-Border Payment Issues?》

Written by: HERCULES | DEFI

Compiled by: TechFlow

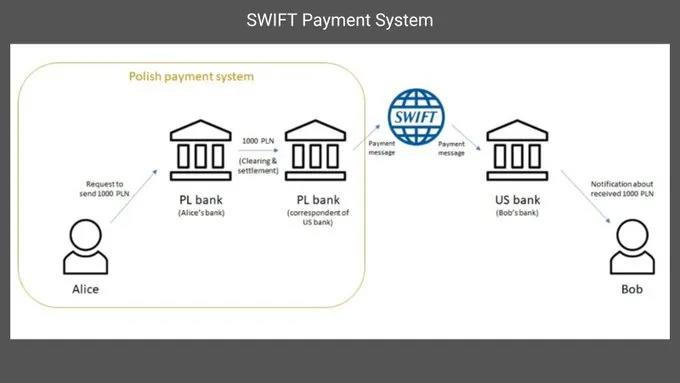

We know that $170 billion flows globally every hour. However, cross-border payments face issues such as high costs and slow transfers.

Globalization, market expansion, and technological innovation highlight the reliance on cross-border payments. However, existing solutions like SWIFT have two major problems:

Additional fees arise if payments must be processed through intermediary banks.

Transaction speeds are slow.

Both of these issues can be resolved by replacing reliance on intermediaries with direct transfers. Blockchain solutions like Ripple, Stellar, and Chainlink can facilitate cross-border transfers.

Stellar

Stellar connects financial institutions for cross-border payments using its blockchain network and IBM's World Wire platform. Compared to SWIFT, Stellar's native cryptocurrency Lumens (XLM) is used for faster and cheaper transactions.

Stellar aims to facilitate cross-border payments for small and medium-sized enterprises and individuals by using a complex system involving deposit institutions, stablecoins, and trading functionalities, thereby replacing SWIFT.

The platform employs blockchain technology and the Stellar Consensus Protocol to achieve an efficient infrastructure. Users deposit with Stellar-certified local deposit institutions, which are recognized by Stellar as "anchors."

Key Features of Stellar:

Fast Processing: 2,000 transactions per second, with cross-border payments confirmed within 5 seconds;

No Intermediaries: Direct transactions through self-triggered smart contracts;

Decentralized: Efficient transfers without reliance on centralized institutions.

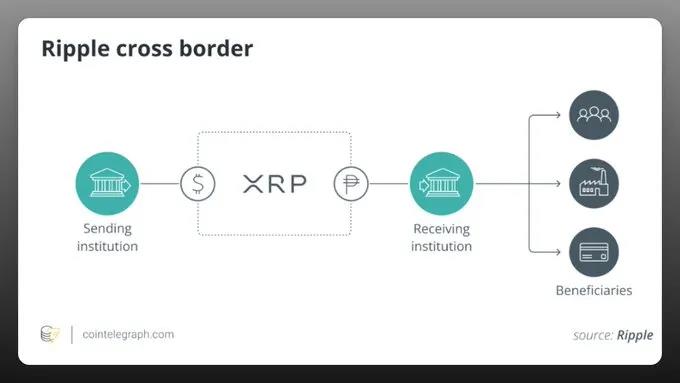

Ripple

Ripple collaborates with global banks and financial institutions to drive technology adoption and enable broader cross-border payment usage through XRP. Key partners include Santander Bank, American Express, SBI Holdings, and PNC Bank.

Ripple utilizes the XRP blockchain payment protocol to allow real-time, low-cost cross-border transactions. It eliminates the need for multiple intermediary banks, resulting in faster settlements and lower costs.

Given SWIFT's influence and the regulatory challenges Ripple faces, there is uncertainty about replacing SWIFT with Ripple. However, Ripple is an ideal choice when favoring decentralized cross-border payments.

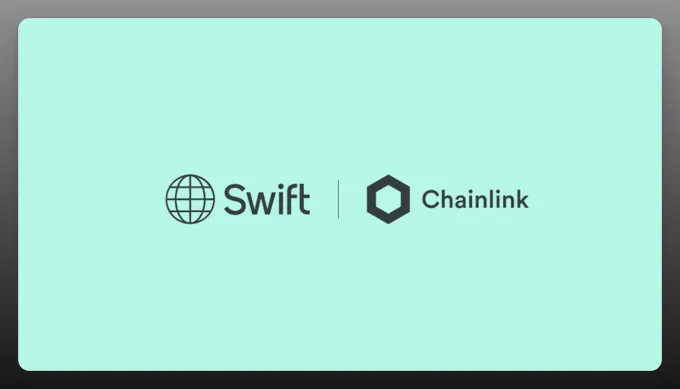

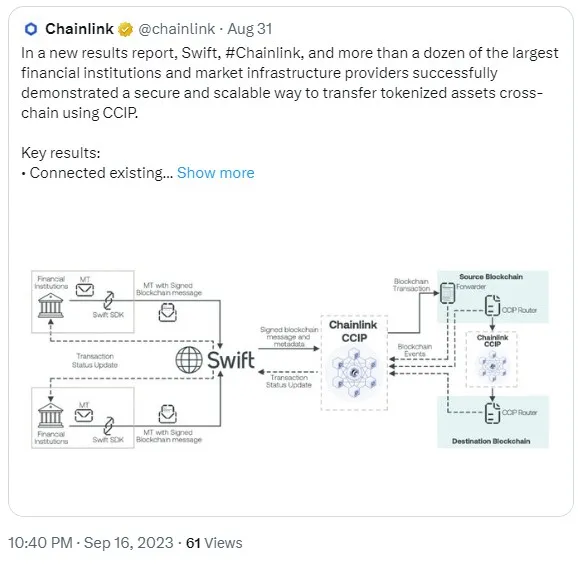

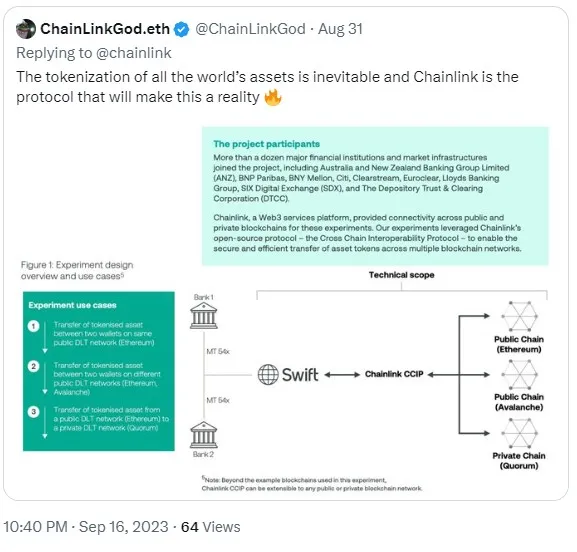

SWIFT is continuously evolving. It actively conducts experiments to highlight the importance of tokenization. SWIFT collaborates with financial institutions to demonstrate the significance of its network by facilitating the transfer of tokenized assets across multiple pathways.

Benefits of Tokenization

Tokenization is still in its early stages, with 97% of institutional investors confident that it will transform asset management. It will enhance efficiency, reduce costs, and provide investors with more options by fractionalizing ownership.

SWIFT has partnered with Chainlink to address the fragmentation of blockchain and improve the trading of tokenized assets.

Chainlink's Cross-Chain Interoperability Protocol (CCIP) has launched on the mainnet. It provides plug-and-play options for inter-chain token transfers, supporting both burn-and-mint and lock-and-mint methods.

By collaborating with Chainlink, SWIFT aims to enhance interoperability and user experience. This partnership streamlines access to multiple networks, reducing operational challenges and costs associated with tokenized assets.

Chainlink is leading the undeniable future towards the tokenization of all global assets.

Chainlink provides data transmission, token transfer, blockchain communication, and computing services. Key services for capital market tokenization include CCIP, proof of audited reserves, and functionalities for synchronizing off-chain events or data.

Chainlink brings over $8 trillion in transaction value to blockchain applications, secured by a decentralized oracle network operated by major enterprises like Deutsche Telekom, LexisNexis, and Swisscom. It maintains long uptime and tamper-proof security even during market volatility.

Conclusion

The future of payments is evolving towards a hybrid model. Combining existing payment systems with digital currencies is the next step towards achieving comprehensive financial decentralization.

Risk warning Risk warning

Risk warning Risk warning

Popular articles