Social Ponzi, can it recreate the glory of DeFi Summer?

Questioning Ponzi, understanding Ponzi, becoming Ponzi?

Questioning Ponzi, understanding Ponzi, becoming Ponzi?Written by: Deep Tide TechFlow

Friend.Tech is on fire.

This model, centered around KOLs, allows fans to buy and sell "shares" of KOLs. It’s not complicated and carries a hint of "Ponzi" flavor; however, in the hot spots and liquidity-scarce deep bear market, Friend.Tech has indeed created a wave of SocialFi excitement.

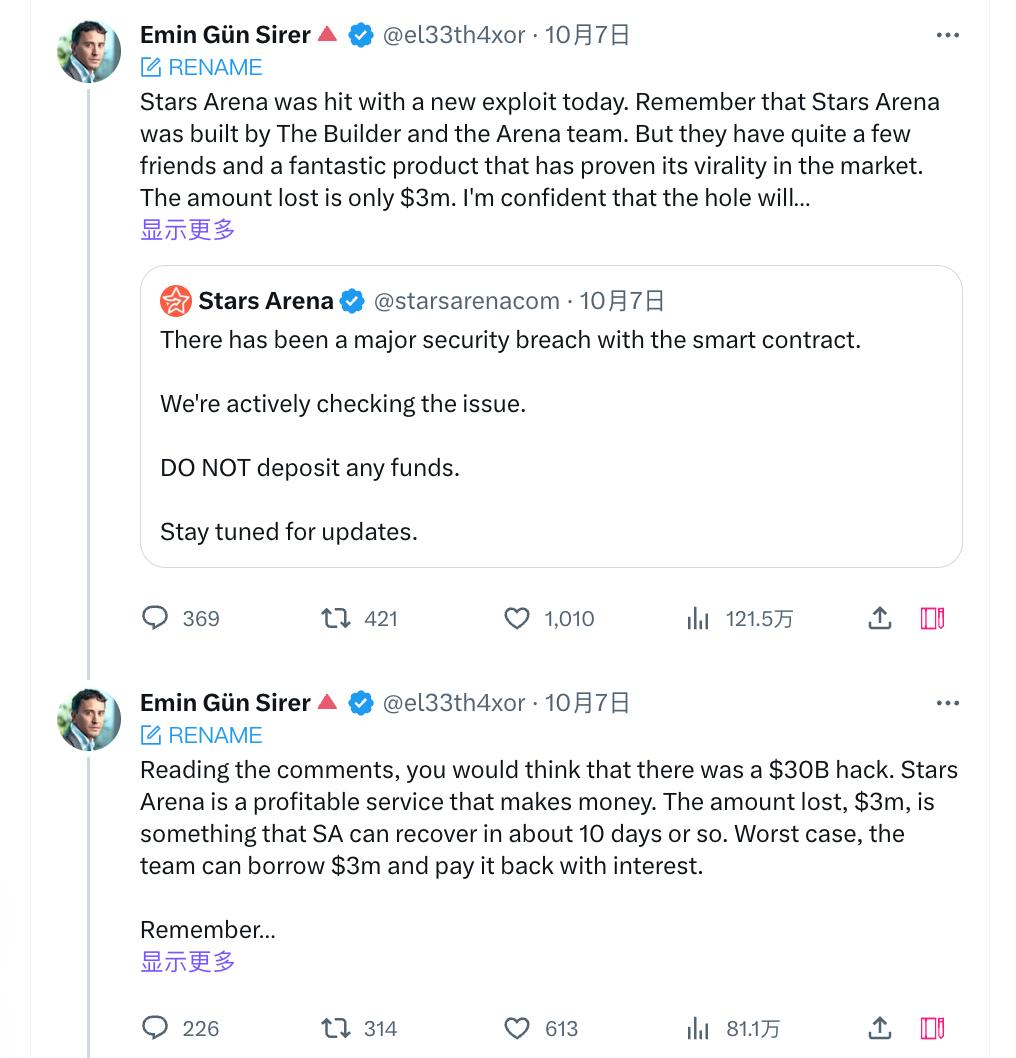

For example, in the past week, Star Arena on Avalanche quickly rose to prominence, remaining the focus of attention despite experiencing dramatic ups and downs, including the founder's endorsement and a contract vulnerability that led to a total loss of funds.

Meanwhile, the trend continues to spread:

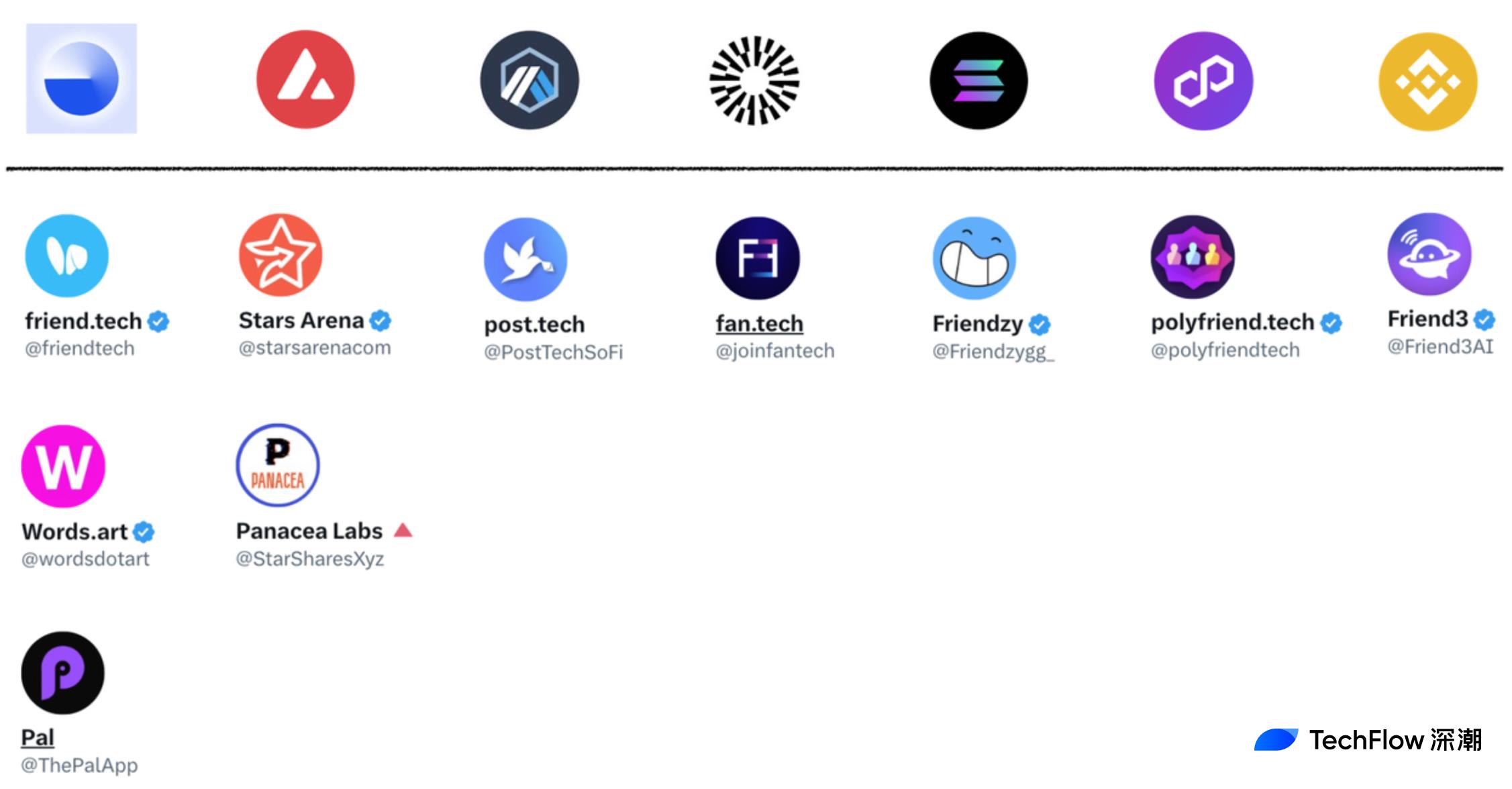

Starting from the Base L2, FT's clone projects have rapidly emerged on other ecosystems like Avax, Arbitrum, Solana, Polygon, and Bnb. These projects are making various improvements and innovations based on FT, trying to capture this hard-won heat;

Opening Twitter, a plethora of crypto-related topics and accounts are continuously discussing and introducing FT and other projects, creating a sense of FOMO that one might miss out on a fortune if they don't participate.

DeFi Summer, a Familiar Taste

The pursuit of yield, the emergence of clones, ongoing discussions… doesn’t all of this feel somewhat familiar?

Indeed, it’s easy to recall the DeFi Summer of 2020.

Chris, a partner at the well-known VC Placeholder, stated that social Ponzi is the new DeFi Summer and described the current development process of projects like FriendTech as similar to that of DeFi Summer:

An experiment --> influx of traffic --> viable model begins to sprout --> attract more attention to improve experience --> emergence of larger-scale applications --> involve others within 18-24 months.

If you carefully review the DeFi Summer from three years ago, you will find that this development path indeed feels familiar.

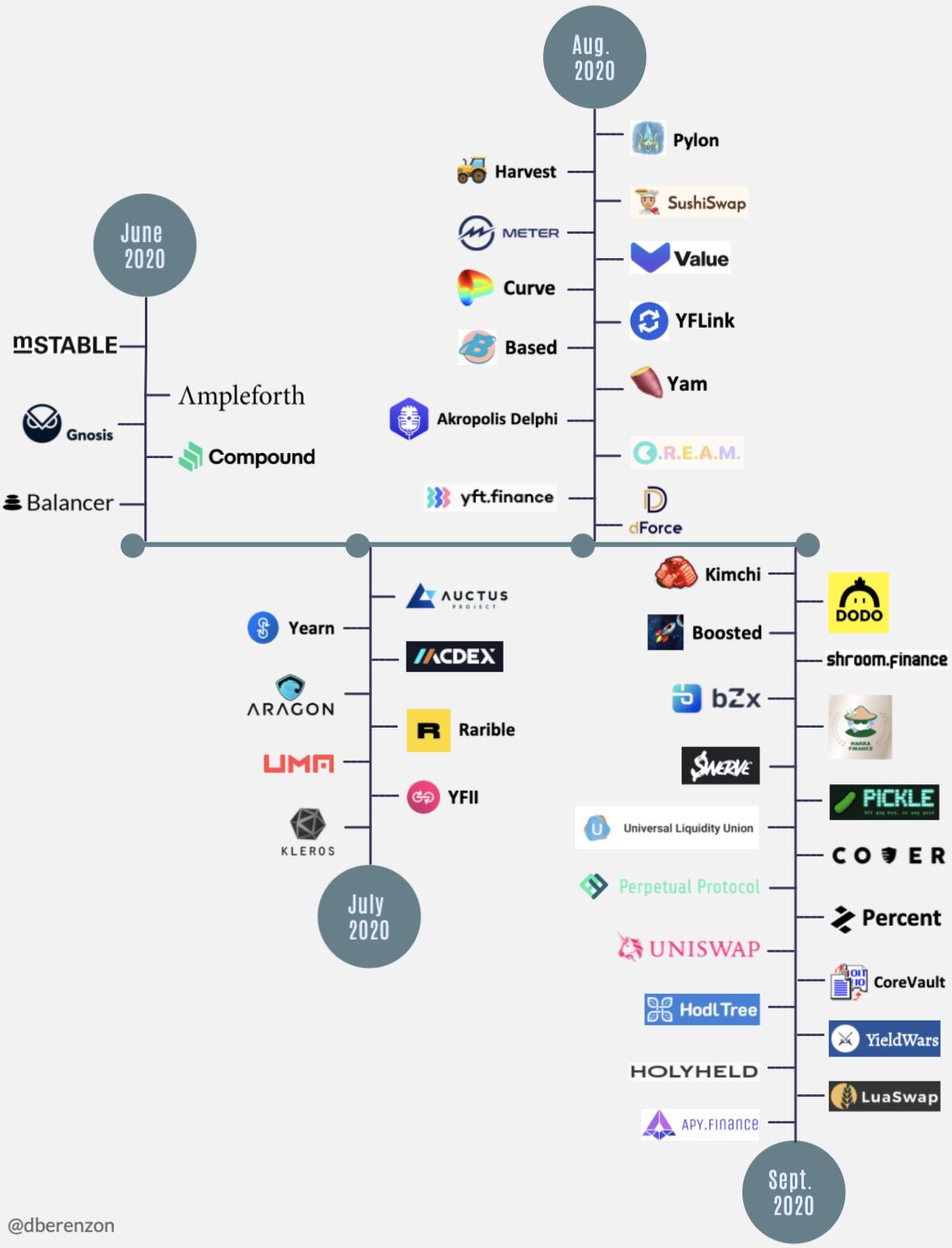

In June 2020, Compound implemented "liquidity mining" on a large scale, attracting numerous players to provide liquidity; subsequently, several different protocols discovered the viability of this model and began to borrow and improve the design of liquidity mining, tweaking tokens and economic models to attract more participants.

Ultimately, the total value locked (TVL) in the entire DeFi sector skyrocketed from $1 billion in June to $10 billion in October, with a dramatic increase in user numbers; at the same time, gas fees on Ethereum reached historical highs.

A concept of liquidity mining, a leading project, drove a vibrant summer, solidifying DeFi's position.

A concept of social Ponzi, a leading Friend.Tech, has sparked a wave of clones across different ecosystems; will it ignite the SocialFi craze? Practitioners seem to sense a similar flavor, eagerly anticipating the market turning point.

Thirst for Traffic, Igniting Flow

The recent rise of SocialFi, while seemingly following a similar development path as DeFi Summer, faces a harsher market environment -- the entire market seems more desperate for traffic than ever.

As the market turns bearish, various L2s have clustered together. With no significant differences in technology and performance, each L2 hopes to find a traffic driver to gain attention and liquidity in this competitive environment.

Thus, we saw Friend.Tech's emergence causing Base's TVL to soar, quickly gaining a solid foothold in the L2 competition.

This thirst for traffic is even more evident on "soon-to-be-outdated" L1s.

The founder of Avalanche, Professor Gun, has publicly expressed support and optimism since the emergence of Star Arena. Even when SA lost all funds due to a contract vulnerability, Professor Gun called for giving new applications some trial and error space, waiting for recovery and rebuilding.

Regardless of whether SA is officially developed by Avalanche or is a so-called national project, the founder's public endorsement highlights the traffic thirst of L1 public chains.

A phenomenal application brings the possibility of revitalizing a previously stagnant public chain ecosystem, which seems even more precious in the current spotlight on L2.

Moreover, the voices and involvement of key figures further validate the basic logic of FT and SA-type social products igniting traffic:

By attracting appealing expectations or incentives, traffic is drawn in to complete the product's cold start; then, using appropriate dissemination strategies, more traffic is ignited to join, increasing the network effect of social products.

Borrowing from the classic book "The Tipping Point," a product or topic needs to follow three major laws to become popular:

- The Law of the Few: For information to become popular, it must be spread by certain special individuals with social skills, energy, enthusiasm, and charisma.

- The Stickiness Factor: Once information becomes practical and meets personal needs, it becomes unforgettable.

- The Power of Context: The spread and popularity of information require a favorable external environment.

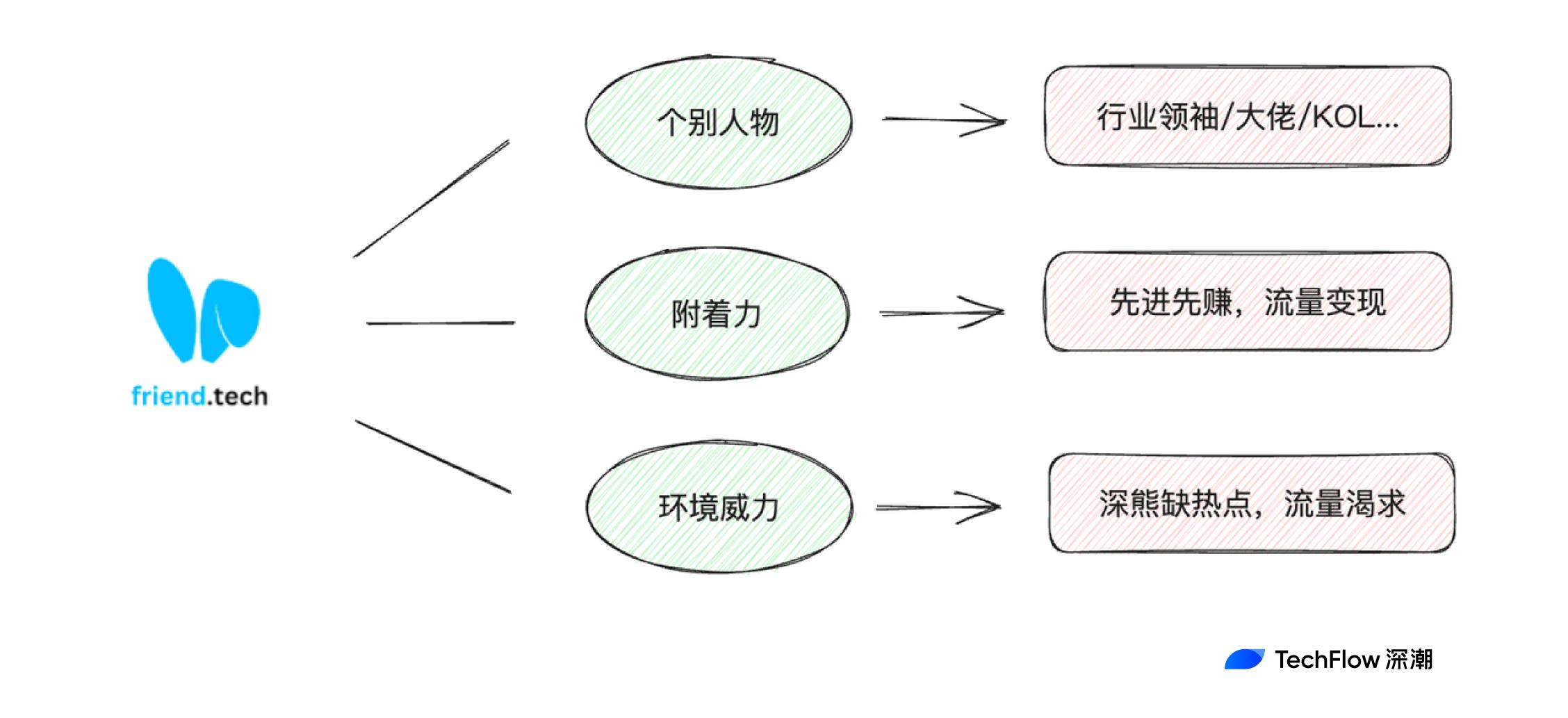

These three laws, when applied to SocialFi products like Friend.Tech, become more specific:

Under this dissemination logic, we can see more and more people joining Friend.Tech, with players who were previously observing starting to try it out under the continuous influence of key individuals and the appealing stickiness.

Under this dissemination logic, we can see more and more people joining Friend.Tech, with players who were previously observing starting to try it out under the continuous influence of key individuals and the appealing stickiness.

At the same time, users in FT are choosing to exit due to declining returns caused by the competition among bots, naturally providing space for numerous clones to absorb this overflow of traffic.

Clearly, Friend.Tech is the first, but it will not be the last. Clones are making minor innovations, enhancing experiences, or adding gameplay to better attract traffic, just like Sushiswap did to Uniswap back in the day.

Questioning Ponzi, Understanding Ponzi, Becoming Ponzi

Friend.Tech has made a good start in dissemination, but the question is whether it can sustain itself like DeFi Summer?

In comparison to DeFi's liquidity mining, while it is also a means of attracting users by providing yields, and earlier participants earn higher returns than later entrants, the income sources differ. DeFi products and LPs earn from transaction fees generated by other users, rather than simply the upstream earning from the downstream.

Social products like FT exhibit very obvious Ponzi characteristics, where early entrants are more likely to earn from latecomers, who may bear higher purchase costs.

Therefore, from an economic design perspective, FT resembles the once-popular StepN more than DeFi in certain aspects. Once there are no more users joining, will the entire chain become difficult to sustain, ultimately falling into a death spiral like most GameFi projects?

But let’s not forget that StepN, as a consumer-grade crypto application, once successfully broke the mold and gained immense popularity and user numbers. Since then, the crypto industry has not seen a similar level of consumer-grade application.

From this perspective, the Ponzi structure in StepN's economic design initially played a positive role in rapidly acquiring customers: those who run first will earn first; if you don’t believe it, you won’t come.

Today, when infrastructure is homogenized and abundant, and everyone is hoping that the social track can produce the next true consumer-grade crypto application, outright denial and questioning of the Ponzi structure in Friend.Tech is clearly not a practical choice.

Questioning Ponzi, understanding Ponzi, becoming Ponzi.

With the understanding that the Ponzi structure and Ponzi schemes are not equivalent, appropriately leveraging Ponzi to attract traffic has become a necessary path for crypto applications to achieve development.

In terms of experience, crypto applications cannot compete with mature Web2 products; when it comes to compliance, crypto applications walk the fine line between black and white; regarding demand, crypto applications do not have a popular and indispensable necessity.

So, how can users be visually impressed enough to take the step from non-use to use?

The current answer is likely still incentives and yields. The earlier you come, the more you earn, using the profit effect to attract more users. This does have a bit of a Ponzi flavor, but for crypto, it is an unavoidable part of application development.

Success and failure both stem from Ponzi.

History shows that applications or projects that rely solely on Ponzi without continuously providing more external value cannot consistently attract user participation; they either rug pull or passively fade away.

In this regard, Ponzi is a means, not an end.

Whether Friend.Tech or Star Arena can provide more functions and gameplay beyond yields, retaining users with practical features after successfully launching to offset the "latecomers suffer" issue brought by the Ponzi structure remains to be seen.

Will the Splendor Reappear?

Can social Ponzi recreate the splendor of DeFi Summer? The author believes it is quite difficult in the short term.

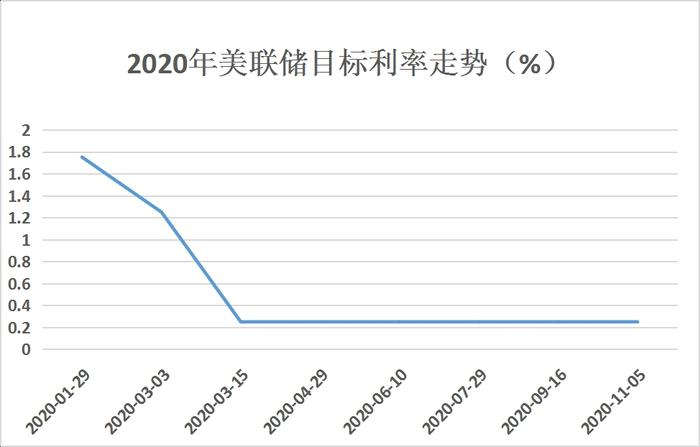

First, the macroeconomic environments of the two are different. In 2020, the Federal Reserve cut interest rates to 0 twice in March and launched a $700 billion quantitative easing (QE) plan, flooding the market and contributing to the crypto market's heat. The following chart shows the period of low interest rates coinciding with the DeFi Summer.

Currently, we are facing tightening liquidity, withdrawal of hot money, and the Federal Reserve's interest rate hike cycle, with VCs also throwing olive branches to the AI industry. For SocialFi to remain hot, it does not have the same loose environment as back then.

Second, the sources of income differ. As mentioned earlier, the earnings of DeFi products and LPs come from transaction fees generated by other users, not simply the upstream earning from the downstream; whereas Friend.Tech's current Ponzi is very evident, and the presence of automated bots has sharply increased costs for latecomers, making it a less healthy profit model for users, leaning more towards zero-sum games.

Once there are no continuously updated features and more players entering, the likelihood of the fortress being breached from within increases.

Finally, the degree of demand differs. DeFi is inherently financial, with the product's orientation being how to earn yields more freely, efficiently, and conveniently, which is somewhat of a "transactional necessity";

Whereas SocialFi's focus is theoretically on Social rather than Fi; aside from yields, ordinary users have no urgent need to choose a crypto application that is clearly inferior in functionality and experience to mainstream social software. The current situation where Fi overshadows Social is unlikely to change in the short term, and the possibility of a mass exodus after the speculative effect diminishes is greater.

However, it cannot be denied that today's social Ponzi has succeeded in customer acquisition, and the functions presented are by no means the ultimate form.

Rather than expecting them to recreate the splendor of DeFi Summer, it might be better to hope that they can create splendor through new paths.

Risk warning

Risk warning Risk warning

Risk warning