RWA Data Report: The Driving Force Behind Blockchain Adoption

The main challenge faced by RWAs is to cope with the current global regulations, either making regulatory laws more favorable to crypto assets or the protocols having no choice.

The main challenge faced by RWAs is to cope with the current global regulations, either making regulatory laws more favorable to crypto assets or the protocols having no choice.Author: Jose Oramas

Compiled by: Shenchao TechFlow

RWAs are expected to become one of the dominant forces behind blockchain in the coming years. This year alone, the total value locked (TVL) in RWAs has doubled, increasing from $1.25 billion to over $6 billion, making it one of the fastest-growing areas in DeFi.

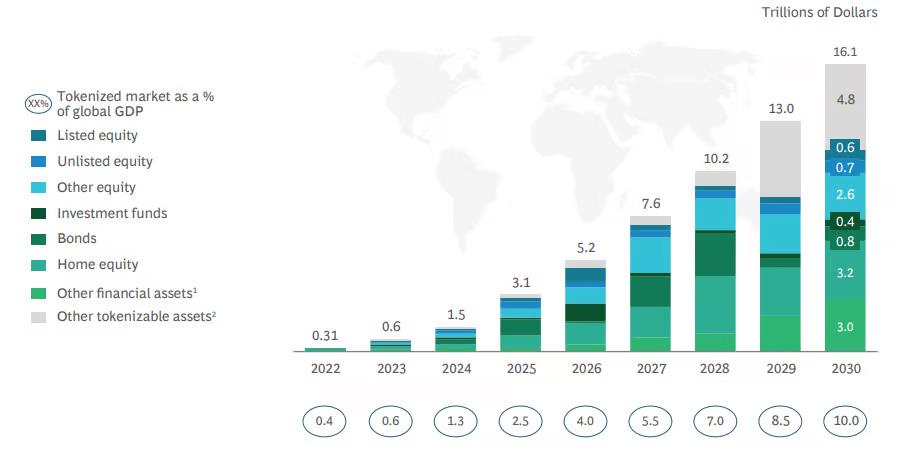

This explosive growth is primarily attributed to the emergence of new sources of yield, including tokenized U.S. Treasuries, corporate bonds, ETFs, and the rise of on-chain credit in emerging markets. RWAs have also attracted a wave of new institutional capital into DeFi; according to data from the Boston Consulting Group, 97% of institutional investors believe tokenization can fundamentally change asset management, creating a $16 trillion opportunity by 2030.

In this report, we will review these new sources of yield, current market leaders, and the benefits of tokenization. We will also discuss future legal challenges and the projected scale of the tokenization market by the end of the century.

Current Growth: What Stage Are We In Now?

This section will review the major categories of RWAs in terms of growth, including on-chain credit, tokenized Treasuries and bonds, and real estate, as they have seen the most significant growth in dollar amounts and user activity.

On-Chain Credit Resurgence

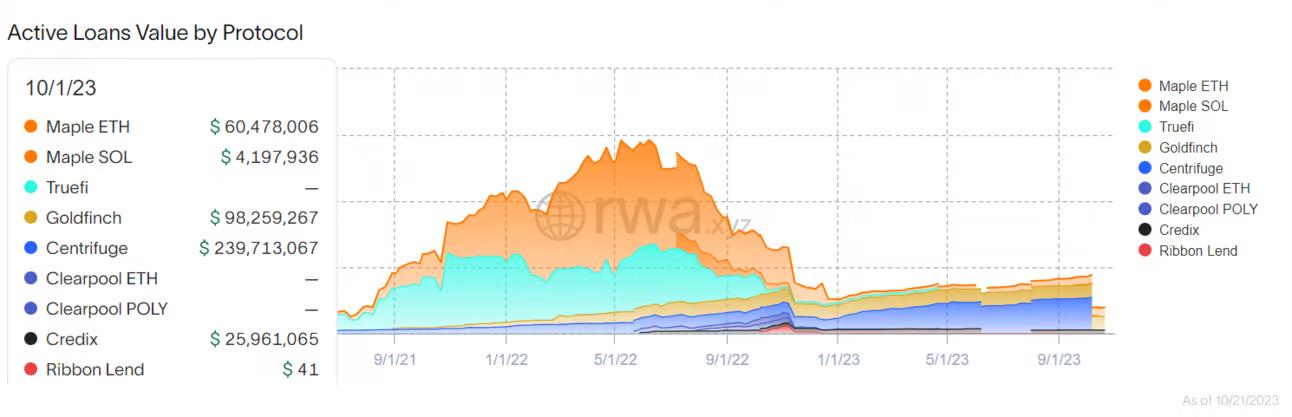

On-chain credit has grown by 84% this year, increasing by $210 million from January 1 to September 30. Centrifuge accounts for 70% of this growth.

Several on-chain credit protocols that were market leaders a year ago have essentially been eliminated in 2023, such as Maple, which once claimed nearly $1 billion. However, Maple is the second-largest contributor to on-chain credit growth, with its active loan value increasing by approximately $60 million as of the third quarter.

But competition is now fiercer; new market leaders are offering borrowers and lenders higher yields and a broader range of investment options. Centrifuge's TVL is now close to $250 million, a 60% increase since May of this year.

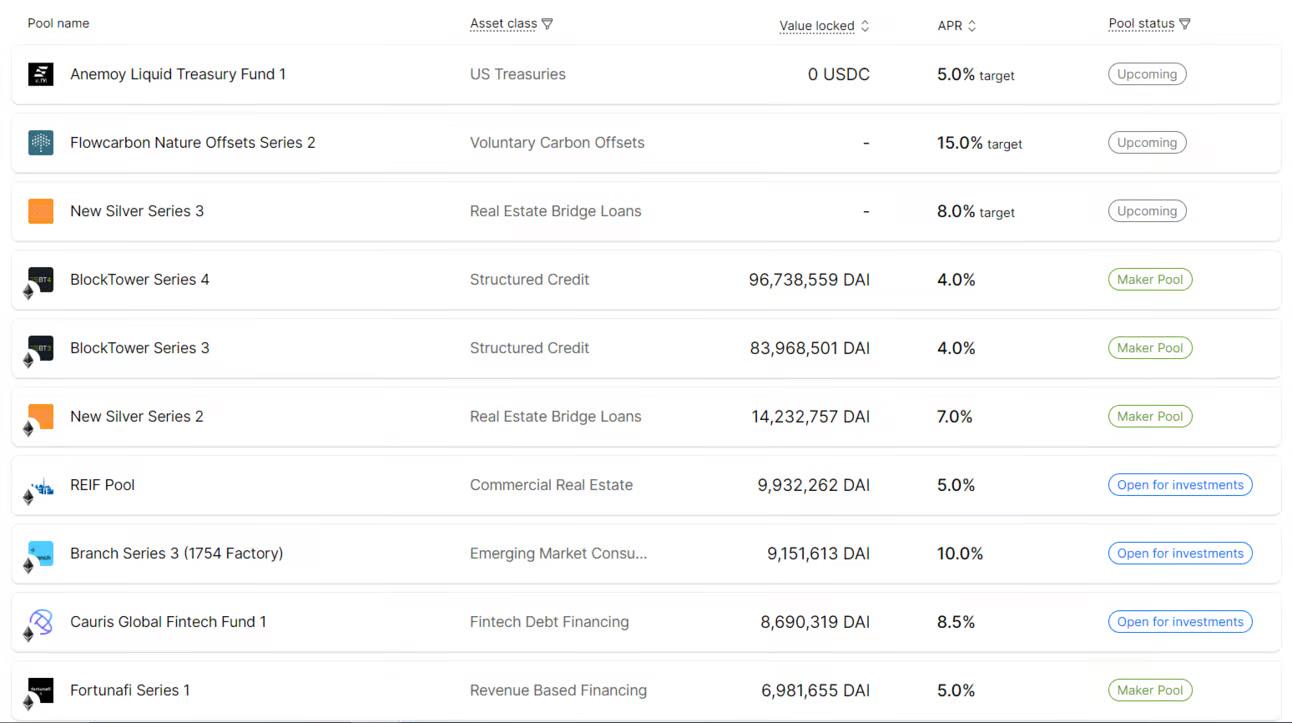

In this example, various RWA pools in Centrifuge track real estate, carbon credits, Treasuries, and emerging markets, providing returns of 7% to 10%. Some even reach 15%. As mentioned, the average APY in DeFi is below 4%, and in protocols like Aave, it can sometimes dip below 3% and 4%.

Regarding the risk exposure of private credit loans, Africa and Asia are currently the most active borrowers in on-chain credit. Kenya has the largest loan amount at approximately $73 million, followed by Nigeria ($70 million), the Philippines ($53 million), and India ($40 million).

Most of these countries are considered emerging economies, with a majority of citizens and small businesses being underbanked. Due to the often underdeveloped financial infrastructure in these countries, obtaining traditional loans is challenging.

Protocols like Goldfinch and Credix incentivize users to deposit stablecoins like USDC and then lend them to businesses in emerging markets. For example, most of Goldfinch's transactions are made with fintech initiatives in Southeast Asia and Africa. All income is used to provide additional support to these startups that are seeking funding to offer financial services to millions of underbanked citizens and businesses.

In such transactions, fixed APYs are often above 10%, far exceeding what most DeFi lenders can currently offer. This is because the yields come from real-world assets, and their portfolios are strategically collateralized off-chain.

What Can Be Expected from On-Chain Private Credit?

On-chain credit is similar to Lido and its dominance in the liquid staking sector. Protocols like Goldfinch have seen almost no growth year-over-year, with Credix being an exception. Thus, Centrifuge and Maple are the largest contributors to this $210 million growth and are likely to remain leaders in the next 12 months.

However, on-chain private credit has dropped 70% compared to last year's all-time high. According to data from RWA.xyz, there are currently $561 million in active loans, far below the $1.54 billion seen in May 2022.

It is likely that the accelerated interest rate hikes at the beginning of 2023 affected the demand for on-chain loans, as private credit protocols rely on both liquid and illiquid real-world assets.

That said, the next 12-24 months will be crucial for on-chain credit protocols. Although the Federal Reserve has taken a more dovish stance, if the U.S. reports a stronger economy and a tighter labor market, it may change its monetary policy, which will affect the on-chain credit sector, as we saw last year.

Treasuries and Bonds

RWAs based on Treasuries and corporate bonds have seen explosive growth in value this year, increasing by nearly $700 million so far, primarily distributed across Ethereum ($339 million), Stella ($323 million), and Polygon ($230 million), with the remainder spread across L1s like Solana.

Ondo Finance, Franklin Templeton, and Matrixdock are the market leaders, accounting for nearly 90% of all tokenized Treasuries.

Why are Treasuries so attractive to cryptocurrency users? Consider the following points:

Throughout 2023, the median APY in DeFi has remained below 3%.

The number of active developers in crypto projects and on-chain is at a three-year low.

Overall, the total value locked in DeFi has decreased by 30% year-over-year.

Cryptocurrency users are seeking higher yields. Liquid markets such as bonds and Treasuries offer better returns, so it is not surprising that the growth of RWAs is primarily due to protocols that tokenize and track U.S. Treasuries, corporate bonds, and indices.

Let’s review some of the major Treasury issuers in the RWA sector:

Ondo Finance currently has a market cap of approximately $160 million. Its flagship product is USDY, a tokenized dollar backed by U.S. Treasuries and on-demand deposits, allowing users to earn yields on U.S. Treasuries, money markets, ETFs, and high-yield corporate bonds.

Franklin Templeton is more like a traditional financial company, but when it began experimenting with tokenization, it became an advocate for crypto, alongside WisdomTree. In January of this year, the issuer started with about $100 million in assets. Now, that figure is approximately $310 million.

stUSDT is also a prominent Treasury issuer. However, a significant amount of suspicious on-chain activity and Justin Sun's centralized control have led to criticism of stUSDT, raising concerns about its long-term sustainability.

Real Estate

On-chain real estate has increased by $90 million this year, showing less growth compared to the dollar value in the third quarter.

RealT is currently the market leader, with its TVL increasing from $62.5 million to $89 million so far, a growth of 30%.

RealT is an Ethereum-based protocol that offers decentralized real estate investment and a wide range of options for buyers and investors. It now holds over 50% market share.

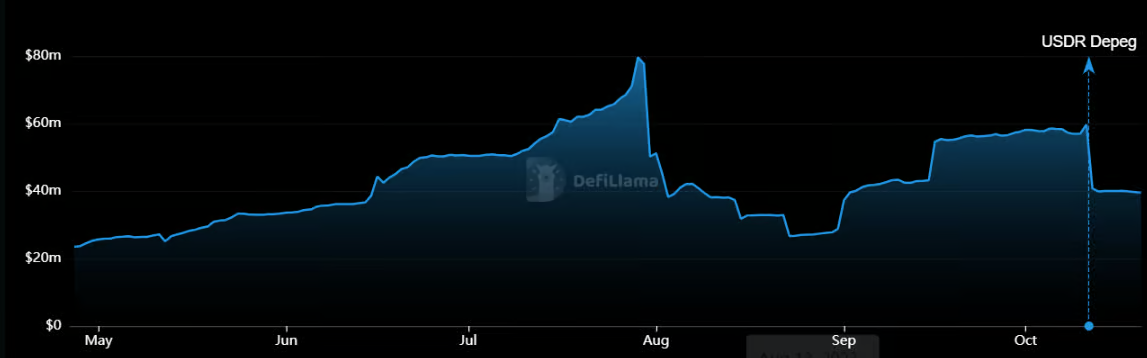

However, Tangible was recently the market leader, but after USDR was unpegged in October of this year, the protocol's TVL dropped from $60 million to $39 million.

Tangible leveraged USDR, a stablecoin that relies on the RWA narrative. It is claimed to be primarily backed by real estate investments. These assets are considered illiquid, making them ineffective in a bank run scenario. When it collapsed, it was too late to drive it back up.

Outlook: How Big Can the Tokenization Market Grow?

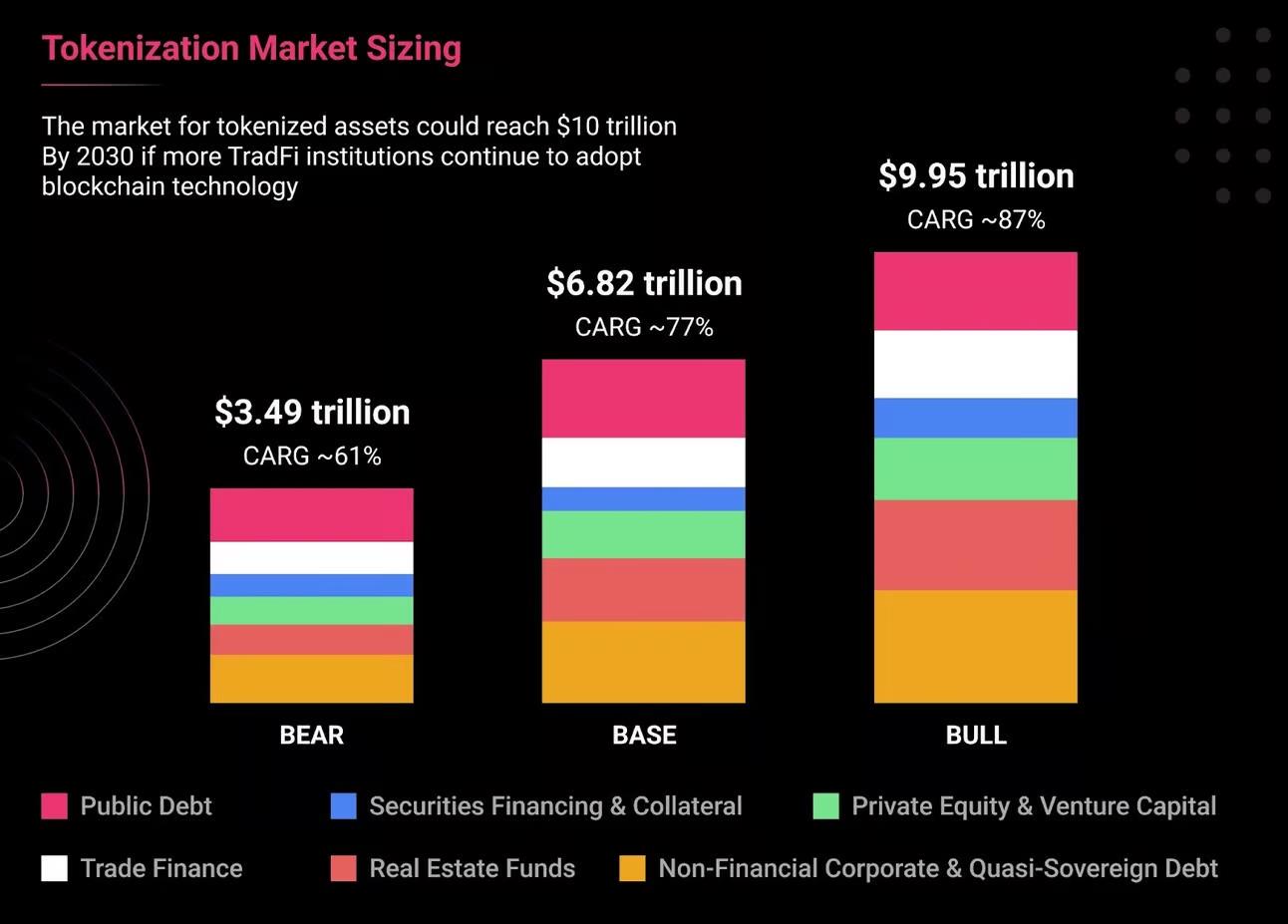

Industry reports suggest that the tokenization market could reach approximately $35 trillion even in the worst-case scenario (a prolonged bear market), and according to 21.co, it could reach $90 trillion in a bull market scenario.

Meanwhile, the Boston Consulting Group estimates that the tokenization of illiquid assets could become a $16 trillion business opportunity, accounting for 10% of global GDP.

As of October, the total valuation of the global asset market is approximately $900 trillion, led by real estate ($330 trillion), bonds ($300 trillion), and equities ($120 trillion). As of October 20, the total market capitalization of the cryptocurrency market is currently estimated at $1.2 trillion. If RWA protocols can capture at least 1% of that market share, the DeFi sector would gain approximately $9 trillion in capital and liquidity, nearly nine times the current market cap of the crypto market.

That said, the tokenization market is just a small part of the global asset market. The recent growth of the tokenization market and RWA protocols can be seen as evidence of the potential large-scale application of blockchain technology. We have seen increased interest from high-level institutional investors and international financial entities. On October 13, members of the International Monetary Fund, bankers, and fintech executives discussed the legal challenges and potential uses of tokenization.

Why Are Traditional Financial Institutions So Interested in Tokenization?

Tokenization can lower barriers and address many operational efficiency issues that the industry faces today. The main advantages of tokenization and blockchain technology include:

Higher accessibility and liquidity

Reduced transaction costs by minimizing intermediaries

Increased transparency

Programmability can provide new investment characteristics and operational options for new issuers.

As we mentioned, Treasuries and real estate occupy the largest share of the total market capitalization of global assets. These income-generating assets do not have the same liquidity advantages, as real estate is often considered a highly illiquid market, primarily due to limited affordability, regulatory barriers, and lack of information. Tokenization can be used to offset these frustrations:

Tokenization eliminates intermediaries, and putting assets on-chain means they can be transferred 24/7.

It is fully transparent, with all information stored on the blockchain and accessible for viewing.

It provides higher accessibility and a better operational framework for fractional ownership.

As evidence of this ongoing institutional interest, the U.S. post-trade financial services company DTCC, with total assets exceeding $40 billion, is collaborating with Chainlink on a blockchain interoperability project for Swift.

Who Are the Main Users of RWA Protocols?

One of the main drivers of growth in RWAs is that crypto-native users are seeking better yield-generating opportunities than simply staking their governance tokens in protocols. Therefore, much of the demand for RWAs is driven by native crypto users.

It is worth noting that WisdomTree and Franklin Templeton have achieved considerable success in RWAs. As two veterans of the traditional financial industry, we can expect new users to join, such as institutional clients or everyday individuals. The key here is that the yields in RWAs are easier to explain compared to those in the traditional DeFi ecosystem, which reaffirms trust and simplicity in the minds of users.

Risks and Legal Challenges of RWAs

Investment opportunities in RWAs depend on the tokenization of assets and their distribution; the platforms that will dominate the RWA narrative are those that provide infrastructure for RWAs, such as compliance protocols (which will play a larger role due to current laws in various jurisdictions) and asset providers. This brings a range of new challenges but also offers opportunities for a broader investor base.

However, there may be some nuances when we talk about adoption. The success of RWAs will largely depend on how these protocols handle/adapt to current regulations, as long as the laws remain unchanged. So far, Switzerland is the only country that has established clear crypto laws. That said, compliance protocols and infrastructure will become more critical than ever on the path to mainstream adoption.

With the rise of RWAs, compliance protocols, audits, custodians, and on-chain oracles will become more prominent. Audits will be an important part of this puzzle, as they can verify on-chain assets and rebuild trust for investors. Meanwhile, on-chain oracles will need to input off-chain data into the protocols. Additionally, compliance protocols like Tokeny are providing legal guidance and infrastructure for seamless onboarding and asset management operations.

Another example is Quadrata, a platform that offers technology called web3 Passport, allowing businesses and investors to connect their wallets to identity passports.

Final Thoughts: The Role of RWAs in Blockchain Adoption

We have analyzed how RWAs can bring billions (and potentially trillions in the best-case scenario) of capital to the DeFi market, and how tokenization can strengthen multiple industries, such as housing, supply chains, finance, and banking, among others.

RWAs are targeting a large market that requires significant liquidity. This liquidity can be obtained by seeking large institutions. However, institutions will not come to DeFi unless they are confident they are operating within legal constraints. Another risk is the vulnerabilities in smart contracts, which is why auditors and infrastructure protocols will play a larger role in this ecosystem.

However, the significant open interest from investors and traditional financial institutions indicates that the RWA sector has great potential.

The main challenge facing RWAs is navigating current global regulations. Either regulatory laws will become more favorable towards crypto assets, or protocols will have no choice but to adapt to the current rules and attempt to navigate around them. So far, Switzerland is one of the few countries that has successfully established a good structural environment for crypto assets.

Risk warning

Risk warning Risk warning

Risk warning