SignalPlus Macro Analysis Special Edition: Deteriorating, A Rapid Decline

The situation has changed significantly in just a few days.

After listening to numerous central bank and Federal Reserve officials discuss the timing of interest rate cuts, combined with the escalation of geopolitical risks, the risk markets have been hit by an unexpected chill.

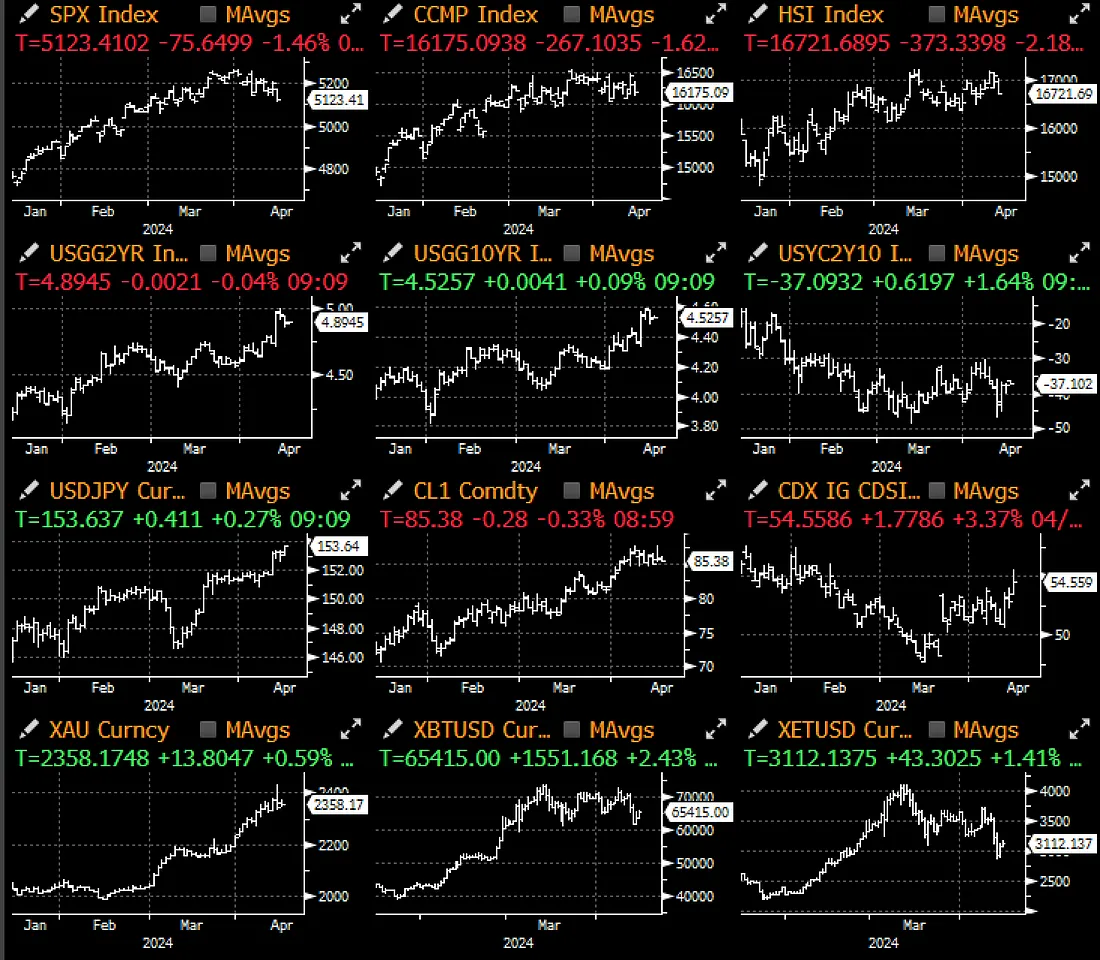

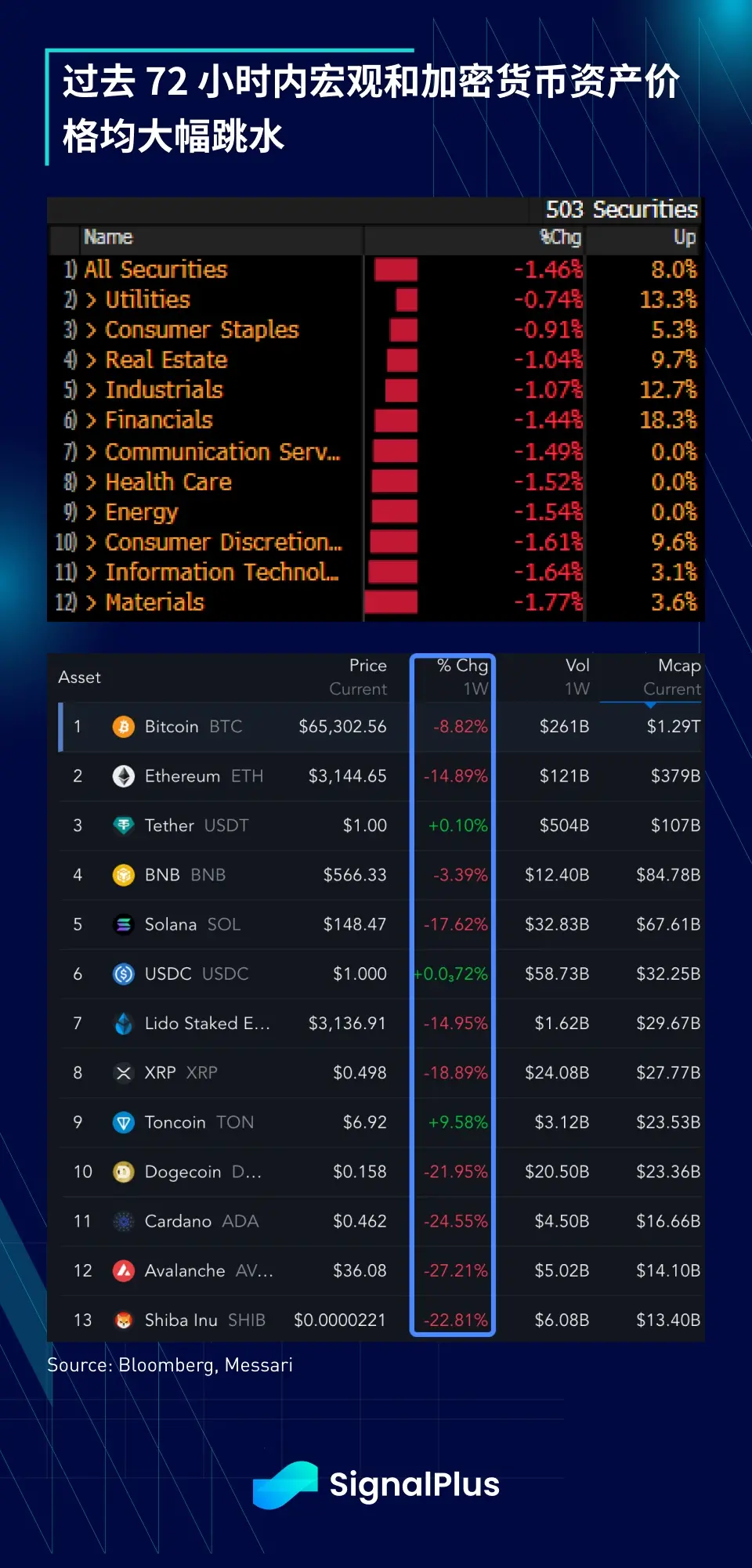

SPX fell 1.5% (with 92% of its constituents declining, and every sector showing losses), U.S. Treasuries and the dollar saw a surge in safe-haven buying, while cryptocurrencies suffered losses of over 10%, with BTC plunging from $69,000 last Friday to $59,000 yesterday, before recovering about half of the drop.

Following a series of unfriendly inflation data, last Friday's economic data remained unkind, with China's trade data coming in significantly below expectations (exports -7.5% vs expected -1.9%, imports -1.9% vs expected +1.0%), while the U.S. Michigan consumer sentiment survey (current and expectations indices missing forecasts, inflation expectations unexpectedly rising) showed some signs of "stagflation."

The technical trends of the major indices have clearly turned negative, with the China CSI 300 index failing to break above the 200-day moving average, and SPX nearing a breach of the 200-day moving average for the first time since the fourth quarter.

According to JPM data, the current cash allocation of traditional investors has returned to a decade-low, a time when fiat deposit interest rates were still around 0%. Two and a half quarters of continuous gains have prompted investors to fully invest, even "going all in" on high beta investments, leaving the market with almost no buffer to face further stock sell-offs.

That said, according to JPM's research, assuming the economy does not fall into recession, the current SPX trajectory is quite similar to the trends observed after previous interest rate hike cycles ended. Of course, the key assumption is that the economy will not enter a recession, and fortunately, the current economic situation still appears to be so.

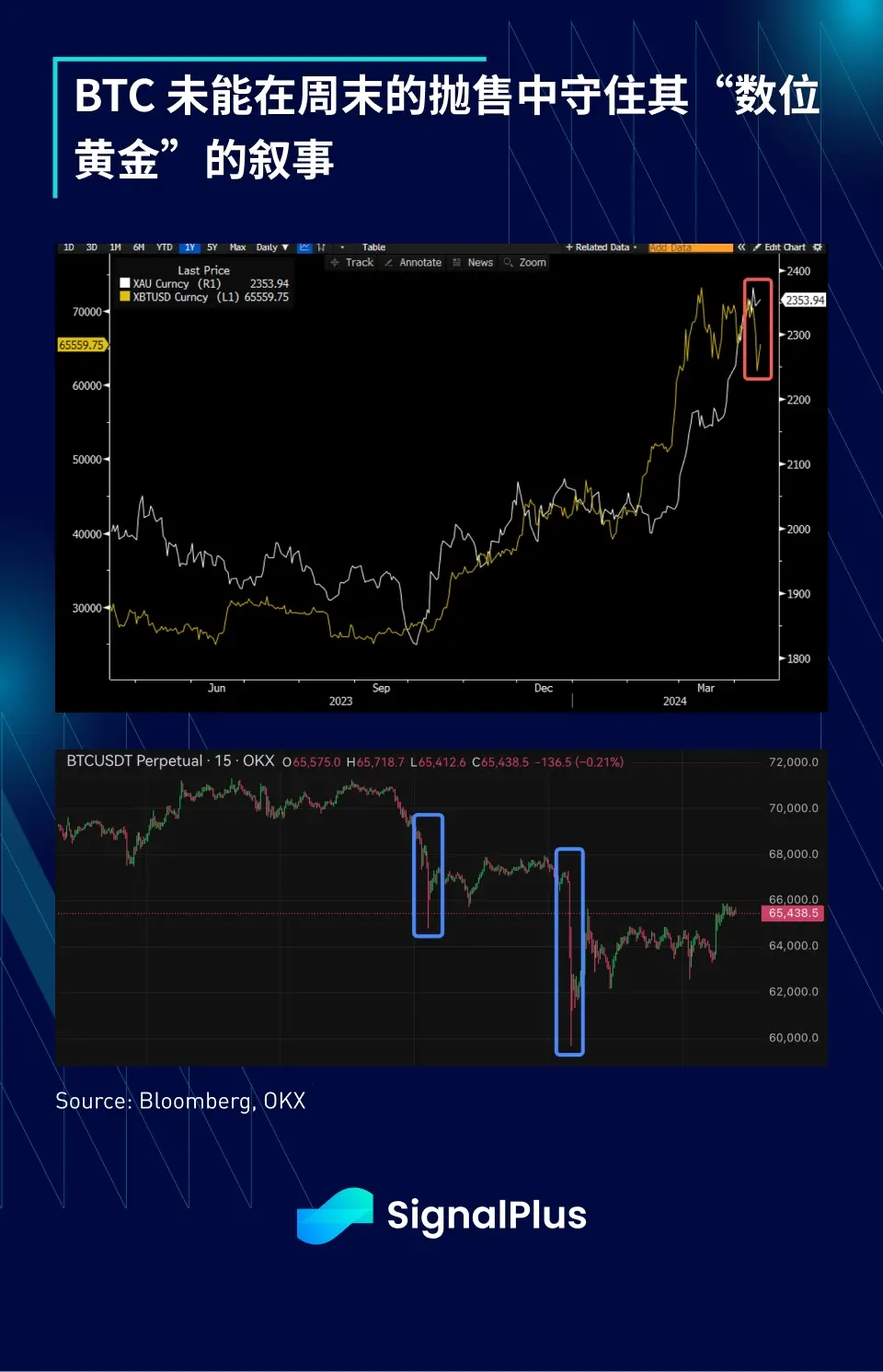

Returning to the geopolitical front, the situation remains highly volatile. Notably, in the past few trading days, while U.S. Treasury yields and stock prices have risen, spot gold has also increased, which is a rare occurrence, as if gold has sensed that tensions are about to escalate, becoming a target for safe-haven buying, while other asset classes are caught off guard.

Speaking of the shift to safe investments, BTC (disappointingly) failed to maintain its "digital gold" narrative, as BTC's price plummeted over 10% in just a few minutes, leading to the ruthless liquidation of over $1 billion in leveraged long positions, with on-chain DEX experiencing the largest long liquidation in over a year.

Although prices eventually rebounded (due to some signs of the U.S. easing tensions), the damage to the technical aspects of cryptocurrencies has already been done, with technical charts showing a downward breakout, and the impact on alt-coins has also been significant, with the top 20 coins experiencing weekly declines of 20-30%, while ETF inflows have begun to slow.

As an old trading adage goes, events themselves rarely lead to sharp price fluctuations, but they do reveal the current positions and risk buffers of market participants. Let's see how we recover from this setback; as we have repeatedly emphasized, risk management is always key, and usually, those who can hold on until the end will emerge as winners.

Risk warning Risk warning

Risk warning Risk warning