Is a Bitcoin sell-off coming? How Smart Money is responding based on on-chain data

OKLink data shows that in the past two months, the unit hash rate revenue of the Bitcoin network has repeatedly fallen below $0.05. Although there were brief rebounds during this period, it has now fallen back to a relatively low point.

OKLink data shows that in the past two months, the unit hash rate revenue of the Bitcoin network has repeatedly fallen below $0.05. Although there were brief rebounds during this period, it has now fallen back to a relatively low point.Author: Jason Jiang, OKG Research

The miner community plays an important role in the Bitcoin network, but due to the impact of halving events and a significant reduction in transaction fees after concepts like inscriptions and runes have calmed down, the income situation for miners has not been optimistic recently, with unit hash rate earnings reaching an all-time low. According to OKLink data, in the past two months, the unit hash rate earnings on the Bitcoin network have repeatedly fallen below $0.05. Although there was a brief rebound during this period, it has now fallen back to a relatively low point.

Due to the deteriorating income situation, many inefficient miners have been forced to exit the market, leading to a significant decrease in Bitcoin hash rate. OKLink data shows that in the past two months, the total Bitcoin network hash rate has decreased by 15% from its peak, and it has been in a continuous decline for nearly a week.

At the same time that the hash rate is declining, the miner community has also increased its selling pressure, becoming one of the largest selling forces in the market. IntoTheBlock data shows that Bitcoin miners have sold over 50,000 Bitcoins cumulatively since the beginning of 2024, and the Bitcoin reserves held by miners have gradually fallen to an all-time low. Compared to previous cycles where miners were overly leveraged and tended to hold long-term, miners are now more focused on short-term gains. This may be related to the fact that as the hash rate is restructured, many listed companies have become important drivers for the scaling and mainstream development of the mining industry.

The compensation plan announced by the Mt. Gox trustee on June 24 also brought significant expectations of selling pressure. This is not the first time Mt. Gox has repaid debts, but it is the first time compensation has been made in the form of BTC and BCH. This means that once the compensation begins, a large amount of BTC and BCH will flow into the market. However, I believe that the selling pressure caused by the Mt. Gox compensation will be less than expected. The reasons are as follows:

The number of Bitcoins ultimately flowing into the market from this compensation is expected to be far less than 140,000. According to Alex Thorn, research director at Galaxy Digital, it is estimated to be only around 65,000;

After the compensation is completed, the selling pressure will be dispersed. Theoretically, creditors will not complete their sales simultaneously in a short period, and the market has already digested some of the selling pressure expectations brought by Mt. Gox. Therefore, the final impact will not be as large as imagined;

More importantly, considering the current stage of the market, rational creditors may be more inclined to continue holding rather than selling immediately.

Whether from the miner community or the potential selling pressure from Mt. Gox compensation, we believe that the impact on the crypto market is short-term and limited. Experience over the past decade tells us that despite numerous challenges, as the most solid consensus in the crypto market, the Bitcoin ecosystem always possesses strong market resilience and elasticity. Therefore, short-term selling pressure will not change the long-term trend, but rather enhance the Bitcoin ecosystem's adaptability to large-scale liquidity. Compared to short-term selling pressure, the current focus should be on the "bleak" situation of Bitcoin's on-chain transactions and liquidity.

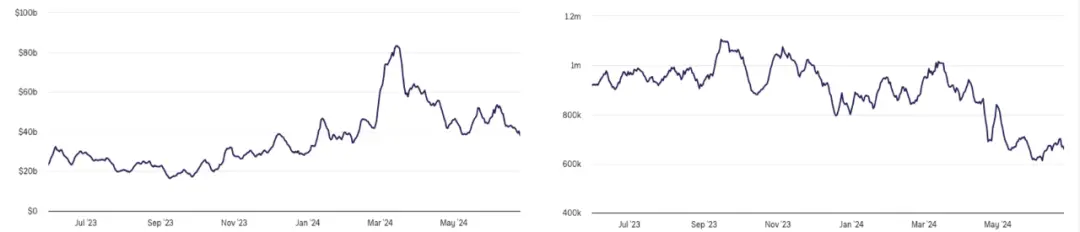

Although Bitcoin has performed poorly recently, it has still achieved over 40% positive returns since the beginning of the year, far exceeding most targets in traditional financial markets. However, after reaching an all-time high in March, the transaction volume on the Bitcoin network (left chart) has continued to decline. This is partly due to the waning popularity of inscriptions and runes, leading to reduced transaction demand, and partly because there has been no strong trading demand from either short-term speculators or long-term investors in the current price range, with on-chain turnover rates remaining at low levels.

The number of active addresses on-chain (right chart) has also seen a significant decline since March, with the number of active addresses currently below 700,000, down over 30% from the peak in 2024, and nearly on par with the same period in 2018.

In addition to the sluggish on-chain trading, Bitcoin spot ETFs have also performed relatively weakly recently. As the main channel for the crypto market to obtain external liquidity in the current cycle, Bitcoin spot ETFs are also an important vehicle supporting optimistic sentiment in the market. Previously, JPMorgan estimated that the net inflow of funds into the crypto market this year reached $12 billion, with about $16 billion net inflow into Bitcoin spot ETFs.

However, since entering June, Bitcoin spot ETFs have seen net outflows for several days, with nearly 20,000 Bitcoins flowing out from June 7 to now (as of June 25), amounting to approximately $1.228 billion at current prices. Such performance is unlikely to satisfy investors, and the "quiet" handling of seized Bitcoins by the German and U.S. governments has further tightened the market's already tense atmosphere.

Although the above data seems to prove that Bitcoin has fallen into a "predicament," there are also many positive signs in the market.

One of the key characteristics of previous cycles that truly reached a peak is a significant increase in the proportion of short-term holders (holding time less than 155 days), even dominating the market. This is because, during the peak, long-term holders gradually choose to take profits and exit, leading to the market being controlled by short-term investors and newcomers. However, according to OKLink data, the current Bitcoin market is still dominated by long-term holders, with Bitcoins held for less than six months accounting for less than 20%, a proportion far lower than that of short-term holders near the peaks of previous cycles. This market structure dominated by long-term holders provides stable support for Bitcoin in the current range, and considering that nearly 80% of the circulating Bitcoins are in profit, most investors are still in a favorable position. Therefore, the theoretical possibility of large-scale selling in the short term is unlikely.

On the other hand, Bitcoin reserves on exchanges also hit a new low in June. Although it is a low point, the low reserve status of exchanges actually releases a clear signal that the selling pressure on Bitcoin is not high. At the same time, the low reserves on exchanges also indicate that the Bitcoin market is in a period of rapid accumulation, although we do not fully understand the group structure of those taking Bitcoins away from exchanges.

Of course, the progress of the Ethereum spot ETF in the U.S. is also worth paying attention to. Although the correlation between Bitcoin and Ethereum has decreased, it remains above 0.8, indicating that the mutual influence between the two is very evident. If the Ethereum spot ETF officially launches trading in early July and can drive Ethereum to rebound again, Bitcoin may also gain some upward momentum from it.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles