Coinbase buys Circle? The harsh business reality of CEX behind the acquisition rumors

USDC is Coinbase's second largest source of revenue, but due to its partnership with Circle, the revenue attribution is limited. Circle controls the protocol layer and focuses on expanding the overall market value, while Coinbase wants to fully capture USDC to achieve revenue consolidation and protocol control. If Coinbase acquires Circle, it can gain complete revenue, product synergy, and regulatory advantages. In the long run, the acquisition is a reasonable and necessary strategic choice, with the key being the price.

USDC is Coinbase's second largest source of revenue, but due to its partnership with Circle, the revenue attribution is limited. Circle controls the protocol layer and focuses on expanding the overall market value, while Coinbase wants to fully capture USDC to achieve revenue consolidation and protocol control. If Coinbase acquires Circle, it can gain complete revenue, product synergy, and regulatory advantages. In the long run, the acquisition is a reasonable and necessary strategic choice, with the key being the price.Original Title: Coinbase Will Have to Acquire Circle -- The Only Question Is Price

Compiled by: zhouzhou, BlockBeats

Background

I have worked in the crypto industry for many years—first at CoinFund (an early-stage fund), and later joined Coinbase to help expand its venture capital strategy.

All content in this article is based on publicly available data: Circle's S-1 prospectus (April 2025) and Coinbase's public financial reports. There is no insider information—just analysis that anyone can replicate, although most people won't.

Breakdown of USDC Supply Structure

Total USDC = USDC held by Coinbase + USDC held by Circle + all other parts

According to the definition in the S-1, platform USDC refers to "the proportion of stablecoins held in custody products or wallet management services by a party." This means:

- Coinbase = Coinbase Prime / Exchange

- Circle = Circle Mint

- Others = USDC stored on platforms like Uniswap, Morpho, Phantom, etc.

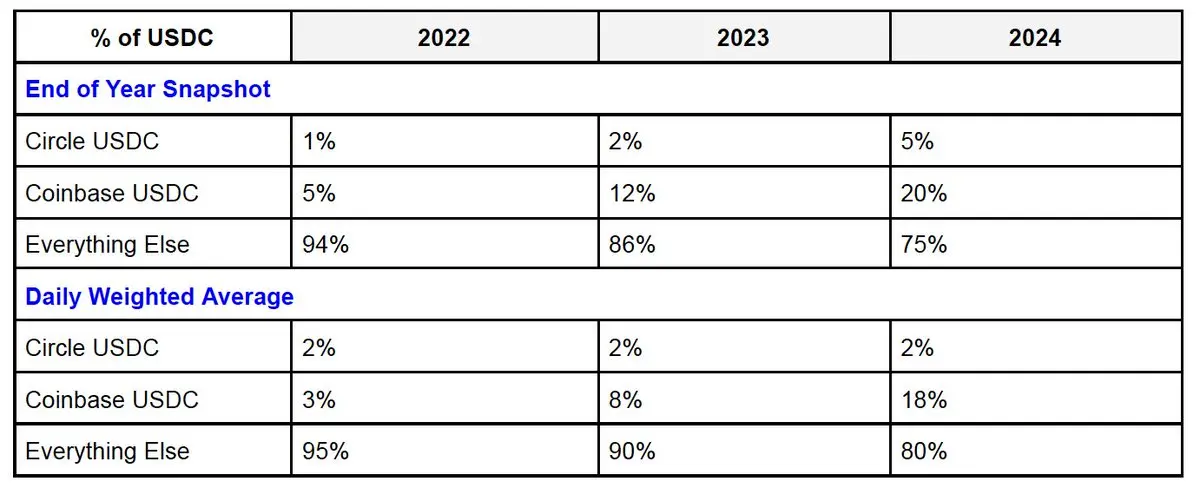

Coinbase's share of the total USDC supply is rapidly increasing—reaching about 23% in Q1 2025. Meanwhile, Circle's share remains stable.

This is reasonable—because Coinbase has a greater influence in the consumer, developer, and institutional markets.

USDC Revenue Attribution

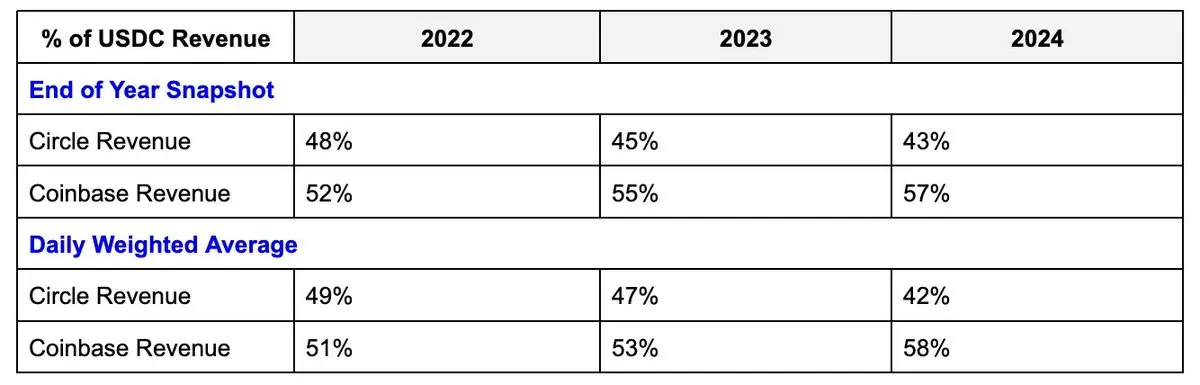

Both Circle and Coinbase can earn 100% of the income from USDC reserves on their platforms. For USDC "off-platform" (i.e., the "other parts"), both parties split the income 50/50.

But there is a key point: Circle derives a disproportionate amount of income from off-platform USDC. Although the amount of USDC on Coinbase's platform is four times that of Circle, its income advantage is only about 1.3 times.

Based on a rough calculation of the 50/50 split of income from the "other parts," the following revenue share situation is derived:

Circle: Betting on Market Size, Not Control

Circle's motivation is clear: to expand the overall circulation of USDC, even if these USDC are not stored on its own platform. Circle's ideal world is for USDC to become the leading stablecoin for the dollar—this alone can secure its strong market position. It benefits from being a protocol layer, such as:

- Issuing and maintaining the USDC smart contract across more than 19 chains;

- Controlling CCTP for native cross-chain and mint/burn liquidity.

While USDC on-platform is more profitable, its growth is not significant. In terms of large client expansion, Circle is likely losing out to Coinbase's scale. However, as long as USDC becomes the largest dollar stablecoin, Circle remains the winner—this is a game of market size, not profit margins.

The total market for USDC in the future could be astonishingly large, so even if it cannot capture all profits, it wouldn't be a bad outcome—most income growth will come from the "off-platform" portion. This motivation aligns with Circle's capabilities: it controls the governance, infrastructure, and technology roadmap of USDC.

Coinbase: Must Fully Control USDC

Macro Perspective

USDC is Coinbase's second-largest source of revenue, accounting for about 15% of total revenue in Q1 2025, surpassing staking business. More importantly, this is Coinbase's most stable and scalable infrastructure revenue source. As USDC expands globally, its potential will grow exponentially.

USDC will become Coinbase's key moat. While centralized exchange (CEX) revenue remains the mainstay, USDC revenue is comparatively more stable and will grow in sync with the overall crypto economy.

USDC is likely to become one of the top three dollar stablecoins, thus becoming a major channel for "tech exporting" the dollar globally. Fintech and traditional financial giants have already recognized this and are entering the market. However, USDC has the advantage of being first and the support of a native crypto ecosystem, making it likely to survive and continue to grow. From an infrastructure and regulatory perspective, fully owning it is a highly valuable story.

Micro Perspective: The Monetization Paradox of Coinbase

Coinbase is the main driver of USDC growth, but it is structurally constrained. Currently, USDC is Coinbase's second-largest revenue source (after trading). Therefore, every product decision must consider revenue and profit margins. The problem is: while Coinbase expands the market, it cannot fully control profits, as "off-platform" income can only be split in half.

Ironically, Coinbase attracts users, builds infrastructure, and increases trading frequency, yet due to structural issues, its revenue potential is capped. Its consumer and developer products have been "diluted" from the start.

Coinbase's natural response is to convert the "potential market" into "Coinbase USDC"—that is, the portion on-platform that can be fully monetized (the balance in custody products can earn 100% reserve income). This strategy has indeed been effective: the proportion of USDC on the Coinbase platform has quadrupled in two years. But this only applies to custody USDC, namely Exchange + Prime.

The problem lies in the "custody gray area"—user growth occurs here, but revenue attribution becomes unclear.

- Coinbase Wallet is non-custodial, and while Smart Wallet enhances the experience and may have introduced shared key mechanisms, it still does not meet the definition of "platform USDC" as defined in the S-1.

- If most users use on-chain products through such wallets in the future, the attribution of this portion of USDC will fall into a gray area between Circle and Coinbase.

- Base (Coinbase's L2) is also a non-custodial architecture, allowing users to exit to Ethereum L1 independently, and Coinbase does not hold the keys. Therefore, even if Coinbase is the entry point, USDC on Base is unlikely to be classified as "Coinbase USDC."

Conclusion: Coinbase has driven USDC growth but has built in a system that dilutes its benefits. As long as it does not control the entire protocol, it will always face uncertainty regarding revenue attribution. The only complete solution is to acquire Circle and rewrite the rules.

Benefits of Coinbase Acquiring Circle

- 100% Revenue Attribution: No more confusion over "custodial vs non-custodial," Coinbase can directly claim all interest income generated by the $60 billion USDC, regardless of where these USDC are held.

- Protocol Control: The USDC smart contracts, multi-chain integration, and CCTP will all become internal assets.

- Strategic Product Synergy: Wallets, Base, and future on-chain experience products can natively monetize USDC without coordination.

- Regulatory Integration: Coinbase is already a leader in policy-making, and by controlling USDC, it can lead the direction of stablecoin regulatory development.

Uncertainties / Points to Explore

- Growth Potential: USDC currently has a market cap of about $60 billion, theoretically capable of growing to $500 billion, corresponding to annual reserve income of $20 billion, potentially pushing Coinbase towards "Mag7" level profitability.

- Regulatory Policy: The U.S. is pushing for stablecoin legislation, which is good for market growth. Stablecoins will become a new vehicle for the globalization of the dollar, but it may also limit how platforms promote income or savings products. If Coinbase owns the entire stack, it can flexibly adjust strategies in response to policy changes.

- Operational Complexity: USDC was initially operated by a consortium, and the structure may have been based on legal/regulatory considerations at the time. While these obstacles may seem manageable under a unified structure, the legal structure may harbor unknown risks. However, at present, there are no insurmountable issues.

Acquisition Price

No one can accurately predict market valuation, but we can refer to the following data:

- Circle plans to IPO at a $5 billion valuation;

- Ripple previously proposed a $10 billion valuation;

- Coinbase's current market cap is about $70 billion;

- USDC currently accounts for 15% of Coinbase's revenue, and if integrated post-acquisition, there is a clear path to increase this proportion to over 30%.

My judgment is:

- Circle is a natural acquisition target for Coinbase, and Coinbase is well aware of this;

- Circle wants the public market to price itself (with a $5 billion target);

- Coinbase wants to see what valuation the market gives Circle;

- Coinbase knows full well:

- It must own the entire USDC stack;

- Post-integration, USDC could account for 15%-30% of its revenue;

- Based on revenue value, the "reasonable valuation" for USDC should be between $10 billion and $20 billion.

Circle is also aware of this—and realizes that as long as USDC continues to grow, Coinbase will ultimately choose to acquire it directly to resolve the ongoing business, product, and governance frictions in their collaboration.

Final Viewpoint

Coinbase should acquire Circle, and it is very likely to do so.

Currently, the cooperation between the two can continue, but in the long run, the conflicts at the platform, product, and governance levels are too significant to ignore. The market will set a price, but both parties already understand each other's value.

Risk warning

Risk warning Risk warning

Risk warning